Reports

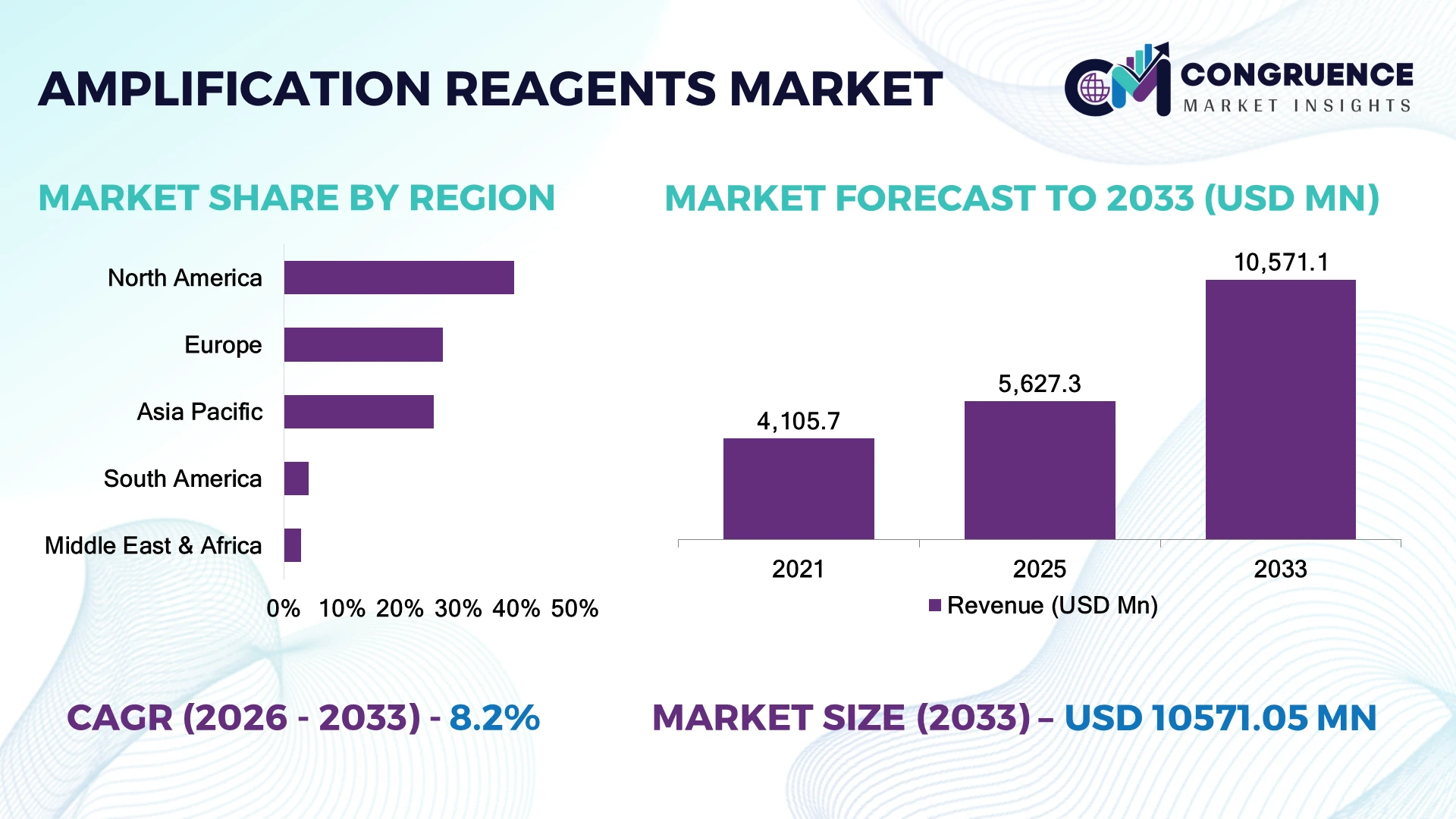

The Global Amplification Reagents Market was valued at USD 5,627.3 Million in 2025 and is anticipated to reach a value of USD 10,571.1 Million by 2033 expanding at a CAGR of 8.2% between 2026 and 2033. Expanding molecular diagnostics, precision oncology, infectious disease surveillance, and next-generation sequencing workflows are accelerating adoption of high-performance amplification reagents with greater sensitivity, reproducibility, and automation compatibility.

The United States remains the dominant country, contributing approximately 39% of global molecular diagnostics reagent consumption, supported by advanced clinical laboratories, biopharmaceutical R&D, and large-scale genomic medicine initiatives. More than 3,000 CLIA-certified high-complexity molecular laboratories utilize advanced amplification workflows, while China is rapidly expanding domestic biotechnology manufacturing and genomic testing capacity. Continued supply-chain diversification following recent geopolitical trade realignments is strengthening localized reagent production and strategic manufacturing resilience.

Manufacturers investing in high-fidelity chemistries, automated workflow compatibility, and regional production capabilities are positioned to secure long-term leadership across clinical and research applications.

Market Size & Growth: USD 5,627.3 Million in 2025, projected to reach USD 10,571.1 Million by 2033 at a CAGR of 8.2%, supported by precision diagnostics and genomics expansion.

Top Growth Drivers: Precision medicine (+32%), molecular diagnostics (+29%), and next-generation sequencing adoption (+24%).

Short-Term Forecast: By 2028, automated workflows improve laboratory productivity by approximately 26% while reducing manual processing time by 22%.

Emerging Technologies: AI-assisted assay optimization, digital PCR, and automation-ready reagent formulations strengthen analytical performance.

Regional Leaders: North America exceeds USD 3,900 Million, Europe approaches USD 2,600 Million, and Asia-Pacific surpasses USD 2,900 Million through expanding genomics infrastructure.

Consumer/End-User Trends: More than 68% of reference laboratories prioritize automation-compatible amplification reagents.

Pilot/Case Example: A 2026 genomics laboratory modernization program improved sample throughput by 35% using integrated amplification workflows.

Competitive Landscape: Leading suppliers collectively hold around 48% market share, including Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories, Roche, and Agilent Technologies.

Regulatory & ESG Impact: Optimized reagent packaging reduces laboratory plastic waste by approximately 18% while supporting sustainable procurement.

Investment & Funding: More than USD 2.3 Billion supports manufacturing expansion, strategic partnerships, and molecular diagnostics capacity worldwide.

Innovation & Future Outlook: Multiplex amplification chemistries and ultra-high-fidelity enzymes are strengthening competitive differentiation across clinical and research markets.

Amplification reagents are becoming central to oncology diagnostics, infectious disease testing, reproductive health screening, agricultural genomics, and translational research. High-fidelity polymerases, inhibitor-resistant master mixes, and multiplex-ready formulations now account for more than 46% of premium laboratory reagent demand. Increasing laboratory automation and regional reagent manufacturing initiatives are strengthening supply continuity and analytical consistency, creating a solid foundation for the strategic market discussion.

The Amplification Reagents Market has become strategically significant as healthcare systems, biotechnology companies, and research organizations expand molecular testing capacity to support precision medicine and advanced genomic analysis. Laboratory modernization, regional manufacturing initiatives, and strengthened regulatory oversight are encouraging suppliers to develop standardized, automation-compatible reagent portfolios capable of supporting high-volume diagnostic workflows while improving supply-chain resilience.

Modern hot-start polymerases and optimized multiplex master mixes deliver approximately 30% higher amplification efficiency and reduce repeat testing compared with conventional reagent formulations. North America leads clinical assay commercialization through established molecular diagnostics infrastructure, while Asia-Pacific is expanding manufacturing capacity and research investment to strengthen domestic biotechnology ecosystems. During the next two to three years, automated molecular laboratories are expected to increase adoption of integrated reagent platforms supporting higher throughput, stronger reproducibility, and faster laboratory turnaround.

A practical example is the deployment of fully automated PCR workflows in hospital laboratory networks, where standardized amplification reagents minimize workflow variability while improving testing consistency. Companies are expanding regional manufacturing, strengthening collaborations with sequencing platform developers, and investing in enzyme engineering to support increasingly complex molecular applications. Organizations combining reagent innovation, manufacturing resilience, and automation compatibility will secure stronger competitive positioning across the evolving global molecular diagnostics landscape.

Rapid expansion of precision diagnostics and genomic medicine is accelerating demand for high-performance amplification reagents across clinical laboratories and biotechnology companies. More than 72% of newly developed molecular diagnostic assays now utilize optimized master mixes and high-fidelity polymerases, while multiplex PCR adoption has increased by approximately 28% in advanced diagnostic laboratories. The United States continues expanding precision medicine programs, encouraging wider implementation of standardized molecular workflows. This structural shift is improving diagnostic accuracy, reducing repeat testing, and increasing laboratory throughput. Reagent manufacturers are responding by expanding enzyme production capacity, investing in proprietary polymerase engineering, and forming strategic collaborations with diagnostic platform developers to deliver automation-ready reagent portfolios supporting increasingly complex molecular applications.

Production of amplification reagents remains sensitive to specialized enzyme manufacturing, high-purity nucleotide supply, and stringent quality-control requirements. Approximately 38% of critical reagent components continue relying on internationally distributed supply networks, while pharmaceutical-grade raw material costs remain nearly 16% above historical averages. Regulatory validation requirements further extend product qualification timelines before commercial deployment. These structural limitations increase manufacturing costs, reduce inventory flexibility, and complicate production planning for laboratory suppliers. Companies are mitigating operational risks through regional manufacturing expansion, dual-source procurement strategies, long-term supplier agreements, and greater investment in vertically integrated enzyme production to strengthen supply continuity and manufacturing resilience.

Growing integration of genomics, transcriptomics, and liquid biopsy workflows is creating high-value opportunities for advanced amplification reagent platforms. Nearly 44% of newly established translational research laboratories are investing in automation-compatible reagent systems, while digital PCR adoption has expanded by approximately 27% across advanced molecular testing facilities. South Korea and Singapore continue strengthening national biotechnology innovation programs supporting next-generation molecular research infrastructure. Companies are developing highly multiplexed reagent chemistries, AI-assisted assay optimization platforms, and strategic collaborations with sequencing instrument manufacturers. A significant emerging opportunity lies in standardized reagent ecosystems that simplify cross-platform compatibility while reducing laboratory workflow complexity and validation costs.

Increasing diversity of molecular diagnostic platforms is creating long-term execution challenges for amplification reagent suppliers. Approximately 32% of clinical laboratories operate multiple PCR and sequencing platforms requiring different reagent validation protocols, while cross-platform assay optimization increases laboratory implementation time by nearly 18%. Regulatory expectations for analytical reproducibility continue tightening as molecular diagnostics expand into decentralized healthcare settings. These complexities affect product scalability, global commercialization, and laboratory consistency. Companies must strengthen universal reagent compatibility through advanced formulation engineering, collaborative platform validation, digital quality management systems, and expanded technical support to ensure reproducible performance across increasingly diverse molecular testing environments.

Automation-Ready Reagent Formulations More than 65% of newly introduced premium amplification reagents are optimized for automated liquid-handling systems, reducing manual workflow time by approximately 24% while improving batch consistency by nearly 20%. Laboratory workforce shortages are accelerating automation investments, prompting manufacturers to expand instrument partnerships and standardize reagent packaging for high-throughput molecular testing environments.

Multiplex Assay Optimization Multiplex amplification workflows now reduce reagent consumption by roughly 18% while increasing laboratory throughput by approximately 30% through simultaneous target detection. Clinical laboratories are consolidating diagnostic panels to improve operational efficiency and reduce turnaround times. Companies are investing in advanced enzyme chemistries and assay design platforms supporting broader diagnostic menus without compromising analytical sensitivity.

Regional Manufacturing Diversification Localized reagent production has increased by nearly 28% as biotechnology companies reduce dependence on international raw material sourcing. Expanded domestic manufacturing improves delivery reliability by approximately 20% and strengthens inventory resilience against global logistics disruptions. Manufacturers are restructuring supply chains, expanding regional production facilities, and establishing strategic raw material partnerships to improve procurement stability.

High-Fidelity Enzyme Innovation Advanced polymerase engineering delivers approximately 35% higher amplification accuracy while reducing nonspecific amplification by nearly 22% compared with conventional formulations. Increasing adoption of next-generation sequencing and precision oncology testing is driving demand for higher analytical performance. Companies are accelerating enzyme research, expanding intellectual property portfolios, and integrating high-fidelity chemistries into comprehensive molecular workflow solutions to strengthen competitive differentiation.

PCR reagents remain the dominant product type, accounting for approximately 61% of global amplification reagent demand due to their established role across clinical diagnostics, molecular biology research, infectious disease testing, and precision oncology. Their proven analytical performance, compatibility with automated PCR platforms, and standardized laboratory workflows make them the preferred choice for routine molecular testing. Isothermal amplification reagents represent the fastest-growing segment as decentralized diagnostics and point-of-care testing increasingly favor rapid nucleic acid amplification without thermal cycling. Nearly 27% of newly introduced molecular diagnostic platforms now support isothermal amplification technologies, reflecting growing demand for portable and simplified testing workflows. Companies continue expanding high-fidelity PCR chemistries while investing in isothermal reagent innovation for emerging diagnostic applications.

Transcription-mediated amplification reagents maintain strong adoption in high-sensitivity infectious disease screening, while rolling circle amplification reagents continue expanding across genomic research and biomarker discovery. Other amplification technologies serve specialized research applications where ultra-high specificity or unique workflow compatibility is required. Manufacturers are strengthening product portfolios through enzyme engineering, multiplex reagent development, and platform partnerships to support diverse molecular workflows. Investment is steadily shifting toward integrated reagent ecosystems capable of supporting both centralized laboratories and decentralized diagnostic environments.

Recent technical assessments from molecular diagnostics industry studies during 2025 indicate that PCR-based amplification continues to represent the reference technology across regulated clinical laboratories, while isothermal amplification platforms are experiencing the strongest deployment growth in decentralized testing environments because of simplified instrumentation requirements.

Clinical diagnostics represents the largest application segment, contributing approximately 55% of amplification reagent consumption as hospitals and reference laboratories continue expanding molecular testing for oncology, infectious diseases, inherited disorders, and transplant monitoring. Standardized reagent performance, regulatory compliance, and high analytical sensitivity continue driving procurement decisions. Research applications are the fastest-growing segment as genomic medicine, biomarker discovery, and precision therapeutics accelerate adoption of advanced amplification chemistries. Nearly 31% of newly established molecular research laboratories have increased investments in high-fidelity amplification reagents supporting sequencing and gene expression analysis. Companies are expanding automation-compatible reagent portfolios while strengthening collaborations with sequencing and molecular diagnostics platform developers.

Food safety, forensic science, and environmental testing continue broadening market diversification through increasing use of rapid nucleic acid amplification technologies. These applications require robust reagent stability, contamination resistance, and reproducible analytical performance under diverse operating conditions. Suppliers are introducing specialized formulations optimized for complex sample matrices while investing in automated workflows that improve laboratory efficiency and reduce validation requirements across multiple testing environments.

Industry analyses released during 2025 consistently identify clinical diagnostics as the largest application for amplification reagents, while research laboratories remain the fastest-expanding users due to growing investments in precision medicine, sequencing, and translational genomics.

Diagnostic laboratories remain the dominant end-user group, accounting for nearly 47% of global amplification reagent procurement due to high routine testing volumes, regulatory-standardized workflows, and continuous expansion of molecular diagnostics. Pharmaceutical and biotechnology companies represent the fastest-growing end-user segment as biologics development, companion diagnostics, and cell and gene therapy programs require increasingly sophisticated amplification technologies. Approximately 34% of advanced molecular assay development programs now integrate high-fidelity amplification reagents during assay optimization. Companies are responding through customized reagent formulations, strategic co-development partnerships, and application-specific product portfolios supporting regulated laboratory environments.

Academic and research institutes continue generating substantial demand through genomics, microbiology, and translational medicine programs, while contract research organizations are expanding molecular testing capabilities to support outsourced pharmaceutical development. Manufacturers are strengthening customer engagement through technical support, flexible packaging configurations, automation-ready reagents, and long-term collaboration models that improve laboratory productivity and customer retention across diverse end-user segments.

Enterprise and laboratory market assessments published during 2025 identify diagnostic laboratories as the largest purchasers of amplification reagents, while pharmaceutical and biotechnology organizations continue recording the fastest expansion in advanced molecular workflow adoption driven by precision medicine and therapeutic development.

North America accounted for the largest market share at 39.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

Precision Diagnostics Leadership Strengthens Molecular Testing Ecosystems

North America maintains the leading position through its extensive molecular diagnostics infrastructure, advanced biotechnology sector, and high concentration of pharmaceutical innovation. The region represented approximately 39.6% of global demand in 2025, supported by large-scale clinical laboratories, genomic medicine programs, and expanding next-generation sequencing capacity. More than 70% of high-throughput molecular laboratories have integrated automated amplification workflows to improve reproducibility and laboratory efficiency. Growing investment in decentralized molecular testing, biopharmaceutical R&D, and companion diagnostics continues expanding demand for high-fidelity amplification reagents. Manufacturers are strengthening domestic enzyme production, expanding automation-compatible product portfolios, and establishing strategic collaborations with sequencing and molecular diagnostics platform developers.

United States Market Outlook: The United States remains the regional growth engine through its mature molecular diagnostics ecosystem, strong biotechnology industry, and advanced clinical laboratory network. More than 3,000 CLIA-certified high-complexity molecular laboratories support large-scale deployment of amplification reagents across oncology, infectious disease diagnostics, and precision medicine. Companies continue investing in domestic manufacturing, enzyme engineering, and integrated molecular workflow solutions to strengthen supply resilience and accelerate commercialization of next-generation diagnostic assays.

Regulatory Standardization Drives Advanced Molecular Workflows

Europe accounts for approximately 27.3% of the global market, supported by expanding genomic medicine initiatives, strong pharmaceutical research, and harmonized molecular diagnostic standards. Clinical laboratories are accelerating adoption of automation-ready amplification reagents to improve testing consistency while supporting personalized medicine programs. The implementation of updated in vitro diagnostic regulations is encouraging greater investment in assay validation, analytical performance, and standardized reagent manufacturing. Companies are expanding regional production, strengthening quality management systems, and developing highly reproducible reagent formulations optimized for regulated laboratory environments.

Germany Market Outlook: Germany leads the regional market through its advanced life sciences industry, strong molecular diagnostics infrastructure, and globally competitive biotechnology manufacturing base. Expanding translational research programs and pharmaceutical innovation continue increasing demand for premium amplification reagents. Domestic manufacturers are investing in automated production technologies, advanced enzyme development, and collaborative research partnerships to strengthen scientific leadership while supporting regulated clinical laboratory applications.

Biotechnology Manufacturing Expansion Accelerates Market Development

Asia-Pacific is the fastest-expanding regional market, contributing approximately 25.8% of global demand through growing biotechnology manufacturing, precision medicine investment, and expanding molecular diagnostics capacity. Governments continue supporting genomic research, infectious disease surveillance, and domestic reagent production to reduce import dependence. More than 40% of newly established molecular laboratories within the region have adopted automated PCR workflows supporting higher sample throughput. Manufacturers are expanding production facilities, increasing localized enzyme manufacturing, and strengthening strategic partnerships with diagnostic platform providers to improve regional supply security.

China Market Outlook: China represents the largest country market in the region through rapid biotechnology industrialization, extensive hospital laboratory modernization, and sustained investment in precision medicine. Domestic manufacturers continue expanding high-quality reagent production while strengthening enzyme research and quality validation systems. Increasing deployment of molecular diagnostics across provincial healthcare networks is encouraging broader commercialization of automation-compatible amplification reagent platforms designed for both clinical and research laboratories.

Clinical Laboratory Modernization Supports Market Expansion

South America is experiencing steady market development through modernization of public healthcare laboratories, expansion of molecular diagnostics, and strengthening infectious disease surveillance capabilities. The region contributes approximately 4.3% of global demand, with investment concentrated in hospital laboratories, research institutes, and national disease monitoring programs. Increasing adoption of automated PCR systems is improving laboratory productivity despite infrastructure and procurement limitations. Suppliers are expanding regional distribution partnerships, improving technical training, and strengthening localized customer support to improve deployment efficiency across healthcare institutions.

Brazil Market Outlook: Brazil remains the largest national market due to its extensive public healthcare system, expanding biotechnology sector, and growing molecular diagnostics capacity. Investments in clinical laboratory modernization and genomic research continue increasing utilization of amplification reagents across infectious disease testing and oncology diagnostics. Manufacturers are strengthening regional logistics, expanding technical support services, and collaborating with research organizations to improve laboratory capability and long-term reagent availability.

Healthcare Infrastructure Investment Expands Molecular Testing Capacity

The Middle East & Africa market is strengthening through healthcare modernization, genomic medicine initiatives, and investment in advanced diagnostic infrastructure. The region accounts for approximately 3.0% of global demand, supported by expanding hospital laboratory networks and national public health surveillance programs. Increasing deployment of molecular diagnostic platforms is encouraging broader use of standardized amplification reagents across infectious disease, oncology, and genetic testing applications. Companies are expanding distributor partnerships, improving technical service capabilities, and introducing application-specific reagent portfolios aligned with evolving regional laboratory requirements.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through sustained investment in biotechnology, healthcare transformation, and national genomic medicine initiatives. Expansion of advanced hospital laboratories and precision medicine programs continues increasing demand for high-quality amplification reagents. Companies are strengthening local distribution partnerships, expanding scientific training programs, and supporting laboratory automation initiatives to improve diagnostic performance while reducing dependence on imported molecular testing workflows.

Global leaders including Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories, Roche, and Agilent Technologies compete directly with specialized reagent innovators such as Takara Bio and Promega, while regional manufacturers challenge through lower-cost production and localized supply. The top five suppliers collectively account for approximately 48% of global market share. Competition centers on enzyme fidelity, multiplex capability, automation compatibility, and manufacturing reliability rather than price alone. Premium suppliers deliver 25–35% higher amplification accuracy through proprietary polymerases, while regional producers typically offer 15–20% lower pricing for standard PCR reagent portfolios. Companies are expanding enzyme manufacturing, securing raw material supply, strengthening sequencing platform partnerships, and vertically integrating critical biological production processes. The competitive landscape is shifting toward automation-ready master mixes, AI-assisted assay optimization, and integrated molecular workflow ecosystems. Stringent regulatory validation, intellectual property protection, and biological manufacturing expertise remain major barriers. Market leadership increasingly depends on superior analytical performance, supply resilience, platform compatibility, and continuous molecular innovation.

Thermo Fisher Scientific

QIAGEN

Bio-Rad Laboratories

F. Hoffmann-La Roche

Agilent Technologies

Takara Bio

Promega Corporation

New England Biolabs

Merck KGaA

LGC Biosearch Technologies

Bio-Techne

Jena Bioscience

Revvity

Advanced hot-start polymerases, high-fidelity enzymes, and multiplex master mixes currently define the technological foundation of the amplification reagents market. More than 68% of premium molecular laboratories now utilize automation-compatible reagent formulations, improving workflow consistency while reducing manual processing errors. High-fidelity polymerases enhance amplification accuracy by approximately 30% and reduce nonspecific amplification by nearly 22%, strengthening clinical confidence across oncology, infectious disease diagnostics, and genomic research. Automated liquid-handling integration further improves laboratory productivity and operational scalability.

Emerging technologies include digital PCR reagents, AI-assisted assay optimization, lyophilized reagent formulations, and CRISPR-compatible amplification chemistries. Compared with conventional PCR reagents, next-generation high-fidelity master mixes reduce repeat testing by approximately 25% while improving sensitivity for low-copy nucleic acid detection. Diagnostic laboratories, pharmaceutical developers, and sequencing service providers gain the greatest competitive advantage through faster validation, standardized workflows, and improved analytical reproducibility across increasingly complex molecular testing environments.

Between 2026 and 2028, intelligent reagent ecosystems integrating cloud-enabled quality management, digital workflow tracking, and platform-independent assay compatibility will accelerate laboratory modernization. Wider adoption of stabilized room-temperature formulations and automation-ready reagent kits will reduce logistics complexity by approximately 18% while improving deployment flexibility. Companies investing early in enzyme engineering, integrated molecular workflows, and scalable manufacturing technologies will strengthen competitive differentiation as laboratories increasingly prioritize analytical precision, operational efficiency, and supply-chain resilience.

June 2025 – QIAGEN launched the QIAcuityDx Digital PCR System for clinical diagnostics, expanding digital PCR capabilities with standardized workflows and multiplex detection supporting up to 12 targets in one assay. Business impact: strengthens regulated molecular diagnostics adoption. Source: qiagen.com

April 2026 – Thermo Fisher Scientific introduced the Applied Biosystems PowerFlex Thermal Cycler, designed to improve PCR workflow flexibility and laboratory productivity through enhanced instrument performance and automation compatibility. Business impact: accelerates high-throughput molecular testing efficiency. Source: thermofisher.com

June 2026 – Agilent Technologies completed the acquisition of Biocare Medical in a transaction valued at approximately USD 950 million, expanding its clinical pathology reagent portfolio. Business impact: broadens integrated diagnostics capabilities and strengthens life sciences market positioning. Source: agilent.com

June 2024 – QIAGEN announced the discontinuation of its NeuMoDx integrated PCR testing systems following post-pandemic market realignment while maintaining customer support through transition programs. Business impact: reallocates resources toward higher-growth molecular diagnostics platforms. Source: The Wall Street Journal

The report provides a comprehensive evaluation of the Amplification Reagents Market across major product types, applications, end-user industries, and regional markets. It analyzes PCR, isothermal amplification, transcription-mediated amplification, and emerging reagent technologies supporting molecular diagnostics, genomics, pharmaceutical research, forensic science, and food safety testing. More than 60% of advanced laboratory workflows now utilize automation-compatible amplification reagents, highlighting the industry's transition toward standardized high-throughput molecular testing.

The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while assessing technology adoption, manufacturing expansion, competitive positioning, and evolving laboratory requirements between 2026 and 2033. It examines deployment trends, enterprise purchasing behavior, platform integration, and innovation strategies across diagnostic laboratories, biotechnology companies, pharmaceutical manufacturers, and research institutions. The report supports investment prioritization, portfolio expansion, competitive benchmarking, partnership evaluation, and long-term strategic planning within the global amplification reagents ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,627.3 Million |

|

Market Revenue in 2033 |

USD 10,571.1 Million |

|

CAGR (2026 - 2033) |

8.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories, F. Hoffmann-La Roche, Agilent Technologies, Takara Bio, Promega Corporation, New England Biolabs, Merck KGaA, LGC Biosearch Technologies, Bio-Techne, Jena Bioscience, Revvity |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |