Reports

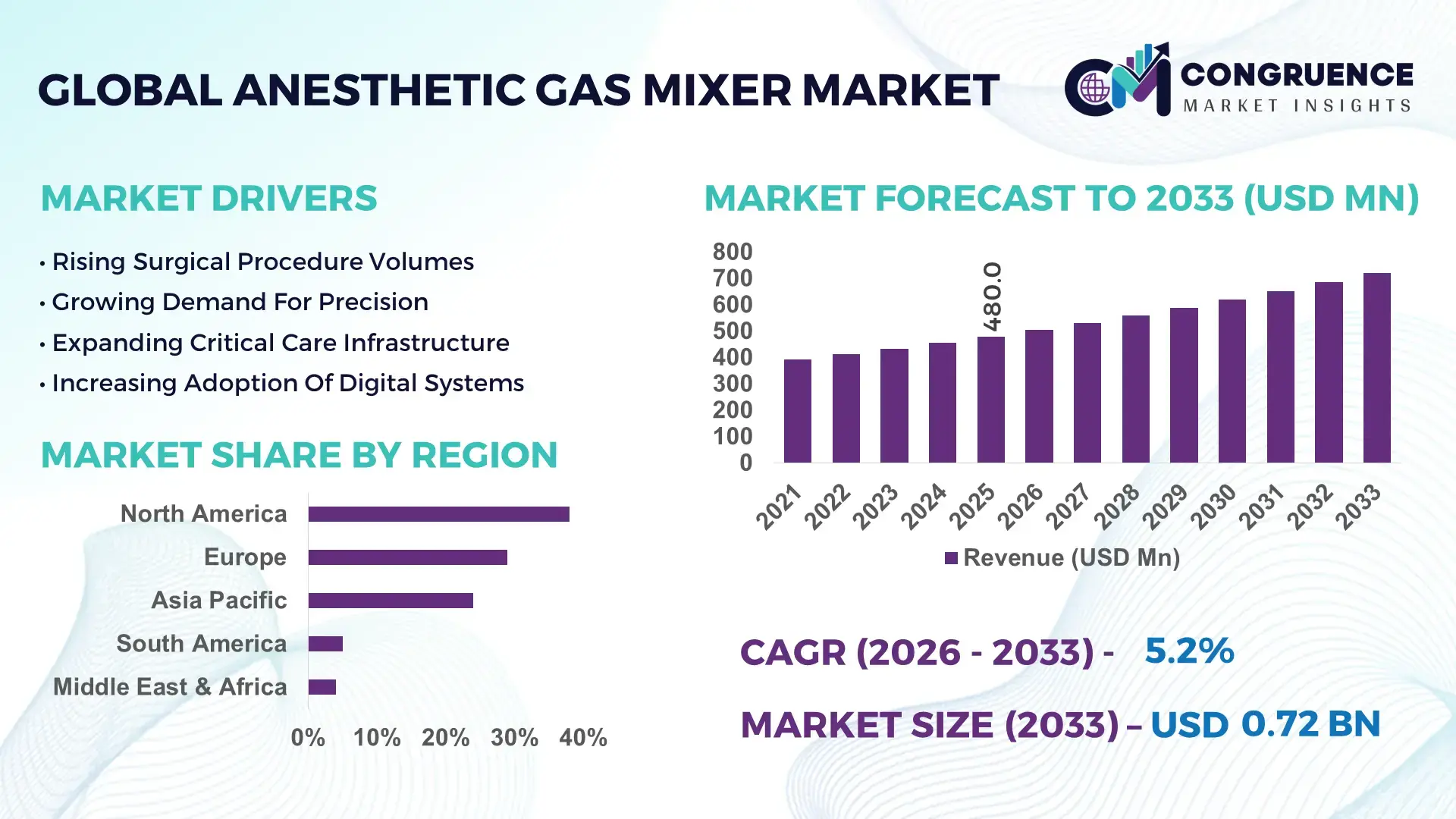

The Global Anesthetic Gas Mixer Market was valued at USD 480.0 Million in 2025 and is anticipated to reach a value of USD 720.1 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. The market is accelerating due to the rapid integration of precision-flow anesthesia delivery systems, with over 42% of advanced hospitals shifting toward digitally calibrated gas mixing platforms to improve patient safety and reduce volatile anesthetic wastage by nearly 18%. Increasing surgical procedure volumes, combined with the expansion of minimally invasive surgeries and ICU infrastructure modernization, are reshaping procurement priorities across developed healthcare systems. The 2024–2026 global healthcare equipment environment has been strongly influenced by medical supply chain diversification and stricter clinical safety compliance frameworks following geopolitical disruptions in semiconductor and medical valve sourcing across Asia and Eastern Europe. Manufacturers are increasingly regionalizing production and investing in automated calibration technologies to stabilize delivery timelines and improve equipment reliability in high-volume surgical centers.

The United States continues to dominate the global Anesthetic Gas Mixer Market with approximately 34% market share, supported by over 6,200 hospitals and ambulatory surgical centers utilizing digitally integrated anesthesia workstations. More than 68% of Tier-1 healthcare facilities in the country have upgraded to smart anesthesia monitoring ecosystems, compared to below 40% across several emerging markets. The country also leads in high-acuity surgical procedures, with over 55 million inpatient surgeries performed annually, driving sustained replacement demand for high-precision gas mixing systems. In comparison, Germany and Japan are focusing more aggressively on compact low-flow anesthesia technologies that reduce gas consumption by nearly 22%, reflecting a broader efficiency-driven transition across mature healthcare markets.

As healthcare providers increasingly prioritize operational precision, gas optimization, and regulatory-grade patient safety, companies investing in digitally connected, low-emission anesthesia delivery infrastructure are positioning themselves for long-term competitive advantage in the global surgical equipment ecosystem.

Market Size & Growth: USD 480.0 Million in 2025 reaching USD 720.1 Million by 2033 at 5.2% CAGR, driven by smart anesthesia workstation integration and precision-flow demand.

Top Growth Drivers: Surgical procedure volumes increased 14%, low-flow anesthesia adoption rose 21%, and digital monitoring integration expanded 27% globally.

Short-Term Forecast: By 2028, automated calibration systems are projected to reduce anesthetic gas wastage by 19% while improving delivery accuracy by 24%.

Emerging Technologies: AI-assisted flow control, IoT-enabled monitoring, and compact touchscreen mixers improved operational efficiency by over 26% in advanced hospitals.

Regional Leaders: North America exceeds USD 185 Million with digital adoption leadership, Europe crosses USD 145 Million with ESG-driven upgrades, while Asia-Pacific surpasses USD 165 Million through hospital expansion.

Consumer/End-User Trends: Over 61% of tertiary hospitals now prioritize integrated anesthesia platforms with real-time gas analytics and remote monitoring capabilities.

Pilot/Case Example: In 2025, a multi-hospital deployment in Japan reduced anesthetic agent consumption by 17% and equipment downtime by 13%.

Competitive Landscape: GE HealthCare controls nearly 18% share alongside Dräger, Mindray, Medtronic, and Penlon in the advanced anesthesia systems segment.

Regulatory & ESG Impact: Low-emission anesthesia protocols reduced volatile gas usage by 16% as healthcare systems tightened sustainability compliance standards.

Investment & Funding: More than USD 210 Million was allocated toward anesthesia equipment modernization, regional manufacturing expansion, and digital integration initiatives.

Innovation & Future Outlook: Cloud-connected anesthesia ecosystems and predictive maintenance platforms are redefining operational reliability and procurement strategies globally.

Hospitals accounted for nearly 58% of total equipment deployment due to rising surgical intensity and increasing ICU modernization programs, while ambulatory surgical centers contributed close to 24% as outpatient procedures expanded rapidly. Digitally integrated anesthesia systems improved operational monitoring efficiency by 26%, particularly across North America and Asia-Pacific. Meanwhile, low-flow anesthesia technologies are gaining traction as healthcare providers respond to tightening environmental compliance standards and volatile medical gas supply costs. Regional procurement strategies are increasingly shifting toward localized manufacturing and predictive maintenance capabilities, setting the foundation for a more resilient and technology-driven competitive landscape.

The Anesthetic Gas Mixer Market is rapidly transforming into a strategically critical segment within the global surgical and intensive care ecosystem as healthcare providers intensify investments in precision anesthesia delivery, patient safety optimization, and operating room efficiency. The accelerating shift toward digitally integrated operating theaters is forcing hospitals and ambulatory care networks to replace legacy analog gas delivery systems with advanced automated platforms capable of real-time gas monitoring and low-flow optimization. More than 48% of large healthcare networks are prioritizing anesthesia infrastructure modernization as surgical complexity and patient monitoring standards continue rising globally.

The market is also being reshaped by supply chain restructuring and stricter regulatory oversight surrounding anesthetic gas emissions and patient safety calibration protocols. Smart anesthesia mixing systems integrated with AI-assisted monitoring improve gas delivery efficiency by 31% while reducing anesthetic agent consumption costs by nearly 19% compared to conventional manual systems. This operational advantage is accelerating procurement cycles among high-volume surgical facilities seeking better clinical outcomes and lower resource waste.

North America leads in deployment volume due to its large installed surgical infrastructure, while Asia-Pacific leads in adoption acceleration with hospital modernization rates exceeding 28% across China, India, and Southeast Asia. Healthcare providers in Germany, Japan, and the United States are aggressively shifting toward low-flow anesthesia technologies that reduce volatile gas emissions by over 20%, creating a measurable ESG-linked operational advantage. A major hospital network implementation in South Korea improved anesthesia workflow efficiency by 23% while reducing calibration downtime by 16% through cloud-connected monitoring integration.

Over the next two to three years, automated anesthesia ecosystems are projected to reduce operating room gas wastage by 18% and shorten device maintenance cycles by nearly 14%. Medical device manufacturers are simultaneously increasing capital allocation toward localized assembly facilities, AI-driven software integration, and predictive maintenance partnerships to strengthen regional responsiveness and supply continuity. Companies capable of optimizing digital precision, sustainability compliance, and integrated operating room connectivity are positioning themselves to dominate the next phase of competitive expansion within the high-performance anesthesia equipment landscape.

The Anesthetic Gas Mixer Market is undergoing a significant transformation driven by the convergence of surgical infrastructure expansion, digital healthcare integration, and tightening patient safety standards. Healthcare systems are increasingly prioritizing precision-based anesthesia delivery technologies to reduce volatile anesthetic wastage, improve procedural consistency, and strengthen operating room efficiency. More than 44% of newly installed anesthesia workstations now include digitally controlled gas mixing modules integrated with advanced patient monitoring systems. Simultaneously, rising outpatient surgical volumes and the expansion of ambulatory surgical centers are accelerating demand for compact, low-maintenance anesthesia delivery platforms. Global procurement behavior is also shifting as hospitals seek long-life systems with predictive maintenance capabilities and lower calibration downtime. Regulatory focus on low-emission anesthesia practices and operational sustainability is further reshaping product development priorities, forcing manufacturers to accelerate innovation cycles, regional manufacturing localization, and software-enabled service models to remain competitive in an increasingly technology-driven clinical equipment environment.

The rapid expansion of high-acuity surgical infrastructure is becoming the primary growth engine for the Anesthetic Gas Mixer Market as healthcare providers increasingly prioritize precision anesthesia delivery and integrated operating room automation. More than 52% of tertiary hospitals globally are upgrading anesthesia systems to digitally controlled gas mixing platforms capable of real-time flow adjustment and low-flow optimization. This transition is reducing anesthetic gas wastage by nearly 18% while improving procedural consistency across high-volume surgical environments. Rising minimally invasive surgical procedures, which increased over 21% globally between 2023 and 2025, are further intensifying demand for advanced gas delivery accuracy and patient monitoring integration. Global supply chain restructuring following semiconductor and medical valve shortages has also forced manufacturers to regionalize production and accelerate automation investments. In response, major companies are expanding calibration facilities, strengthening component partnerships, and investing heavily in AI-assisted anesthesia monitoring technologies. Healthcare systems across North America and Asia-Pacific are prioritizing long-term procurement agreements focused on operational reliability, lower maintenance downtime, and smart connectivity integration, redefining competitive positioning across the anesthesia equipment sector.

The Anesthetic Gas Mixer Market continues facing structural limitations tied to regulatory certification complexity, precision-component dependency, and elevated maintenance costs associated with advanced anesthesia delivery systems. More than 37% of manufacturers report extended approval timelines due to evolving patient safety compliance standards and stricter calibration validation requirements across North America and Europe. Simultaneously, nearly 46% of critical flow-control valves and sensor assemblies remain concentrated within limited global supplier networks, increasing exposure to component shortages and pricing volatility. These constraints are directly affecting production scalability and procurement timelines, particularly in cost-sensitive emerging healthcare markets where imported anesthesia equipment can increase operational costs by over 22%. Hospital administrators are also delaying replacement cycles due to rising maintenance expenditures and technician training requirements for digitally integrated systems. In response, companies are diversifying supplier partnerships, increasing local component sourcing, and investing in modular platform architectures that simplify servicing and regulatory adaptation. Several manufacturers are additionally focusing on hybrid low-cost product configurations to improve accessibility without compromising precision performance or compliance readiness.

The emergence of smart low-flow anesthesia technologies is opening a major strategic opportunity within the Anesthetic Gas Mixer Market as healthcare providers intensify focus on operational efficiency, sustainability compliance, and intelligent operating room management. More than 41% of advanced surgical centers are transitioning toward automated low-flow gas delivery systems capable of reducing anesthetic agent consumption by nearly 24% while improving patient monitoring responsiveness by 19%. This efficiency advantage is creating strong demand across both developed healthcare systems and rapidly modernizing hospital networks in Asia-Pacific and the Middle East. A major future signal is the integration of AI-enabled predictive calibration and cloud-connected maintenance platforms, which are reducing unexpected device downtime by over 17%. Manufacturers are aggressively positioning for long-term dominance through software partnerships, localized production expansion, and ecosystem-based anesthesia workstation integration strategies. Emerging economies are also creating non-obvious upside opportunities as governments accelerate investments in public surgical infrastructure and outpatient care expansion. Companies capable of combining digital precision, low-emission performance, and scalable deployment economics are capturing strategic procurement advantages across increasingly competitive healthcare equipment markets.

Long-term scalability within the Anesthetic Gas Mixer Market is being constrained by infrastructure inconsistency, technical workforce limitations, and integration complexity associated with digitally connected anesthesia systems. Nearly 39% of mid-sized healthcare facilities in emerging regions lack fully standardized operating room infrastructure required for advanced automated gas mixing deployment. Additionally, calibration and compliance servicing costs have increased by approximately 16% over the last two years due to rising software integration complexity and shortages of specialized biomedical technicians. Healthcare providers also face operational resistance during migration from analog systems to digitally networked anesthesia ecosystems, particularly where interoperability with existing monitoring equipment remains limited. Supply chain pressure surrounding semiconductor availability and precision sensor manufacturing continues affecting deployment timelines and inventory planning across global medical equipment manufacturers. To remain competitive, companies must accelerate investment in simplified integration architectures, remote diagnostics capabilities, and technician training ecosystems. Strategic partnerships with hospitals, software providers, and localized service networks are becoming essential to maintain deployment consistency, operational reliability, and long-term market sustainability in an increasingly digitized surgical equipment environment.

The Anesthetic Gas Mixer Market is segmented by type, application, and end-user, with demand concentration strongly aligned to surgical infrastructure modernization and precision anesthesia delivery requirements. Integrated electronic gas mixers currently dominate deployment due to their compatibility with digitally connected anesthesia workstations, accounting for nearly 54% of total demand. However, compact portable systems are gaining traction across ambulatory surgical centers and emergency care environments as outpatient procedures continue expanding globally. Application demand remains heavily concentrated in hospitals and operating rooms, although ICU-based anesthesia support and mobile emergency units are increasing procurement intensity. Demand patterns are also shifting geographically, with Asia-Pacific healthcare networks accelerating adoption of modular anesthesia delivery platforms to improve procedural efficiency and reduce maintenance complexity. Companies are increasingly segmenting product portfolios around workflow integration, portability, low-flow optimization, and software-enabled monitoring to capture emerging operational demand pockets across both mature and developing healthcare ecosystems.

Electronic anesthetic gas mixers dominate the Anesthetic Gas Mixer Market with approximately 54% share due to their superior precision control, real-time monitoring integration, and compatibility with advanced anesthesia workstations used in high-volume surgical environments. Their structural dominance is reinforced by increasing hospital demand for digitally calibrated gas delivery systems capable of reducing anesthetic wastage by nearly 18% while improving patient monitoring efficiency. Pneumatic gas mixers continue maintaining relevance across mid-tier healthcare facilities because of lower servicing complexity and stronger cost accessibility, particularly in emerging markets where budget-sensitive procurement remains a key decision factor. Portable anesthetic gas mixers are emerging as the fastest-growing segment, with adoption expanding by nearly 23% as ambulatory surgical centers and emergency response units prioritize mobility, rapid deployment, and compact infrastructure integration. In comparison, fixed integrated systems still dominate large hospitals due to centralized workflow efficiency and higher surgical throughput capabilities. Remaining niche mixer configurations collectively account for roughly 19% of demand and serve specialized critical-care, transport, and field-anesthesia applications. Manufacturers are increasingly focusing on modular portable designs, touchscreen automation, and AI-assisted monitoring integration to capture the accelerating shift toward decentralized and flexible anesthesia delivery ecosystems.

• According to a 2025 report by the American Society of Anesthesiologists, electronic anesthetic gas mixer systems were adopted by over 64% of large surgical hospitals, resulting in nearly 21% improvement in anesthesia delivery precision and workflow efficiency, reinforcing their growing strategic importance.

Hospital operating rooms remain the leading application segment within the Anesthetic Gas Mixer Market, accounting for nearly 61% of total deployment due to the concentration of complex surgical procedures and continuous demand for precision anesthesia delivery. High surgical throughput, intensive monitoring requirements, and integration with digital operating room infrastructure continue reinforcing this segment’s dominance. Intensive care units are also increasing adoption rates as advanced ventilation-linked anesthesia support systems become more widely utilized for critical patient management and emergency respiratory interventions. Ambulatory surgical centers represent the fastest-growing application segment, with deployment rates increasing by approximately 26% as outpatient surgical procedures continue shifting away from traditional inpatient hospital settings. Compared to conventional hospital operating rooms, ambulatory facilities prioritize compact, low-maintenance, and fast-calibration systems that optimize turnover efficiency and reduce operational overhead. Emergency transport and mobile surgical units collectively account for nearly 15% of total application demand, serving specialized trauma response and military healthcare requirements. Manufacturers are increasingly redesigning anesthesia delivery platforms around portability, digital workflow synchronization, and simplified maintenance to align with evolving procedural decentralization and outpatient surgical expansion trends.

• According to a 2025 report by the World Federation of Societies of Anaesthesiologists, advanced anesthetic gas mixer systems were deployed across more than 8,500 surgical facilities globally, improving operating room workflow efficiency by 24%, highlighting their rapid operational adoption.

Hospitals remain the dominant end-user segment in the Anesthetic Gas Mixer Market with nearly 67% share due to their high surgical procedure volumes, centralized anesthesia infrastructure, and intensive dependence on integrated operating room technologies. Large multi-specialty hospitals continue prioritizing advanced electronic gas mixers capable of supporting high-acuity surgical environments, reducing gas wastage, and improving procedural consistency. Their procurement strategies increasingly favor connected anesthesia ecosystems with predictive maintenance and real-time monitoring integration. Ambulatory surgical centers are emerging as the fastest-growing end-user category, with adoption increasing by approximately 25% as healthcare systems accelerate outpatient surgery expansion and cost-efficient procedural delivery models. Compared to hospitals, these facilities prioritize portability, low maintenance requirements, and rapid operational scalability. Clinics, emergency response centers, and specialized care units collectively account for nearly 18% of total end-user demand, particularly across developing healthcare systems where infrastructure flexibility remains essential. Companies are aggressively targeting these evolving buyer groups through flexible pricing models, compact device configurations, and regional service partnerships designed to improve deployment speed and long-term equipment support.

• According to a 2025 report by the International Hospital Federation, adoption among ambulatory surgical centers increased by 27%, with over 5,200 facilities implementing advanced anesthesia delivery systems, leading to nearly 18% improvement in procedural efficiency and patient turnover optimization, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Europe maintained approximately 29% share due to strong adoption of low-emission anesthesia systems and strict patient safety compliance frameworks, while Asia-Pacific captured nearly 24% driven by hospital infrastructure expansion and localized medical equipment manufacturing. South America and the Middle East & Africa collectively contributed around 9%, supported by gradual modernization of surgical facilities and rising healthcare investments. North America leads in installed surgical infrastructure scale, Europe dominates regulatory-driven innovation, while Asia-Pacific is accelerating in deployment speed and production efficiency. Ongoing healthcare supply chain regionalization and medical equipment localization strategies are increasingly influencing global expansion priorities, with manufacturers concentrating investments toward Asia-Pacific production hubs and digitally integrated healthcare markets.

North America represents approximately 38% of the global Anesthetic Gas Mixer Market, supported by high surgical procedure volumes, strong hospital digitization, and widespread adoption of integrated anesthesia workstations. More than 69% of tertiary healthcare facilities across the United States and Canada now utilize electronically controlled gas mixing systems with real-time monitoring capabilities. Regulatory focus on patient safety calibration standards and low-emission anesthesia practices is accelerating replacement cycles for legacy analog systems. Healthcare providers are increasingly deploying AI-assisted monitoring platforms that improve anesthesia workflow efficiency by nearly 23% while reducing gas wastage by 17%. Major manufacturers are expanding regional service centers and cloud-based maintenance support networks as hospitals prioritize operational continuity, predictive servicing, and digitally connected operating room ecosystems, making North America a strategic priority for premium anesthesia technology investment.

Europe accounts for nearly 29% of the global Anesthetic Gas Mixer Market, driven by strict medical device compliance standards, sustainability-focused anesthesia protocols, and widespread adoption of low-flow gas delivery technologies. Germany, France, and the United Kingdom lead regional demand due to advanced surgical infrastructure and aggressive operating room modernization programs. Nearly 58% of hospitals across Western Europe have implemented low-emission anesthesia strategies aimed at reducing volatile anesthetic gas consumption by over 19%. Regulatory emphasis on carbon reduction and patient safety validation is forcing manufacturers to redesign systems around efficiency optimization and advanced digital calibration. Healthcare providers increasingly favor premium precision systems with integrated analytics and predictive servicing capabilities, positioning Europe as a highly influential market driving innovation, regulatory adaptation, and environmentally optimized anesthesia technology development.

Asia-Pacific holds approximately 24% share of the global Anesthetic Gas Mixer Market and represents the fastest-expanding regional demand center due to accelerating hospital construction, rising surgical volumes, and localized medical equipment manufacturing expansion. China, India, Japan, and South Korea are leading adoption as healthcare systems intensify investments in digitally integrated surgical infrastructure. Regional manufacturers have increased localized production capacity by nearly 31%, shortening delivery timelines and reducing procurement costs across high-growth healthcare markets. More than 46% of newly commissioned tertiary hospitals in key Asian economies now prioritize electronically controlled anesthesia platforms with remote diagnostics integration. Healthcare providers are heavily focused on scalability, affordability, and deployment speed, prompting companies to expand regional assembly operations, calibration centers, and distributor ecosystems to capture long-term surgical infrastructure growth opportunities.

South America contributes nearly 5% of the global Anesthetic Gas Mixer Market, with Brazil and Argentina accounting for the majority of regional demand due to expanding surgical infrastructure and increasing public healthcare investments. Demand is being driven by rising elective surgeries and modernization initiatives across urban hospitals, particularly in private healthcare networks. However, import dependency and healthcare budget limitations continue constraining large-scale equipment replacement cycles, increasing procurement costs by nearly 14% across several markets. Hospitals are increasingly adopting compact and cost-efficient anesthesia delivery systems designed for lower maintenance complexity and flexible deployment. Regional distributors are expanding localized servicing capabilities and financing partnerships to improve accessibility. The market presents strong long-term expansion potential, although operational scalability remains closely tied to economic stability and healthcare infrastructure modernization pace.

The Middle East & Africa region accounts for approximately 4% of the global Anesthetic Gas Mixer Market, supported by expanding healthcare infrastructure investments and growing demand for advanced surgical capabilities. Saudi Arabia, the United Arab Emirates, and South Africa are leading regional deployment through hospital modernization programs and public-private healthcare partnerships. More than 34% of newly commissioned tertiary healthcare facilities across Gulf countries now integrate digitally connected anesthesia systems with advanced patient monitoring features. Governments and private healthcare groups are accelerating investment in surgical equipment upgrades to improve clinical efficiency and reduce dependence on overseas medical treatment. Healthcare providers increasingly prefer scalable, low-maintenance anesthesia platforms capable of supporting high patient throughput. This regional transformation is positioning the Middle East & Africa as an emerging strategic market for long-term healthcare equipment expansion and infrastructure-driven deployment growth.

United States – 34% Market share: Dominates due to advanced surgical infrastructure, high adoption of digitally integrated anesthesia systems, and strong hospital modernization investments.

China – 16% Market share: Leads rapid expansion through large-scale hospital construction, localized medical equipment manufacturing growth, and increasing deployment of smart anesthesia technologies across urban healthcare networks.

The Anesthetic Gas Mixer Market is defined by intense competition between global anesthesia technology leaders such as GE HealthCare, Dräger, Mindray, Medtronic, Penlon, and Getinge, alongside fast-expanding regional manufacturers competing aggressively on pricing and deployment flexibility. The top five players collectively control nearly 63% of the global market, with competition increasingly centered on digital integration, low-flow precision, predictive maintenance, and operating room interoperability rather than standalone hardware performance.

Global leaders are competing through AI-assisted anesthesia platforms and integrated workflow ecosystems, while regional suppliers are targeting ambulatory surgical centers and mid-tier hospitals with systems priced 18%–25% lower. Advanced digital gas mixers improve anesthesia delivery efficiency by nearly 23% and reduce anesthetic wastage by approximately 17%, forcing manufacturers to accelerate innovation cycles and software integration capabilities. Companies are actively strengthening market position through localized manufacturing expansion, cloud-based servicing partnerships, and vertically integrated component sourcing strategies to reduce supply disruption risk.

Competitive dynamics are rapidly shifting toward software-enabled anesthesia ecosystems and sustainability-driven low-emission systems, creating higher entry barriers tied to regulatory compliance, precision calibration expertise, and long-term hospital service networks. Winning in this market now requires integrated digital capability, operational reliability, regional servicing scale, and continuous clinical workflow optimization.

Dräger

Mindray

Medtronic

Penlon

Getinge

Smiths Medical

Dameca

Spacelabs Healthcare

Infinium Medical

Heyer Medical

Beijing Aeonmed

Comen Medical

Shenzhen Superstar Medical

The Anesthetic Gas Mixer Market is rapidly evolving through the integration of AI-assisted flow control systems, cloud-connected monitoring platforms, and digitally calibrated low-flow anesthesia technologies. More than 46% of newly installed anesthesia workstations now incorporate touchscreen-controlled electronic gas mixing systems capable of improving delivery precision by nearly 24%. Hospitals are increasingly prioritizing automated gas adjustment algorithms that reduce anesthetic wastage by approximately 18% while improving operating room efficiency and patient monitoring responsiveness.

Traditional pneumatic anesthesia systems are steadily being replaced by smart electronic platforms with predictive analytics and remote diagnostics integration. Advanced AI-enabled gas delivery technologies improve calibration accuracy by over 27% while reducing maintenance downtime by nearly 16% compared to legacy analog systems. This shift is providing a major competitive advantage to manufacturers capable of integrating software intelligence, interoperability, and real-time workflow analytics into broader perioperative care ecosystems.

Cloud-based predictive maintenance platforms are also reshaping operational strategies across large hospital networks. Nearly 38% of tertiary healthcare facilities are deploying connected anesthesia monitoring infrastructures that enable remote diagnostics, software updates, and lifecycle performance optimization. Companies with strong digital servicing capabilities are capturing long-term procurement advantages as hospitals increasingly favor subscription-linked support ecosystems over standalone hardware purchasing models.

Between 2026 and 2028, low-emission anesthesia delivery systems and AI-driven automation are expected to become standard procurement priorities across advanced surgical centers. Manufacturers investing aggressively in software-enabled anesthesia ecosystems, cybersecurity integration, and scalable digital servicing networks are positioning themselves to dominate the next phase of surgical infrastructure modernization.

October 2025 – GE HealthCare unveiled the Carestation 850 anesthesia delivery system featuring continuously optimized algorithms, enhanced visualization, and sustainable low-flow functionality designed to support evolving surgical workloads. The platform addressed growing operational pressure, with 68% of anesthesia professionals identified as high burnout risk. [AI-Integrated Precision] Source: www.gehealthcare.com

October 2025 – GE HealthCare highlighted University of Michigan findings involving nearly 15,000 anesthesia cases demonstrating that End-tidal Control software significantly reduced anesthetic agent usage and greenhouse gas emissions through automated gas concentration adjustment. The development strengthened demand for environmentally optimized anesthesia workflows. [Low-Emission Automation]

February 2026 – GE HealthCare accelerated investment in precision-care technologies and cloud-enabled healthcare optimization following strong demand across imaging and patient care solutions. The company expanded its operational “Heartbeat” business system to improve productivity and customer experience while advancing digitally connected perioperative care infrastructure. [Workflow Optimization Push]

November 2025 – GE HealthCare announced the USD 2.3 billion acquisition of Intelerad to strengthen cloud-based outpatient imaging and software-as-a-service capabilities. The deal expanded recurring digital healthcare infrastructure exposure and reinforced strategic integration of AI-enabled clinical workflow technologies across connected care ecosystems. [Cloud Expansion Strategy]

The Anesthetic Gas Mixer Market Report delivers comprehensive coverage of the global anesthesia delivery ecosystem across product types, clinical applications, end-user categories, and regional healthcare infrastructure trends. The report evaluates electronic, pneumatic, portable, and integrated anesthesia gas mixing systems across hospitals, ambulatory surgical centers, intensive care units, and emergency care environments. It further analyzes operational demand patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while assessing technology deployment intensity, healthcare modernization pace, and surgical infrastructure expansion dynamics.

The study includes deep analysis of more than 14 major market participants and evaluates over 25 strategic performance indicators linked to deployment scale, digital integration, low-flow anesthesia adoption, predictive maintenance capability, and operating room connectivity trends. More than 46% of advanced healthcare facilities now prioritize digitally integrated anesthesia ecosystems, while nearly 41% are transitioning toward low-emission anesthesia technologies designed to reduce anesthetic gas consumption and improve workflow precision.

The report also delivers forward-looking strategic insights covering AI-assisted anesthesia monitoring, cloud-connected servicing platforms, localized manufacturing expansion, and next-generation low-flow delivery systems expected to reshape procurement strategies between 2026 and 2033. It supports decision-makers in investment prioritization, regional expansion planning, competitive benchmarking, operational optimization, and long-term technology positioning across the rapidly transforming surgical equipment landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 480.0 Million |

| Market Revenue (2033) | USD 720.1 Million |

| CAGR (2026–2033) | 5.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | GE HealthCare; Dräger; Mindray; Medtronic; Penlon; Getinge; Smiths Medical; Dameca; Spacelabs Healthcare; Infinium Medical; Heyer Medical; Beijing Aeonmed; Comen Medical; Shenzhen Superstar Medical |

| Customization & Pricing | Available on Request (10% Customization Free) |