Reports

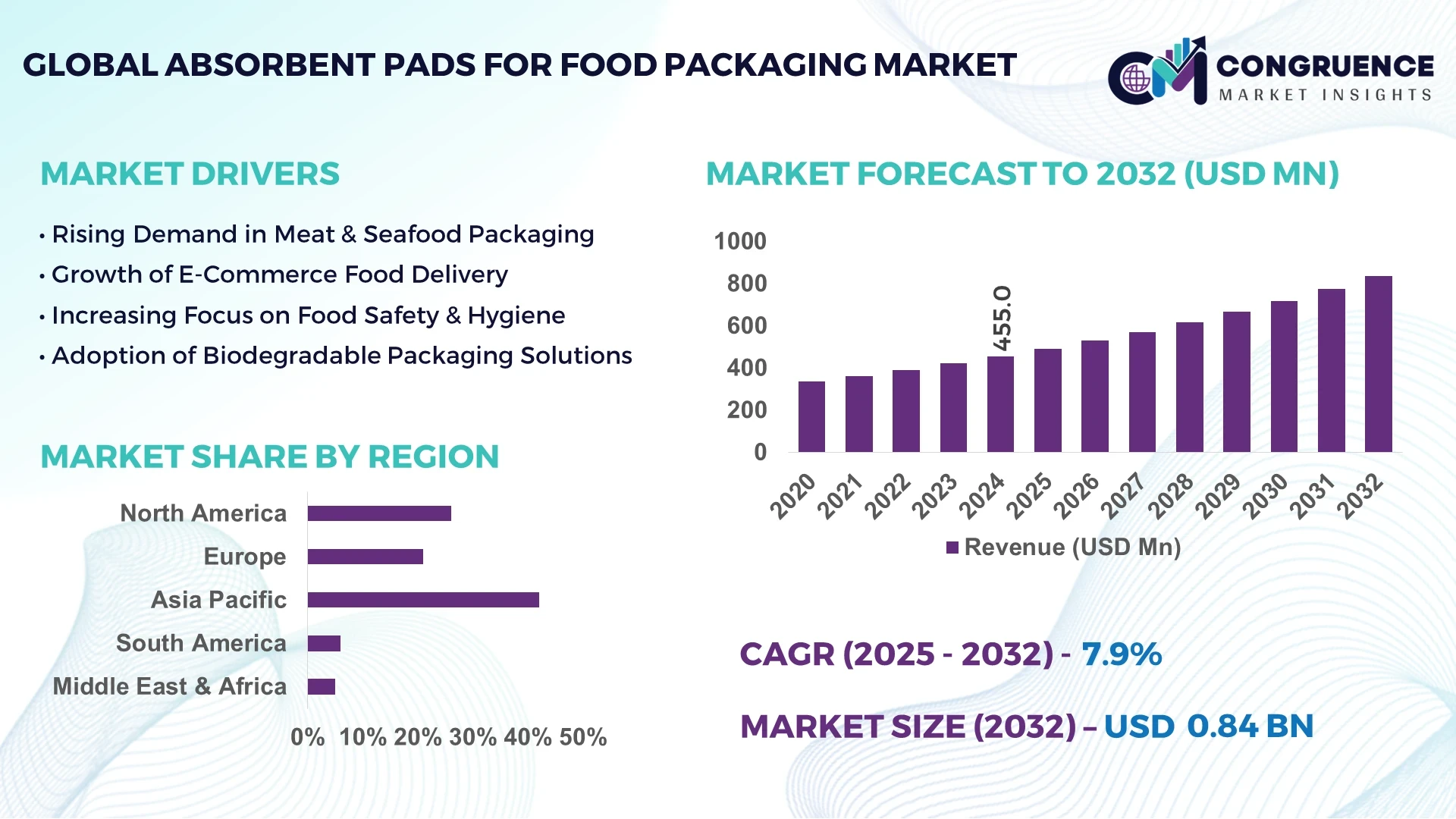

The Global Absorbent Pads for Food Packaging Market was valued at USD 455 Million in 2024 and is anticipated to reach a value of USD 836.0 Million by 2032 expanding at a CAGR of 7.9% between 2025 and 2032.

China holds a commanding position in this arena, boasting expansive production capacity with multiple high-throughput extrusion and molding facilities dedicated to absorbent pads for food packaging. The nation has made significant capital investments in automated converting lines and state-of-the-art slitting and embossing technologies, largely to serve its robust meat and seafood packing industries. Advanced applications there include multilayer laminated pads with odor-absorbing and antimicrobial functionality, driven by local R&D centers focused on biodegradable core technologies and sensor-integrated freshness indicators.

In terms of broader market scope, the Absorbent Pads for Food Packaging Market serves key industry segments such as meat and poultry, seafood, fresh produce, and ready‐to‐eat meals—meat and poultry absorbent pads account for the largest share, followed by fresh produce. Recent product innovations include pads incorporating sodium polyacrylate–based superabsorbent polymers and activated carbon layers to improve moisture and odor control. Regulatory and environmental factors increasingly drive demand for non-chlorine-bleached and compostable pad variants, especially in Europe, where single-use plastic reduction mandates are in effect. Economic pressures, including rising freight costs, are prompting regional players in Southeast Asia to promote localized supply chains. Consumption patterns show strong growth in emerging markets across Latin America and South Asia due to rising disposable incomes and expanding supermarket chains. Emerging trends include sensor-embedded “smart” absorbent pads that change color based on pH shifts, and future outlook anticipates integration of biodegradable polymers derived from agricultural waste, enabling both performance improvements and sustainability in the Absorbent Pads for Food Packaging Market.

The Absorbent Pads for Food Packaging Market is experiencing transformative advances through the application of artificial intelligence across production, quality assurance, and supply chain optimization. AI-powered vision systems deployed on production lines now identify defects such as mis-aligned adhesive layers or inconsistent embossing patterns in real time, enabling instantaneous rejects and reducing waste by more than 30%. Machine learning algorithms analyze sensor data—such as moisture pickup, temperature, and pad compression—to fine-tune glue application and pad thickness on the fly, enhancing operational performance and consistency in real-world packaging environments.

In logistics, AI-driven forecasting tools predict daily demand for absorbent pads across distribution centers with precision within 5%, allowing manufacturers to adjust manufacturing schedules, reduce idle capacity, and minimize stockouts. Process optimization through AI has also enabled energy consumption reductions in drying ovens by roughly 12%, by adjusting parameters in response to sensor-monitored ambient humidity and production throughput. Furthermore, AI chatbots embedded in supplier portals streamline procurement of raw materials like SAP granules and adhesive films by automatically comparing multiple vendor quotes and delivery timelines, ensuring timely, cost-effective sourcing—crucial for maintaining uninterrupted production in the Absorbent Pads for Food Packaging Market.

Through these enhancements—automated quality control, energy-efficient processing, demand-aware production planning, and smarter procurement—AI is materially strengthening efficiency, resilience, and competitiveness in the Absorbent Pads for Food Packaging Market. Decision-makers and industry professionals see these concrete improvements as fundamental to achieving operational excellence and sustaining innovation in this evolving sector.

“In 2025, a multinational food-packaging manufacturer integrated an AI-based inline optical system that reduced pad rejection rates by 28% and lowered material usage by 15%, while throughput increased by 18 %.”

The Absorbent Pads for Food Packaging Market is shaped by several overarching dynamics influencing production protocols, customer requirements, and industry viability. One key trend is escalating demand for multifunctional pads that combine moisture absorption, antimicrobial features, and biodegradability, reflecting evolving standards in food safety and environmental regulation. Meanwhile, supply-chain digitization is becoming paramount; real-time tracking and ERP integration allow pad manufacturers to align output with shifting retailer inventory needs. On the vendor side, raw material costs—especially of superabsorbent polymers and non-woven substrates—are closely monitored to preserve margins amid input volatility. At the same time, packaging industry consolidation is pressuring smaller pad producers to differentiate through innovation or vertical integration. Finally, pressure to reduce single-use plastic and adopt compostable alternatives is fostering collaboration with composting facilities and encouraging certifications such as OK Compost or ASTM 6400, further influencing product design and market entry strategies within the Absorbent Pads for Food Packaging Market.

The Absorbent Pads for Food Packaging Market is gaining momentum from the rising deployment of multifunctional pad technologies, such as those with integrated moisture control, odor absorption, and antimicrobial layers. These advanced pads enable food processors and packers to extend shelf life and reduce spoilage in perishable products. For instance, adoption of pads containing activated carbon and silver-ion polymers has increased in meat and seafood segments to mitigate bacterial growth and odor transmission. Additionally, regulatory pressures to minimize food waste are prompting major retail chains to specify such high-performance pad types in purchase contracts, reinforcing demand. As a result, manufacturers are investing in R&D and line upgrades to produce multilayer composite pads with precise control over absorbent core distribution and antimicrobial agent release profiles, enhancing product performance in the Absorbent Pads for Food Packaging Market.

One significant challenge facing the Absorbent Pads for Food Packaging Market is extreme volatility in raw material inputs—particularly prices and availability of superabsorbent polymers (SAPs) and spunbond non-woven substrates. Global fluctuations in crude oil and petrochemical feedstocks directly affect the cost base for pad manufacturers, tightening profitability. Moreover, shortages in non-woven fabrics, caused by capacity constraints or resin supply bottlenecks, have led to production delays and backlog orders in certain regional markets. To maintain delivery schedules, some manufacturers are forced to source costlier substitutes or accept thinner pad structures, potentially compromising quality. This instability complicates forecasting and long-term planning, impacting operational continuity and requiring manufacturers to establish diversified supplier networks and hedging strategies.

An emerging opportunity in the Absorbent Pads for Food Packaging Market lies in the adoption of biodegradable and compostable pad materials derived from starch, polylactic acid (PLA), or agricultural residues. Driven by tightening environmental legislation and sustainability mandates, pad producers are piloting fully compostable variants that maintain absorption efficacy while breaking down within industrial composting timelines. In some pilot deployments, compostable pads have demonstrated moisture retention within 10% of traditional SAP-based counterparts during shelf tests. With consumer and retailer appetite for green packaging growing, these alternatives offer manufacturers differentiation and access to new segments. Strategic partnerships with waste-management and composting firms can further enable closed-loop systems, enhancing brand positioning and future-proofing the Absorbent Pads for Food Packaging Market.

A notable challenge for the Absorbent Pads for Food Packaging Market is scaling sustainable production without compromising absorption and structural performance. Biodegradable substrates and alternative absorbents—though environmentally attractive—often exhibit lower absorption per unit weight or faster breakdown under moist conditions. Manufacturers must therefore reformulate pad designs, adding more layers or denser materials, which can increase thickness and cost. Transitioning production lines to handle new materials (such as PLA films or compostable non-wovens) may require capital-intensive retrofits, new adhesives, and equipment recalibration. Additionally, maintaining shelf-stability and moisture absorption consistency in variable temperature and humidity environments becomes more complex. Balancing these technical and operational hurdles is critical to delivering sustainable, high-performance solutions in the competitive Absorbent Pads for Food Packaging Market.

Surge in Sensor-Embedded “Smart” Pads: The market is witnessing a clear uptick in sensor-embedded absorbent pads featuring pH- or freshness-indicating dyes. Manufacturers now regularly incorporate reactive color-change indicators that activate within minutes of spoilage onset. These “smart” pads are now used in over 10 % of premium meat and seafood products in Europe, gaining traction in refrigerated distribution to reduce waste and improve traceability.

Adoption of Heat-Sealable Eco-Films: There is a growing switch toward heat-sealable absorbent pad films that integrate biodegradable polymers. These films not only streamline automated tray-sealing operations but also dissolve entirely in industrial composting setups within 12 weeks, aligning with regulatory thresholds for compostability. Early adopters report up to a 25 % reduction in packaging line downtime.

Rise of Regional Micro-Manufacturing Hubs: In regions such as Southeast Asia and Latin America, the establishment of small-scale, automated pad converters is creating localized supply hubs. These hubs are reducing lead times by up to 40 % and cutting freight-related carbon emissions by nearly one-third, while enabling rapid response to local retailer specifications.

Growth in Custom-Sized Pads for E-Commerce Packaging: E-commerce’s expansion in fresh food deliveries is driving demand for custom-sized absorbent pads. Manufacturers are now offering pads tailored to specific carton formats, with precise absorption capacities. This has led to a 15 % reduction in material waste and improved pad fitment in automated carton-packing systems.

The Absorbent Pads for Food Packaging Market is segmented by type, application, and end-user, each of which reflects specific functional needs, industry standards, and evolving consumer preferences. By type, the market encompasses standard absorbent pads, multilayer pads, antimicrobial variants, and biodegradable solutions, each tailored to food safety and preservation requirements. Applications span meat and poultry, seafood, fruits and vegetables, bakery, and ready-to-eat meals, with varying absorption capacity and design features depending on perishability and moisture content. End-users include food processors, supermarkets, retail packaging firms, and food delivery services, all adopting absorbent pad technologies to ensure extended shelf life, compliance with safety regulations, and reduced food waste. This segmentation highlights the industry’s growing emphasis on multifunctionality, sustainability, and tailored solutions to meet the needs of both traditional retail and emerging e-commerce channels.

The Absorbent Pads for Food Packaging Market includes standard single-layer pads, multilayer composite pads, antimicrobial-enhanced pads, and biodegradable/compostable variants. Among these, multilayer absorbent pads hold the leading position, as they combine superior liquid retention with advanced structural stability, making them the preferred choice for packaging high-drip products such as meat and seafood. Their use of superabsorbent polymers and enhanced distribution channels contributes to consistent uptake by processors handling large product volumes.

The fastest-growing type is biodegradable absorbent pads, driven by increasing global emphasis on sustainability and stricter packaging regulations. Manufacturers are scaling production of starch-based and PLA-integrated pads, which are now being trialed in major supermarket chains as eco-friendly replacements for conventional pads. Early tests demonstrate comparable absorption efficiency, while offering compostability within industrial facilities.

Other niche segments include antimicrobial pads, gaining attention for their ability to suppress bacterial growth through silver-ion or plant-based additives, and standard pads, which remain cost-effective options for low-drip food categories like bakery and produce. Together, this diverse product landscape ensures both mainstream and specialized demands are met.

The most prominent application for absorbent pads is in the packaging of meat and poultry, where they serve as a critical tool in preventing leakage, preserving freshness, and enhancing visual appeal. This segment dominates because of the high moisture release associated with poultry and red meat, and industry reliance on pads to maintain strict food safety compliance.

The fastest-growing application is fresh fruits and vegetables, where absorbent pads are being increasingly adopted to extend freshness during transport and storage. Pads specifically designed with breathable layers and antimicrobial additives are showing strong uptake among exporters and supermarkets, as consumer demand for longer-lasting produce rises.

Seafood is another important application, with absorbent pads providing necessary fluid management during shipping of high-value products. Ready-to-eat meals and bakery packaging utilize thinner pads with moderate absorption capacity to control condensation, prevent sogginess, and improve shelf presentation. Collectively, these applications demonstrate how pads are being customized across food categories to meet functional requirements and reduce spoilage rates.

Food processors represent the leading end-user segment in the Absorbent Pads for Food Packaging Market. Their dominance stems from high-volume production environments where pads are incorporated into automated packing lines to ensure consistency, compliance with hygiene regulations, and minimization of leakage in downstream logistics.

The fastest-growing end-user category is e-commerce food delivery services, as the rise of online grocery platforms and fresh meal-kit subscriptions requires efficient, lightweight, and safe packaging solutions. Pads tailored for direct-to-consumer delivery are designed with higher absorption-to-weight ratios and compact formats to align with courier distribution requirements.

Supermarkets and retail packaging companies also play an important role, often dictating pad specifications to match shelf presentation standards and sustainability commitments. Smaller but relevant end-users include food exporters, particularly in seafood and fresh produce, who rely on pads to maintain quality during international shipping. This evolving end-user mix reflects a balance between traditional large-scale processors and the rapidly expanding digital food retail sector, shaping the future trajectory of the market.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

The Asia-Pacific region’s dominance is underpinned by its extensive manufacturing base, strong consumer demand for packaged meat and seafood, and the rapid adoption of sustainable materials in packaging technologies. North America, meanwhile, is projected to achieve the most significant growth due to rising demand for eco-friendly packaging solutions, stringent food safety regulations, and ongoing technological modernization within the packaging industry.

North America represented 26% of the Absorbent Pads for Food Packaging Market in 2024, with the United States and Canada as key contributors. High demand originates from the meat and poultry processing industries, along with a growing fresh produce and meal-kit delivery sector. Government emphasis on food safety compliance and single-use plastic reduction has accelerated the shift toward biodegradable and compostable absorbent pads. Digital transformation initiatives, including AI-based quality monitoring and IoT-enabled packaging lines, are gaining traction among large processors to ensure efficiency and compliance. Retailers in the region also mandate strict packaging standards, further fueling innovation and uptake of advanced absorbent pad solutions.

Europe held 21% of the Absorbent Pads for Food Packaging Market in 2024, with Germany, the United Kingdom, and France leading demand. Regional sustainability initiatives, such as the EU’s circular economy targets and packaging waste reduction directives, are encouraging manufacturers to transition to compostable and recyclable pad materials. Adoption of antimicrobial and multifunctional pads is accelerating across supermarkets to address food waste reduction goals. European companies are also at the forefront of smart pad technologies, including freshness-indicating pads, with early trials in major retail chains. Regulatory pressure combined with consumer demand for sustainable solutions makes Europe a hub for innovation in absorbent pad technologies.

Asia-Pacific dominated the Absorbent Pads for Food Packaging Market with 42% share in 2024. China remains the top consumer and producer, leveraging extensive production capacity and heavy investment in high-speed converting lines. India and Japan also represent major markets due to rising urbanization and demand for ready-to-eat foods. Infrastructure improvements and increasing adoption of automation in regional food processing facilities are reinforcing the use of absorbent pads. Innovation hubs in China and Japan are developing biodegradable and sensor-integrated pads, which are gradually being adopted across export-oriented industries such as seafood and fresh produce. This makes Asia-Pacific both a production and consumption leader in the market.

South America contributed 6% of the Absorbent Pads for Food Packaging Market in 2024, led by Brazil and Argentina. Demand is largely concentrated in the meat and seafood export industries, where absorbent pads are vital for maintaining quality during long-distance shipments. Regional governments are supporting food packaging modernization with policies encouraging adoption of hygienic and eco-friendly packaging solutions. Infrastructure upgrades, particularly in cold chain logistics, are also boosting the use of absorbent pads in export operations. Although smaller in overall market share, the region presents steady opportunities for growth as its food exports expand globally.

The Middle East & Africa accounted for 5% of the Absorbent Pads for Food Packaging Market in 2024, with the UAE and South Africa at the forefront. Growing urban retail networks and expanding meat processing facilities are driving regional adoption. Technological modernization, including the installation of automated pad-converting lines, is becoming increasingly common. Trade partnerships with Europe and Asia are encouraging alignment with international food packaging standards. Local regulatory frameworks promoting food safety and waste reduction are also supporting the steady integration of absorbent pads across both domestic and export-oriented food supply chains.

China – 28% Market Share

Dominates the Absorbent Pads for Food Packaging Market due to its expansive production capacity, large domestic consumption of packaged meat and seafood, and continuous investment in sustainable pad technologies.

United States – 18% Market Share

Leads with strong demand from industrial meat processors, rapid adoption of biodegradable pad solutions, and technological advancements in automated and AI-driven packaging lines.

The Absorbent Pads for Food Packaging Market is characterized by a moderately fragmented competitive landscape, with over 40 active international and regional manufacturers. Competition is driven by innovation, cost efficiency, and compliance with evolving sustainability regulations. Leading players are investing in product diversification, particularly biodegradable and antimicrobial pads, to differentiate themselves. Strategic initiatives such as mergers, cross-border partnerships, and licensing agreements are increasingly common, allowing firms to strengthen distribution channels and expand product portfolios across multiple geographies. Several competitors have announced expansions of production facilities in Asia-Pacific and North America to meet rising demand from meat and seafood packaging industries. Innovation trends are strongly shaping the market, with companies introducing multilayer composite pads, smart freshness-indicating solutions, and automated production lines capable of reducing material wastage by up to 20%. The emphasis on sustainability and technological modernization is intensifying competition, as companies seek to secure long-term contracts with global retailers and food processors while positioning themselves as leaders in eco-friendly packaging solutions.

Novipax

McAirlaid’s Vliesstoffe GmbH

Paper Pak Industries

Sirane Ltd.

Gelok International

Cellcomb AB

Thermoform Engineered Quality LLC (TEQ)

Attindas Hygiene Partners

NEXX Technologies

Delta Absorbents

The Absorbent Pads for Food Packaging Market is being reshaped by a wave of technological innovations that focus on performance, sustainability, and digital integration. One of the most prominent advancements is the use of superabsorbent polymers (SAPs) that enable pads to retain liquids many times their weight, significantly extending product shelf life. New formulations are incorporating antimicrobial additives, such as silver ions or plant-derived compounds, to reduce bacterial activity and improve food safety in perishable categories.

Biodegradable and compostable technologies are also advancing, with pads made from polylactic acid (PLA), starch, and cellulose fibers increasingly adopted in response to global regulatory shifts on single-use plastics. These products are engineered to maintain absorption capacity while meeting industrial composting timelines of under 12 weeks. At the same time, multilayer composite pads with breathable top sheets are gaining traction, particularly in fresh produce packaging, where they help maintain optimal humidity levels.

Digital technologies are beginning to transform the sector as well. Smart absorbent pads embedded with pH-sensitive indicators and freshness sensors are under trial, capable of signaling food spoilage in real time. Automated converting lines equipped with AI-based vision systems are reducing pad defects and improving efficiency, with some manufacturers reporting defect detection accuracy above 95%. Collectively, these advancements demonstrate how the Absorbent Pads for Food Packaging Market is converging around sustainability, efficiency, and intelligent packaging solutions tailored for modern supply chains.

• In March 2023, a leading packaging company launched compostable absorbent pads made from PLA and starch-based materials, designed to degrade within 90 days under industrial composting, reducing landfill dependency and supporting sustainable retail initiatives.

• In October 2023, a European food-packaging manufacturer introduced antimicrobial absorbent pads with embedded plant-based additives, achieving a 35% reduction in microbial growth during shelf-life testing for poultry and seafood products.

• In May 2024, a Japanese firm unveiled freshness-indicating absorbent pads with pH-sensitive dyes, enabling visual spoilage detection within 30 minutes of meat degradation, significantly improving food safety monitoring across retail chains.

• In July 2024, a North American producer installed AI-driven quality control systems in its absorbent pad manufacturing lines, reducing material waste by 22% and improving throughput efficiency by nearly 18% compared to traditional inspection methods.

The scope of the Absorbent Pads for Food Packaging Market Report covers a comprehensive analysis of the industry’s structural, technological, and regional dimensions, offering decision-makers a detailed framework for strategic planning. The report examines product segmentation across standard pads, multilayer composites, antimicrobial solutions, and biodegradable/compostable pads, highlighting their role in addressing functional requirements of different food categories. Applications explored include meat and poultry, seafood, fresh produce, bakery, and ready-to-eat meals, with insights into consumption trends across traditional retail and e-commerce channels.

Regionally, the report provides in-depth insights into Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, identifying market leadership in Asia-Pacific and highlighting fast-growing opportunities in North America. Industry dynamics are contextualized through analysis of regulatory landscapes, sustainability initiatives, and regional demand drivers.

From a technological standpoint, the report emphasizes innovations such as superabsorbent polymers, antimicrobial additives, biodegradable substrates, and emerging smart pad technologies that incorporate sensors for real-time freshness monitoring. End-user insights cover large-scale food processors, supermarkets, exporters, and digital retail platforms, reflecting how industry adoption patterns are evolving in line with global food supply chain modernization.

The report’s breadth ensures coverage of both established and emerging market segments, offering a strategic perspective on drivers, restraints, opportunities, and challenges shaping the Absorbent Pads for Food Packaging Market. This structured scope enables stakeholders to evaluate investment opportunities, competitive positioning, and future growth strategies across a dynamic and sustainability-driven packaging industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 455 Million |

| Market Revenue (2032) | USD 836.0 Million |

| CAGR (2025–2032) | 7.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Novipax, McAirlaid’s Vliesstoffe GmbH, Paper Pak Industries, Sirane Ltd., Gelok International, Cellcomb AB, Thermoform Engineered Quality LLC (TEQ), Attindas Hygiene Partners, NEXX Technologies, Delta Absorbents |

| Customization & Pricing | Available on Request (10% Customization is Free) |