Reports

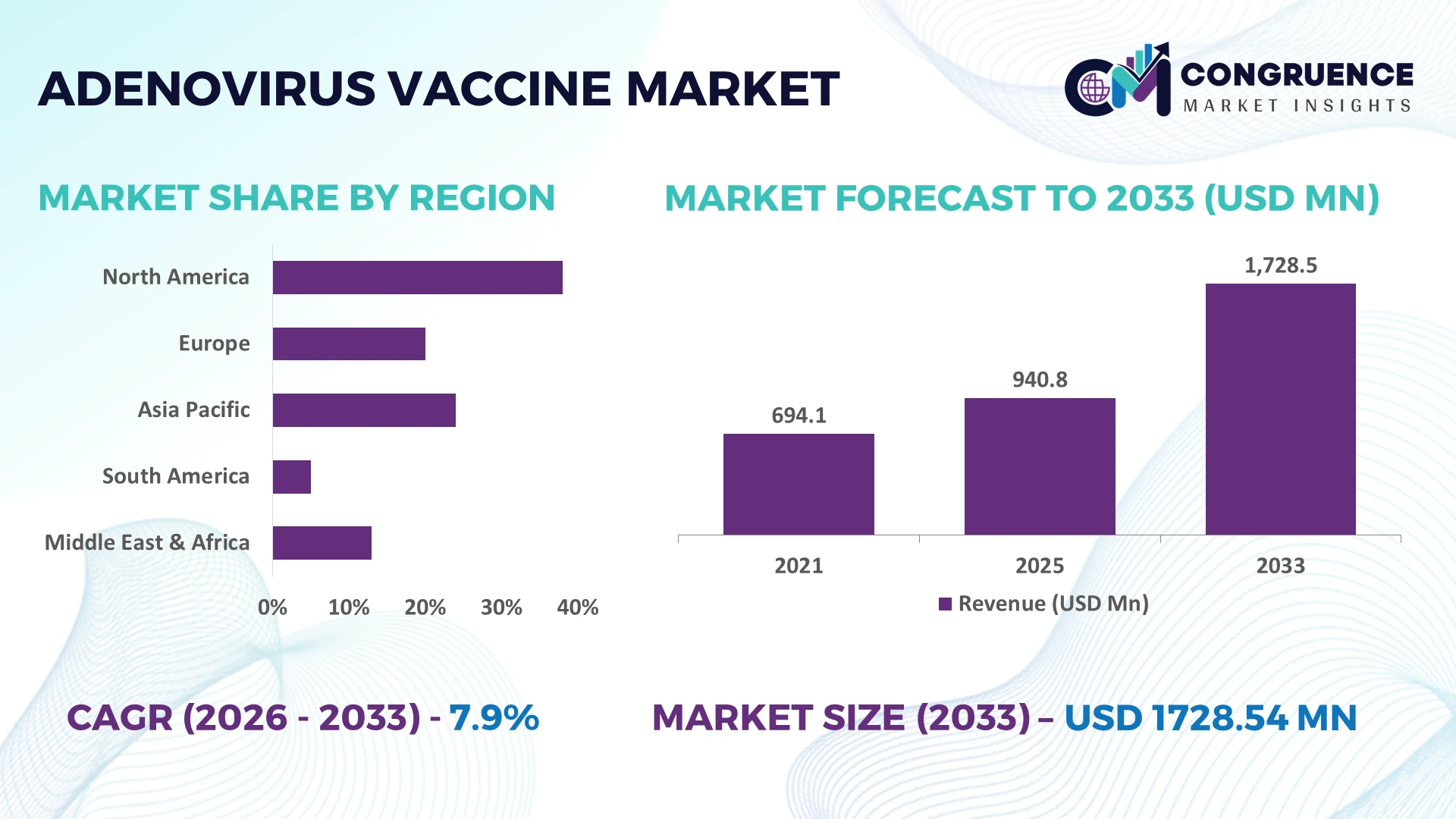

The Global Adenovirus Vaccine Market was valued at USD 940.82 Million in 2025 and is anticipated to reach a value of USD 1728.54 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Growth is driven by expanding viral vector vaccine manufacturing, military immunization programs, and increasing investments in next-generation adenoviral platform technologies for infectious diseases and therapeutic applications.

The United States remains the dominant country, accounting for approximately 42% of global adenovirus vaccine production capacity, supported by advanced biomanufacturing infrastructure, defense healthcare programs, and biotechnology investments exceeding USD 3 billion in viral vector manufacturing. Compared with China, where production capacity has expanded by nearly 18% through government-backed vaccine facilities, the U.S. maintains stronger regulatory readiness and clinical development capabilities amid evolving global biosecurity priorities and post-pandemic preparedness initiatives.

Strategic expansion of regional manufacturing and diversified viral vector capabilities will define long-term competitive positioning across the global adenovirus vaccine market.

Market Size & Growth: USD 940.82 Million in 2025 to USD 1728.54 Million by 2033 at 7.9% CAGR, supported by advanced viral vector manufacturing and expanded immunization programs.

Top Growth Drivers: Viral vector platform adoption +24%, government vaccine preparedness funding +18%, biologics manufacturing expansion +21% accelerate market momentum.

Short-Term Forecast: By 2028, production efficiency improves 16% while manufacturing turnaround time declines 14% through process automation.

Emerging Technologies: AI-assisted antigen design, continuous bioprocessing, and advanced cell-culture platforms improve development speed by nearly 20%.

Regional Leaders: North America exceeds USD 690 Million, Europe approaches USD 430 Million, Asia-Pacific surpasses USD 380 Million, driven by regional manufacturing expansion.

Consumer/End-User Trends: More than 62% of institutional procurement focuses on strategic stockpiling and high-priority immunization programs.

Pilot/Case Example: In 2026, automated viral vector manufacturing initiatives improved batch consistency by approximately 22%, strengthening supply resilience.

Competitive Landscape: Top manufacturers collectively control nearly 58% of global capacity, with leadership supported by AstraZeneca, CanSino Biologics, Bharat Biotech, Emergent BioSolutions, and Serum Institute.

Regulatory & ESG Impact: Sustainable manufacturing initiatives reduce production waste by approximately 15% while accelerated regulatory pathways shorten review timelines.

Investment & Funding: More than USD 2.5 Billion supports manufacturing expansion, strategic partnerships, and regional supply-chain localization across high-growth markets.

Innovation & Future Outlook: Next-generation adenoviral vectors, thermostable formulations, and precision manufacturing strengthen long-term commercialization and global vaccine resilience.

Rising demand for adenovirus vaccine platforms extends beyond infectious disease prevention into oncology research and emerging therapeutic applications. Manufacturing innovations, including scalable viral vector production and improved formulation technologies, enhance operational efficiency by approximately 19%, while regional supply-chain diversification and evolving regulatory preparedness in 2026 strengthen product availability, creating a solid foundation for the strategic market assessment that follows.

The Adenovirus Vaccine Market has become strategically important as governments, biotechnology companies, and contract manufacturing organizations prioritize rapid-response vaccine platforms capable of supporting infectious disease preparedness and therapeutic innovation. Supply-chain restructuring since the pandemic has accelerated localized viral vector manufacturing, while updated regulatory frameworks are reducing technology transfer timelines. These developments strengthen manufacturing resilience, improve procurement security, and intensify competition among companies seeking long-term strategic partnerships and production capacity.

Modern suspension-cell bioprocessing delivers approximately 28% higher production efficiency than conventional adherent-cell manufacturing while reducing batch preparation time by nearly 18%, improving operational productivity across commercial facilities. The United States leads large-scale manufacturing and advanced clinical deployment, whereas China continues expanding high-capacity production infrastructure and domestic technology integration through state-supported biotechnology investments. Over the next two to three years, digital manufacturing systems and automated quality analytics are expected to increase production consistency by around 20%, supporting faster product release and stronger supply reliability.

A practical example is the expansion of dedicated viral vector manufacturing lines integrated with automated quality monitoring, enabling manufacturers to improve batch utilization while supporting multiple vaccine candidates from shared infrastructure. Companies are increasing investments in flexible manufacturing facilities, strategic licensing agreements, and regional production partnerships to reduce operational risk. Organizations establishing scalable manufacturing ecosystems and diversified technology capabilities will secure stronger competitive positioning and long-term strategic relevance.

The strongest market driver is the rapid expansion of viral vector manufacturing supported by national healthcare preparedness programs and biotechnology investments. Automated bioprocessing has improved production productivity by approximately 24%, while continuous manufacturing technologies reduce processing time by nearly 17%. In the United States, expanded domestic biologics manufacturing initiatives are strengthening vaccine supply resilience and reducing dependence on external production networks. This structural shift enables faster commercialization and more reliable institutional procurement. Companies are responding through capacity expansion, technology licensing, and partnerships with contract development and manufacturing organizations to improve manufacturing flexibility. A key strategic advantage is the ability to utilize shared viral vector infrastructure across multiple vaccine and therapeutic programs, improving long-term asset utilization and operational efficiency.

Manufacturing complexity continues to constrain operational scalability because adenovirus vaccines require highly controlled production environments, specialized workforce expertise, and validated quality systems. Quality assurance activities account for nearly 22% of manufacturing operations, while cold-chain logistics increase distribution costs by approximately 15% in several international markets. India and other emerging manufacturing hubs continue expanding production capabilities but face infrastructure disparities affecting deployment consistency. These constraints reduce manufacturing flexibility and pressure operating margins during capacity expansion. Companies are mitigating risk through localized production facilities, multi-supplier procurement contracts, digital inventory management, and greater investment in thermostable formulations that reduce dependence on continuous refrigerated distribution while strengthening long-term supply security.

A significant opportunity lies in expanding adenoviral vector technologies beyond infectious disease prevention into oncology immunotherapy and personalized therapeutic platforms. Artificial intelligence-supported vector optimization shortens early-stage development cycles by nearly 25%, while improved vector engineering enhances transgene delivery efficiency by approximately 18%. The United Kingdom is strengthening advanced therapy infrastructure through integrated biotechnology research ecosystems that accelerate translational development. Companies are expanding research partnerships with academic institutions, investing in modular manufacturing facilities, and building innovation ecosystems supporting multiple therapeutic indications. An emerging strategic advantage is the ability to leverage one validated production platform across vaccines and advanced biologics, improving operational efficiency and technology commercialization.

Long-term competitiveness depends on maintaining consistent manufacturing quality while expanding production across multiple facilities and jurisdictions. Cross-site process validation can extend implementation timelines by approximately 20%, while specialized workforce shortages increase operational training requirements by nearly 16%. Germany and other established biomanufacturing centers continue facing pressure to standardize advanced digital quality systems across growing production networks. These execution challenges directly affect manufacturing consistency, technology transfer, and international regulatory compliance. Companies must strengthen digital quality management, invest in workforce development, standardize analytical platforms, and expand collaborative manufacturing networks. Organizations that successfully integrate advanced automation with harmonized quality systems will achieve stronger operational resilience and sustainable competitive differentiation.

Automated Manufacturing Expansion Automated bioprocessing platforms are increasing batch productivity by approximately 23% while reducing manual intervention by nearly 30%. Manufacturers in the United States are integrating digital process monitoring to improve batch consistency and shorten release cycles. Companies are expanding automated production lines and standardizing manufacturing workflows to strengthen supply continuity as regulatory expectations for process traceability continue to increase.

Regional Supply Network Diversification Localized production strategies have reduced international logistics dependence by around 18%, while dual-sourcing procurement models have expanded by nearly 22% across vaccine manufacturers. China and India continue strengthening domestic fill-finish capabilities to improve operational resilience. Companies are restructuring supplier networks, forming regional manufacturing partnerships, and increasing inventory flexibility to minimize disruptions caused by geopolitical trade shifts and transportation bottlenecks.

Advanced Vector Platform Integration Next-generation adenoviral vector engineering has improved antigen expression efficiency by approximately 19% and shortened preclinical optimization timelines by nearly 17%. Biotechnology developers are adopting computational design tools alongside standardized vector platforms to accelerate development workflows. Companies are increasing collaborative research programs and platform-based product strategies, enabling multiple vaccine candidates to share validated manufacturing infrastructure with lower operational complexity.

Flexible Production Facility Deployment Modular manufacturing facilities have reduced facility commissioning time by roughly 26% while improving production utilization by approximately 20%. The United Kingdom and Singapore continue expanding flexible biologics infrastructure to strengthen rapid-response capabilities. Companies are prioritizing scalable manufacturing assets, technology-transfer partnerships, and adaptable production suites that support faster product changeovers under evolving public health preparedness requirements.

Viral Vector Vaccines represent the leading segment because they combine established manufacturing capability with broad applicability across infectious diseases and therapeutic development. Standardized production platforms improve manufacturing efficiency by approximately 24%, while process harmonization reduces validation timelines by nearly 16%. Live Oral Vaccines remain strategically important for specific immunization programs requiring simplified administration, whereas Monovalent Vaccines continue supporting targeted disease prevention where focused immune responses remain operationally preferred.

Recombinant Vaccines are the fastest-growing segment as biotechnology companies prioritize precision antigen engineering and scalable platform development. Multivalent Vaccines are gaining momentum through expanded protection against multiple targets, improving program efficiency by reducing separate immunization requirements. Companies are increasing investment in recombinant platform innovation, strategic licensing agreements, and flexible manufacturing capabilities while balancing mature viral vector portfolios with emerging next-generation vaccine technologies. This shift is directing product development toward adaptable platforms capable of supporting diverse clinical pipelines and future therapeutic expansion.

Respiratory Infections remain the largest application because healthcare systems continue prioritizing rapid immunization capacity and preparedness planning. Approximately 61% of institutional procurement focuses on respiratory disease prevention, while expanded surveillance programs have improved deployment planning by nearly 18%. Military Immunization maintains stable demand through structured vaccination schedules, and Routine Vaccination supports ongoing protection for defined high-risk populations using established healthcare infrastructure.

Outbreak Control is the fastest-growing application as governments strengthen emergency response frameworks and deploy scalable vaccine stockpiles. Clinical Research continues expanding through broader therapeutic investigations using adenoviral platforms, supporting innovation beyond traditional prevention programs. Companies are increasing manufacturing flexibility, integrating digital distribution systems, and strengthening collaboration with public health organizations to improve deployment speed and inventory management. These operational adjustments are shifting demand toward rapid-response vaccine availability and more resilient immunization networks.

Government Health Agencies remain the dominant end-user because they manage national immunization strategies, strategic stockpiles, and public procurement programs. Centralized purchasing represents approximately 46% of institutional vaccine procurement, while integrated distribution planning has improved nationwide allocation efficiency by nearly 19%. Hospitals continue serving as major administration centers for specialized immunization programs, and Military Healthcare sustains consistent procurement through defense health readiness initiatives requiring uninterrupted vaccine availability.

Research Institutes are emerging as the fastest-growing end-user group as adenoviral technologies expand into therapeutic research and next-generation vaccine development. Vaccination Centers continue increasing operational importance through higher-volume immunization campaigns and digital scheduling systems. Companies are responding with customized supply agreements, collaborative research partnerships, differentiated pricing models, and expanded technical support services to strengthen long-term institutional relationships. Competitive positioning increasingly depends on serving both large public procurement programs and innovation-focused research organizations with flexible product portfolios.

North America accounted for the largest market share at 39.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 9.4% CAGR between 2026 and 2033.

Strategic Manufacturing Leadership and Advanced Vaccine Infrastructure

North America maintains the largest share of the Adenovirus Vaccine Market through extensive biopharmaceutical manufacturing capacity, mature regulatory systems, and sustained government-supported immunization preparedness. More than 40% of commercial adenoviral vector production capacity is concentrated within the region, supported by integrated contract manufacturing organizations and advanced biologics facilities. Automation has improved manufacturing throughput by approximately 22%, while digital quality management systems continue reducing batch-release timelines. Enterprise collaboration between biotechnology firms, research institutions, and manufacturers is strengthening clinical translation and production scalability. Companies continue expanding flexible manufacturing assets, improving inventory resilience, and strengthening domestic supply chains to support both public health preparedness and therapeutic pipeline development.

United States Market Outlook: The United States leads regional demand through its extensive vaccine research ecosystem, established viral vector manufacturing network, and defense-supported immunization infrastructure. Approximately 45% of North American adenoviral vector development programs are coordinated by U.S.-based organizations, supported by advanced biologics manufacturing clusters. Companies continue investing in automated production technologies, domestic fill-finish expansion, and strategic partnerships with contract manufacturers to improve operational flexibility and accelerate commercialization.

Regulatory Harmonization Accelerates Platform Innovation

Europe continues strengthening its market position through coordinated biotechnology policies, advanced vaccine manufacturing infrastructure, and cross-border research collaboration. The region contributes approximately 28% of global adenovirus vaccine production capacity, supported by established pharmaceutical manufacturing hubs and standardized regulatory pathways. Modernized biologics facilities have improved production efficiency by nearly 18%, while collaborative development programs continue accelerating technology transfer. Manufacturers are investing in digital manufacturing systems, sustainable production practices, and regional manufacturing resilience to improve operational continuity while supporting expanding therapeutic applications across infectious disease and advanced biologics development.

United Kingdom Market Outlook: The United Kingdom remains the region's strategic innovation center through globally recognized viral vector expertise, academic collaboration, and commercial manufacturing capability. More than 30% of regional adenoviral platform research programs involve UK-based institutions and biotechnology enterprises. Continued investment in advanced therapy manufacturing centers and integrated translational research supports faster product development while strengthening international technology partnerships and industrial competitiveness.

High-Volume Manufacturing Drives Expansion

Asia-Pacific is rapidly strengthening its position through expanding vaccine manufacturing infrastructure, government-backed biotechnology investment, and competitive production economics. The region accounts for approximately 31% of global manufacturing capacity, with production facilities expanding by nearly 20% during recent modernization initiatives. Large-scale biologics manufacturing, improving regulatory capabilities, and expanding domestic immunization programs continue supporting deployment growth. Manufacturers are investing in modular production facilities, automated quality systems, and localized supply networks that improve manufacturing flexibility while strengthening export readiness for international vaccine markets.

China Market Outlook: China leads regional expansion through extensive biologics manufacturing investment, integrated pharmaceutical supply chains, and national biotechnology modernization strategies. Domestic manufacturers have increased viral vector production capability by approximately 18% through facility expansion and technology upgrades. Companies continue strengthening international regulatory compliance, expanding commercial partnerships, and improving production standardization to support both domestic vaccination requirements and overseas market participation.

Public Health Modernization Supports Deployment

South America is expanding adenovirus vaccine deployment through stronger public immunization programs, upgraded cold-chain infrastructure, and increasing domestic pharmaceutical participation. The region represents approximately 7% of global market activity, while public-sector vaccine procurement has increased by nearly 15% across several national immunization initiatives. Manufacturers are collaborating with government agencies to strengthen distribution efficiency and improve regional supply reliability. Although infrastructure disparities remain across several countries, investment in logistics modernization and localized manufacturing partnerships continues improving long-term operational resilience and deployment consistency.

Brazil Market Outlook: Brazil serves as the region's principal vaccine manufacturing and public health center through established biomedical institutions and national immunization infrastructure. More than half of South America's large-scale vaccine manufacturing capability is concentrated within Brazil. Continued expansion of domestic production facilities, public procurement programs, and technology-transfer collaborations is strengthening manufacturing independence while improving national vaccine availability and regional distribution capacity.

Healthcare Infrastructure Investment Expands Capacity

The Middle East & Africa market is progressing through strategic healthcare modernization, increasing vaccine manufacturing investment, and expanding immunization infrastructure. The region contributes approximately 5% of global deployment, while biologics manufacturing investment has increased by nearly 17% across selected healthcare development initiatives. Governments are strengthening vaccine procurement frameworks, expanding cold-chain logistics, and encouraging international manufacturing partnerships to improve long-term supply security. Companies are responding by establishing regional distribution agreements, supporting technology transfer, and strengthening localized production capabilities to improve operational sustainability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading investment destination through healthcare transformation initiatives, biotechnology expansion, and pharmaceutical localization policies. National programs continue supporting advanced vaccine manufacturing infrastructure, with biologics capacity increasing by approximately 16% through new industrial projects. Companies are expanding regional partnerships, investing in technology transfer, and strengthening domestic production ecosystems to reduce import dependence while improving healthcare resilience.

The Adenovirus Vaccine Market is shaped by competition between global vaccine innovators including AstraZeneca, CanSino Biologics, Bharat Biotech, Emergent BioSolutions, and Serum Institute of India, against regional manufacturers expanding localized production and contract development organizations strengthening manufacturing capabilities. The top five participants collectively control approximately 58% of commercial market activity. Competition centers on platform technology, manufacturing speed, supply-chain resilience, and regulatory execution rather than price alone. Advanced automated bioprocessing improves production efficiency by nearly 22%, while digital quality systems reduce batch-release timelines by around 18%, creating measurable operational advantages. Leading companies are expanding through strategic manufacturing partnerships, regional production facilities, technology licensing, and vertical integration of fill-finish operations to secure dependable supply. Competitive pressure is shifting toward platform-based vaccine development capable of supporting multiple products from shared infrastructure, increasing capital efficiency. High regulatory validation requirements and specialized manufacturing expertise remain significant entry barriers. Success depends on scalable production, platform innovation, resilient supply networks, and rapid commercialization supported by strong regulatory execution.

AstraZeneca

CanSino Biologics

Bharat Biotech

Emergent BioSolutions

Serum Institute of India

Johnson & Johnson

Bavarian Nordic

Moderna

BioNTech

GSK

Sanofi

Merck & Co.

Vaxart

ReiThera

Current technology development is centered on advanced adenoviral vector engineering, automated bioprocessing, and digital manufacturing platforms that improve production consistency and accelerate commercialization. Suspension-cell manufacturing has replaced conventional adherent-cell production in many facilities, increasing production efficiency by approximately 28% while reducing manual processing requirements by nearly 20%. Around 60% of newly commissioned vaccine manufacturing facilities now integrate automated monitoring systems, enabling faster batch verification and reducing operational variability. Companies with established biologics infrastructure benefit through higher manufacturing utilization and improved regulatory readiness.

Emerging technologies include artificial intelligence-assisted vector optimization, continuous manufacturing, and advanced analytical quality control. AI-supported development shortens early-stage candidate optimization by nearly 24%, while real-time process analytics reduce production deviations by approximately 17%. Compared with legacy offline quality testing, integrated digital quality platforms enable faster release decisions and lower operational costs. Manufacturers adopting modular facilities and digital twins gain stronger manufacturing flexibility and more efficient technology transfer across multiple production sites.

Between 2026 and 2028, platform-based manufacturing, thermostable formulations, and standardized viral vector systems will become primary competitive differentiators. Deployment of integrated digital manufacturing is expected to exceed 70% among major commercial producers, strengthening production resilience and reducing supply interruptions. Companies investing early in scalable platform technologies, automation, and predictive quality management will secure stronger operational advantages, faster product deployment, improved manufacturing economics, and greater competitiveness across both vaccine and therapeutic adenoviral applications.

May 2024 AstraZeneca began the global withdrawal of its adenovirus-based COVID-19 vaccine (Vaxzevria) after declining commercial demand and the availability of updated vaccines across international markets. The vaccine had previously been supplied to more than 170 countries, marking a major portfolio transition.

November 2024 CanSino Biologics published peer-reviewed clinical evidence confirming that its Ad5-nCoV adenovirus vector vaccine showed no increased likelihood of HIV infection among vaccinated participants, reinforcing long-term confidence in adenoviral vector technology. The study evaluated data from over 14,000 participants.

April 2025 McMaster University advanced its inhaled adenovirus-vector respiratory vaccine program into expanded human clinical evaluation, supported by Canadian research partnerships. Preclinical findings demonstrated stronger mucosal immune responses than conventional intramuscular delivery, supporting next-generation respiratory vaccine development. Source: (https://healthsci.mcmaster.ca)

2026 The World Health Organization continued strengthening global pathogen preparedness through expanded support for platform-based vaccine manufacturing, encouraging standardized adenoviral vector production capabilities and technology transfer initiatives to improve rapid outbreak response across participating countries. Source: (https://www.who.int)

This report provides a comprehensive assessment of the Adenovirus Vaccine Market by analyzing technology evolution, manufacturing capabilities, competitive positioning, and deployment strategies across the value chain. It covers major product types including Live Oral Vaccines, Viral Vector Vaccines, Monovalent Vaccines, Multivalent Vaccines, and Recombinant Vaccines, together with applications spanning respiratory infections, clinical research, military immunization, routine vaccination, and outbreak control. The analysis evaluates demand patterns across hospitals, vaccination centers, research institutes, military healthcare, and government health agencies across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report examines operational trends across more than five major end-user groups and multiple strategic market segments, highlighting manufacturing modernization, digital quality systems, advanced viral vector technologies, and regional supply-chain localization. It delivers actionable insights supporting investment prioritization, expansion planning, partnership evaluation, competitive benchmarking, and technology adoption while identifying emerging therapeutic applications and strategic opportunities expected to shape market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 940.82 Million |

Market Revenue in 2033 | USD 1728.54 Million |

CAGR (2026 - 2033) | 7.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | AstraZeneca, CanSino Biologics, Bharat Biotech, Emergent BioSolutions, Serum Institute of India, Johnson & Johnson, Bavarian Nordic, Moderna, BioNTech, GSK, Sanofi, Merck & Co., Vaxart, ReiThera |

Customization & Pricing | Available on Request (10% Customization is Free) |