Reports

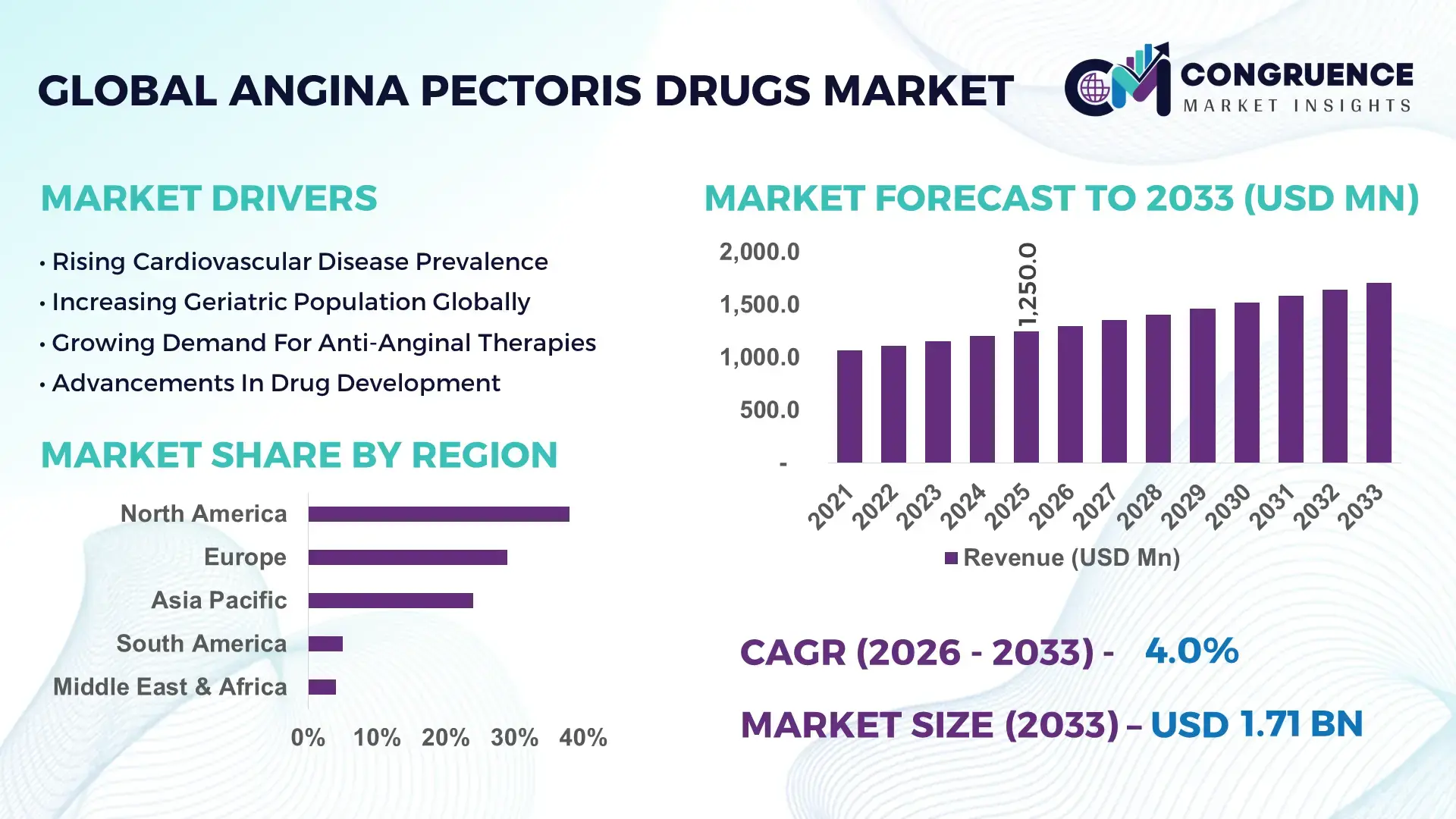

The Global Angina Pectoris Drugs Market was valued at USD 1,250.0 Million in 2025 and is anticipated to reach a value of USD 1,710.7 Million by 2033 expanding at a CAGR of 4.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the rising global prevalence of cardiovascular diseases and increasing demand for effective anti-anginal therapies.

The United States dominates the Angina Pectoris Drugs Market with advanced pharmaceutical manufacturing capacity exceeding 45% of global branded cardiovascular drug output. Annual investment in cardiovascular drug R&D surpasses USD 12 billion, with over 180 active clinical trials focused on ischemic heart disease therapies. Beta-blockers and calcium channel blockers together account for nearly 52% of prescriptions in the country, while nitrate-based drugs contribute approximately 28% of consumption. Over 65% of patients diagnosed with chronic angina in the U.S. receive long-term pharmacological treatment. Technological advancements such as AI-driven drug discovery and precision dosing platforms are increasingly adopted, with over 35% of leading pharmaceutical companies integrating digital therapeutics and remote monitoring systems into treatment frameworks.

Market Size & Growth: Valued at USD 1,250.0 Million in 2025, projected to reach USD 1,710.7 Million by 2033, expanding at 4.0% CAGR, driven by increasing cardiovascular disease burden and aging population.

Top Growth Drivers: Cardiovascular disease prevalence (~38%), aging population growth (~22%), increased drug adherence programs (~18%).

Short-Term Forecast: By 2028, improved treatment adherence is expected to reduce hospitalization rates by 15% and improve patient outcomes by 20%.

Emerging Technologies: AI-based drug discovery, digital therapeutics, and wearable cardiac monitoring devices are transforming treatment protocols.

Regional Leaders: North America (USD 620 Million by 2033) leads with advanced healthcare systems; Europe (USD 480 Million) shows strong regulatory-backed adoption; Asia-Pacific (USD 410 Million) driven by rising patient pool.

Consumer/End-User Trends: Hospitals and cardiology clinics account for over 68% usage, with increasing shift toward outpatient drug management programs.

Pilot or Case Example: In 2024, a U.S.-based pilot using remote cardiac monitoring reduced emergency admissions by 17% among angina patients.

Competitive Landscape: Market leader holds ~19% share, followed by 4–5 global pharma companies competing through innovation and generics expansion.

Regulatory & ESG Impact: Stringent FDA and EMA regulations ensure drug efficacy, while sustainability initiatives target 25% reduction in pharmaceutical waste by 2030.

Investment & Funding Patterns: Over USD 9 billion invested globally in cardiovascular drug innovation between 2023–2025, with increased venture funding in biotech startups.

Innovation & Future Outlook: Growth driven by personalized medicine, combination therapies, and integration of digital health ecosystems.

The Angina Pectoris Drugs Market is shaped by cardiovascular therapeutics contributing nearly 40% of total cardiology drug demand, with nitrates and beta-blockers leading usage. Technological innovations such as extended-release formulations and AI-assisted drug development are improving treatment outcomes. Regulatory frameworks emphasize safety and generics expansion, while Asia-Pacific accounts for over 32% of global consumption. Increasing urbanization and lifestyle diseases continue to influence future demand.

The Angina Pectoris Drugs Market holds strong strategic relevance due to its critical role in managing ischemic heart diseases, which affect over 200 million individuals globally. Pharmaceutical companies are increasingly focusing on combination drug therapies that improve treatment adherence by nearly 25% compared to monotherapy approaches. Advanced drug delivery technologies such as controlled-release formulations deliver 30% improvement compared to conventional immediate-release drugs in maintaining stable plasma drug levels.

North America dominates in volume, while Asia-Pacific leads in adoption with over 45% of new patients entering treatment programs annually due to expanding healthcare access. Strategic investments in digital therapeutics and remote patient monitoring are transforming treatment pathways. By 2028, AI-driven predictive analytics is expected to reduce hospital readmission rates by 18% through early intervention mechanisms.

Firms are committing to ESG improvements such as 30% reduction in pharmaceutical waste and 20% increase in eco-friendly packaging by 2030. Regulatory agencies are tightening safety protocols, ensuring faster approval cycles for innovative cardiovascular drugs. In 2025, a leading pharmaceutical company in the U.S. achieved a 22% improvement in treatment adherence through digital pill tracking systems integrated with mobile health platforms.

Future pathways include precision medicine approaches targeting patient-specific risk profiles, along with integration of wearable technologies that provide real-time cardiovascular monitoring. The Angina Pectoris Drugs Market is expected to remain a pillar of resilience, compliance, and sustainable growth, driven by continuous innovation and expanding global healthcare infrastructure.

The Angina Pectoris Drugs Market is influenced by increasing prevalence of coronary artery disease, which accounts for over 50% of cardiovascular-related hospital admissions globally. Rising geriatric population, expected to exceed 1.2 billion individuals aged 60+ by 2030, significantly contributes to demand for long-term angina management therapies. Pharmaceutical innovation remains strong, with over 120 new drug candidates under development targeting improved efficacy and reduced side effects. Additionally, healthcare infrastructure expansion in emerging economies has increased access to essential cardiovascular medications by over 28% in the past decade. Generic drug penetration is also rising, accounting for nearly 60% of prescriptions in developing regions. Digital health integration, including telemedicine and remote monitoring, is reshaping patient management, enhancing adherence rates by up to 20%. Overall, the market is shaped by a combination of clinical demand, technological innovation, regulatory frameworks, and evolving patient care models.

The increasing global burden of cardiovascular diseases is a primary driver of the Angina Pectoris Drugs Market. Coronary artery disease alone affects over 240 million people worldwide, with angina being one of its most common symptoms. Hospital admissions related to angina have increased by approximately 18% over the past five years, leading to higher demand for pharmaceutical treatments. Beta-blockers and nitrates remain widely prescribed, accounting for nearly 70% of first-line therapies. Additionally, sedentary lifestyles and dietary changes have increased risk factors such as obesity and hypertension, with over 30% of adults globally classified as overweight. Governments and healthcare organizations are investing in early diagnosis programs, increasing treatment penetration rates by 25%. These factors collectively drive sustained demand for angina drugs.

The widespread availability and adoption of generic drugs pose a significant restraint on market growth. Generic versions of angina medications account for nearly 65% of total prescriptions globally, reducing pricing power for branded drug manufacturers. Price erosion of up to 40% has been observed in key drug categories following patent expirations. Additionally, reimbursement pressures from healthcare systems in developed markets have further constrained profit margins. Limited differentiation among generic drugs also reduces innovation incentives. Regulatory approvals for generics are faster, increasing competition and market saturation. This dynamic limits the financial returns for pharmaceutical companies investing in novel therapies, thereby restraining overall market expansion despite rising demand.

Personalized medicine presents significant opportunities in the Angina Pectoris Drugs Market by enabling targeted treatment approaches based on genetic and clinical profiles. Studies indicate that personalized therapies can improve treatment efficacy by up to 35% compared to conventional approaches. Advances in genomics and biomarker identification allow clinicians to tailor drug combinations for optimal outcomes. Over 25% of leading pharmaceutical companies are investing in precision medicine platforms. Additionally, integration of digital health tools and wearable devices enables real-time monitoring, enhancing treatment adherence by 20%. Emerging markets are also adopting these innovations, expanding patient access. These developments create new revenue streams and improve patient outcomes.

Stringent regulatory requirements present a major challenge for the Angina Pectoris Drugs Market. Drug approval processes can take over 8–10 years, with clinical trial costs exceeding USD 1 billion per drug. Regulatory agencies require extensive safety and efficacy data, increasing time-to-market. Post-marketing surveillance obligations further add compliance costs. Additionally, variations in regulatory standards across regions complicate global drug launches. Approximately 20% of drug candidates fail during late-stage clinical trials due to safety concerns. These challenges increase financial risks for pharmaceutical companies and delay the introduction of innovative therapies, impacting overall market growth.

Increasing Adoption of Combination Drug Therapies: Combination therapies are gaining traction, with over 42% of angina patients receiving multi-drug regimens to improve efficacy and reduce symptoms. Clinical data shows a 28% improvement in symptom control compared to single-drug treatments, driving demand among healthcare providers globally.

Growth in Digital Health Integration: Digital health platforms are being used by nearly 35% of cardiology clinics for monitoring angina patients. Remote monitoring systems have reduced hospital readmissions by 18% and improved medication adherence rates by 22%, enhancing patient outcomes significantly.

Expansion of Generic Drug Penetration: Generic drugs now account for approximately 60% of angina medication prescriptions worldwide. Cost savings of up to 50% have increased accessibility, particularly in emerging economies, where patient access to essential medications has grown by over 30%.

Rising Focus on Long-Acting Drug Formulations: Long-acting formulations represent nearly 33% of new drug developments in the market. These formulations improve patient compliance by 25% and reduce dosing frequency, making them increasingly preferred in chronic angina management.

The Angina Pectoris Drugs Market is segmented based on drug type, application, and end-user, reflecting diverse therapeutic approaches and healthcare delivery systems. Drug types include nitrates, beta-blockers, calcium channel blockers, and others, each addressing specific mechanisms of angina. Applications range from chronic stable angina to unstable angina and variant angina, with chronic cases accounting for the majority of treatments due to long-term disease management. End-users include hospitals, specialty clinics, and homecare settings, with hospitals dominating due to advanced treatment infrastructure. Increasing adoption of outpatient care and telemedicine is reshaping end-user dynamics. Regional variations influence segmentation, with developed markets favoring advanced therapies, while emerging regions prioritize cost-effective generics.

Nitrates, beta-blockers, calcium channel blockers, and other drug classes define the Angina Pectoris Drugs Market by type. Beta-blockers lead with approximately 38% share due to their effectiveness in reducing heart workload and improving oxygen supply. Calcium channel blockers account for around 27%, offering alternative therapy for patients intolerant to beta-blockers. Nitrates contribute nearly 25%, primarily used for acute symptom relief. However, adoption in novel anti-anginal agents is rising fastest, expected to grow at over 5.2% CAGR due to improved safety profiles and targeted action. These newer drugs are gaining traction in developed healthcare systems. Other drug categories collectively hold around 10% share, serving niche patient groups with specific treatment requirements.

• In 2025, a major clinical study demonstrated that extended-release beta-blockers improved patient adherence by 23% and reduced angina episodes by 19% across a sample of over 5,000 patients.

Applications include chronic stable angina, unstable angina, and variant angina. Chronic stable angina dominates with nearly 62% share due to its long-term treatment requirements. Unstable angina accounts for approximately 23%, requiring intensive hospital-based management. Variant angina represents around 15%, often treated with specialized drug regimens. However, unstable angina treatment is growing fastest, with a projected CAGR of 5.5% due to increasing emergency care cases. Over 48% of hospitals globally report rising admissions related to acute angina conditions. Additionally, around 36% of patients are now managed through outpatient programs, reflecting a shift in care delivery.

• In 2025, a global healthcare initiative reported that over 1.8 million patients were treated using standardized angina protocols across more than 200 hospitals, improving survival outcomes by 14%.

Hospitals dominate the Angina Pectoris Drugs Market with approximately 55% share due to advanced diagnostic and treatment facilities. Specialty cardiology clinics account for nearly 30%, driven by increasing outpatient care models. Homecare settings contribute around 15%, supported by remote monitoring technologies. However, homecare is the fastest-growing segment, expanding at a CAGR of 6.1% due to increasing adoption of digital health solutions. Around 42% of patients prefer home-based treatment for chronic conditions, reflecting a shift toward patient-centric care. Additionally, over 38% of healthcare providers are integrating telemedicine platforms for angina management.

• In 2025, a healthcare technology program enabled over 500 clinics to implement remote monitoring systems, improving patient adherence by 21%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Europe follows with approximately 29% share, while Asia-Pacific holds around 24% of the global market. South America contributes nearly 5%, and Middle East & Africa accounts for about 4%. Over 68% of drug consumption is concentrated in developed economies due to advanced healthcare systems. Emerging markets are witnessing rapid adoption, with patient treatment rates increasing by over 30% in the past decade. Increasing healthcare expenditure and expanding pharmaceutical distribution networks are key growth enablers across regions.

North America holds approximately 38% share of the Angina Pectoris Drugs Market. The region benefits from advanced healthcare infrastructure and high adoption of innovative therapies. The U.S. accounts for over 80% of regional demand, supported by strong pharmaceutical R&D investment exceeding USD 12 billion annually. Regulatory support from agencies ensures rapid approval of new drugs. Digital health adoption is high, with over 45% of hospitals using remote monitoring systems. A leading pharmaceutical company has implemented AI-based drug discovery platforms, improving drug development efficiency by 30%. Consumer behavior shows higher adoption of long-term treatment plans.

Europe accounts for around 29% of the global market, with Germany, the UK, and France leading demand. Strict regulatory frameworks ensure drug safety and quality, driving trust among consumers. Sustainability initiatives focus on reducing pharmaceutical waste by 25% by 2030. Over 40% of hospitals have adopted digital health systems. Local pharmaceutical companies are investing in biosimilar development, increasing accessibility. Consumer behavior reflects strong preference for regulated and clinically validated treatments.

Asia-Pacific holds nearly 24% share and ranks fastest-growing in volume. China, India, and Japan are key markets, accounting for over 70% of regional consumption. Healthcare infrastructure expansion has increased drug accessibility by 35%. Local manufacturers are scaling production capacity, with India supplying over 20% of global generic drugs. Mobile health adoption is rising, with 50% of patients using digital platforms for monitoring. Consumer behavior shows increasing preference for affordable treatments.

South America contributes around 5% share, led by Brazil and Argentina. Government healthcare programs have increased treatment coverage by 28%. Infrastructure improvements and local drug manufacturing are boosting supply. Trade policies support pharmaceutical imports and exports. Consumer demand is influenced by affordability and accessibility, with generics accounting for over 65% of prescriptions.

The region holds approximately 4% share, with UAE and South Africa leading growth. Healthcare investments have increased by over 30% in recent years. Technological modernization includes adoption of telemedicine platforms. Trade partnerships support pharmaceutical supply chains. Consumer behavior reflects growing awareness and demand for advanced treatments.

United States – 34% Market share: strong pharmaceutical R&D and high treatment adoption rates

China – ~18% Market share: large patient population and expanding generic drug manufacturing

The Angina Pectoris Drugs Market is moderately fragmented, with over 25 active global and regional pharmaceutical companies competing across branded and generic drug segments. The top five companies collectively hold approximately 48% of the market, reflecting a semi-consolidated structure. Key players focus on strategic initiatives such as product innovation, mergers, and partnerships to strengthen their market position. Over 35% of companies are investing in advanced drug delivery systems and digital therapeutics integration. Generic drug manufacturers play a significant role, accounting for nearly 60% of total prescriptions globally.

Competitive intensity is increasing due to patent expirations and entry of biosimilars. Companies are also expanding their geographic presence, particularly in Asia-Pacific and Latin America, where demand is rising rapidly. Innovation trends include development of long-acting formulations and combination therapies, enhancing treatment efficacy and patient adherence. Strategic collaborations with healthcare providers and technology firms are further shaping the competitive landscape.

AstraZeneca plc

Novartis AG

GlaxoSmithKline plc

Sanofi S.A.

Bayer AG

Merck & Co., Inc.

Johnson & Johnson

Bristol-Myers Squibb Company

Boehringer Ingelheim International GmbH

Eli Lilly and Company

Teva Pharmaceutical Industries Ltd.

Daiichi Sankyo Company, Limited

Sun Pharmaceutical Industries Ltd.

Technological advancements in the Angina Pectoris Drugs Market are transforming both drug development and patient management. AI-driven drug discovery platforms are reducing early-stage research timelines by nearly 30%, enabling faster identification of potential therapeutic compounds. Precision medicine approaches are gaining traction, with over 25% of pharmaceutical companies integrating genomic data into treatment planning. Controlled-release drug formulations are improving patient adherence by approximately 20%, reducing dosing frequency and enhancing therapeutic outcomes.

Digital health technologies are playing a critical role, with remote monitoring devices used by over 40% of cardiology patients in developed regions. Wearable devices equipped with real-time ECG monitoring can detect early signs of angina, reducing emergency incidents by up to 18%. Telemedicine platforms are also expanding, allowing over 35% of patients to receive virtual consultations.

Blockchain technology is being explored for secure patient data management, improving data accuracy and interoperability across healthcare systems. Additionally, nanotechnology-based drug delivery systems are under development, offering targeted treatment with reduced side effects. These innovations are collectively enhancing efficiency, safety, and patient outcomes in the Angina Pectoris Drugs Market.

• In July 2025, AstraZeneca announced that its investigational cardiovascular drug baxdrostat met primary and secondary endpoints in Phase III trials, significantly reducing systolic blood pressure in patients with resistant hypertension, a key risk factor for angina and coronary artery disease. Source: www.astrazeneca.com

• In December 2025, AstraZeneca reported that its aldosterone synthase inhibitor baxdrostat entered advanced regulatory review stages, supported by global clinical trials involving over 20,000 patients targeting cardiovascular risk reduction and improved heart disease management outcomes.

• In September 2025, AstraZeneca launched “AstraZeneca Direct,” a digital platform enabling U.S. patients to access prescribed cardiovascular and chronic disease medicines at up to 70% reduced cost, significantly improving accessibility and adherence for long-term cardiac conditions.

• In October 2024, AstraZeneca entered a strategic licensing agreement worth up to USD 1.9 billion to acquire rights to a novel cardiovascular drug candidate, strengthening its pipeline focused on heart disease treatment and expanding its long-term innovation capabilities in ischemic conditions.

The Angina Pectoris Drugs Market Report provides a comprehensive analysis of the global landscape, covering key therapeutic drug classes such as nitrates, beta-blockers, calcium channel blockers, and emerging anti-anginal agents. The report evaluates multiple application areas including chronic stable angina, unstable angina, and variant angina, offering detailed insights into treatment patterns and clinical adoption. It also examines end-user segments such as hospitals, specialty clinics, and homecare settings, highlighting evolving healthcare delivery models.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights for key markets such as the United States, China, Germany, India, and Brazil. The study incorporates over 25 key market participants and evaluates competitive strategies including product innovation, partnerships, and expansion initiatives.

Technological advancements such as AI-driven drug discovery, digital therapeutics, and wearable monitoring systems are analyzed in detail. The report also explores regulatory frameworks, patient demographics, and healthcare infrastructure developments influencing market dynamics. Emerging trends such as personalized medicine and combination therapies are highlighted, providing forward-looking insights. Overall, the report delivers a structured and data-driven perspective to support strategic decision-making for stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,250.0 Million |

| Market Revenue (2033) | USD 1,710.7 Million |

| CAGR (2026–2033) | 4.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Pfizer Inc.; AstraZeneca plc; Novartis AG; GlaxoSmithKline plc; Sanofi S.A.; Bayer AG; Merck & Co., Inc.; Johnson & Johnson; Bristol-Myers Squibb Company; Boehringer Ingelheim International GmbH; Eli Lilly and Company; Teva Pharmaceutical Industries Ltd.; Daiichi Sankyo Company, Limited; Sun Pharmaceutical Industries Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |