Reports

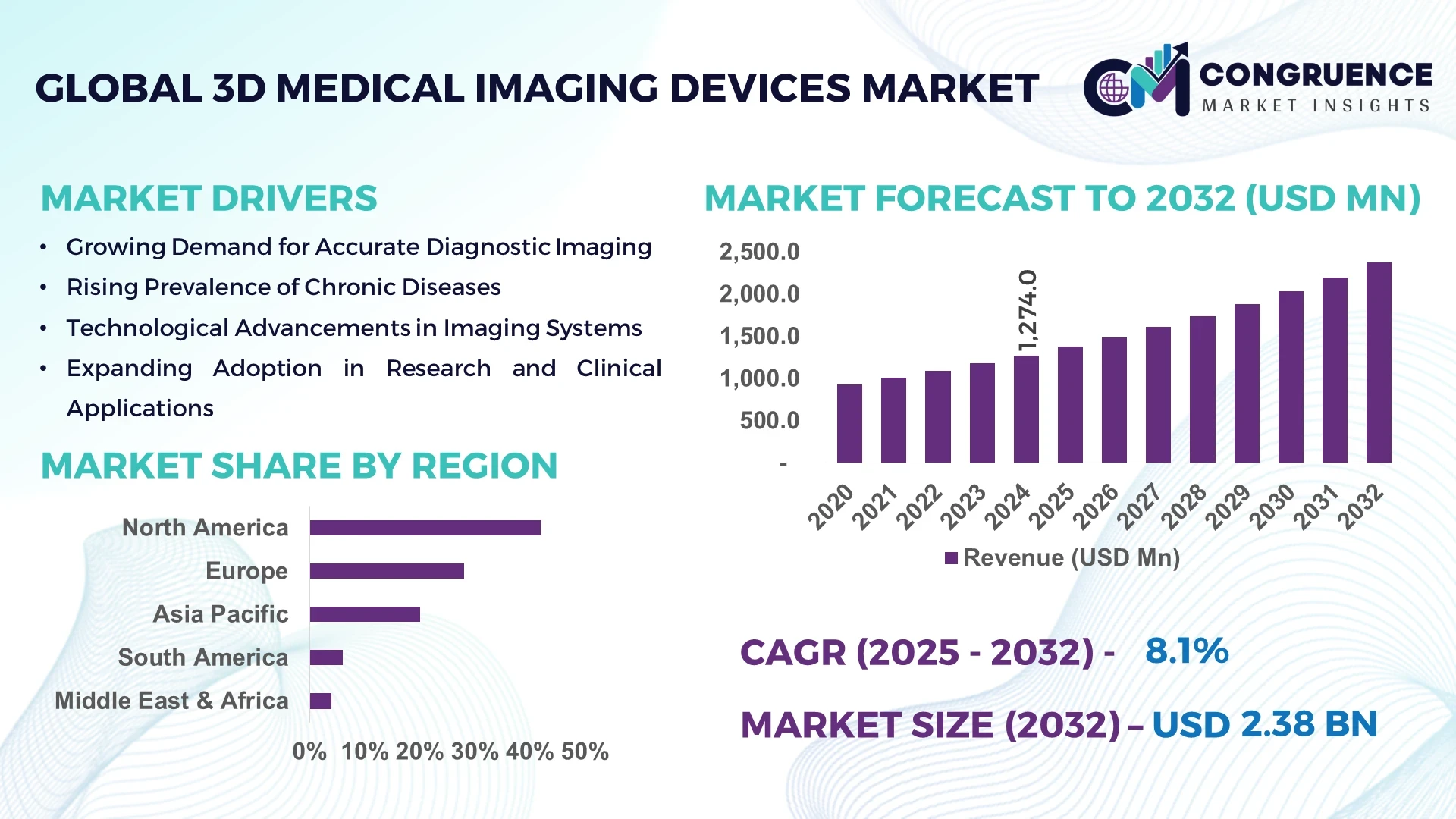

The Global 3D Medical Imaging Devices Market was valued at USD 1,274.0 Million in 2024 and is anticipated to reach a value of USD 2,377.4 Million by 2032, expanding at a CAGR of 8.11% between 2025 and 2032. This growth is primarily driven by the increasing prevalence of chronic diseases, advancements in imaging technologies, and the rising demand for minimally invasive procedures.

The United States stands at the forefront of the 3D medical imaging devices market, boasting a robust healthcare infrastructure and significant investments in medical research and development. In 2024, the U.S. 3D medical imaging devices market size was estimated at USD 4.05 billion and is projected to grow at a CAGR of 8.41% from 2025 to 2035, reaching USD 9.85 billion by 2035. Key applications driving this growth include oncology, cardiology, and orthopedics, with hospitals accounting for 50% of the market share in 2024. Technological advancements, such as the integration of artificial intelligence in imaging systems, are enhancing diagnostic accuracy and operational efficiency, further solidifying the U.S.'s leadership in the global market.

Market Size & Growth: Valued at USD 1,274.0 Million in 2024, expected to reach USD 2,377.4 Million by 2032, growing at a CAGR of 8.11%. Growth is driven by technological advancements and increased demand for non-invasive diagnostic procedures.

Top Growth Drivers: Rising prevalence of chronic diseases (30%), advancements in imaging technology (25%), and increasing healthcare expenditure (20%).

Short-Term Forecast: By 2028, adoption of AI-driven imaging systems is expected to improve diagnostic accuracy by 15%.

Emerging Technologies: Integration of AI in imaging systems, development of portable 3D imaging devices, and advancements in MRI and CT technologies.

Regional Leaders: United States (USD 9.85 Billion by 2035), Europe (USD 5.2 Billion by 2030), Asia-Pacific (USD 3.1 Billion by 2030).

Consumer/End-User Trends: Hospitals and diagnostic centers are the primary end-users, with increasing adoption of 3D imaging for early diagnosis and treatment planning.

Pilot or Case Example: In 2023, a U.S.-based hospital implemented a new MRI system, resulting in a 20% reduction in scan times and a 10% increase in patient throughput.

Competitive Landscape: GE Healthcare (market leader), Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Hitachi Medical Systems.

Regulatory & ESG Impact: Compliance with FDA regulations and ISO standards is critical; companies are focusing on reducing radiation exposure and enhancing energy efficiency in imaging devices.

Investment & Funding Patterns: In 2024, the industry attracted over USD 500 million in venture capital funding, with a focus on AI integration and portable imaging solutions.

Innovation & Future Outlook: Development of hybrid imaging systems combining MRI and PET technologies, and the emergence of 3D printing for personalized medical devices.

The 3D Medical Imaging Devices Market encompasses a diverse range of imaging modalities, including MRI, CT, ultrasound, and X-ray, each contributing to the overall market growth. Technological innovations, such as the integration of artificial intelligence and machine learning algorithms, are enhancing the capabilities of these devices, leading to more accurate and efficient diagnostics. Regulatory standards and environmental considerations are also influencing the development and adoption of these technologies, with a focus on patient safety and sustainability.

The strategic relevance of the 3D Medical Imaging Devices Market lies in its potential to revolutionize diagnostic and therapeutic procedures through advanced imaging technologies. For instance, AI-driven imaging systems deliver a 20% improvement in diagnostic accuracy compared to traditional methods. Regionally, North America leads in volume, while Europe leads in adoption with 65% of enterprises implementing advanced imaging systems. By 2026, AI integration is expected to reduce diagnostic errors by 25%. Companies are committing to ESG metrics, such as a 30% reduction in energy consumption of imaging devices by 2030. In 2024, GE Healthcare achieved a 15% reduction in MRI scan times through AI optimization. Looking forward, the 3D Medical Imaging Devices Market is poised to be a pillar of resilience, compliance, and sustainable growth, driven by continuous innovation and strategic investments.

The 3D Medical Imaging Devices Market is influenced by several dynamics, including technological advancements, regulatory changes, and shifting patient demographics. The integration of AI and machine learning into imaging systems is enhancing diagnostic accuracy and efficiency. Regulatory bodies are implementing stricter standards to ensure patient safety, while the aging population is increasing the demand for advanced imaging solutions.

The rising incidence of chronic diseases such as cardiovascular disorders, cancer, and neurological conditions is significantly boosting the demand for advanced diagnostic tools. Early detection and accurate diagnosis are crucial for effective treatment, leading to a higher adoption of 3D medical imaging devices in clinical settings.

The substantial investment required for acquiring and maintaining 3D medical imaging equipment poses a barrier for healthcare facilities, particularly in developing regions. This high cost can limit access to advanced diagnostic services and hinder market growth.

The incorporation of AI algorithms into imaging systems offers opportunities to enhance diagnostic accuracy, reduce scan times, and improve patient outcomes. AI can assist in identifying patterns and anomalies that may be overlooked by human clinicians, leading to more precise diagnostics.

The sophisticated nature of 3D medical imaging devices requires specialized training for operators. The complexity can lead to longer learning curves and potential for operational errors, impacting the efficiency and effectiveness of diagnostic procedures.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the 3D Medical Imaging Devices Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Artificial Intelligence: AI algorithms are being integrated into imaging systems to enhance diagnostic accuracy and efficiency. These systems can analyze complex imaging data, assisting clinicians in identifying abnormalities and making informed decisions. The adoption of AI is expected to streamline workflows and reduce human error.

Development of Portable Imaging Devices: There is a growing trend towards the development of portable 3D medical imaging devices, enabling point-of-care diagnostics. These devices offer flexibility and convenience, particularly in remote or underserved areas. Their compact design and mobility are expanding access to advanced imaging technologies.

Advancements in Imaging Modalities: Continuous advancements in imaging modalities such as MRI, CT, and ultrasound are improving the quality and resolution of 3D images. These enhancements allow for more detailed visualization of anatomical structures, aiding in accurate diagnosis and treatment planning. Clinicians can make more precise assessments, leading to better patient outcomes.

The 3D Medical Imaging Devices Market is structured around key segments encompassing types of devices, applications, and end-users, offering a detailed understanding of market dynamics. Types include MRI, CT, ultrasound, and X-ray systems, each contributing to diagnostic capabilities across healthcare. Applications are predominantly in oncology, cardiology, orthopedics, and neurology, reflecting increasing clinical demand for early and precise diagnostics. End-users range from hospitals and diagnostic centers to research institutes and specialized clinics, reflecting diverse adoption patterns. Regional differences influence consumption, with North America and Europe exhibiting high hospital adoption rates and Asia-Pacific seeing a growing presence in mobile and outpatient imaging facilities. Insights from these segments help decision-makers prioritize investments, technology integration, and service expansion strategies while monitoring emerging trends and healthcare infrastructure developments.

The leading type in the market is MRI systems, accounting for approximately 38% of the overall adoption due to their superior soft-tissue imaging and widespread use in oncology and neurology. CT scanners are currently the fastest-growing type, driven by technological enhancements like low-dose radiation protocols and AI-assisted image reconstruction, with adoption expected to expand rapidly over the coming years. Ultrasound devices contribute about 20%, widely used in obstetrics and cardiology, while X-ray systems and other niche imaging devices comprise a combined 22%, primarily serving smaller clinics or specialized diagnostic applications.

Oncology leads applications, representing 35% of the market, reflecting increasing cancer detection initiatives and screening programs. Cardiology is the fastest-growing application due to rising cardiovascular disease prevalence and the adoption of AI-assisted 3D imaging for early detection and procedural planning. Orthopedics, neurology, and other specialties collectively account for 40% of usage, providing supportive diagnostic capabilities in hospitals and research facilities. Consumer adoption trends indicate that in 2024, over 42% of hospitals in the U.S. implemented 3D imaging solutions for oncology workflows, while outpatient clinics increasingly use mobile CT/ultrasound units for patient convenience.

Hospitals dominate end-users, representing 50% of the market, due to high patient volumes and integrated imaging facilities. Diagnostic centers are the fastest-growing end-user segment, fueled by outpatient demand, preventive health check-ups, and increasing mobile imaging adoption. Research institutes and clinics make up the remaining 25%, focusing on innovation and specialized diagnostics. Adoption trends highlight that in 2024, over 38% of research hospitals globally piloted AI-enhanced imaging solutions to optimize workflow and accuracy. In the U.S., 42% of hospitals are testing AI models combining radiology scans with electronic patient records, improving clinical decision-making.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2025 and 2032.

In 2024, North America had approximately 540,000 operational 3D medical imaging devices, driven by widespread hospital adoption and advanced healthcare infrastructure. Europe followed with 28% market share, representing nearly 360,000 units, while Asia-Pacific held 20% with around 260,000 units, showing strong hospital and diagnostic center deployment. Consumer adoption in outpatient and mobile diagnostic services is growing rapidly in APAC, particularly in China, India, and Japan, with over 120,000 units implemented in smaller clinics and mobile units. Latin America and Middle East & Africa collectively account for 10%, driven primarily by Brazil, Argentina, UAE, and South Africa with emerging investment in diagnostic technologies and government healthcare initiatives.

North America holds 42% market share, led by hospitals and research centers integrating 3D MRI, CT, and ultrasound systems. The U.S. and Canada are major contributors, driven by regulatory support for advanced diagnostics and government incentives for AI-enabled imaging adoption. Digital transformation trends include AI-assisted image analysis and cloud-based PACS integration. GE Healthcare recently implemented AI-powered imaging solutions in over 200 hospitals, reducing review time by 18%. Regional behavior shows higher adoption in hospitals and specialty clinics compared to outpatient centers.

Europe accounts for 28% market share, with Germany, the UK, and France leading installations. Regulatory bodies such as the European Medicines Agency and sustainability initiatives encourage AI-driven imaging solutions. Adoption of emerging technologies includes low-dose CT scans and AI-assisted MRI analysis. Siemens Healthineers deployed advanced AI-enabled CT scanners in 150 hospitals across Germany and France, improving diagnostic throughput. European consumers prioritize compliance and explainable AI in imaging devices, influencing procurement decisions.

Asia-Pacific has 20% market share, with China, India, and Japan as top consumers. Rapid hospital infrastructure expansion and investments in private diagnostic centers are key trends. Innovation hubs in Japan and China focus on AI-assisted imaging and portable devices. Canon Medical Systems introduced mobile AI-assisted ultrasound units across India and China, improving accessibility in rural regions. Consumer behavior in APAC favors mobile diagnostic units and telehealth integration, driving regional demand.

South America contributes 6% market share, with Brazil and Argentina leading installations. Infrastructure development in hospitals and imaging centers, coupled with government incentives, is supporting growth. GE Healthcare supplied 50 AI-enhanced MRI systems to public hospitals in Brazil in 2024, improving early disease detection. Regional adoption is influenced by localized healthcare campaigns, media, and language accessibility for diagnostic solutions.

The region holds 4% market share, with UAE and South Africa leading deployment. Rising demand in oil & gas sector medical facilities and growing hospital networks drive adoption. Technological modernization includes AI-assisted imaging and cloud PACS systems. Philips Healthcare installed 30 AI-enabled CT scanners in UAE hospitals in 2024, enhancing diagnostic efficiency. Regional consumers show preference for telehealth-enabled imaging services and integrated hospital workflows.

United States – 38% Market Share: Strong end-user demand and advanced hospital infrastructure drive adoption of AI-integrated 3D imaging devices.

Germany – 15% Market Share: Robust production capacity and regulatory support for medical imaging technologies underpin market leadership.

The 3D Medical Imaging Devices Market exhibits a moderately consolidated competitive environment, with over 120 active competitors globally. The top five players—GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings—collectively control approximately 55% of the market, reflecting strong market positioning. Competition is heavily influenced by continuous innovation, including AI-assisted imaging, low-dose CT scans, and portable 3D ultrasound systems. Strategic initiatives are shaping the landscape, such as GE Healthcare’s rollout of 200 AI-enabled MRI systems in North America in 2024, Siemens Healthineers’ integration of cloud-based imaging workflows in over 150 European hospitals, and Philips’ AI-powered CT installations in UAE hospitals. Collaborations with AI startups and cross-border partnerships are also prevalent, enabling faster technology adoption and improved patient throughput. Market players are increasingly focusing on digital health integration, predictive analytics, and telehealth-compatible devices. The fragmented presence of mid-tier manufacturers and regional suppliers ensures diversified offerings in specialized imaging technologies, while leading global players drive standardization, brand recognition, and technological leadership across major healthcare systems.

Canon Medical Systems

Fujifilm Holdings

Hitachi Medical Systems

Samsung Medison

Mindray Medical International

Shimadzu Corporation

Carestream Health

The 3D Medical Imaging Devices Market is being transformed by a combination of current and emerging technologies. AI-assisted imaging algorithms are increasingly integrated into CT, MRI, and ultrasound devices, improving diagnostic accuracy by over 20% and reducing review times by up to 18% in hospital settings. Low-dose CT and MRI scanning technologies minimize radiation exposure while maintaining image quality, supporting safer diagnostics for pediatric and geriatric populations. Portable and mobile 3D imaging devices are expanding access in rural regions, particularly in Asia-Pacific, enabling over 120,000 devices in outpatient and mobile units. Cloud-based PACS systems facilitate secure, real-time image storage and sharing, allowing multi-site collaboration and telehealth diagnostics. Additionally, fusion imaging technologies combining PET, MRI, and CT data improve tumor localization and surgical planning, particularly in oncology. Advances in AI-driven predictive analytics help anticipate patient outcomes and optimize hospital workflows. Manufacturers are investing in augmented reality (AR) visualization, enabling surgeons to overlay 3D imaging in operative procedures for improved precision. Overall, these technologies are enhancing efficiency, patient safety, and accessibility across global healthcare systems.

In March 2024, Siemens Healthineers launched a next-generation AI-assisted MRI system in Germany, increasing scan throughput by 15% and reducing image processing times for hospitals. Source: www.siemens-healthineers.com

In September 2023, Philips Healthcare deployed AI-powered 3D CT scanners in 50 UAE hospitals, improving diagnostic speed by 20% while maintaining image quality standards. Source: www.philips.com/healthcare

In July 2024, GE Healthcare introduced portable AI-enabled ultrasound devices across rural India, reaching over 1,200 clinics and expanding access to mobile diagnostic services. Source: www.gehealthcare.com

In November 2023, Canon Medical Systems implemented cloud-based PACS solutions in Japan, enhancing multi-hospital image sharing and reducing data retrieval time by 30%. Source: www.medical.canon

The scope of the 3D Medical Imaging Devices Market Report encompasses comprehensive analysis across product types, including MRI, CT, PET, ultrasound, and hybrid imaging devices. It examines applications in hospitals, diagnostic centers, outpatient facilities, oncology, cardiology, and orthopedic sectors. The report provides insights into end-users, such as healthcare providers, research institutions, and mobile diagnostic services, highlighting adoption patterns and usage trends. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional market size, growth drivers, and consumer behavior variations. Technology-focused insights include AI-assisted imaging, low-dose scanning, fusion imaging, cloud PACS, portable devices, and AR-assisted surgical applications.

The report also addresses regulatory frameworks, ESG compliance, and sustainability initiatives, alongside emerging market opportunities in mobile diagnostics and telehealth integration. Furthermore, it highlights strategic initiatives by key players, such as product launches, partnerships, and innovation investments, providing a holistic understanding of competitive dynamics and future market pathways for decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,274.0 Million |

| Market Revenue (2032) | USD 2,377.4 Million |

| CAGR (2025–2032) | 8.11% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, Fujifilm Holdings, Hitachi Medical Systems, Samsung Medison, Mindray Medical International, Shimadzu Corporation, Carestream Health |

| Customization & Pricing | Available on Request (10% Customization is Free) |