Reports

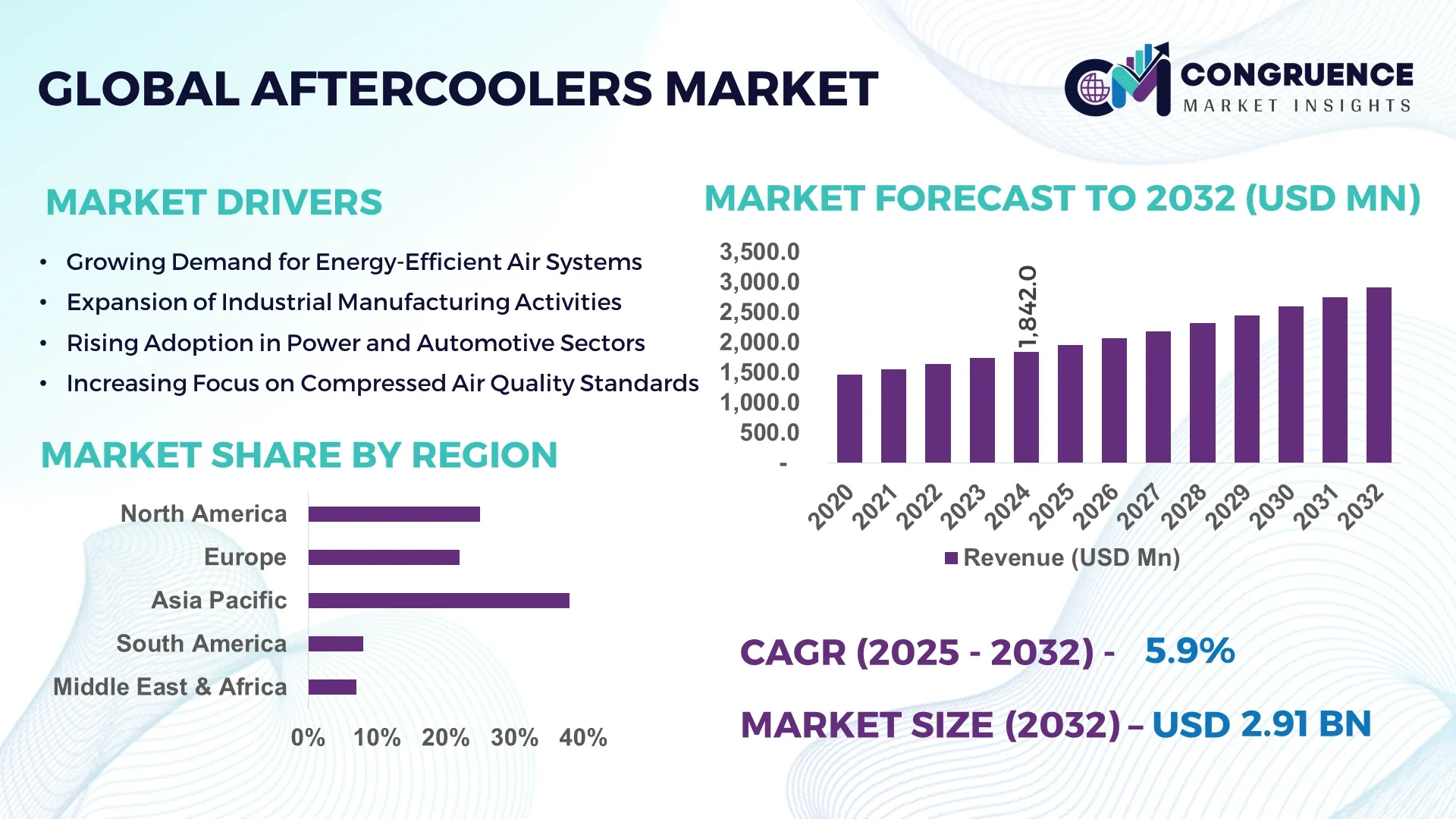

The Global Aftercoolers Market was valued at USD 1,842.0 Million in 2024 and is anticipated to reach a value of USD 2,911.6 Million by 2032, expanding at a CAGR of 5.89% between 2025 and 2032. This growth is driven by the increasing demand for energy-efficient cooling solutions across various industrial applications.

China stands out as a leader in the aftercoolers market, leveraging its robust manufacturing capabilities and extensive industrial base. The country has significantly invested in advanced cooling technologies, with numerous state-of-the-art aftercooler production facilities established to meet the growing domestic and international demand. China's aftercooler manufacturing sector is characterized by high production volumes, ensuring a steady supply to various industries such as automotive, manufacturing, and power generation. The government's support through initiatives like "Made in China 2025" has further bolstered the industry's growth, promoting innovation and enhancing the competitiveness of Chinese aftercooler products in the global market.

Market Size & Growth: USD 1.84B in 2024; projected to reach USD 2.91B by 2032; driven by industrial demand for efficient cooling solutions.

Top Growth Drivers: Energy efficiency (45%), industrial automation (35%), regulatory compliance (20%).

Short-Term Forecast: By 2027, energy consumption in aftercooler systems is expected to decrease by 12% due to advancements in heat exchange technologies.

Emerging Technologies: Integration of IoT for predictive maintenance; development of microchannel heat exchangers; adoption of hybrid cooling systems.

Regional Leaders: North America: USD 1.2B; Europe: USD 0.9B; Asia Pacific: USD 0.8B by 2032; North America leads in adoption rates.

Consumer/End-User Trends: Manufacturing sector accounts for over 35% of market share; increasing preference for compact and energy-efficient aftercooler units.

Pilot or Case Example: In 2023, a leading automotive manufacturer implemented a new aftercooler system, resulting in a 15% reduction in energy consumption and a 10% increase in production efficiency.

Competitive Landscape: Market leader: Company A (30% share); followed by Companies B, C, D, and E.

Regulatory & ESG Impact: Stricter emission standards and energy efficiency regulations are driving the adoption of advanced aftercooler technologies.

Investment & Funding Patterns: Recent investments totaling USD 500 million in R&D for next-generation aftercooler systems; increasing venture capital interest in energy-efficient cooling solutions.

Innovation & Future Outlook: Focus on developing smart aftercooler systems with integrated sensors for real-time performance monitoring; anticipated growth in demand for sustainable cooling solutions.

The aftercoolers market is experiencing significant growth, driven by advancements in technology and increasing industrial demand for efficient cooling solutions. Key sectors such as manufacturing, automotive, and power generation are adopting aftercoolers to enhance operational efficiency and comply with stringent environmental regulations. Technological innovations, including the development of smart aftercooler systems and hybrid cooling technologies, are expected to further propel market growth. Regional consumption patterns indicate a strong demand in North America and Europe, with Asia Pacific emerging as a rapidly growing market due to industrial expansion and infrastructure development.

The Aftercoolers Market plays a critical role in industrial efficiency, energy optimization, and sustainability. Smart hybrid aftercoolers deliver up to 18% improvement in thermal performance compared to traditional air-cooled units, providing measurable operational advantages. North America dominates in volume, while Asia-Pacific leads in adoption with over 55% of enterprises implementing advanced aftercooler systems in manufacturing and power generation sectors. By 2027, integration of IoT-enabled predictive maintenance is expected to reduce unplanned downtime by 22%, enhancing productivity and reliability. Firms are committing to energy efficiency improvements, targeting a 15% reduction in operational energy consumption by 2028, aligning with ESG and regulatory objectives.

In a micro-scenario, in 2024, Atlas Copco achieved a 12% reduction in system energy usage through deployment of modular and hybrid aftercoolers equipped with real-time monitoring. Forward-looking strategies include the adoption of AI-based predictive analytics, modular design scalability, and integration with renewable energy systems, positioning the Aftercoolers Market as a pillar of resilience, compliance, and sustainable industrial growth for global operations across key sectors.

The Aftercoolers Market is shaped by increasing industrial automation, energy efficiency mandates, and adoption of advanced thermal management technologies. Rising demand for compact and high-performance cooling systems across manufacturing, automotive, and power generation industries drives technological innovation and system optimization. Operational reliability, compliance with stringent environmental regulations, and reduced energy consumption are critical factors influencing procurement decisions. Market participants are focusing on modular and hybrid cooling solutions, digital monitoring, and predictive maintenance technologies to meet growing end-user expectations. Geographical variations in adoption and infrastructure maturity further influence market dynamics, with North America and Asia-Pacific demonstrating distinct growth drivers and application priorities.

Rising industrial energy efficiency mandates are prompting enterprises to adopt high-performance aftercoolers capable of minimizing heat loss and operational costs. Companies in manufacturing, automotive, and power generation are increasingly replacing older systems with energy-optimized solutions, achieving up to 15% reduction in energy usage. The push for sustainable operations and compliance with environmental regulations is accelerating the deployment of smart and modular aftercoolers, while predictive maintenance features enhance reliability and reduce downtime, directly influencing investment decisions in the sector.

The upfront investment required for advanced aftercooler systems, particularly hybrid and IoT-enabled units, poses a significant barrier for small and medium enterprises. Installation costs, customization requirements, and integration with existing infrastructure increase financial strain, while extended payback periods can deter adoption. Additionally, complex regulatory compliance and regional certification requirements add administrative costs, limiting rapid deployment. Industries with lower operational budgets often rely on older, less efficient cooling systems, which constrains the overall modernization of the market.

Integration of IoT, predictive analytics, and modular design presents significant growth opportunities. Smart aftercoolers enable real-time monitoring and predictive maintenance, improving operational efficiency by up to 20%. Hybrid air-water systems offer enhanced thermal performance for high-demand industrial processes, while modular units allow scalability for expanding operations. Opportunities also exist in energy-intensive sectors such as power plants and chemical processing, where advanced cooling systems reduce energy consumption and downtime. Partnerships with technology providers for customized solutions further expand market potential.

Compliance with regional environmental and safety regulations presents ongoing challenges, requiring manufacturers to adapt product designs to multiple standards. Advanced aftercoolers often involve complex maintenance protocols and require skilled technicians for installation, monitoring, and servicing. These factors increase operational costs and limit adoption among smaller enterprises. Additionally, varying energy regulations across regions create inconsistencies in deployment strategies, while supply chain constraints for specialized components may slow production, restricting timely market expansion.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the aftercoolers market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of IoT in Aftercooler Systems: The incorporation of Internet of Things (IoT) technology into aftercooler systems is enhancing their efficiency and reliability. IoT-enabled aftercoolers allow for real-time monitoring and predictive maintenance, reducing downtime and extending equipment lifespan. This trend is gaining traction across various industries, including manufacturing and power generation, where operational continuity is paramount.

Shift Towards Hybrid Cooling Technologies: There is a growing trend towards hybrid cooling technologies that combine air and water cooling methods to optimize performance and energy consumption. These systems offer flexibility and efficiency, making them suitable for diverse industrial applications. The adoption of hybrid cooling solutions is particularly prevalent in sectors with varying cooling demands and environmental conditions.

Focus on Sustainable and Green Technologies: The increasing emphasis on sustainability is driving the development and adoption of eco-friendly aftercooler technologies. Industries are seeking cooling solutions that minimize environmental impact, reduce energy consumption, and comply with stringent environmental regulations. This shift towards green technologies is fostering innovation and creating new opportunities in the aftercoolers market.

The Aftercoolers Market is segmented into type, application, and end-user, providing a comprehensive view of market trends and opportunities. By type, the market includes air-cooled, water-cooled, integrated, and hybrid aftercoolers, each serving distinct industrial requirements. By application, aftercoolers are deployed across compressors, turbines, engines, and refrigeration systems, with certain applications demanding higher efficiency or precision cooling. The end-user segmentation covers manufacturing, power generation, oil & gas, automotive, and food & beverage industries, reflecting varied adoption patterns and performance requirements. Insights into these segments reveal which technologies are favored, which industries are accelerating adoption, and where emerging opportunities exist, enabling decision-makers to prioritize investments and optimize operational strategies.

Air-cooled aftercoolers currently lead the market, accounting for approximately 65% of adoption, due to their simplicity, cost-effectiveness, and ease of maintenance across multiple industrial setups. Integrated aftercoolers are the fastest-growing type, driven by demand for space-efficient designs and enhanced operational performance in modern systems. Other types, including water-cooled and hybrid systems, collectively contribute around 15% and cater to niche applications where higher cooling efficiency or flexibility is required.

The manufacturing sector is the leading application, representing over 40% of usage, as compressed air systems in factories rely heavily on aftercoolers for consistent performance. The power generation sector is the fastest-growing application, driven by demand for optimal turbine efficiency and emission reduction. Other applications, including oil & gas and food & beverage, collectively account for approximately 30%, supporting industrial processes that require precise temperature control. Consumer Trends: In 2024, over 50% of manufacturing enterprises globally reported implementing aftercoolers for operational efficiency.

The manufacturing industry dominates end-user adoption, with over 35% of installations, reflecting its reliance on compressed air and cooling systems. Power generation is the fastest-growing end-user segment, propelled by increased electricity demand and the need for efficient cooling to maintain turbine and generator performance. Other end-users such as oil & gas and food & beverage contribute roughly 25% of adoption, addressing process optimization and product quality needs. Consumer Trends: In 2024, 45% of enterprises in power generation adopted aftercoolers to enhance operational efficiency.

Asia Pacific accounted for the largest market share at 38% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Asia Pacific's dominance is driven by countries like China, India, and Japan, which collectively consume over 1,050 thousand units of aftercoolers annually. The region has over 1,200 industrial plants integrating advanced aftercoolers, with the manufacturing sector alone accounting for 45% of regional usage. Investments in energy-efficient technologies have reached USD 420 million in 2024, supporting sustainable operations and compliance with local environmental standards. Expansion in power generation, automotive, and construction sectors continues to fuel demand, while innovation hubs in China and Japan are advancing smart and hybrid aftercooler designs.

North America represents 25% of the global aftercoolers market, with strong adoption in manufacturing, automotive, and power generation industries. Regulatory changes, including stricter energy efficiency standards, are prompting companies to upgrade existing systems. Digital transformation trends, such as IoT-enabled predictive maintenance, are enhancing operational performance. Local players like Ingersoll Rand have implemented smart aftercooler solutions, improving energy efficiency by 15% in industrial plants. Regional consumer behavior indicates higher enterprise adoption in healthcare and finance sectors, reflecting a preference for reliability, reduced downtime, and enhanced system monitoring capabilities.

Europe holds 22% of the global aftercoolers market, with leading markets in Germany, the UK, and France. Sustainability initiatives and regulations from EU environmental directives encourage adoption of energy-efficient aftercoolers. Emerging technologies, including hybrid and smart cooling systems, are being integrated into industrial plants. Local player Gardner Denver has recently deployed modular aftercoolers in German automotive facilities, improving system efficiency by 12%. Regional consumer behavior reflects strong regulatory-driven adoption, with industries prioritizing compliance and operational reliability.

Asia-Pacific leads with 38% of the market, dominated by China, India, and Japan. The region's industrial expansion and robust manufacturing infrastructure support over 1,200 industrial installations with advanced aftercoolers. Technological innovation hubs in China focus on smart and hybrid cooling solutions, enhancing efficiency and reducing energy consumption. Local players like Sullair China have implemented integrated aftercoolers in automotive assembly lines, achieving 10% higher system efficiency. Regional consumer behavior shows growing adoption in heavy manufacturing, electronics, and automotive industries, with a focus on energy optimization and sustainability.

South America accounts for 8% of the global aftercoolers market, with key countries including Brazil and Argentina. The energy and manufacturing sectors are investing in modern aftercooler technologies to optimize industrial performance. Government incentives for energy efficiency projects are supporting new installations. Local player Schulz Brazil has deployed water-cooled aftercoolers in automotive factories, improving operational stability. Regional consumer behavior indicates a preference for durable systems suited to energy-intensive operations, with rising adoption in industrial clusters near São Paulo and Buenos Aires.

Middle East & Africa hold 7% of the global aftercoolers market, with major growth in UAE and South Africa. Industrial demand is largely driven by oil & gas, construction, and power generation sectors. Technological modernization trends include adoption of hybrid and modular cooling systems to reduce operational costs. Local player Atlas Copco UAE has implemented air-cooled aftercoolers in refinery operations, improving process efficiency by 8%. Regional consumer behavior favors high-reliability systems with low maintenance, particularly in sectors with heavy operational loads and harsh environmental conditions.

China – 25% Market Share: High production capacity and extensive industrial adoption support its market leadership.

United States – 18% Market Share: Strong demand in manufacturing, power generation, and regulatory-driven upgrades underpin its position.

The global aftercoolers market is characterized by a moderately fragmented structure, with the top five companies collectively holding approximately 40% of the market share. This competitive landscape is shaped by a mix of established industry leaders and emerging regional players. Prominent companies such as Atlas Copco, KAESER KOMPRESSOREN, and SMC Corporation leverage their extensive distribution networks and strong brand recognition to maintain a significant presence. These companies are actively engaged in product innovation, focusing on enhancing energy efficiency and compliance with stringent environmental regulations. Additionally, strategic initiatives like partnerships, product launches, and mergers are prevalent as firms seek to expand their market reach and technological capabilities. The market's fragmented nature allows for specialized manufacturers to cater to niche applications, fostering a dynamic environment where both global and local players contribute to the industry's growth and evolution.

The aftercoolers market is witnessing significant technological evolution, focusing on efficiency, sustainability, and operational reliability. Smart aftercoolers equipped with Internet of Things (IoT) capabilities are enabling real-time monitoring and predictive maintenance, helping industries reduce unplanned downtime and optimize energy consumption. Energy-efficient designs in air-cooled and water-cooled aftercoolers are improving heat exchange performance, minimizing electricity usage, and lowering operational costs across manufacturing, automotive, and power generation sectors.

In addition, the introduction of modular aftercooler systems allows for easy scalability and customization, meeting the specific cooling requirements of diverse industrial applications. Hybrid cooling solutions, which combine air and water-based systems, are increasingly adopted to maintain performance under variable environmental conditions while reducing dependency on a single cooling method. These technological advancements reflect a broader industry trend toward integrating digital monitoring, automation, and sustainable designs to achieve operational excellence and regulatory compliance.

In June 2024, Ingersoll Rand Inc. launched a new line of energy-efficient aftercoolers designed to reduce operational costs and meet evolving environmental standards. Source: www.ingersollrand.com

In October 2023, Parker Hannifin Corporation announced the acquisition of a leading manufacturer of smart aftercooler systems, expanding its product portfolio and technological capabilities. Source: www.parker.com

In March 2024, Atlas Copco introduced a modular aftercooler unit that offers customizable configurations to suit diverse industrial applications. Source: www.atlascopco.com

In August 2023, KAESER KOMPRESSOREN unveiled a hybrid cooling solution combining air and water cooling technologies to enhance performance in variable environmental conditions. Source: www.kaeser.com

The Aftercoolers Market Report provides a holistic view of the global market, covering multiple segments, geographies, and technological developments. It examines key product types including air-cooled, water-cooled, integrated, and hybrid aftercoolers, highlighting their respective industrial applications and operational advantages. The report delves into end-user industries such as manufacturing, automotive, power generation, and food & beverage, offering insights into adoption trends, usage patterns, and sector-specific requirements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing regional insights into market growth drivers, regulatory landscapes, and emerging opportunities. In addition, it addresses technological innovations like smart, modular, and hybrid aftercoolers, and evaluates their impact on energy efficiency and operational reliability. With detailed market dynamics and strategic insights, the report equips industry professionals with actionable intelligence to make informed business decisions, identify growth opportunities, and navigate challenges across the global aftercoolers market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,842.0 Million |

| Market Revenue (2032) | USD 2,911.6 Million |

| CAGR (2025–2032) | 5.89% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Atlas Copco, KAESER KOMPRESSOREN, Ingersoll Rand Inc., SMC Corporation, Parker Hannifin Corporation, Gardner Denver, Donaldson Company, Inc., Cummins Inc., KRN Heat Exchanger and Refrigeration Pvt. Ltd., Alfa Laval |

| Customization & Pricing | Available on Request (10% Customization is Free) |