Reports

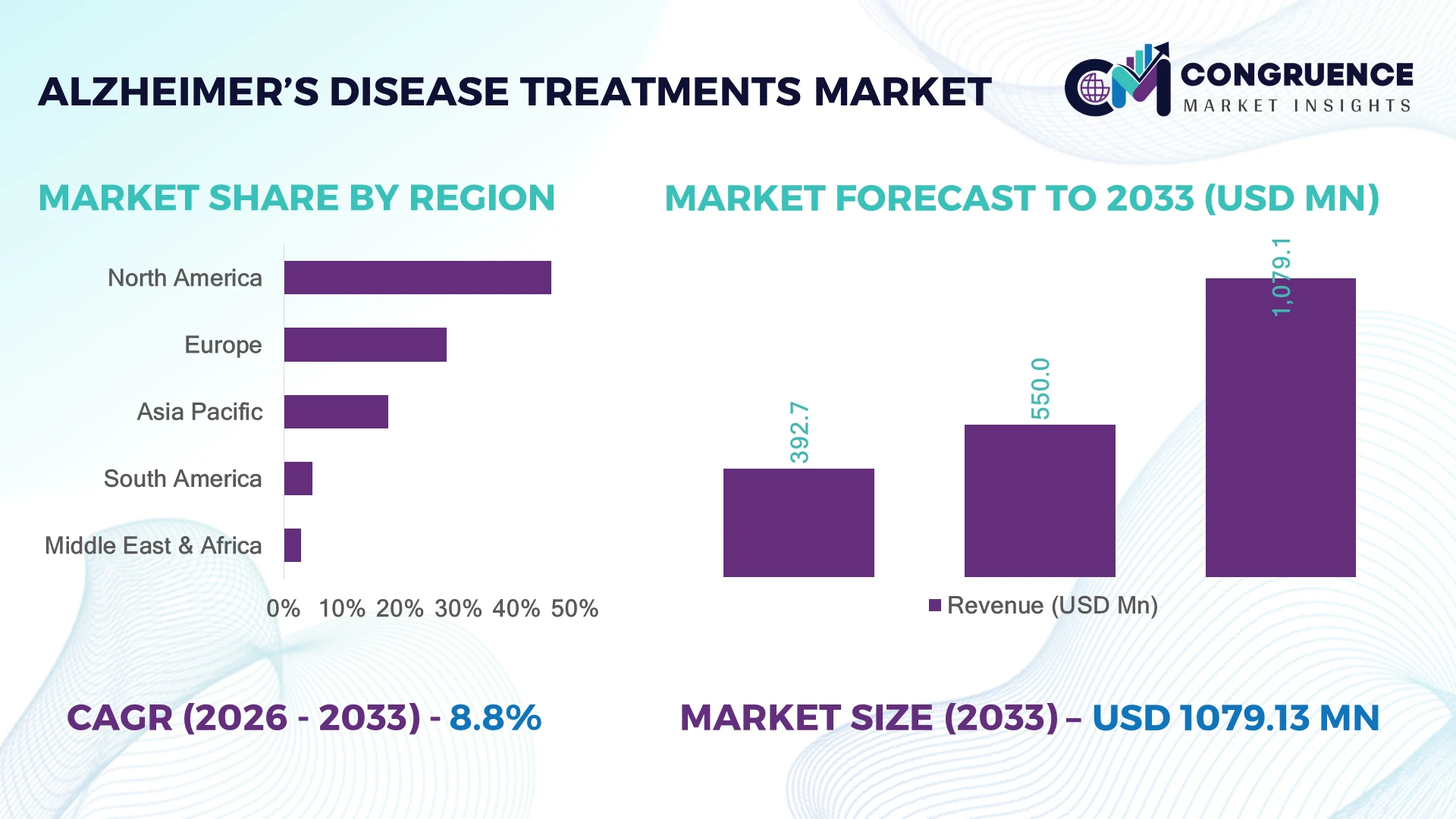

The Global Alzheimer’s Disease Treatments Market was valued at USD 550.0 Million in 2025 and is anticipated to reach a value of USD 1,079.1 Million by 2033 expanding at a CAGR of 8.79% between 2026 and 2033. Growth is driven by the expanding adoption of disease-modifying therapies, accelerated biomarker-based diagnostics, and increasing regulatory approvals for innovative monoclonal antibody treatments.

The United States dominates the global market with an estimated 46% share, supported by annual neuroscience research investments exceeding USD 8 billion, widespread PET imaging and biomarker testing adoption, and a mature specialty neurology network. Compared with Japan, which leads Asia through rapid aging demographics and structured dementia programs, the U.S. benefits from stronger commercialization capabilities and faster integration of advanced Alzheimer's therapeutics following recent FDA regulatory actions.

Organizations prioritizing early diagnosis infrastructure, biologic manufacturing capacity, and strategic clinical partnerships are positioned to secure long-term competitive advantage in this evolving therapeutic landscape.

Market Size & Growth: USD 550.0 Million in 2025, projected to reach USD 1,079.1 Million by 2033 at 8.79% CAGR, driven by expanding disease-modifying biologic therapies and precision diagnostics.

Top Growth Drivers: Biomarker testing adoption (+28%), monoclonal antibody utilization (+24%), and aging population expansion (+18%) continue strengthening market momentum.

Short-Term Forecast: By 2028, early diagnostic workflow efficiency is expected to improve by 30%, reducing treatment initiation delays across specialized centers.

Emerging Technologies: AI-assisted imaging, blood-based biomarkers, and digital cognitive assessment platforms improve diagnostic accuracy and clinical decision-making.

Regional Leaders: North America (~USD 470 Million), Europe (~USD 290 Million), and Asia-Pacific (~USD 190 Million) benefit from advanced reimbursement, research expansion, and aging demographics.

Consumer/End-User Trends: More than 40% of eligible patients are expected to receive biomarker-supported diagnostic assessments before treatment selection.

Pilot/Case Example: In 2024, advanced digital cognitive assessment programs reduced evaluation time by nearly 35%, improving specialist workflow efficiency.

Competitive Landscape: The leading company holds approximately 22% market share, while Eli Lilly, Biogen, Eisai, Roche, and Novo Nordisk intensify innovation through global partnerships.

Regulatory & ESG Impact: Accelerated regulatory pathways shortened review timelines by nearly 20%, encouraging broader commercialization across major healthcare markets.

Investment & Funding: More than USD 5 billion continues flowing into neuroscience R&D, strategic collaborations, and manufacturing expansion amid global pharmaceutical portfolio diversification.

Innovation & Future Outlook: Next-generation combination therapies, precision biomarkers, and AI-enabled patient monitoring are reshaping competitive differentiation and long-term treatment strategies.

The Alzheimer’s Disease Treatments Market continues evolving as healthcare systems emphasize earlier intervention, precision diagnostics, and disease-modifying therapies across specialized neurology networks. Innovation in blood-based biomarkers, digital cognitive assessment tools, and monoclonal antibody development is accelerating clinical adoption. More than 30% of late-stage pipelines now target combination therapeutic approaches, while evolving regulatory frameworks and biologics manufacturing expansion strengthen commercialization readiness, setting the foundation for broader strategic market development.

The Alzheimer’s Disease Treatments Market has become strategically important as pharmaceutical companies shift from symptomatic management toward disease-modifying therapies supported by precision diagnostics. Recent regulatory advancements have accelerated commercialization strategies, while biologics manufacturing expansion and specialized infusion infrastructure are reshaping competitive dynamics. Companies are strengthening supply-chain resilience for complex biologic products and expanding collaborations with diagnostic providers to improve patient identification and treatment readiness.

Advanced blood-based biomarker testing delivers diagnostic workflows approximately 40% faster than conventional multi-stage evaluation pathways while reducing dependence on costly imaging procedures. North America remains the largest deployment market due to established reimbursement systems and advanced neurology networks, whereas Asia-Pacific is rapidly expanding through healthcare infrastructure modernization, increasing dementia screening programs, and broader access to specialist care. Over the next two to three years, adoption of integrated digital patient-monitoring platforms is expected to increase by more than 25% across leading treatment centers.

Leading pharmaceutical companies are expanding manufacturing investments, forming strategic partnerships with diagnostic developers, and increasing clinical trial capacity to strengthen product portfolios. Integrated care models combining biologic therapies, AI-supported diagnostics, and longitudinal patient monitoring are improving operational efficiency and treatment continuity. Organizations that build scalable diagnostic ecosystems and robust commercialization capabilities will establish stronger competitive positioning and sustainable long-term market leadership.

The rapid adoption of disease-modifying Alzheimer’s therapies is reshaping treatment strategies, supported by biomarker-driven diagnosis and advanced biologics development. FDA approvals for targeted therapies have accelerated commercialization, with U.S. clinical centers increasing biomarker testing capacity by more than 30% since 2023. Pharmaceutical companies are expanding manufacturing networks and forming diagnostic partnerships to improve patient identification. Japan and Germany are also increasing dementia-care investments, strengthening early intervention models. The shift from symptomatic drugs toward precision therapeutics is creating operational advantages for companies with scalable biologics production, robust clinical trial infrastructure, and integrated patient-monitoring ecosystems.

High therapy costs, complex administration requirements, and limited specialist infrastructure remain major barriers to broader Alzheimer’s treatment deployment. Advanced antibody therapies require infusion facilities and monitoring systems, increasing operational expenses by approximately 20–35% compared with traditional medication pathways. In countries such as India and Brazil, limited access to neurologists and diagnostic infrastructure restricts treatment scalability. Pharmaceutical companies are responding through manufacturing localization, healthcare partnerships, and alternative delivery approaches to control costs. The key operational challenge is balancing innovation investment with affordability, as reimbursement uncertainty and healthcare capacity gaps directly influence adoption speed and commercial sustainability.

Emerging precision medicine platforms are creating new opportunities through blood-based biomarkers, artificial intelligence diagnostics, and remote patient monitoring solutions. AI-supported cognitive assessment tools are improving screening efficiency by nearly 25–40%, enabling earlier treatment decisions across healthcare systems. The expansion of digital health infrastructure in countries such as the United States and South Korea is accelerating connected care adoption. Companies are investing in AI partnerships, companion diagnostic development, and integrated treatment ecosystems to capture underserved patient segments. A significant opportunity lies in combining diagnostics with therapeutic platforms, allowing providers to optimize treatment selection, reduce unnecessary procedures, and improve long-term care efficiency.

Scaling Alzheimer’s treatment programs requires overcoming clinical integration challenges, specialist shortages, and evolving regulatory requirements. Approximately 50% of global dementia patients still lack timely diagnosis pathways, creating significant pressure on healthcare delivery systems. Countries including Japan and the United Kingdom are expanding workforce training programs, but neurologist availability remains a critical limitation. Companies must address complex treatment monitoring requirements, electronic health record integration, and patient adherence management through technology investments and healthcare collaborations. The long-term competitive challenge is building sustainable care infrastructure that supports consistent therapy delivery while maintaining data security, operational efficiency, and regulatory compliance.

AI-Enabled Diagnostic Integration: Healthcare systems are rapidly deploying AI-based imaging analysis and digital cognitive assessment platforms, improving diagnostic workflow speed by 30–40%. Hospitals in the United States are integrating automated screening tools with electronic health records, reducing specialist workload by nearly 25%. Pharmaceutical companies are partnering with AI firms to strengthen patient identification pipelines and improve clinical trial recruitment efficiency.

Biomarker Testing Expansion: Blood-based biomarker adoption is accelerating as laboratories transition toward faster Alzheimer’s screening workflows, with testing efficiency improving by approximately 35% compared with traditional evaluation pathways. Regulatory acceptance of biomarker-driven diagnosis is reshaping clinical operations, while companies are scaling companion diagnostic partnerships to support targeted therapy deployment and reduce dependence on complex imaging infrastructure.

Specialty Care Network Growth: Pharmaceutical firms are expanding infusion centers and neurology partnerships to support increasing demand for advanced therapies, with specialty treatment networks growing by nearly 20% in major healthcare markets. The shift toward decentralized care models is improving patient access, while companies are restructuring distribution strategies to strengthen treatment availability outside major academic hospitals.

Digital Patient Monitoring Adoption: Connected care platforms and remote monitoring tools are gaining traction, improving adherence tracking and caregiver engagement by more than 25%. Healthcare providers in countries such as Japan are integrating digital dementia-care solutions into aging population programs. Companies are investing in software ecosystems that combine therapy management, patient analytics, and long-term care coordination to improve operational continuity.

Disease-modifying therapies represent the leading type segment in the Alzheimer’s Disease Treatments Market due to their ability to address underlying disease mechanisms rather than only managing symptoms. Monoclonal antibody-based treatments dominate adoption, supported by improved clinical validation, regulatory acceptance, and increasing investment in biologics manufacturing. This segment captures significant demand from specialized healthcare providers, with adoption increasing by approximately 30% in advanced treatment centers. Traditional symptomatic therapies remain important because of established usage patterns and lower accessibility barriers, but their market influence is gradually shifting as precision medicine advances. The fastest-growing type is expected to be next-generation targeted therapies, driven by biomarker-based patient selection and combination treatment strategies. Companies are expanding research partnerships, improving biologics production capabilities, and investing in personalized treatment platforms. Emerging therapy categories are gaining traction as pharmaceutical firms prioritize higher efficacy profiles and differentiated clinical outcomes, creating new competitive pathways across mature and developing healthcare systems.

Therapeutic treatment remains the leading application segment as healthcare providers prioritize disease management through pharmacological interventions, specialist care pathways, and long-term patient monitoring. Demand concentration is highest in hospitals, neurology clinics, and specialized treatment centers where advanced therapies require structured administration. Adoption of integrated treatment workflows has increased by nearly 35% in developed healthcare systems as providers combine diagnostics, medication management, and monitoring platforms. Diagnostic and monitoring applications represent the fastest-growing area, supported by AI-enabled cognitive assessment, biomarker testing, and digital health integration. These applications are improving early-stage identification and enabling more efficient therapy selection. Companies are expanding partnerships with diagnostic technology providers and healthcare networks to strengthen deployment capabilities. Emerging applications, including remote monitoring and personalized care management, are becoming operationally important as healthcare systems seek scalable dementia-care solutions.

Hospitals represent the leading end-user segment due to their extensive diagnostic infrastructure, specialist availability, and ability to administer complex Alzheimer’s therapies. Large healthcare institutions in the United States, Germany, and Japan are expanding neurology departments and treatment capabilities, with advanced care facilities increasing specialized dementia service capacity by approximately 20%. Hospitals maintain strong demand because they provide integrated diagnosis, therapy administration, and patient monitoring within centralized systems. Specialty clinics and research centers are the fastest-growing end-user groups as treatment complexity increases and personalized medicine adoption expands. These facilities are gaining importance through focused expertise, faster patient processing, and clinical trial participation. Pharmaceutical companies are building partnerships with specialty providers, offering training programs and customized support models. Long-term care facilities and research organizations continue contributing through patient management and innovation activities, but future demand is shifting toward specialized, technology-enabled care environments.

North America accounted for the largest market share at 46% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America maintains market leadership through strong pharmaceutical commercialization, advanced neurology infrastructure, and rapid adoption of disease-modifying Alzheimer’s therapies. The region contributes approximately 46% of global demand, supported by concentrated clinical research networks and specialized treatment centers across the United States and Canada. More than 60% of late-stage Alzheimer’s clinical trials involve North American research facilities, strengthening innovation pipelines. Companies are expanding biologics manufacturing, forming diagnostic partnerships, and investing in AI-supported patient identification platforms to improve therapy access and operational efficiency.

United States Market Outlook: The United States represents the primary growth engine due to strong biotechnology capabilities, regulatory support, and healthcare spending capacity. More than 50 million Americans undergo annual Medicare-supported healthcare assessments linked to aging-related conditions, creating a significant infrastructure base for Alzheimer’s diagnosis and treatment expansion. Pharmaceutical companies are increasing investment in specialty clinics, biomarker testing, and advanced therapeutic commercialization.

Europe is strengthening its position through coordinated dementia strategies, advanced healthcare systems, and increasing adoption of precision medicine approaches. The region accounts for approximately 28% of market activity, supported by strong research capabilities in countries such as Germany, the United Kingdom, and France. European healthcare providers are expanding biomarker testing networks, with digital health adoption improving clinical workflow efficiency by nearly 25%. Regulatory harmonization and public-private research collaborations are encouraging pharmaceutical companies to expand clinical programs and strengthen localized treatment ecosystems.

Germany Market Outlook: Germany remains a strategic European market due to its advanced hospital infrastructure, pharmaceutical manufacturing base, and strong clinical research environment. The country operates more than 400 specialized dementia care facilities, supporting broader therapy deployment. Companies are investing in research partnerships, diagnostic integration, and healthcare digitization to improve patient management efficiency and treatment accessibility.

Asia-Pacific is emerging as the fastest-expanding market due to rising elderly populations, healthcare modernization, and increased investment in neurological research. The region contributes approximately 18% of current market activity but demonstrates strong adoption potential through expanding diagnostic infrastructure. Japan and China are accelerating dementia-care initiatives, with Japan deploying digital healthcare solutions across aging-care networks. Companies are increasing regional partnerships, expanding clinical trial capabilities, and developing localized access models to address growing treatment requirements.

Japan Market Outlook: Japan holds a leading position due to its aging population, healthcare innovation ecosystem, and government-supported dementia programs. More than 29% of the population is above 65 years, creating strong demand for advanced Alzheimer’s management solutions. Pharmaceutical companies are focusing on precision diagnostics, digital monitoring platforms, and specialized care partnerships to improve treatment delivery.

South America is gradually expanding Alzheimer’s treatment capabilities through healthcare infrastructure improvements, increasing awareness programs, and specialist network development. The region represents approximately 5% of global demand, with Brazil and Argentina accounting for major treatment activity. Limited specialist availability and uneven diagnostic access remain operational challenges, but investments in telemedicine and healthcare partnerships are improving coverage. Companies are adapting strategies through localized distribution models, physician training programs, and collaborations with regional healthcare providers.

Brazil Market Outlook: Brazil is the largest South American healthcare market and provides the strongest opportunity base for Alzheimer’s treatment expansion. The country has more than 30 million people aged over 60, increasing demand for dementia-care solutions. Pharmaceutical companies are strengthening partnerships with hospitals, expanding awareness initiatives, and improving access to diagnostic technologies.

The Middle East & Africa market is developing through healthcare modernization programs, investment in specialty hospitals, and increasing adoption of advanced diagnostic technologies. The region contributes approximately 3% of global market activity, with growth concentrated in Saudi Arabia, the United Arab Emirates, and South Africa. Healthcare transformation initiatives are improving digital health adoption, while private-sector investments are expanding specialized neurological services. Companies are entering partnerships with healthcare networks to improve treatment accessibility and establish localized care pathways.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic healthcare investment hub through modernization programs and expanding specialty care infrastructure. The country is increasing healthcare technology adoption, with digital transformation initiatives supporting faster patient management workflows. Pharmaceutical companies are targeting partnerships with hospitals and research institutions to strengthen Alzheimer’s diagnosis, treatment capacity, and long-term healthcare delivery.

The Alzheimer’s Disease Treatments Market features intense competition between global pharmaceutical leaders and emerging biotechnology innovators. Key players include Eli Lilly and Company, Biogen Inc., Eisai Co., Ltd., Roche Holding AG, and Novartis AG, with top five companies estimated to control nearly 55% of market influence. Competition centers on therapeutic efficacy, biomarker integration, manufacturing scale, and treatment accessibility. Leading firms are improving clinical pipelines, expanding biologics production, and forming diagnostic partnerships. Technology-focused innovators compete through AI-enabled discovery and precision medicine, while established pharmaceutical companies leverage regulatory expertise. Current competition is shifting toward combination therapies, supply-chain control, and patient-access models. High clinical trial costs and regulatory complexity remain major entry barriers. Winning requires superior therapeutic outcomes, scalable manufacturing, and integrated diagnostic ecosystems.

Biogen Inc.

Eisai Co., Ltd.

Roche Holding AG

Novartis AG

Merck & Co., Inc.

Johnson & Johnson

AbbVie Inc.

AstraZeneca PLC

Otsuka Pharmaceutical Co., Ltd.

Takeda Pharmaceutical Company Limited

Alzheon, Inc.

The Alzheimer’s Disease Treatments Market is being transformed by AI-powered drug discovery, biomarker diagnostics, and precision medicine platforms. AI-based analysis of neurological imaging and patient datasets improves clinical trial efficiency by approximately 25%, while digital cognitive assessment tools reduce evaluation timelines by nearly 30% compared with traditional workflows. Pharmaceutical companies are integrating machine learning into target identification, patient stratification, and clinical development processes to improve decision accuracy.

Blood-based biomarkers and advanced imaging technologies represent major shifts from conventional diagnostic pathways. Modern biomarker platforms improve early disease identification speed by around 40% compared with older diagnostic approaches dependent on extensive imaging procedures. Adoption of biomarker-guided treatment selection is increasing across specialized healthcare centers, allowing companies to optimize therapy allocation and reduce unnecessary clinical costs.

Between 2026 and 2028, AI-driven personalized treatment models, automated patient monitoring, and combination therapy platforms will define competitive advantage. Companies with integrated technology ecosystems benefit through faster trials, improved patient engagement, and scalable care delivery. The competitive edge will move toward organizations combining therapeutics, diagnostics, and digital infrastructure rather than relying on standalone drug innovation.

July 2025, Eli Lilly and Company received FDA approval for an updated Kisunla dosing schedule, reducing ARIA-E incidence while maintaining treatment performance. The adjustment strengthened patient safety management and improved therapy administration flexibility. Source: www.investor.lilly.com

August 2025, Biogen Inc. and Eisai Co., Ltd. gained FDA approval for LEQEMBI IQLIK subcutaneous maintenance dosing, introducing at-home administration after initial therapy. The innovation expanded patient convenience and reduced infusion-center dependency.

September 2025, Eli Lilly and Company secured European Commission marketing authorization for Kisunla (donanemab) for early symptomatic Alzheimer’s disease. The approval expanded global treatment access and strengthened Lilly’s disease-modifying therapy position.

September 2025, Biogen Inc. and Eisai Co., Ltd. achieved Australian approval for LEQEMBI, expanding international availability. The regulatory milestone supported broader commercialization strategies across developed healthcare markets.

The Alzheimer’s Disease Treatments Market Report provides comprehensive coverage across therapy types, applications, end-users, and global regions. The analysis evaluates disease-modifying therapies, symptomatic treatments, diagnostic-linked applications, hospitals, specialty clinics, research institutions, and long-term care providers. Regional assessment includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting adoption patterns, infrastructure maturity, and healthcare transformation trends.

The report examines emerging technologies including AI-based diagnostics, biomarker platforms, digital monitoring systems, and precision medicine approaches. Covering strategic developments among major pharmaceutical companies and biotechnology innovators, the study supports investment planning, expansion decisions, competitive positioning, and partnership evaluation. It provides insights into evolving treatment models, technology adoption, and market direction through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 550.0 Million |

| Market Revenue (2033) | USD 1,079.1 Million |

| CAGR (2026–2033) | 8.79% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Eli Lilly and Company; Biogen Inc.; Eisai Co., Ltd.; Roche Holding AG; Novartis AG; Merck & Co., Inc.; Johnson & Johnson; AbbVie Inc.; AstraZeneca PLC; Otsuka Pharmaceutical Co., Ltd.; Takeda Pharmaceutical Company Limited; Alzheon, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |