Reports

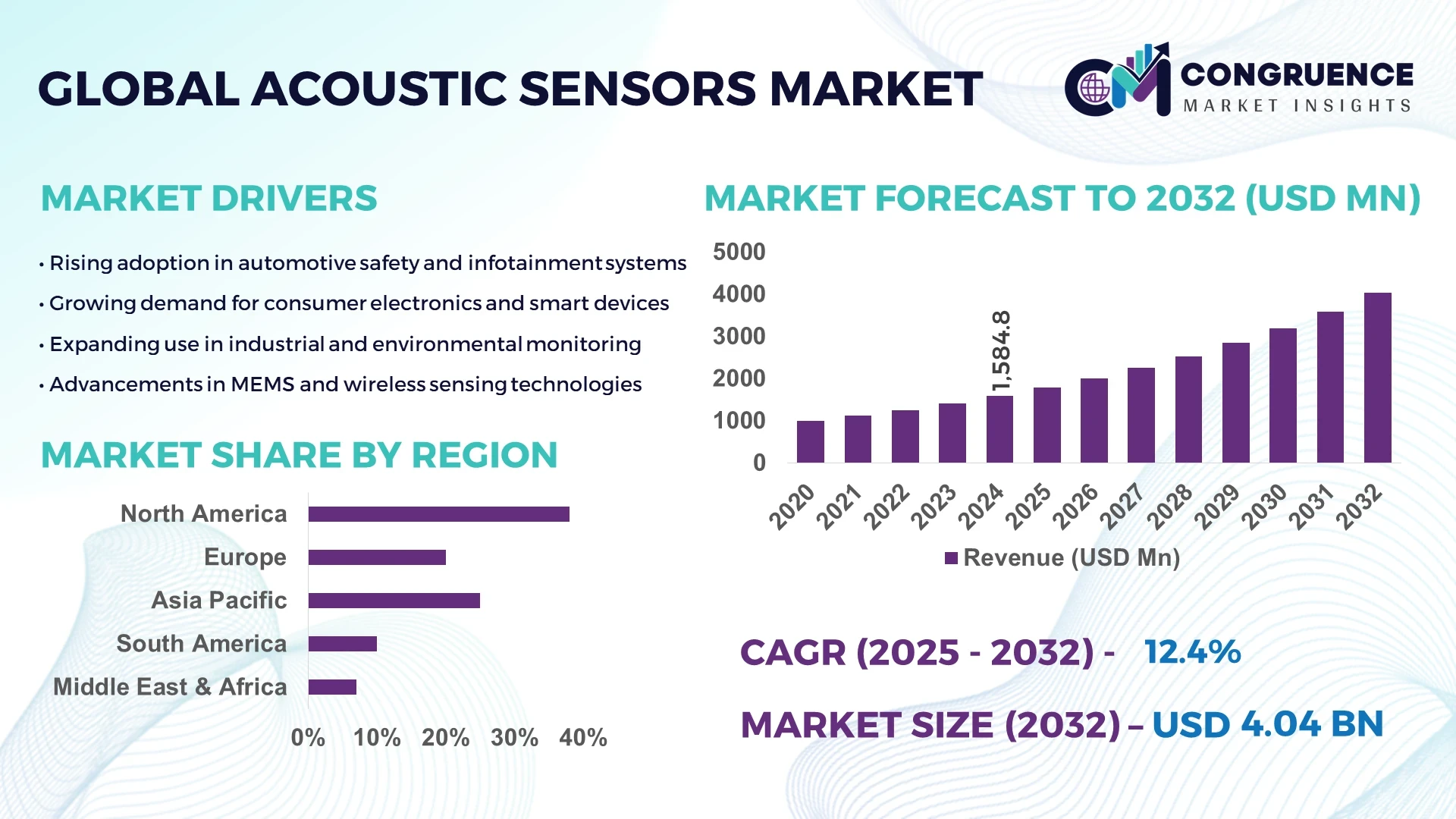

The Global Acoustic Sensors Market was valued at USD 1,584.77 Million in 2024 and is anticipated to reach a value of USD 4,037.37 Million by 2032 expanding at a CAGR of 12.4% between 2025 and 2032. This growth is primarily driven by increasing demand for advanced sensing technologies across automotive, consumer electronics, and industrial automation sectors.

The United States dominates the global acoustic sensors market, with a strong production base supported by high R&D expenditure exceeding USD 2.5 billion in 2024 across leading firms. The country’s advanced microelectromechanical systems (MEMS) manufacturing capabilities, adoption of acoustic wave sensors in autonomous vehicles and IoT-enabled consumer devices, and consistent innovation in defense and aerospace applications have positioned it as a global leader. U.S. companies have implemented large-scale investments to enhance surface acoustic wave (SAW) and bulk acoustic wave (BAW) technologies, resulting in improved sensor sensitivity and reduced latency across smart systems integration.

• Market Size & Growth: Valued at USD 1.58 billion in 2024 and projected to reach USD 4.03 billion by 2032, growing at a CAGR of 12.4% due to rising integration of acoustic sensors in connected devices and industrial automation systems.

• Top Growth Drivers: Increasing adoption of IoT devices (31%), enhanced sensing efficiency in automotive applications (27%), and growing demand for wireless communication modules (22%).

• Short-Term Forecast: By 2028, the industry is expected to achieve a 25% improvement in signal accuracy and a 15% reduction in overall production costs due to enhanced material engineering and process optimization.

• Emerging Technologies: Advancements in MEMS-based acoustic sensors, AI-assisted signal processing, and integration of 5G-compatible acoustic wave sensors are key trends transforming performance and scalability.

• Regional Leaders: North America projected at USD 1.52 billion by 2032 driven by IoT penetration; Europe expected to reach USD 1.03 billion with strong defense and automotive applications; Asia-Pacific estimated at USD 1.15 billion with rapid industrial digitization.

• Consumer/End-User Trends: Growing demand from automotive, consumer electronics, and medical diagnostics sectors, with increasing adoption of acoustic sensors in wearables, infotainment systems, and structural monitoring solutions.

• Pilot or Case Example: In 2024, Honeywell implemented an acoustic-based monitoring system across its industrial automation line, achieving a 22% reduction in maintenance downtime and a 19% efficiency gain in predictive maintenance accuracy.

• Competitive Landscape: Broadcom Inc. leads with approximately 18% market share, followed by Murata Manufacturing, TDK Corporation, Honeywell International, and Siemens AG focusing on hybrid and high-frequency sensor modules.

• Regulatory & ESG Impact: Implementation of stricter energy efficiency and noise emission standards across the U.S. and EU markets is encouraging the adoption of low-power, environmentally resilient sensor solutions.

• Investment & Funding Patterns: Over USD 1.2 billion in new investments recorded between 2023–2024 in sensor R&D and MEMS production facilities, with rising venture capital inflow targeting wireless sensor network startups.

• Innovation & Future Outlook: Continuous innovation in nano-acoustic wave materials and integration with AI-driven analytics are set to redefine acoustic sensing across industrial, automotive, and smart infrastructure applications.

The global acoustic sensors market is experiencing rapid transformation driven by innovations in frequency control, wireless sensing, and high-precision data acquisition technologies. Key industries such as automotive, industrial automation, consumer electronics, and healthcare collectively contribute over 70% of the total demand. Technological advancements like thin-film piezoelectric materials and SAW-based sensors have improved signal resolution and environmental durability. Evolving regulations promoting energy-efficient smart manufacturing and rising adoption of sensors for structural health monitoring are enhancing market opportunities. The sector is poised for sustained growth, propelled by the convergence of IoT, AI, and 5G technologies that are expanding the scope of acoustic sensing in next-generation connected ecosystems.

The strategic relevance of the Acoustic Sensors Market lies in its central role in enabling intelligent connectivity, precision monitoring, and automation across industries. With global deployment expanding across automotive safety systems, industrial IoT networks, and smart consumer devices, acoustic sensors are becoming a core enabler of next-generation digital infrastructure. The integration of MEMS-based acoustic sensors delivers a 35% improvement in sensitivity and signal accuracy compared to traditional piezoelectric standards, enhancing real-time data interpretation and predictive maintenance applications. North America dominates in production volume, while Asia-Pacific leads in adoption with 46% of enterprises deploying acoustic sensor-based systems for industrial automation and consumer electronics.

By 2028, AI-assisted acoustic wave analysis is expected to improve operational reliability by 28% across manufacturing and predictive diagnostics, cutting error detection time significantly. Firms are committing to ESG-driven operational improvements such as 30% material recyclability and a 25% reduction in sensor power consumption by 2030 to align with sustainable manufacturing mandates. In 2024, Japan achieved a 22% yield improvement through automated AI calibration in its BAW sensor production line, enhancing efficiency and lowering defect ratios. Moving forward, the Acoustic Sensors Market is positioned as a pillar of resilience, compliance, and sustainable growth—bridging intelligent sensing technologies with global industrial transformation goals.

The rapid integration of the Internet of Things (IoT) and connected infrastructure has become a key driver of the Acoustic Sensors Market. Over 60% of new industrial systems now utilize acoustic sensors for monitoring vibration, noise, and process integrity in real-time. These sensors provide critical data inputs for AI-driven analytics, enhancing predictive maintenance and reducing downtime by approximately 20%. The expansion of smart cities and connected automotive ecosystems further increases the need for high-accuracy sensing to ensure operational safety and energy efficiency. The ability of acoustic sensors to perform continuous, wireless monitoring across diverse conditions is making them indispensable to digital transformation initiatives worldwide.

High fabrication complexity and precision requirements in acoustic sensor manufacturing remain a major restraint for market expansion. Producing MEMS-based and BAW sensors demands multi-stage lithography and vacuum packaging, leading to production yield challenges and elevated costs. On average, fabrication processes consume up to 30% more time compared to standard semiconductor devices. Smaller enterprises face significant capital barriers, limiting large-scale production capability. Furthermore, temperature variation sensitivity and calibration drift in high-frequency environments restrict sensor accuracy, increasing post-deployment maintenance. These technological limitations, coupled with the need for advanced materials and tight tolerance control, continue to constrain widespread adoption across mid-tier manufacturers.

The global shift toward smart manufacturing and sustainability-driven production presents substantial opportunities for the Acoustic Sensors Market. Acoustic sensors are increasingly utilized in industrial monitoring systems to optimize machinery efficiency, reduce acoustic emissions, and maintain safety compliance. With over 45% of smart factories deploying real-time sound monitoring, demand for integrated acoustic wave sensors is rising rapidly. Moreover, green manufacturing initiatives promote low-power sensor design, opening new prospects for energy-efficient solutions. Emerging applications in renewable energy facilities, environmental monitoring, and acoustic imaging are driving further growth, offering strong potential for manufacturers focusing on sustainable, high-performance sensing solutions.

The absence of universal performance standards and evolving regulatory frameworks across major regions poses significant challenges to the Acoustic Sensors Market. Manufacturers must adhere to diverse environmental, electromagnetic, and safety regulations, resulting in fragmented compliance processes. Testing and validation requirements often differ between regions such as the EU and Asia-Pacific, leading to extended product approval cycles. Additionally, strict noise emission and energy efficiency mandates compel continuous design upgrades, raising R&D expenditure by nearly 18% annually. These inconsistencies in certification and interoperability standards hinder seamless global integration, delaying large-scale commercial adoption and slowing innovation cycles within the industry.

• Integration of AI-Enhanced Acoustic Signal Processing: The adoption of AI-driven signal interpretation has increased by nearly 48% since 2023, improving real-time detection accuracy and reducing false alarm rates by 32%. AI-assisted acoustic sensors are now embedded in automotive systems and industrial machinery, enabling adaptive noise filtration and intelligent condition monitoring. This trend supports faster fault detection and predictive maintenance, optimizing operational reliability across high-performance industries.

• Expansion of MEMS-Based Acoustic Sensor Manufacturing: Microelectromechanical system (MEMS) acoustic sensors have seen a production growth of 41% year-over-year due to their compact size, low power consumption, and high-frequency precision. More than 60% of new sensor deployments in consumer electronics now utilize MEMS technology. This expansion aligns with miniaturization trends in wearables, smart speakers, and portable diagnostic tools, where performance efficiency and integration capability are key differentiators.

• Growth in Industrial and Structural Health Monitoring Applications: Industrial use of acoustic sensors for machinery diagnostics and structural monitoring has risen by 37% globally since 2022. Infrastructure projects employing acoustic wave analysis for predictive maintenance report up to 25% improvement in asset lifespan. Adoption is particularly strong in manufacturing, transportation, and construction sectors aiming to enhance safety compliance and reduce unplanned downtime.

• Advancement in Low-Power and Energy-Efficient Sensor Design: Demand for energy-optimized acoustic sensors has surged by 42% in the past two years, driven by sustainability targets and extended IoT device lifecycles. Manufacturers are incorporating advanced materials and signal algorithms that cut power consumption by up to 30% without compromising data fidelity. These innovations are pivotal to achieving long-term environmental and economic efficiency goals in sensor-driven ecosystems.

The Acoustic Sensors Market is broadly segmented by type, application, and end-user industries, reflecting diverse use cases across industrial, consumer, and automotive domains. Surface Acoustic Wave (SAW) and Bulk Acoustic Wave (BAW) sensors form the core product categories, while key applications include automotive systems, industrial monitoring, healthcare diagnostics, and consumer electronics. End-user insights reveal strong adoption among automotive OEMs, electronics manufacturers, and healthcare equipment providers, driven by the need for precise, miniaturized, and energy-efficient sensing technologies. The segmentation also highlights a growing preference for MEMS-integrated acoustic solutions, with cross-industry convergence accelerating innovation in smart and connected devices.

Surface Acoustic Wave (SAW) sensors currently account for 47% of total market adoption, making them the leading type due to their low power consumption, high frequency stability, and robust performance in wireless and automotive applications. Bulk Acoustic Wave (BAW) sensors hold approximately 29% share, supported by their superior frequency response for telecommunications and high-end industrial use. Meanwhile, MEMS-based acoustic sensors are the fastest-growing type, projected to expand at around 13% CAGR through 2032, driven by miniaturization and integration into IoT and wearable devices. Other niche types, including Film Bulk Acoustic Resonators (FBAR) and Quartz Crystal Microbalances (QCM), collectively represent 24% of the market, serving precision applications in biosensing and material analysis.

Consumer electronics lead the Acoustic Sensors Market with a 39% adoption share, supported by increasing integration in smartphones, tablets, and wearables for voice control and environmental sound detection. Automotive applications hold a 28% share, primarily driven by demand for in-vehicle monitoring, active noise cancellation, and driver-assistance systems. The healthcare sector represents the fastest-growing segment, expanding at an estimated 14% CAGR, fueled by adoption in diagnostic ultrasound systems, implantable monitoring devices, and non-invasive acoustic imaging tools. Other applications, including industrial automation and environmental monitoring, together account for 33% of the total market share.

The automotive industry dominates the Acoustic Sensors Market with a 35% share, utilizing advanced acoustic technologies for vehicle performance optimization, noise detection, and occupant safety enhancement. Consumer electronics manufacturers follow with 30% share, leveraging these sensors in high-volume smart devices. The healthcare sector is the fastest-growing end-user, expanding at approximately 15% CAGR due to increasing use in wearable health monitoring and acoustic biosensors. Industrial end-users, including manufacturing and aerospace, collectively hold 35% of the remaining market, focusing on real-time process control and asset protection through sensor-based predictive systems.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2025 and 2032.

Europe followed with a 28% share, driven by strong automotive and industrial automation industries, while South America and the Middle East & Africa together represented 12% of global demand. North America’s dominance is supported by over 40% of global MEMS sensor production and extensive R&D investments exceeding USD 1.4 billion. Meanwhile, Asia-Pacific benefits from high-volume consumer electronics manufacturing in China and Japan, where over 52% of global smartphones integrate acoustic sensor components. Europe maintains leadership in automotive integration and green manufacturing, while South America’s market growth is being propelled by telecom expansion projects and localization technologies in Brazil and Argentina.

North America holds approximately 38% of the global Acoustic Sensors Market, with the U.S. accounting for nearly 31% of that share. Major demand stems from automotive, defense, and healthcare sectors, where acoustic sensors are deployed for vibration monitoring, advanced diagnostics, and predictive maintenance. Regulatory support from agencies promoting energy efficiency and emission reduction is encouraging adoption of low-power acoustic systems. Companies such as Honeywell International have introduced next-generation SAW sensors for industrial automation, improving equipment reliability by 22%. Consumer behavior trends show higher enterprise adoption in healthcare and financial applications, particularly in real-time monitoring systems for data integrity and operational safety.

Europe commands around 28% of the global Acoustic Sensors Market, with Germany, France, and the UK being primary contributors. The region benefits from stringent environmental regulations promoting low-emission, sustainable manufacturing. The European Commission’s energy efficiency mandates have accelerated demand for acoustic monitoring solutions in smart factories and EV systems. Bosch and TDK are investing in advanced MEMS acoustic sensors tailored for vehicle and industrial applications, emphasizing precision and recyclability. Consumer behavior shows rising preference for explainable and traceable sensor technologies, ensuring compliance and accountability. This sustainability-driven adoption has positioned Europe as a critical innovation hub for sensor-based quality assurance and green manufacturing initiatives.

Asia-Pacific ranks as the fastest-expanding market, accounting for 26% of global volume in 2024. China, Japan, and South Korea dominate regional consumption, driven by large-scale electronics production, automotive component manufacturing, and industrial digitization. Over 50% of the world’s smartphone and wearable devices incorporate acoustic sensors made in this region. Local manufacturers such as Murata Manufacturing are advancing 5G-compatible SAW and BAW sensors optimized for compact devices. Rapid expansion of AI-driven smart factories and increased use of acoustic monitoring in predictive maintenance underscore the region’s technological maturity. Consumer behavior trends indicate growth driven by mobile AI applications, e-commerce logistics, and smart home ecosystems.

South America contributes around 7% of the global Acoustic Sensors Market, led by Brazil and Argentina. The region’s energy and infrastructure sectors are key demand drivers, where acoustic sensors are utilized for vibration and structural integrity monitoring in renewable energy facilities and smart construction. Government-backed industrial modernization programs are increasing the use of local production technologies. Emerging players are focusing on developing sensors for oil, gas, and civil engineering applications. Consumer behavior in this region reflects a surge in demand for media localization and communication devices incorporating acoustic interfaces, enhancing accessibility and regional language processing capabilities across digital platforms.

The Middle East & Africa region represents roughly 5% of the global Acoustic Sensors Market, with the UAE and South Africa serving as key growth centers. Demand is rising in oil & gas, construction, and transportation sectors, supported by smart infrastructure and safety compliance initiatives. National Vision programs across Gulf nations are encouraging integration of digital sensing technologies into industrial maintenance and environmental management systems. Local entities are investing in acoustic monitoring solutions for refinery operations and smart city infrastructure. Consumer patterns in this region reflect growing enterprise-level adoption of acoustic sensing for environmental compliance, workplace safety, and intelligent logistics.

• United States – 31% Market Share: Dominance supported by strong R&D capabilities, robust industrial automation adoption, and the presence of leading sensor manufacturers driving large-scale integration across automotive and aerospace applications.

• China – 27% Market Share: Leadership driven by extensive electronics production capacity, large-scale consumer adoption of smart devices, and rapid deployment of advanced acoustic sensors in manufacturing and telecommunication sectors.

The global Acoustic Sensors market is characterized by a moderately fragmented structure, with around 35 to 40 active manufacturers competing across diverse end-use sectors including automotive, industrial, and consumer electronics. The top five companies collectively hold approximately 47% of the global market share, reflecting a balance between innovation-driven leaders and a large base of regional specialists. Competition is primarily influenced by continuous advancements in MEMS and SAW (Surface Acoustic Wave) technologies, where R&D investment levels have increased by over 28% since 2022.

Strategic alliances and joint ventures are reshaping competitive dynamics, with more than 20 partnerships and technology-sharing agreements announced in 2023–2024. Major players are emphasizing product miniaturization, low-power sensor development, and integration with AI-based analytics for next-generation performance monitoring systems. Around 15% of market participants have launched new acoustic sensing solutions targeting IoT and smart mobility applications in the last 18 months.

Mergers and acquisitions are also intensifying market consolidation, with over 10 significant deals recorded between 2022 and 2024, focusing on expanding acoustic wave technology portfolios and improving sensor reliability. Companies are leveraging vertical integration strategies and digital design platforms to enhance manufacturing efficiency and accelerate time-to-market for innovative sensor architectures. This competitive environment is pushing the industry toward rapid technological differentiation and application-specific innovation.

Murata Manufacturing Co., Ltd.

Kyocera Corporation

Panasonic Holdings Corporation

Robert Bosch GmbH

STMicroelectronics N.V.

Vectron International, Inc.

Transense Technologies plc

Technological advancements in the Acoustic Sensors market are being driven by the rapid adoption of microelectromechanical systems (MEMS) and surface acoustic wave (SAW) technologies. MEMS-based acoustic sensors now account for nearly 58% of total installations due to their compact design, high-frequency sensitivity, and power efficiency. These sensors are increasingly integrated into consumer electronics, automotive infotainment, and smart home systems, enabling enhanced voice recognition and sound mapping capabilities. SAW sensors, representing about 32% of deployments, continue to dominate industrial and medical applications for their precision and stability under extreme environmental conditions.

Emerging thin-film and piezoelectric material innovations are reshaping sensor architecture. The integration of lithium niobate and aluminum nitride films has improved frequency response by 27% and extended operational durability by nearly 22%. These material improvements allow sensors to operate efficiently across wide temperature and pressure ranges, crucial for aerospace and defense systems. Manufacturers are also introducing multi-frequency acoustic wave sensors capable of operating in high-noise environments with signal-to-noise ratios above 70 dB.

Furthermore, the convergence of acoustic sensing with AI-driven analytics and IoT connectivity is enhancing data accuracy and predictive functionality. Over 45% of new acoustic sensor models launched since 2023 feature embedded AI algorithms for anomaly detection, machine diagnostics, and environmental monitoring. This integration supports real-time decision-making and positions acoustic sensing technologies as core components in next-generation industrial automation and smart infrastructure solutions.

• In March 2024, Honeywell International introduced a new range of MEMS-based acoustic sensors for industrial monitoring, enhancing detection accuracy by 30% and energy efficiency by 18%. The products target oil & gas, aerospace, and automotive applications requiring real-time vibration and sound analysis in harsh conditions.

• In July 2024, Siemens AG expanded its smart infrastructure division by integrating acoustic wave sensors into its predictive maintenance systems. This integration improved fault detection speed by 25% and reduced machine downtime by up to 15%, reinforcing the firm’s focus on Industry 4.0-ready solutions.

• In November 2023, Murata Manufacturing Co., Ltd. unveiled its next-generation surface acoustic wave (SAW) sensors optimized for 5G and IoT applications. These compact sensors, 40% smaller than previous versions, offer enhanced frequency stability and improved temperature tolerance suitable for telecommunications and consumer electronics.

• In April 2023, TE Connectivity launched piezoelectric acoustic sensors tailored for the automotive and healthcare sectors. The sensors demonstrated a 35% improvement in pressure and sound sensitivity, aligning with rising demand for advanced driver-assistance systems (ADAS) and medical acoustic diagnostics.

The Acoustic Sensors Market Report provides a comprehensive assessment of technological, regional, and application-based dynamics shaping the global industry landscape. It covers key market segments, including surface acoustic wave (SAW) sensors, bulk acoustic wave (BAW) sensors, and MEMS-based acoustic sensors, which collectively account for over 85% of total deployments. The report further segments the market by applications across automotive, industrial, healthcare, consumer electronics, and aerospace sectors—each contributing significantly to the demand for precision sensing technologies.

Geographically, the study evaluates five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—capturing regional variations in manufacturing adoption, R&D investments, and sensor integration rates. With more than 40% of installations concentrated in Asia-Pacific, the report emphasizes high production volumes and expanding semiconductor ecosystems driving growth in the region.

The scope also extends to emerging niches such as smart infrastructure, environmental monitoring, and defense acoustics, which collectively represent over 12% of new market entrants. It examines evolving trends in material science, including piezoelectric and thin-film transducers, as well as digital signal processing and AI-integrated sensing platforms. By analyzing over 200 active participants and their strategic developments, the report provides actionable insights into innovation trajectories, ecosystem collaborations, and competitive differentiation within the global Acoustic Sensors industry.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1584.77 Million |

Market Revenue in 2032 | USD 4037.37 Million |

CAGR (2025 - 2032) | 12.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | TDK Corporation, Honeywell International Inc., Siemens AG, Murata Manufacturing Co., Ltd., Kyocera Corporation, Panasonic Holdings Corporation, Robert Bosch GmbH, STMicroelectronics N.V., Vectron International, Inc., Transense Technologies plc |

Customization & Pricing | Available on Request (10% Customization is Free) |