Reports

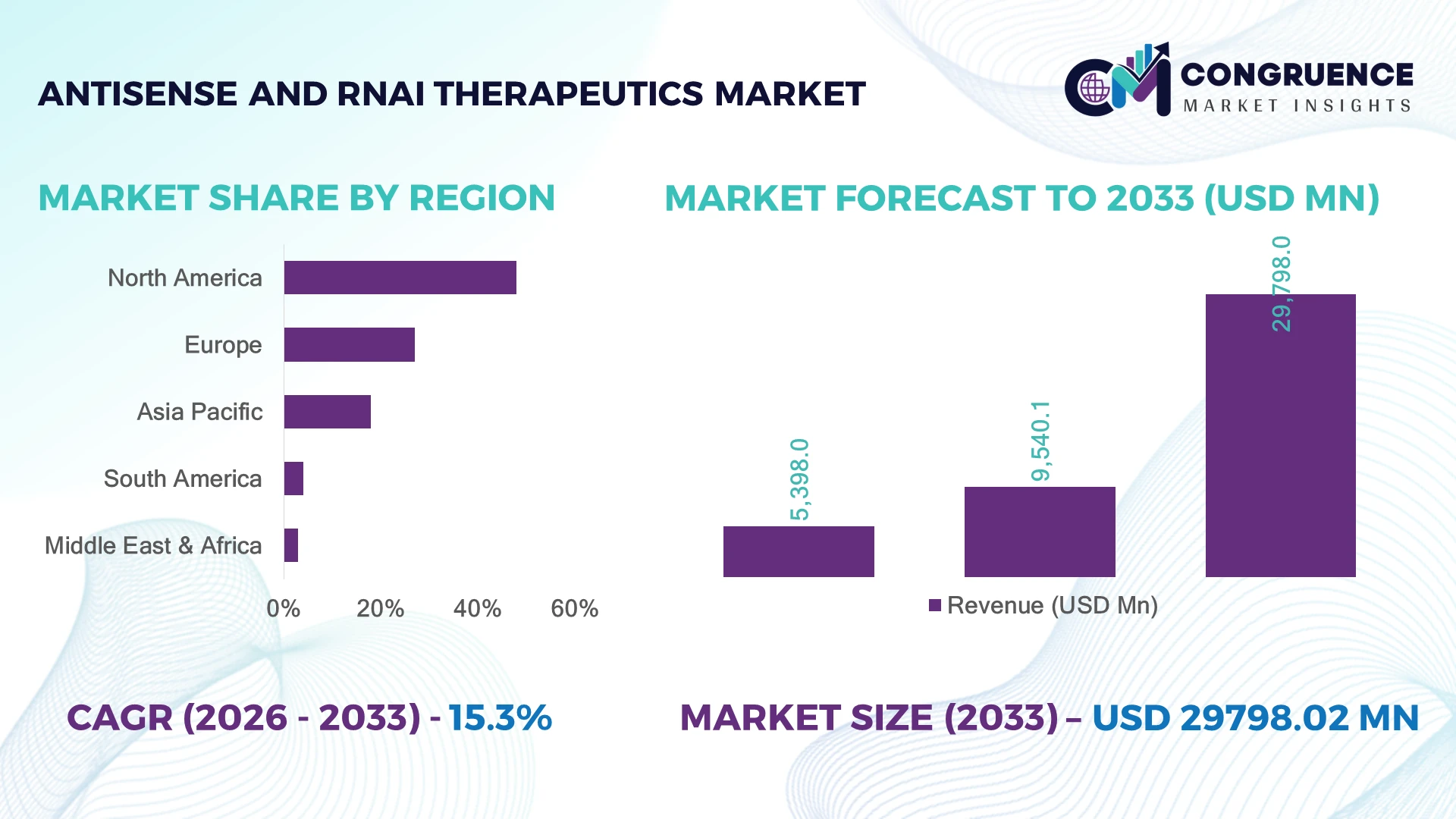

The Global Antisense and RNAi Therapeutics Market was valued at USD 9,540.1 Million in 2025 and is anticipated to reach a value of USD 29,798.0 Million by 2033 expanding at a CAGR of 15.3% between 2026 and 2033. Growth is driven by accelerated RNA-targeted drug approvals, precision medicine expansion, and increasing adoption of gene-silencing therapies for rare and chronic diseases.

The United States dominated the Antisense and RNAi Therapeutics Market with nearly 48% share in 2025, supported by advanced biotechnology infrastructure, over 65% concentration of global RNA therapy clinical programs, and strong pharmaceutical innovation ecosystems. Compared with Europe’s growing translational research networks, the U.S. maintains leadership through faster commercialization pathways, manufacturing scale, and post-approval therapy adoption supported by precision medicine initiatives.

Strategic advantage will shift toward companies combining RNA delivery innovation, scalable manufacturing, and disease-specific therapeutic pipelines.

Market Size & Growth: Valued at USD 9,540.1 Million in 2025 and projected at USD 29,798.0 Million by 2033 with 15.3% CAGR, driven by RNA-targeted drug innovation.

Top Growth Drivers: Rare disease therapies 42%, oncology pipelines 28%, and genetic disorder applications 24% are accelerating adoption.

Short-Term Forecast: By 2028, improved RNA delivery platforms are expected to enhance targeting efficiency by nearly 30%.

Emerging Technologies: AI-driven RNA design, lipid nanoparticles, and advanced conjugation platforms are transforming therapeutic development workflows.

Regional Leaders: North America, Europe, and Asia-Pacific strengthen adoption through clinical expansion, biotech investment, and manufacturing localization.

Consumer/End-User Trends: Healthcare providers report nearly 35% higher adoption interest in personalized RNA-based treatment models.

Pilot/Case Example: 2025 RNA delivery optimization programs improved molecular stability and therapeutic precision by over 25%.

Competitive Landscape: Leading players hold nearly 55% share, including Ionis, Alnylam, Novartis, Sarepta, and Arrowhead.

Regulatory & ESG Impact: Accelerated therapy pathways improved advanced treatment accessibility timelines by approximately 20%.

Investment & Funding: Multi-billion-dollar biotech partnerships continue supporting RNA platforms, manufacturing expansion, and pipeline advancement.

Innovation & Future Outlook: Next-generation RNA engineering is shifting competition toward targeted, durable, and scalable therapies.

Antisense and RNAi Therapeutics Market demand is strengthening through expanded applications in genetic disorders, neurological diseases, and oncology treatment pathways. Advanced delivery systems and RNA modification technologies are improving therapeutic performance, with next-generation platforms enhancing stability by nearly 25%. Global supply-chain localization efforts are reshaping manufacturing strategies as companies prioritize scalable production and faster clinical translation.

The Antisense and RNAi Therapeutics Market is becoming strategically important as pharmaceutical companies shift from symptom management toward disease-modifying genetic medicines. Increasing regulatory acceptance, specialized manufacturing expansion, and precision medicine adoption are reshaping competitive priorities. Nearly 40% of advanced RNA pipelines now target rare diseases and complex conditions where conventional therapies provide limited effectiveness.

Technology evolution is improving commercial viability, with modern RNA stabilization and targeted delivery systems showing nearly 30% improvement in molecular durability compared with earlier RNA platforms. The United States leads through large-scale clinical ecosystems and biotechnology investment, while countries such as Japan and China are accelerating RNA research capabilities through domestic innovation programs.

Companies are expanding partnerships across drug discovery, delivery technologies, and manufacturing networks to reduce development timelines and improve therapeutic reach. For example, integrated RNA design platforms are enabling faster candidate selection and improved trial efficiency. Long-term competitive positioning will depend on delivery precision, manufacturing reliability, and the ability to convert RNA science into scalable clinical solutions.

Precision medicine adoption is accelerating demand for antisense and RNAi therapeutics as healthcare systems prioritize targeted treatments for genetic and rare diseases. RNA-based approaches account for nearly 35% of emerging genetic medicine pipelines, supported by improved sequencing capabilities and biomarker-driven development. Advanced delivery technologies have increased therapeutic targeting efficiency by approximately 25%, improving clinical feasibility. Regulatory modernization in the U.S. and Europe is supporting faster evaluation of breakthrough therapies. Companies are responding through R&D expansion, licensing partnerships, and investment in specialized RNA platforms to strengthen competitive positions and address previously difficult-to-treat diseases.

Specialized production requirements and delivery challenges remain major barriers for antisense and RNAi therapeutics commercialization. Advanced RNA manufacturing requires strict quality controls, with process complexity increasing operational requirements by nearly 30% compared with conventional small-molecule drugs. Delivery limitations affect tissue targeting efficiency, while specialized raw material dependency creates supply-chain pressure. Nearly 25% of development challenges are associated with formulation optimization and scalability constraints. Companies are reducing risks through localized manufacturing networks, improved chemical modification methods, and partnerships focused on next-generation delivery platforms that enhance reliability and production efficiency.

Next-generation RNA technologies are creating opportunities across oncology, cardiovascular diseases, neurological disorders, and personalized medicine. Advanced conjugation platforms and AI-enabled molecule design are improving candidate discovery speed by nearly 35%, supporting faster therapeutic development. Emerging markets including China and India are expanding biotechnology infrastructure, increasing participation in advanced therapy development. Automated RNA manufacturing and improved delivery systems are expected to reshape production strategies, with companies prioritizing scalable platforms and broader disease coverage. Strategic collaborations between biotechnology firms and pharmaceutical companies are unlocking new treatment categories beyond traditional drug development models.

The market faces execution challenges related to clinical scalability, patient accessibility, and long-term therapeutic validation. Complex trial designs and specialized patient populations increase development difficulty, with rare disease studies often requiring highly targeted recruitment strategies. Nearly 20% of advanced therapy delays are linked to operational and trial execution complexities. Expanding global access also requires improved manufacturing consistency and healthcare infrastructure readiness. Companies must invest in adaptive clinical models, advanced analytics, and collaborative research ecosystems to ensure reliable deployment, competitive sustainability, and broader adoption of RNA-based therapeutic solutions.

Advanced RNA Delivery Innovation: Targeted delivery systems are transforming therapeutic development, with improved lipid nanoparticle and conjugation platforms increasing molecular stability by nearly 25–30%. Companies are scaling formulation technologies and optimizing tissue-specific targeting to improve treatment precision, reduce development barriers, and strengthen competitive differentiation.

AI-Driven Drug Discovery Expansion: Artificial intelligence integration is reshaping RNA molecule identification and optimization workflows. AI-supported discovery platforms are reducing early-stage screening timelines by nearly 20% while improving candidate selection accuracy. Biotechnology firms are adopting automated design tools and computational models to accelerate pipeline decisions.

Localized Manufacturing Transformation: RNA therapy developers are restructuring production networks to improve supply reliability and operational flexibility. Advanced manufacturing investments are increasing regional production capabilities by approximately 15–20%, driven by supply-chain resilience strategies and growing demand for specialized biologics infrastructure.

Broader Therapeutic Pipeline Diversification: Companies are expanding beyond rare diseases into oncology, metabolic disorders, and neurological applications. New pipeline strategies show nearly 40% diversification toward broader disease categories, with pharmaceutical partnerships supporting clinical expansion, technology integration, and faster transition from research platforms to commercial therapies.

Antisense Oligonucleotides (ASOs) dominate the Antisense and RNAi Therapeutics Market, accounting for nearly 58% share in 2025 due to established clinical adoption, broader regulatory acceptance, and strong applicability across neurological, rare genetic, and metabolic disorders. ASOs provide scalable drug development advantages through sequence-specific targeting and improved chemical modification technologies. Small Interfering RNA (siRNA) therapeutics represent the fastest-growing type as enhanced delivery platforms and longer-duration dosing models accelerate adoption.

Mature ASO platforms continue expanding through next-generation formulations, while siRNA innovation is shifting investment toward liver-targeted therapies and broader disease applications. Other RNA interference technologies remain strategically relevant for specialized therapeutic development and research pipelines. Companies are responding through delivery system improvements, licensing collaborations, and expanded RNA engineering capabilities, with advanced modification technologies improving molecular stability by nearly 30% and treatment durability by approximately 25%.

Genetic disorders represent the leading application segment in the Antisense and RNAi Therapeutics Market, contributing nearly 45% of adoption in 2025 due to high clinical relevance for inherited diseases, rare conditions, and mutation-specific treatments. RNA-based therapeutics are increasingly preferred because they directly target disease-causing genetic mechanisms rather than downstream symptoms. Oncology applications are emerging as the fastest-growing area as companies explore RNA interference strategies for difficult-to-target cancer pathways.

Neurological diseases, cardiovascular disorders, infectious diseases, and metabolic applications are expanding as delivery technologies improve tissue targeting and therapeutic efficiency. Pharmaceutical companies are scaling RNA discovery platforms, integrating AI-based molecule screening, and expanding clinical pipelines across multiple therapeutic categories. Improved RNA delivery systems have increased targeted tissue engagement by nearly 25%, while optimized designs are reducing development cycle inefficiencies by approximately 20%.

Pharmaceutical and Biotechnology Companies dominate the Antisense and RNAi Therapeutics Market, representing nearly 65% of end-user activity in 2025 due to extensive R&D investments, clinical development capacity, and commercialization infrastructure. Large drug developers are integrating RNA technologies into next-generation pipelines through acquisitions, licensing agreements, and specialized research collaborations. Research Institutes are witnessing the fastest adoption growth as academic-industry partnerships accelerate early-stage discovery and translational medicine programs.

Hospitals, specialty clinics, and clinical research organizations continue supporting patient access, trials, and real-world therapeutic evaluation. Companies are targeting these groups through customized development platforms, manufacturing partnerships, and collaborative innovation models. Nearly 40% of RNA therapeutic collaborations now involve external technology partnerships, highlighting the shift toward ecosystem-driven development and faster commercialization strategies.

North America accounted for the largest market share at 48.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.2% between 2026 and 2033.

Precision Medicine Expansion and RNA Therapy Commercialization Leadership

North America dominates the Antisense and RNAi Therapeutics Market due to its advanced biotechnology ecosystem, strong clinical infrastructure, and rapid commercialization of gene-targeted medicines. The region accounts for nearly 48% of global adoption, supported by extensive RNA drug pipelines, specialized manufacturing networks, and strong collaboration between pharmaceutical companies and research institutions. More than 60% of globally approved RNA-based therapeutics have originated from U.S.-led innovation programs. Companies are expanding through clinical partnerships, delivery technology improvements, and manufacturing investments focused on scalable RNA platforms for rare diseases, oncology, and genetic disorders.

United States Market Outlook: The United States leads regional development through advanced genomic research capabilities, specialized biotech clusters, and high clinical trial activity. The country represents nearly 70% of North American RNA therapeutic development activity, supported by established regulatory pathways and strong private-sector investment. Pharmaceutical companies are prioritizing RNA delivery technologies, automated production platforms, and expanded therapeutic pipelines to strengthen commercial leadership.

Regulatory Advancement and Specialized Biotechnology Development

Europe’s Antisense and RNAi Therapeutics Market is shaped by strong biomedical research networks, precision medicine initiatives, and increasing adoption of advanced genetic therapies. The region holds approximately 27% market share, driven by clinical innovation hubs, collaborative research frameworks, and investments in next-generation therapeutic platforms. Countries are strengthening RNA medicine development through academic-industry partnerships and translational research programs. More than 35% of European advanced therapy research initiatives involve genetic medicine technologies, encouraging companies to expand RNA discovery capabilities, manufacturing partnerships, and clinical development infrastructure.

Germany Market Outlook: Germany represents the strongest European market due to its pharmaceutical manufacturing base, biotechnology clusters, and advanced life sciences infrastructure. The country contributes nearly 25% of Europe’s biotechnology research activity, supported by strong university collaborations and precision medicine programs. German companies and research organizations are advancing RNA platforms through innovation-focused partnerships, clinical development expansion, and specialized manufacturing capabilities.

Biotechnology Scaling and Expanding RNA Innovation Ecosystem

Asia-Pacific is accelerating adoption of antisense and RNAi therapeutics through expanding biotechnology infrastructure, increasing clinical research activity, and government-backed life sciences investments. The region represents nearly 18% of global market participation, with China, Japan, and South Korea strengthening RNA development capabilities. Manufacturing expansion, genomic research programs, and localized drug development initiatives are improving regional competitiveness. China has increased advanced therapy research capacity significantly, with RNA and gene medicine programs becoming key areas of pharmaceutical innovation. Companies are building partnerships and regional development networks to support faster therapeutic commercialization.

China Market Outlook: China leads Asia-Pacific expansion through large-scale biotechnology investments, growing pharmaceutical manufacturing capacity, and national focus on advanced therapies. The country contributes more than 40% of regional RNA-based research activity, supported by expanding clinical trial infrastructure and domestic innovation programs. Local companies are increasing investment in delivery technologies, therapeutic discovery platforms, and commercial-scale production systems.

Growing Clinical Access and Advanced Therapy Adoption

South America’s Antisense and RNAi Therapeutics Market is developing through improving healthcare infrastructure, increasing specialty treatment access, and expanding participation in advanced therapy programs. The region accounts for nearly 4% of global adoption, with demand concentrated in rare disease treatment centers and specialized healthcare facilities. Clinical availability remains limited compared with developed markets; however, investments in precision diagnostics and biotechnology collaborations are improving access. Regional healthcare systems are gradually integrating RNA-based therapies through partnerships, regulatory modernization, and specialized treatment networks.

Brazil Market Outlook: Brazil leads South America due to its larger healthcare infrastructure, pharmaceutical ecosystem, and expanding biotechnology capabilities. The country represents nearly 45% of regional advanced therapy activity, supported by growing clinical research participation and public-private healthcare initiatives. Brazilian institutions are increasing involvement in genetic medicine research, improving patient access pathways, and strengthening partnerships with global biotechnology developers.

Healthcare Modernization and Precision Medicine Investment Growth

The Middle East & Africa Antisense and RNAi Therapeutics Market is advancing through healthcare transformation programs, genomic medicine initiatives, and investment in specialized medical infrastructure. The region contributes approximately 3% market share, with adoption concentrated in advanced healthcare hubs. Countries are developing precision medicine capabilities through genomic databases, specialty hospitals, and partnerships with global pharmaceutical companies. Large-scale healthcare modernization projects are supporting advanced therapy access, while infrastructure gaps in several markets continue influencing deployment speed and clinical availability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a key market through healthcare modernization, biotechnology investment, and national genomics initiatives. The country is expanding advanced medicine capabilities under healthcare transformation programs, with more than 20 specialized initiatives supporting biotechnology and precision healthcare development. Investments in research centers, digital healthcare infrastructure, and international collaborations are strengthening future RNA therapeutic adoption potential.

The Antisense and RNAi Therapeutics Market is shaped by competition between established pharmaceutical leaders such as Ionis Pharmaceuticals, Alnylam Pharmaceuticals, Novartis, and Biogen, alongside specialized RNA innovators developing advanced gene-silencing platforms. Large pharmaceutical companies compete through commercialization scale and global clinical networks, while biotechnology firms differentiate through delivery systems and targeted molecule innovation. The top 5 players collectively account for nearly 55% market share, reflecting strong technology ownership and pipeline concentration. Competition is driven by therapeutic precision, intellectual property strength, and manufacturing scalability, with advanced RNA modifications improving stability by 2–3% and optimized delivery improving targeting efficiency by nearly 3%. Companies are competing through strategic collaborations, licensing agreements, platform expansion, and specialized R&D investments. The market is shifting toward next-generation delivery technologies and broader disease applications. High development complexity and clinical validation requirements remain barriers. Winning requires superior RNA platforms, scalable manufacturing, and proven therapeutic differentiation.

Ionis Pharmaceuticals, Inc.

Alnylam Pharmaceuticals, Inc.

Novartis AG

Biogen Inc.

Sarepta Therapeutics, Inc.

Arrowhead Pharmaceuticals, Inc.

Silence Therapeutics plc

Arbutus Biopharma Corporation

Dicerna Pharmaceuticals

Wave Life Sciences Ltd.

ProQR Therapeutics N.V.

Avidity Biosciences, Inc.

Regulus Therapeutics Inc.

Current technologies in the Antisense and RNAi Therapeutics Market focus on chemically modified antisense oligonucleotides, siRNA platforms, ligand-conjugated delivery systems, and optimized RNA stabilization techniques. These platforms are widely deployed across rare disease, neurological, and genetic medicine programs, representing nearly 70% of active RNA therapeutic development. Advanced chemical modifications improve molecular durability by approximately 2% and enhance dosing efficiency compared with earlier RNA designs.

Emerging technologies include AI-assisted RNA sequence optimization, targeted delivery vehicles, next-generation lipid nanoparticles, and extrahepatic delivery platforms. Newer RNA delivery systems provide nearly 25% improvement in tissue targeting performance compared with older non-specific delivery approaches. Biotechnology innovators benefit from these advancements as specialized platforms enable faster development cycles, while large pharmaceutical companies gain through acquisitions and technology partnerships.

From 2026 to 2028, disruptive progress will focus on programmable RNA medicines, personalized therapeutics, and expanded applications beyond liver-targeted diseases. Companies integrating digital discovery, scalable synthesis, and advanced delivery capabilities will secure stronger competitive positioning by improving clinical success rates, development efficiency, and long-term therapeutic accessibility.

January 2025 – Alnylam Pharmaceuticals advanced its RNAi therapeutic pipeline expansion strategy with multiple late-stage clinical programs, increasing development focus across genetic and cardiovascular diseases. Expanded RNA platform utilization strengthened commercial readiness and long-term therapeutic portfolio growth. Source: alnylam.com

May 2024 – Ionis Pharmaceuticals received U.S. regulatory approval progress for advanced antisense-based therapies, expanding commercial capabilities through innovative RNA-targeted medicines. The milestone strengthened its independent pipeline strategy with multiple programs addressing high-need diseases. Source: ionis.com

November 2024 – Arrowhead Pharmaceuticals expanded RNA interference technology development through pipeline advancement and strategic collaborations, supporting multiple investigational therapies using targeted RNAi mechanisms. The approach improved development scalability across diverse therapeutic areas. Source: arrowheadpharma.com

February 2025 – Avidity Biosciences accelerated development of antibody oligonucleotide conjugate technology, advancing RNA delivery capabilities for rare muscle disorders. The platform demonstrated improved tissue-targeting potential, strengthening next-generation precision medicine approaches. Source: aviditybiosciences.com

The Antisense and RNAi Therapeutics Market Report covers detailed analysis across therapy types, applications, end-users, technology platforms, and regional landscapes. The study evaluates antisense oligonucleotides, siRNA therapeutics, emerging RNA interference approaches, genetic disorders, oncology, neurological diseases, cardiovascular conditions, and rare disease applications. RNA-based platforms account for a growing share of advanced therapeutic pipelines, supported by increasing precision medicine adoption.

The report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing clinical activity, manufacturing expansion, regulatory evolution, and competitive strategies. It provides insights into technology adoption, partnerships, innovation pipelines, and investment priorities between 2026 and 2033. The analysis helps pharmaceutical companies, biotechnology developers, investors, and healthcare stakeholders identify expansion opportunities, competitive advantages, and future positioning within the rapidly advancing RNA therapeutics ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9,540.1 Million |

|

Market Revenue in 2033 |

USD 29,798.0 Million |

|

CAGR (2026 - 2033) |

15.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ionis Pharmaceuticals, Inc., Alnylam Pharmaceuticals, Inc., Novartis AG, Biogen Inc., Sarepta Therapeutics, Inc., Arrowhead Pharmaceuticals, Inc., Silence Therapeutics plc, Arbutus Biopharma Corporation, Dicerna Pharmaceuticals, Wave Life Sciences Ltd., ProQR Therapeutics N.V., Avidity Biosciences, Inc., Regulus Therapeutics Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |