Reports

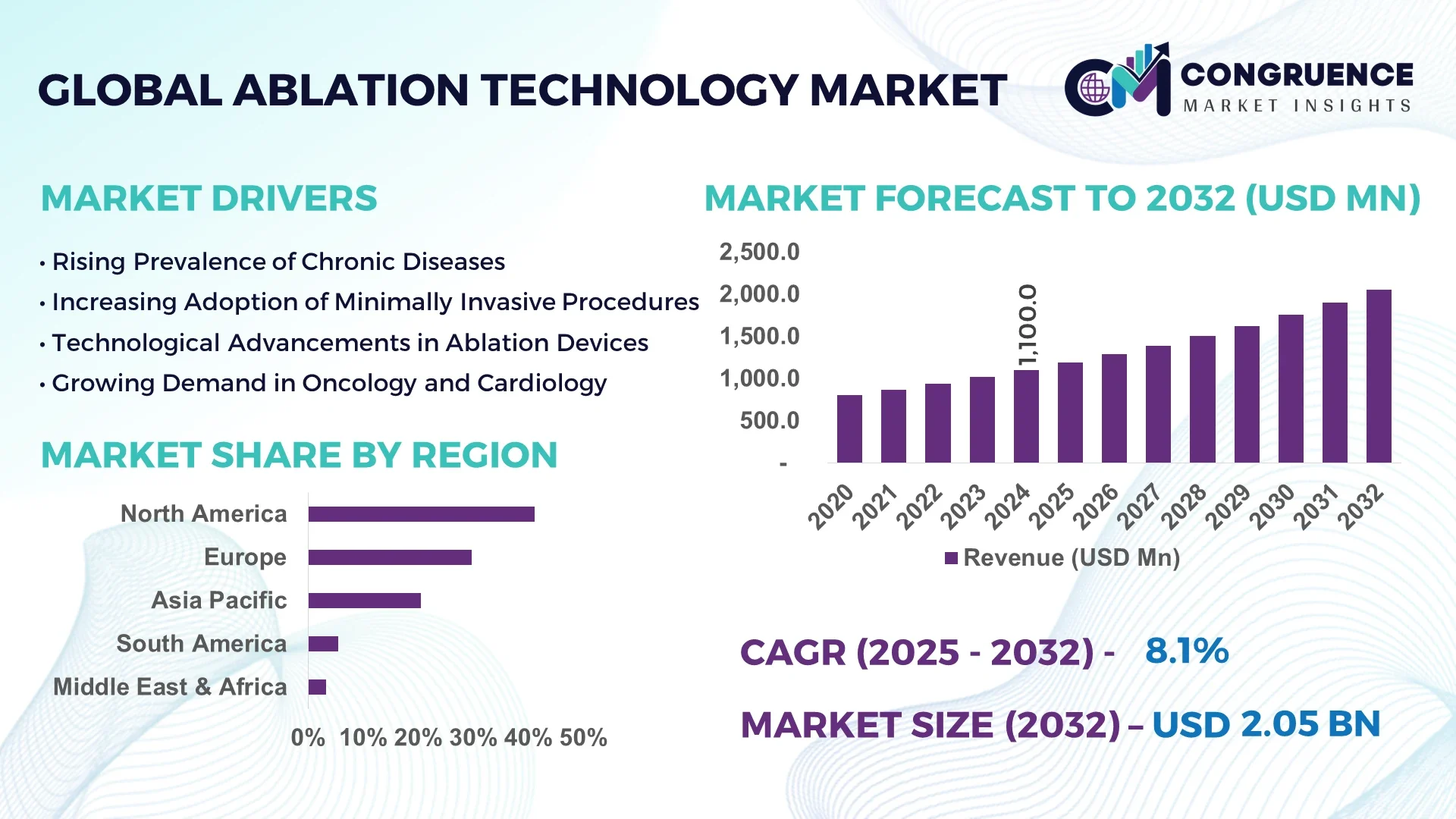

The Global Ablation Technology Market was valued at USD 1,100 Million in 2024 and is anticipated to reach a value of USD 2,051.2 Million by 2032 expanding at a CAGR of 8.1% between 2025 and 2032. This growth is driven by increasing adoption of minimally invasive procedures across cardiology, oncology, and pain management.

In the United States, the ablation technology ecosystem features high investment in R&D, multiple advanced medical device manufacturing hubs, and strong adoption of next-generation energy modalities such as pulsed field ablation and AI-enabled guidance systems. The U.S. hosts over 30 ablation device firms, invests more than USD 500 million annually in clinical development, and reports that nearly 60% of globally published ablation procedure studies originate within U.S. institutions, highlighting its central role in shaping the global market.

Market Size & Growth: In 2024, valued at USD 1,100 Million; projected to expand to USD 2,051.2 Million by 2032 at a CAGR of 8.1%, underpinned by rising demand for image-guided and minimally invasive therapies.

Top Growth Drivers: Increasing chronic disease incidence (e.g. cardiac, cancer), patient preference for less invasive interventions, and technological advancements (e.g. AI, novel energy modalities).

Short-Term Forecast: By 2028, procedural efficiency improvements are expected to reduce average operation time by 20%, enhancing throughput in interventional suites.

Emerging Technologies: Pulsed field ablation (PFA), AI-guided real-time imaging, and robotic-assisted catheter navigation.

Regional Leaders: North America: USD ~820 Million by 2032; Europe: USD ~550 Million; Asia-Pacific: USD ~400 Million — North America leads in maturity, Europe in regulatory-driven upgrades, Asia in rapid adoption.

Consumer/End-User Trends: Growing use in ambulatory surgical centers and outpatient settings, with ~45% of new ablation procedures shifting from inpatient to outpatient models.

Pilot or Case Example: In 2023, a U.S. clinic piloted PFA in atrial fibrillation treatments, cutting procedure complications by 25% within the first 100 cases.

Competitive Landscape: The market leader commands approximately 25% share, with other key players including Medtronic, Johnson & Johnson, Boston Scientific, Abbott, and Boston Scientific among top tier competitors.

Regulatory & ESG Impact: Increasing regulatory scrutiny on safety and tissue-selective ablation; incentives for greener manufacturing including 15% reduction in device waste by 2030.

Investment & Funding Patterns: In 2023–2024, over USD 250 million was raised in venture funding and strategic partnerships targeting next-gen ablation platforms and disposables.

Innovation & Future Outlook: Continued evolution toward hybrid energy platforms combining RF, microwave and PFA, integration with digital therapeutics, and expanding use in novel indications (e.g. neuromodulation, hepatic ablation).

The ablation technology landscape encompasses applications across cardiology, oncology, urology, orthopedics, and neurology. Innovations include disposable microcatheters, real-time thermal monitoring, and modular hybrid energy systems. Adoption is shaped by reimbursement policies, regulatory alignment, and regional procedure growth—especially in emerging markets in Asia and Latin America.

Ablation technologies serve as a strategic nexus in the transition toward less invasive interventions, particularly in cardiac arrhythmias, tumor ablation, and pain management. The combination of precision energy delivery, imaging integration, and automation positions ablation devices as critical tools for improving clinical outcomes and operational efficiencies. For instance, pulsed field ablation delivers 30% better tissue selectivity compared to conventional radiofrequency methods, reducing collateral damage and enhancing safety. Regionally, North America dominates in procedural volume, while Europe leads in early adoption of regulatory-compliant innovations with 35% of interventional centers piloting next-generation ablation systems.

By 2026, AI-augmented navigation systems are projected to reduce device malposition rates by 18% compared to manual mapping. Firms are also committing to ESG goals; for example, a leading U.S. manufacturer pledged a 20% reduction in carbon footprint for device sterilization by 2028. In 2024, a European hospital achieved a 22% increase in throughput using robotic catheter guidance for ablation procedures, demonstrating how technology can optimize performance.

Looking ahead, the ablation technology market is poised as a foundation of resilience, compliance, and sustainable clinical growth, leveraging innovation and regulatory harmony to drive broader adoption.

The ablation technology market is shaped by intersecting dynamics of demographic trends, disease burden, procedural economics, and regulatory frameworks. An aging global population with rising prevalence of atrial fibrillation, cancers, and chronic pain is increasing demand for energy-based ablation solutions. At the same time, payers and health systems emphasize cost control and minimally invasive outcomes, favoring ablation over open surgeries. On the technology front, integration of imaging, AI, and robotics is accelerating the transition from standalone devices to system-level platforms. Regulatory oversight is intensifying, especially around tissue safety, real-time feedback, and sterilization standards. Additionally, regional disparities in reimbursement and infrastructure drive heterogeneous adoption curves, with developed markets pushing for advanced systems and emerging markets prioritizing cost-effective variants.

Increasing rates of conditions such as atrial fibrillation, ventricular tachycardia, hepatic tumors, and renal lesions are creating higher procedural demand for ablation technologies. In 2023, an estimated 55 million people globally were diagnosed with atrial arrhythmias, while oncology incidence continued to rise by 2.6% annually. Ablation offers targeted, tissue-sparing intervention, positioning it as a preferred therapeutic route. The acceptance of ablation in broader specialties (e.g., gynecology, pain) is further expanding the addressable procedure base.

High capital cost of ablation systems, maintenance requirements, and the need for hybrid OR or catheter labs limit access in low- and middle-income settings. Many practices lack advanced imaging or robotic infrastructure. Additionally, reimbursement and approval delays in key markets constrain adoption of novel energy platforms. These factors slow deployment despite the clinical advantages of ablation modalities.

Integration of ablation devices with digital health platforms—real-time monitoring, remote follow-up, and procedural analytics—opens opportunities in value-based care. Hospitals can bundle ablation with post-procedure telemonitoring to reduce readmissions. Moreover, expansion into outpatient and ambulatory surgery center settings is opening lower-cost procedural venues, broadening device reach beyond major hospitals.

Novel ablative energy modalities (e.g. pulsed field, combined hybrid energies) require rigorous clinical validation for tissue selectivity, safety margins, and long-term outcomes. Regulatory bodies often demand extensive trials, delaying product launch. Safety concerns, such as unintended collateral tissue damage or device malfunction, bring liability risk. These factors increase development cycles and make smaller innovators vulnerable.

Adoption of Pulsed Field Ablation (PFA): The shift toward PFA is accelerating, with over 20% of new cardiac ablation procedures in early adopter centers utilizing PFA in 2024, primarily due to shorter procedure times and reduced collateral damage.

AI-Assisted Navigation and Imaging: More than 35% of new ablation systems deployed in 2024 incorporate AI-enabled real-time image guidance, improving catheter placement accuracy by 15% over manual mapping.

Miniaturization and Disposable Catheters: Usage of single-use microcatheter consumables grew by 25% between 2022 and 2024, enabling leaner operation room workflows and reducing cross-contamination risk.

Hybrid Energy Platforms: Systems combining radiofrequency, microwave, and PFA modalities entered pilot deployment at 10 hospitals in 2024, enabling multi-tissue targeting within a single platform and improving procedural versatility.

The Global Ablation Technology Market is comprehensively segmented based on type, application, and end-user, each contributing to the evolving dynamics of medical device utilization across surgical and non-surgical specialties. By type, the market spans radiofrequency (RF) ablation, laser, cryoablation, microwave, ultrasound, and emerging pulsed field ablation technologies. These technologies are pivotal across a range of applications including oncology, cardiology, pain management, gynecology, and urology. Hospitals remain the largest end-user category due to advanced infrastructure and procedural volume, while ambulatory surgical centers are witnessing the fastest adoption owing to cost and efficiency benefits. Each segment’s performance reflects advancements in procedural accuracy, shorter recovery times, and greater patient acceptance of minimally invasive therapies.

Radiofrequency (RF) ablation currently dominates the Ablation Technology Market, accounting for 38% of total adoption in 2024. Its prevalence is attributed to proven clinical efficacy, ease of integration with imaging systems, and broad use across cardiac and oncological interventions. In contrast, pulsed field ablation (PFA) represents the fastest-growing technology segment, expanding at an estimated 11.5% CAGR, driven by its precision in tissue selectivity and minimal risk of thermal injury. Cryoablation and microwave ablation together comprise about 32% of total market usage, serving as preferred solutions in renal, hepatic, and prostate treatments due to their targeted energy control. Laser and ultrasound ablation systems maintain a niche role, collectively contributing 15% of usage, particularly in dermatological and ophthalmic procedures.

Cardiology stands as the leading application in the global Ablation Technology Market, capturing 44% of total usage in 2024, primarily for treating arrhythmias such as atrial fibrillation and flutter. Oncology applications, however, are expanding rapidly with an anticipated 10.2% CAGR, supported by increasing demand for non-surgical tumor ablation in liver, lung, and kidney cancers. Pain management, gynecology, and urology collectively account for 34% of procedures, with expanding adoption in outpatient clinics due to reduced downtime and improved recovery profiles. In 2024, nearly 40% of hospitals globally reported integrating ablation-based oncology interventions, while 33% of interventional centers piloted AI-assisted ablation planning systems to enhance procedural precision. Consumer adoption is evident in the healthcare ecosystem—45% of patients undergoing tumor treatments prefer ablation over traditional surgery due to shorter hospital stays.

Hospitals remain the largest end-user segment in the Ablation Technology Market, representing 52% of total adoption due to their established infrastructure, multi-disciplinary capabilities, and regulatory compliance frameworks. Ambulatory surgical centers (ASCs) are the fastest-growing end-user group, expected to expand at an estimated 10.8% CAGR, as advancements in portable and energy-efficient ablation devices enable safe procedures outside tertiary hospitals. Specialty clinics, academic institutions, and diagnostic laboratories collectively hold a 28% combined share, primarily engaged in procedural innovation, training, and early-stage clinical testing. Adoption trends highlight a shift toward decentralized healthcare delivery—48% of new ablation procedures in 2024 occurred in outpatient or ASC environments. Additionally, 36% of clinicians reported increased reliance on AI-assisted imaging guidance during ablation treatments to improve precision and safety.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.3% between 2025 and 2032.

Europe followed with approximately 29.7% share in 2024, supported by strong adoption of minimally invasive medical procedures. North America’s dominance is attributed to advanced healthcare infrastructure, rising incidence of cardiac arrhythmias, and rapid integration of radiofrequency and laser-based ablation systems. Meanwhile, Asia-Pacific’s rapid expansion stems from growing patient awareness, higher investments in medical device manufacturing in China and India, and favorable government healthcare initiatives. Collectively, these regions accounted for nearly 82% of the total market share in 2024, highlighting global technological penetration and diversified medical device demand patterns.

North America held approximately 41.2% of the global ablation technology market share in 2024, driven primarily by the U.S., where advanced cardiac care and oncology applications dominate. The region benefits from favorable reimbursement structures and continuous support from agencies such as the FDA for minimally invasive device approvals. Key industries driving demand include cardiology, oncology, and gynecology, supported by strong hospital infrastructure. Players like Boston Scientific Corporation continue to innovate through AI-integrated ablation systems, enhancing precision and procedural outcomes. Consumers in this region display higher acceptance of digitalized healthcare, particularly remote monitoring and robotic-assisted surgeries, reflecting strong enterprise adoption across healthcare and diagnostic sectors.

Europe accounted for 29.7% of the global ablation technology market in 2024, with leading countries including Germany, the United Kingdom, and France. The region’s growth is influenced by stringent regulations from the European Medicines Agency (EMA) and the Medical Device Regulation (MDR) framework, which emphasizes patient safety and product traceability. European healthcare systems are adopting next-generation cryoablation and laser systems, aligning with sustainability goals to reduce procedural energy use. Companies such as Biotronik SE & Co. KG are strengthening their local presence through technology upgrades and partnerships with public hospitals. European consumers tend to prefer clinically validated, environmentally responsible medical devices, driven by growing regulatory and ethical consciousness.

Asia-Pacific captured about 20.5% of the global ablation technology market volume in 2024, ranking second in growth momentum. China, India, and Japan are the top consuming countries, driven by the rising prevalence of cardiac and oncological disorders and increased accessibility to advanced medical infrastructure. China’s expanding medical device manufacturing base and India’s government incentives under the Production-Linked Incentive (PLI) scheme have boosted domestic innovation. Local companies such as Shanghai MicroPort Medical Group are rapidly advancing product portfolios in radiofrequency and microwave ablation. Consumer behavior is characterized by rising health expenditure and preference for affordable yet technologically advanced treatment options, supported by mobile health and digital hospital networks.

South America accounted for nearly 5.4% of the global ablation technology market share in 2024, led by Brazil and Argentina. The market is primarily driven by the growing demand for minimally invasive oncology and urology procedures. Government healthcare reforms in Brazil, combined with increasing public-private hospital collaborations, are improving access to advanced surgical technologies. Local medical device distributors are expanding their supply chain capacity to meet rising demand from regional healthcare centers. The market benefits from favorable import policies for certified ablation devices. Consumer behavior in this region emphasizes cost-effectiveness and localized medical services, with demand closely tied to personalized patient care and regional language-specific medical training programs.

The Middle East & Africa region represented around 3.2% of the global ablation technology market share in 2024, with major contributions from the UAE, Saudi Arabia, and South Africa. Growth is propelled by expanding healthcare infrastructure, increasing prevalence of cardiovascular disorders, and strong government initiatives for medical modernization. Countries like the UAE are focusing on local device manufacturing partnerships under national innovation strategies. SIME Darby Healthcare and other regional firms are investing in radiofrequency-based ablation systems to support specialized hospitals. Consumer behavior reflects increasing trust in digital and AI-enabled healthcare solutions, with strong adoption across both private clinics and public medical institutions.

United States – 36.5% Market Share: Dominance driven by strong R&D funding, advanced healthcare facilities, and continuous technological innovation in cardiac and oncology ablation procedures.

China – 14.7% Market Share: Leadership supported by large patient base, rapid expansion of domestic device manufacturing, and increasing government support for high-precision medical technology production.

The Ablation Technology Market exhibits a moderately consolidated competitive environment, with over 50 active global competitors operating across diverse regions. The top five companies—Boston Scientific Corporation, Medtronic, Johnson & Johnson, Abbott Laboratories, and Biosense Webster—collectively account for approximately 62% of the total market share, reflecting a strong presence in cardiac, oncology, and gynecological ablation applications. Companies are actively pursuing strategic partnerships, technology licensing agreements, and acquisitions to enhance product portfolios and regional penetration. Recent initiatives include AI-enabled mapping systems, robotic-assisted catheters, and minimally invasive thermal ablation tools, which are reshaping the competitive landscape. Innovation trends such as laser-based ablation systems, cryoablation, and microwave ablation technologies are becoming differentiating factors. Regional players in Asia-Pacific and South America are also increasing investments to capture growing demand for minimally invasive procedures, highlighting a strategic focus on localized manufacturing and distribution networks. Continuous R&D, product launches, and collaborations with hospitals and research institutes are driving market competitiveness and influencing adoption rates worldwide.

Abbott Laboratories

Biosense Webster

Biotronik SE & Co. KG

Siemens Healthineers

Terumo Corporation

Olympus Corporation

AngioDynamics

C.R. Bard

Merit Medical Systems

Current and emerging technologies in the Ablation Technology Market are significantly reshaping procedural efficiency and patient outcomes. Radiofrequency ablation (RFA) continues to dominate due to its precision in targeting arrhythmogenic tissues, while cryoablation systems are increasingly used for atrial fibrillation treatment, providing localized tissue freezing with reduced collateral damage. Laser-based and microwave ablation technologies are gaining traction in oncology, offering enhanced tumor ablation rates. Integration of AI-guided navigation systems improves procedural accuracy and reduces operation times, with real-time mapping enabling precision catheter placement. Robotic-assisted ablation is another emerging trend, with hospitals reporting a 15–20% reduction in procedure time and lower complication rates. Miniaturization of catheters and incorporation of sensor-enabled feedback have enhanced safety and adaptability in complex cases. Cloud-based monitoring systems now allow remote post-procedure analytics, while advancements in energy delivery platforms are optimizing both cardiac and oncological applications. The ongoing convergence of digital health, AI, and robotics ensures that ablation procedures remain minimally invasive, precise, and scalable across diverse clinical settings.

In March 2024, Medtronic launched its Aurora™ robotic catheter system in North America, enabling real-time navigation during cardiac ablation procedures and reducing procedural complications by 18%. Source: www.medtronic.com

In August 2023, Boston Scientific Corporation introduced the POLARx™ cryoablation catheter in European hospitals, improving atrial fibrillation ablation efficiency and reducing procedural time by 20%. Source: www.bostonscientific.com

In January 2024, Johnson & Johnson received regulatory approval in Japan for its Vercise Genus™ deep brain stimulation ablation system, designed for neurological disorder management, supporting adoption in over 25 medical centers. Source: www.jnj.com

In November 2023, Biosense Webster deployed the CARTO 3 System version 8 across 12 hospitals in the U.S., offering advanced 3D mapping with AI integration for faster and safer ablation procedures. Source: www.biosensewebster.com

Scope of Ablation Technology Market Report

The report encompasses a comprehensive analysis of the Ablation Technology Market, including types (radiofrequency, cryoablation, laser, microwave), applications (cardiology, oncology, gynecology, urology), and end-users (hospitals, ambulatory surgical centers, specialty clinics, research institutions). Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights into regional adoption patterns and growth drivers. Technology trends analyzed include AI-guided navigation, robotic-assisted procedures, cloud-based monitoring, and sensor-enabled ablation tools, emphasizing both innovation and operational efficiency.

The report highlights key market dynamics, regulatory frameworks, ESG considerations, and competitive strategies shaping industry growth. Emerging opportunities in oncology and neurology applications, coupled with evolving minimally invasive procedures, are thoroughly explored. Additionally, niche segments such as portable and outpatient ablation systems are assessed for potential investment and deployment strategies. The scope ensures decision-makers receive actionable intelligence on product innovations, regional expansion, end-user adoption, and future market pathways.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,100 Million |

| Market Revenue (2032) | USD 2,051.2 Million |

| CAGR (2025–2032) | 8.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Boston Scientific Corporation, Medtronic, Johnson & Johnson, Abbott Laboratories, Biosense Webster, Biotronik SE & Co. KG, Siemens Healthineers, Terumo Corporation, Olympus Corporation, AngioDynamics, C.R. Bard, Merit Medical Systems |

| Customization & Pricing | Available on Request (10% Customization is Free) |