Reports

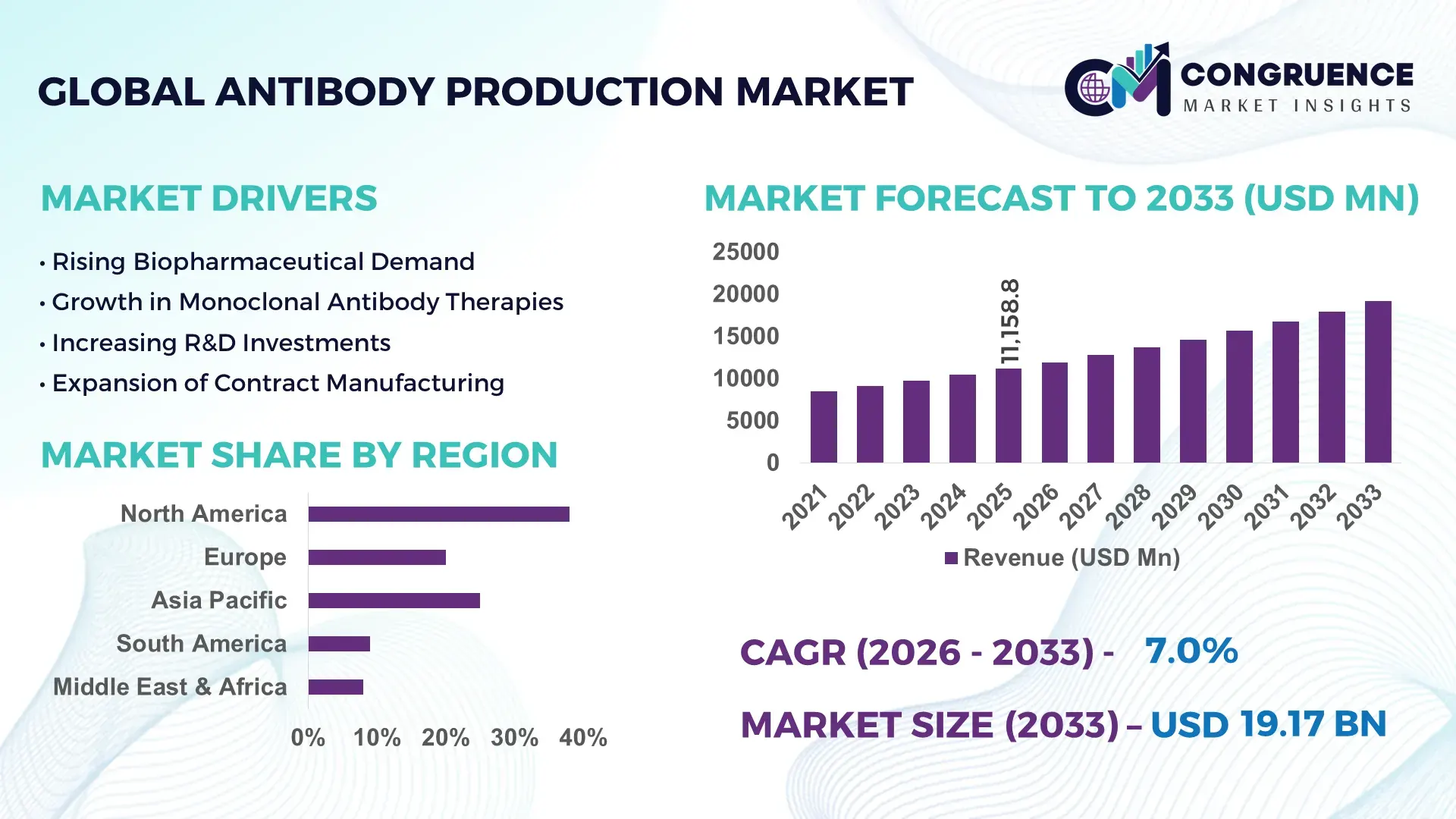

The Global Antibody Production Market was valued at USD 11158.76 Million in 2025 and is anticipated to reach a value of USD 19172.84 Million by 2033 expanding at a CAGR of 7% between 2026 and 2033. This growth is primarily driven by the increasing global demand for targeted biologics and precision therapeutics across oncology and autoimmune disease segments.

The United States continues to demonstrate substantial advancements in antibody production infrastructure, supported by over 1,200 active biopharmaceutical manufacturing facilities and continuous capital investments exceeding USD 25 billion annually in biologics development. The country has integrated large-scale mammalian cell culture systems, enabling production capacities exceeding 20,000 liters per batch in advanced facilities. Additionally, monoclonal antibodies account for nearly 60% of biologics pipelines in the U.S., with extensive applications in cancer immunotherapy, infectious disease management, and chronic inflammatory disorders. Adoption of single-use bioreactors has increased by over 45% among major manufacturers, significantly improving production flexibility and reducing contamination risks.

Market Size & Growth: USD 11158.76 Million in 2025, projected to reach USD 19172.84 Million by 2033, growing at 7% CAGR driven by rising biologics demand and precision medicine expansion.

Top Growth Drivers: Biopharmaceutical demand growth (38%), monoclonal antibody adoption (42%), R&D investment increase (35%).

Short-Term Forecast: By 2028, production efficiency is expected to improve by 30% due to automation and AI-based bioprocess optimization.

Emerging Technologies: Single-use bioreactors, CRISPR-based cell line engineering, continuous bioprocessing systems.

Regional Leaders: North America projected at USD 7.5 billion by 2033 with strong biologics pipelines; Europe at USD 5.2 billion driven by biosimilars adoption; Asia-Pacific at USD 4.8 billion with rapid contract manufacturing expansion.

Consumer/End-User Trends: Pharmaceutical and biotechnology companies contribute over 70% of demand, with increasing outsourcing to contract manufacturing organizations.

Pilot or Case Example: In 2024, a European biotech firm improved antibody yield by 28% using continuous perfusion bioreactor systems.

Competitive Landscape: Leading player holds approximately 18% share, followed by major companies including Lonza, Thermo Fisher Scientific, Merck KGaA, Sartorius AG, and Danaher Corporation.

Regulatory & ESG Impact: Regulatory frameworks are promoting biologics safety compliance, while firms target 25% reduction in single-use plastic waste by 2030.

Investment & Funding Patterns: Over USD 18 billion invested globally in biologics manufacturing expansion and innovation platforms in recent years.

Innovation & Future Outlook: Integration of AI-driven bioprocess analytics and modular manufacturing units is reshaping scalable antibody production.

The antibody production market is evolving across diverse industry sectors, with oncology applications contributing nearly 45% of total demand, followed by autoimmune diseases at approximately 25% and infectious diseases at 15%. Continuous innovation in recombinant DNA technology and hybridoma techniques has enhanced antibody specificity and yield efficiency. Regulatory frameworks are increasingly emphasizing Good Manufacturing Practices (GMP) compliance, driving investments in advanced cleanroom facilities and automated quality control systems. Regionally, Asia-Pacific is witnessing accelerated consumption due to expanding healthcare infrastructure and rising biosimilar production, while Europe continues to lead in sustainable manufacturing practices. Emerging trends such as bispecific antibodies, antibody-drug conjugates, and personalized immunotherapy are expected to redefine future production strategies, creating new avenues for scalability and cost optimization.

The antibody production market holds strategic significance within the global biopharmaceutical ecosystem, as it underpins the development of next-generation therapeutics, including monoclonal antibodies, bispecific antibodies, and antibody-drug conjugates. Advanced technologies such as continuous bioprocessing deliver nearly 35% higher productivity compared to traditional batch processing systems, enabling faster turnaround times and reduced operational costs. North America dominates in production volume, while Asia-Pacific leads in adoption, with over 55% of emerging biotech firms leveraging contract manufacturing services to scale antibody production efficiently.

By 2028, artificial intelligence-driven process optimization is expected to reduce production downtime by approximately 25%, while improving yield consistency across large-scale manufacturing facilities. Companies are increasingly aligning with ESG commitments by targeting a 30% reduction in carbon emissions and transitioning toward recyclable single-use systems by 2030. These sustainability-driven initiatives are becoming critical differentiators in regulatory approvals and investor evaluations.

In 2024, a leading biopharmaceutical company in Germany achieved a 32% increase in production efficiency through the integration of automated perfusion systems and predictive analytics, demonstrating the tangible benefits of digital transformation in antibody manufacturing. Additionally, global supply chain diversification strategies are being implemented to mitigate risks associated with raw material shortages and geopolitical disruptions. As precision medicine continues to expand, the antibody production market is poised to serve as a foundational pillar for resilient healthcare systems, ensuring scalable, compliant, and sustainable biologics manufacturing pathways while supporting innovation-driven growth across therapeutic domains.

The increasing demand for targeted biologics, particularly monoclonal antibodies, is a primary driver of the antibody production market. Monoclonal antibodies now account for more than 50% of newly approved biologic drugs, reflecting their effectiveness in treating complex diseases such as cancer and autoimmune disorders. The global oncology pipeline includes over 1,500 antibody-based therapeutics currently under development, highlighting strong future demand. Furthermore, advancements in antibody engineering have improved binding specificity by up to 60%, enhancing therapeutic efficacy and reducing side effects. The rapid expansion of personalized medicine is also contributing to higher antibody consumption, as therapies are increasingly tailored to individual patient profiles. Pharmaceutical companies are expanding manufacturing capacities and investing in high-throughput screening technologies to meet this growing demand, thereby accelerating market expansion and technological innovation.

Despite strong growth prospects, high production costs and complex manufacturing processes remain significant restraints for the antibody production market. The cost of developing a monoclonal antibody can exceed USD 1 billion, largely due to expensive raw materials, stringent regulatory requirements, and lengthy development timelines. Bioreactor systems, purification processes, and quality assurance protocols require highly specialized infrastructure and skilled personnel, increasing operational expenses. Additionally, maintaining sterile environments and complying with Good Manufacturing Practices (GMP) adds further cost burdens. Production failures or contamination events can lead to losses exceeding millions of dollars per batch. Smaller biotechnology firms often face financial constraints, limiting their ability to scale production independently, which in turn restricts overall market accessibility and slows innovation in certain segments.

The expansion of biosimilars and increasing demand from emerging markets present significant growth opportunities for the antibody production market. Biosimilars are expected to account for nearly 35% of biologics consumption in developing regions, driven by cost-effectiveness and improved healthcare access. Countries in Asia-Pacific and Latin America are investing heavily in local manufacturing infrastructure, with several governments offering incentives and subsidies to encourage domestic biologics production. The adoption of single-use technologies has reduced setup costs by up to 40%, enabling smaller facilities to enter the market. Additionally, partnerships between global pharmaceutical companies and regional manufacturers are facilitating technology transfer and capacity building. These developments are creating new revenue streams and expanding the global footprint of antibody production, particularly in underserved healthcare markets.

Regulatory complexity and supply chain disruptions pose critical challenges to the antibody production market. Stringent regulatory approvals require extensive clinical validation, quality testing, and documentation, often extending product development timelines by several years. Differences in regulatory standards across regions further complicate global market entry. Additionally, the supply chain for raw materials, including cell culture media and reagents, is highly sensitive to geopolitical factors and manufacturing bottlenecks. During recent global disruptions, shortages of critical inputs led to production delays of up to 20% in several facilities. Cold chain logistics for antibody storage and transportation add another layer of complexity, requiring specialized infrastructure and increasing operational risks. Addressing these challenges requires coordinated efforts across stakeholders, investment in supply chain resilience, and harmonization of regulatory frameworks.

• Rapid Adoption of Single-Use Bioreactors Enhancing Production Efficiency: The global antibody production market is witnessing a strong shift toward single-use bioreactors, with over 65% of new biologics manufacturing facilities integrating disposable systems to streamline operations. These systems have demonstrated up to 40% reduction in cleaning and validation time while lowering contamination risks by nearly 30%. Additionally, manufacturing flexibility has improved by 50%, enabling faster batch turnaround and reduced downtime. North America and Europe account for more than 70% of installations, while Asia-Pacific adoption is increasing at a pace exceeding 25% annually, driven by expanding contract manufacturing demand.

• Expansion of Continuous Bioprocessing Improving Yield Output: Continuous bioprocessing technologies are gaining traction, with approximately 48% of large-scale antibody manufacturers transitioning from batch to perfusion-based systems. These advanced systems have improved antibody yield by 35% to 45% compared to traditional batch methods, while reducing production timelines by nearly 20%. The integration of real-time monitoring and automation tools has enhanced process consistency by over 30%. Leading pharmaceutical firms report that continuous manufacturing has increased facility utilization rates to above 85%, significantly optimizing operational efficiency.

• Integration of AI and Digital Bioprocessing Platforms Accelerating Optimization: Artificial intelligence and digital twins are being increasingly deployed in antibody production, with nearly 52% of manufacturers implementing AI-driven analytics for process optimization. These technologies have improved predictive maintenance accuracy by 28% and reduced process deviations by 22%. AI-enabled platforms are also enhancing yield forecasting accuracy by over 35%, enabling better resource planning and inventory management. The adoption of cloud-based manufacturing execution systems has increased by 45%, particularly among large biopharma companies seeking scalable and data-driven production environments.

• Growing Demand for Bispecific and Next-Generation Antibodies: The market is experiencing a significant rise in next-generation antibody formats, with bispecific antibodies accounting for over 18% of clinical pipelines in 2025, up from 10% in 2020. Antibody-drug conjugates (ADCs) have shown efficacy improvements of up to 60% in targeted cancer therapies, driving increased investment and production focus. Over 70 new bispecific antibody candidates are currently in late-stage development, reflecting strong innovation momentum. This trend is further supported by a 33% increase in R&D collaborations between biotech firms and academic institutions, accelerating the commercialization of advanced antibody therapies.

The antibody production market is segmented based on type, application, and end-user, each contributing distinctively to the overall industry structure. Monoclonal antibodies dominate the type segment due to their high specificity and widespread therapeutic use, while polyclonal and recombinant antibodies serve niche and research-driven applications. In terms of application, therapeutic use leads the market, accounting for a significant proportion of antibody demand driven by oncology and autoimmune disease treatments. Diagnostic applications are also expanding steadily with increasing demand for precision testing. From an end-user perspective, pharmaceutical and biotechnology companies represent the largest segment, supported by robust R&D pipelines and manufacturing investments, while academic and research institutions contribute to early-stage innovation. The segmentation reflects a balanced interplay between commercial-scale production and research-oriented demand, shaping the competitive and technological landscape of the market.

Monoclonal antibodies represent the leading segment in the antibody production market, accounting for approximately 62% of total adoption due to their high specificity, scalability, and widespread use in therapeutic applications. In comparison, polyclonal antibodies hold around 18% share, primarily used in research and diagnostic applications, while recombinant antibodies contribute nearly 20% due to their consistency and customization capabilities. Although monoclonal antibodies dominate, recombinant antibodies are emerging as the fastest-growing segment with an expected CAGR of 9.5%, driven by advancements in genetic engineering and increasing demand for reproducible results in research and clinical applications.

Polyclonal antibodies continue to play a critical role in niche applications such as immunoassays and protein detection, benefiting from their ability to recognize multiple epitopes, which enhances sensitivity by nearly 25% in certain assays. Meanwhile, recombinant antibody technologies are gaining traction due to their ability to reduce batch variability by over 30% and improve production efficiency through optimized expression systems.

Therapeutic applications dominate the antibody production market, accounting for approximately 58% of total usage, largely driven by the growing prevalence of cancer and autoimmune diseases. Diagnostic applications hold around 27% share, supported by the increasing adoption of antibody-based diagnostic kits for infectious diseases and chronic conditions. Research applications contribute the remaining 15%, focusing on drug discovery and molecular biology studies.

While therapeutics lead in adoption, diagnostic applications are emerging as the fastest-growing segment with a CAGR of 8.2%, fueled by advancements in point-of-care testing and rapid diagnostic technologies. Antibody-based diagnostics have improved detection sensitivity by up to 40%, enabling earlier disease identification and improved patient outcomes. Additionally, the integration of biosensors and microfluidic systems is enhancing diagnostic accuracy and reducing processing time by nearly 35%.

Pharmaceutical and biotechnology companies represent the leading end-user segment in the antibody production market, accounting for approximately 68% of total demand, driven by extensive biologics pipelines and large-scale manufacturing capabilities. Contract research and manufacturing organizations (CROs and CMOs) hold around 20% share, reflecting the growing trend of outsourcing production to reduce costs and improve scalability. Academic and research institutions contribute approximately 12%, focusing on early-stage research and innovation.

Among these, CROs and CMOs are the fastest-growing segment, with an estimated CAGR of 10.1%, supported by increasing outsourcing activities and the need for flexible manufacturing solutions. These organizations have improved production turnaround times by nearly 35% and reduced operational costs for clients by up to 25%. Pharmaceutical companies, while dominant, are increasingly partnering with external service providers to enhance capacity and accelerate time-to-market.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America maintains strong dominance with over 1,000 biologics manufacturing facilities and more than 60% of global monoclonal antibody production capacity concentrated in the United States and Canada. Europe follows with approximately 27% share, supported by over 350 biopharmaceutical companies and increasing biosimilar approvals across Germany, the UK, and France. Asia-Pacific accounts for nearly 25% of the market, with China and India collectively contributing over 45% of regional production volume due to expanding contract manufacturing infrastructure. South America holds around 6% share, with Brazil representing over 55% of regional demand. The Middle East & Africa region contributes close to 4%, driven by healthcare infrastructure investments exceeding USD 5 billion in the past five years. Across all regions, increasing adoption of single-use technologies, which now represent over 50% of new installations globally, is significantly enhancing production flexibility and reducing operational costs by up to 30%.

How are advanced biologics manufacturing ecosystems accelerating innovation and scalability?

North America accounts for approximately 38% of the global antibody production market, supported by a highly developed biopharmaceutical industry and extensive R&D infrastructure. The region hosts over 70% of global clinical trials involving antibody-based therapies, with oncology and immunology sectors driving more than 65% of demand. Regulatory frameworks such as accelerated biologics approval pathways and strong government funding exceeding USD 10 billion annually for life sciences research continue to strengthen market growth. Technological advancements, including AI-enabled bioprocessing and automation, have improved production efficiency by nearly 30% across large-scale facilities. A notable example includes a leading U.S.-based biopharmaceutical company expanding its single-use bioreactor capacity by over 40% in 2024 to meet rising demand for monoclonal antibodies. Consumer behavior in this region reflects high enterprise adoption, with over 75% of pharmaceutical firms leveraging digital manufacturing solutions to enhance productivity and ensure regulatory compliance.

What role do sustainability-driven regulations and biosimilar expansion play in shaping industry demand?

Europe holds approximately 27% share of the global antibody production market, with key markets including Germany, the United Kingdom, and France contributing over 65% of regional output. The region is characterized by stringent regulatory oversight and strong emphasis on sustainable manufacturing practices, with more than 50% of facilities adopting environmentally friendly production systems to reduce emissions and waste. Regulatory bodies have implemented guidelines promoting biosimilar development, leading to a 35% increase in biosimilar approvals over the past five years. Technological adoption is also significant, with over 45% of manufacturers integrating continuous bioprocessing systems to enhance efficiency. A prominent European life sciences company expanded its biologics manufacturing footprint in 2024, increasing production capacity by 25% to support growing demand for antibody therapeutics. Consumer behavior reflects a preference for compliant and transparent production methods, with regulatory pressure driving the adoption of explainable and traceable antibody production processes across the region.

How is rapid industrial expansion and contract manufacturing transforming production capabilities?

Asia-Pacific represents approximately 25% of the global antibody production market and ranks as the fastest-growing region in terms of production expansion. China, India, and Japan collectively account for over 70% of regional demand, with China alone contributing nearly 40% of manufacturing volume. The region has witnessed a 50% increase in contract manufacturing facilities over the past five years, significantly enhancing production scalability. Infrastructure development, including large-scale bioparks and innovation hubs, has supported over 200 new biologics manufacturing projects. Technological advancements such as automated cell culture systems and AI-driven analytics have improved production efficiency by 20% to 30%. A leading Chinese biotechnology firm expanded its antibody production capacity by over 35% in 2024, reflecting strong domestic demand. Consumer behavior in this region is driven by cost-effective manufacturing and growing adoption of biosimilars, with over 60% of pharmaceutical companies outsourcing production to specialized contract manufacturers.

What factors are influencing gradual expansion and regional manufacturing capabilities?

South America accounts for approximately 6% of the global antibody production market, with Brazil and Argentina representing over 70% of regional demand. The region is experiencing gradual growth supported by increasing investments in healthcare infrastructure and local manufacturing capabilities. Government incentives, including tax benefits and funding programs, have encouraged domestic production, leading to a 20% increase in biologics manufacturing facilities over recent years. Infrastructure development in energy and logistics sectors has improved supply chain efficiency by nearly 15%, supporting antibody production operations. A Brazilian biopharmaceutical company has recently enhanced its production capabilities by integrating automated purification systems, improving yield efficiency by 18%. Consumer behavior in this region is influenced by localized healthcare needs, with growing demand for cost-effective biologics and biosimilars driving adoption across public healthcare systems.

How are healthcare investments and modernization initiatives driving emerging demand patterns?

The Middle East & Africa region contributes approximately 4% to the global antibody production market, with major growth observed in the UAE, Saudi Arabia, and South Africa. Healthcare investments exceeding USD 5 billion have supported the establishment of advanced biopharmaceutical facilities, leading to a 25% increase in local production capacity. Technological modernization, including the adoption of automated bioprocessing systems, has improved manufacturing efficiency by over 20%. Trade partnerships and regulatory reforms are facilitating easier access to advanced biologics and manufacturing technologies. A regional biotechnology firm in the UAE has recently initiated a biologics manufacturing project aimed at increasing domestic production capacity by 30%. Consumer behavior reflects a growing demand for advanced therapeutics, with healthcare providers prioritizing access to high-quality antibody treatments for chronic and infectious diseases.

United States – 34% share in the Antibody Production market, driven by extensive biologics manufacturing capacity and strong pharmaceutical R&D investments.

China – 18% share in the Antibody Production market, supported by rapid expansion of contract manufacturing facilities and increasing domestic demand for biosimilars.

The antibody production market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 45% of the global market share. There are over 150 active competitors operating across different segments, including biopharmaceutical companies, contract manufacturing organizations, and specialized biotechnology firms. Market leaders are focusing heavily on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their production capabilities and expand geographic presence. Over the past three years, more than 25 major strategic collaborations have been established to enhance biologics manufacturing and technology integration.

Innovation remains a key competitive factor, with over 60% of leading players investing in advanced technologies such as single-use systems, continuous bioprocessing, and AI-driven analytics. Product launches in next-generation antibody formats, including bispecific antibodies and antibody-drug conjugates, have increased by nearly 35%, intensifying competition in high-value therapeutic segments. Additionally, capacity expansion initiatives have resulted in a 30% increase in global biologics manufacturing infrastructure, enabling companies to meet rising demand. The market is also witnessing growing competition from emerging players in Asia-Pacific, where lower production costs and government support are attracting global partnerships and outsourcing contracts.

Thermo Fisher Scientific

Merck KGaA

Danaher Corporation

Sartorius AG

Lonza Group

Bio-Rad Laboratories

Agilent Technologies

GE HealthCare

WuXi Biologics

Samsung Biologics

The antibody production market is undergoing rapid technological transformation, driven by the need for higher efficiency, scalability, and product consistency. One of the most impactful advancements is the widespread adoption of single-use bioreactor systems, now utilized in over 65% of newly established biologics facilities. These systems reduce cleaning requirements by up to 40% and minimize cross-contamination risks by nearly 30%, significantly improving operational reliability. Additionally, continuous bioprocessing technologies are replacing traditional batch production, enabling yield improvements of 35% to 45% and reducing production cycle times by approximately 20%.

Cell line engineering technologies, particularly CRISPR-based gene editing, are enhancing antibody expression levels by over 50%, enabling faster development timelines and higher production outputs. Chinese Hamster Ovary (CHO) cells remain the dominant expression system, accounting for more than 70% of commercial antibody production due to their stability and scalability. Advances in upstream processing, including high-density cell culture systems, have increased volumetric productivity by nearly 2 to 3 times compared to conventional methods.

In downstream processing, innovations such as membrane chromatography and automated purification platforms have reduced processing time by up to 25% while improving purity levels beyond 99%. Digital transformation is also playing a crucial role, with approximately 55% of manufacturers implementing AI-driven analytics and real-time monitoring systems to optimize process parameters and reduce batch failures by nearly 20%. Furthermore, modular and prefabricated facility designs are enabling faster plant deployment, reducing construction timelines by up to 30%. These integrated technological advancements are collectively enhancing the efficiency, flexibility, and sustainability of antibody production operations worldwide.

• In March 2025, Thermo Fisher Scientific expanded its biologics manufacturing capabilities by opening a new sterile drug product facility in the United States, enhancing capacity for clinical and commercial antibody production with advanced single-use technologies and integrated digital monitoring systems. Source: www.thermofisher.com

• In October 2024, Lonza Group announced the expansion of its mammalian manufacturing platform, adding multiple large-scale bioreactors exceeding 15,000 liters capacity to support increasing demand for monoclonal antibody production and contract development services. Source: www.lonza.com

• In April 2025, Sartorius AG introduced an upgraded bioprocessing platform integrating AI-based analytics and automated control systems, improving process efficiency by over 25% and enabling real-time optimization of antibody production workflows. Source: www.sartorius.com

• In December 2024, WuXi Biologics launched a new biologics manufacturing facility in Asia with over 20,000 liters of bioreactor capacity, designed to support global antibody production with enhanced sustainability features and reduced energy consumption by approximately 30%. Source: www.wuxibiologics.com

The Antibody Production Market Report provides a comprehensive analysis of the global industry, covering a wide spectrum of segments, technologies, and geographic regions. The report evaluates key product types, including monoclonal antibodies, polyclonal antibodies, and recombinant antibodies, which collectively account for over 95% of total production activities. It also examines critical applications such as therapeutics, diagnostics, and research, with therapeutic use representing more than 50% of overall demand due to the increasing prevalence of chronic diseases.

Geographically, the report encompasses major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global market activity. It provides detailed insights into over 20 key countries, highlighting production capacities, infrastructure developments, and regional demand variations. The study also analyzes more than 150 active market participants, ranging from large biopharmaceutical companies to specialized contract manufacturing organizations, offering a holistic view of the competitive landscape.

Technological coverage includes upstream and downstream processing innovations, single-use systems, continuous bioprocessing, and AI-driven manufacturing solutions, which are currently adopted by over 50% of industry players. The report further explores emerging segments such as bispecific antibodies and antibody-drug conjugates, which together account for over 20% of clinical development pipelines. Additionally, it addresses regulatory frameworks, sustainability initiatives, and supply chain dynamics, providing decision-makers with actionable insights into operational efficiencies, investment priorities, and future growth opportunities within the antibody production market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Merck KGaA, Danaher Corporation, Sartorius AG, Lonza Group, Bio-Rad Laboratories, Agilent Technologies, GE HealthCare, WuXi Biologics, Samsung Biologics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |