Reports

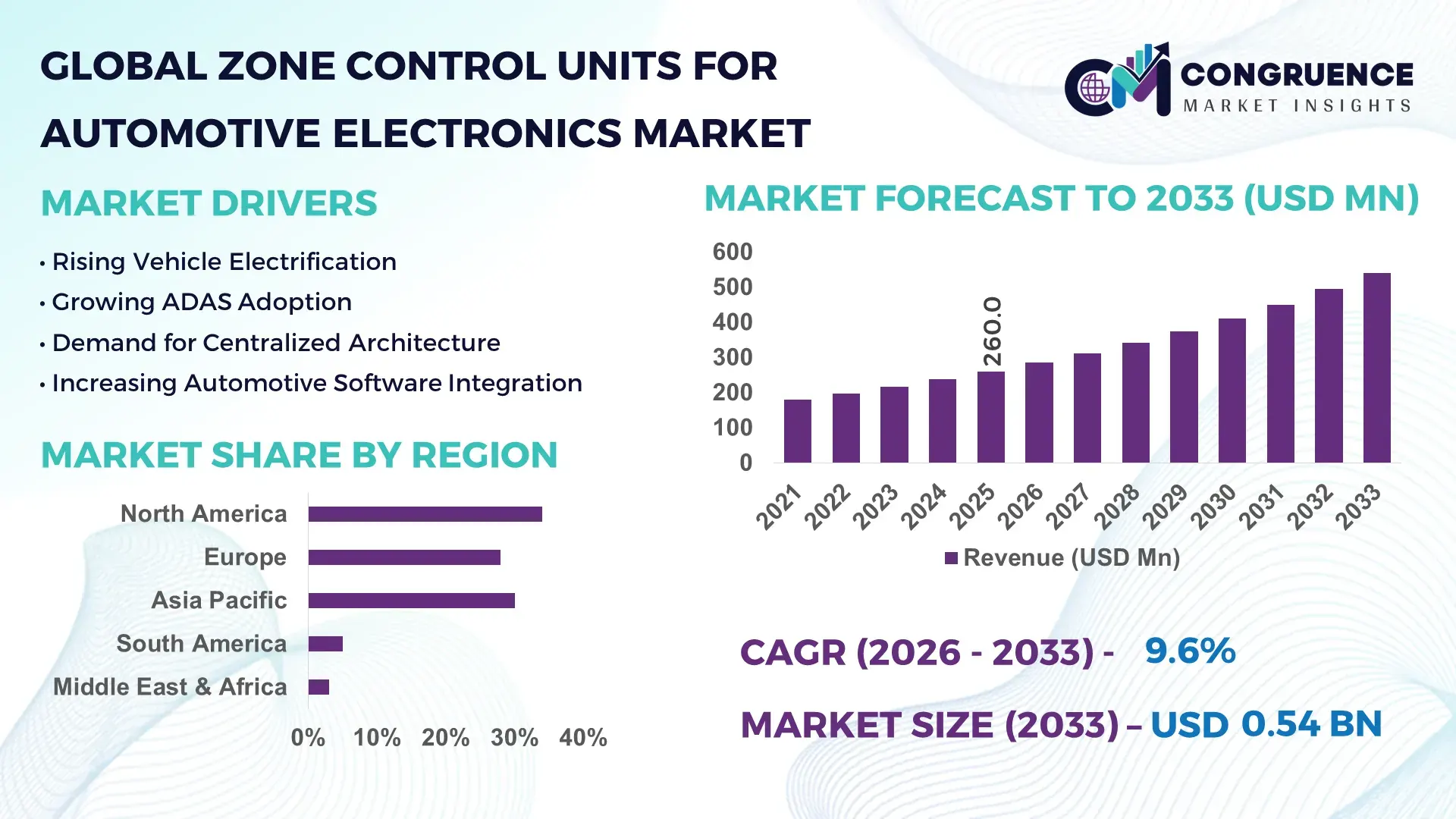

The Global Zone Control Units for Automotive Electronics Market was valued at USD 260.0 Million in 2025 and is anticipated to reach a value of USD 541.3 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rapid transition toward centralized and software-defined vehicle architectures that reduce wiring complexity and improve vehicle efficiency.

The United States remains a dominant force in the Zone Control Units for Automotive Electronics Market, supported by strong automotive electronics production capacity and high R&D investments. In 2025, the U.S. automotive electronics sector accounted for over 28% of global advanced vehicle electronics manufacturing output, with more than USD 18 billion invested annually in autonomous and connected vehicle technologies. Over 62% of new vehicles produced in North America now incorporate zonal or domain-based architectures. Leading OEMs are deploying ZCUs across EV platforms, with integration rates exceeding 45% in premium electric vehicles. Additionally, more than 70% of automotive semiconductor innovation patents related to vehicle networking and control systems originate from U.S.-based firms, reinforcing technological leadership in this space.

Market Size & Growth: USD 260.0 Million in 2025, projected to reach USD 541.3 Million by 2033, growing at 9.6% CAGR, driven by increasing adoption of zonal architectures in EVs and SDVs.

Top Growth Drivers: EV adoption (48%), wiring reduction efficiency gains (35%), ADAS integration demand (42%).

Short-Term Forecast: By 2028, vehicle wiring harness complexity is expected to reduce by 30%, improving manufacturing efficiency.

Emerging Technologies: Automotive Ethernet, centralized computing platforms, AI-driven vehicle network management systems.

Regional Leaders: North America (~USD 180M by 2033) driven by EV innovation, Europe (~USD 150M) driven by regulatory electrification mandates, Asia-Pacific (~USD 160M) driven by high-volume vehicle production.

Consumer/End-User Trends: Over 55% of EV buyers prefer vehicles with advanced electronic architecture supporting OTA updates and connectivity features.

Pilot or Case Example: In 2024, a leading OEM reduced wiring weight by 25% using ZCU integration, improving energy efficiency by 12%.

Competitive Landscape: Market leader holds ~22% share, followed by major players including Bosch, Continental, Aptiv, ZF Friedrichshafen, and Denso.

Regulatory & ESG Impact: Emission reduction mandates are pushing OEMs to adopt lightweight electronic architectures, reducing vehicle weight by up to 15%.

Investment & Funding Patterns: Over USD 10 billion invested globally in automotive electronics platforms and SDV technologies in recent years.

Innovation & Future Outlook: Increasing integration of AI-based control systems and scalable zonal platforms will redefine vehicle electronics architecture.

Zone Control Units are increasingly integrated across passenger vehicles (approx. 60%), commercial vehicles (25%), and EV-specific platforms (15%), driven by rising electrification and ADAS demand. Innovations such as high-speed Ethernet communication and centralized compute modules are enhancing system efficiency. Regulatory mandates on emissions and energy efficiency are accelerating adoption, particularly in Europe and North America, while Asia-Pacific leads in volume deployment. The market is expected to witness strong momentum with scalable SDV architectures and OTA-enabled systems shaping future growth.

Zone Control Units (ZCUs) are becoming a cornerstone of next-generation automotive electronics as OEMs transition from distributed electronic control units (ECUs) to centralized and zonal architectures. Strategically, ZCUs enable automakers to reduce wiring harness length by up to 40%, resulting in lighter vehicles, improved fuel efficiency, and simplified assembly processes. Compared to traditional ECU-based systems, zonal architectures deliver nearly 30% improvement in system integration efficiency and up to 20% reduction in overall electronic system costs, positioning them as a critical enabler for software-defined vehicles (SDVs).

From a regional standpoint, Asia-Pacific dominates in production volume due to large-scale automotive manufacturing hubs, while North America leads in adoption, with over 58% of OEMs integrating zonal architectures into new EV platforms. Europe, meanwhile, is focusing on regulatory-driven innovation, with more than 65% of automotive R&D budgets allocated toward electrification and digital vehicle platforms. By 2028, AI-enabled vehicle network optimization is expected to improve real-time data processing efficiency by over 35%, enhancing safety and autonomous driving capabilities.

Sustainability and compliance are also shaping the strategic direction of the market. Automotive manufacturers are committing to reducing vehicle weight by 10–15% through advanced electronics and wiring reduction techniques by 2030, contributing to lower emissions and improved energy efficiency. In 2024, a major European automaker achieved a 28% reduction in wiring harness complexity by implementing zonal architecture in its EV lineup, demonstrating measurable operational benefits.

Looking ahead, the Zone Control Units for Automotive Electronics Market is poised to become a foundational pillar for resilient, scalable, and software-driven vehicle ecosystems. As integration with AI, edge computing, and OTA capabilities expands, ZCUs will play a pivotal role in ensuring compliance, operational efficiency, and sustainable growth across the global automotive industry.

The Zone Control Units for Automotive Electronics Market is undergoing significant transformation driven by the automotive industry’s shift toward centralized and software-defined architectures. Traditional vehicle systems relying on numerous distributed ECUs are being replaced with zonal systems that consolidate control functions, improving performance and reducing system complexity. The rise in electric vehicles, connected mobility solutions, and advanced driver-assistance systems (ADAS) is intensifying demand for efficient electronic architectures. Additionally, advancements in automotive Ethernet and high-speed data communication are enabling seamless integration of ZCUs across multiple vehicle domains. OEMs are focusing on reducing vehicle weight and improving energy efficiency, leading to increased deployment of ZCUs to minimize wiring harness requirements. Industry collaborations between semiconductor manufacturers and automotive OEMs are further accelerating innovation. However, integration complexity, high initial development costs, and cybersecurity concerns continue to influence adoption strategies across global markets.

The rapid adoption of software-defined vehicles (SDVs) is significantly driving the demand for Zone Control Units. Modern vehicles now incorporate over 100 electronic control units in traditional architectures, creating complexity in communication and wiring. ZCUs simplify this by reducing wiring length by up to 40% and enabling centralized processing. Over 65% of new EV platforms launched in 2025 are designed with zonal or domain-based architectures, highlighting strong adoption momentum. Additionally, ADAS integration has increased by nearly 50% in premium vehicles, requiring efficient data handling and low-latency communication systems, which ZCUs provide. Automotive Ethernet adoption has surged beyond 60% in next-generation vehicles, further supporting zonal systems. The demand for OTA updates and real-time vehicle diagnostics has also increased, with more than 55% of connected vehicles supporting such features, reinforcing the need for scalable ZCU-based architectures.

Despite strong growth potential, the Zone Control Units market faces challenges due to high integration complexity and reliance on advanced semiconductor components. ZCUs require sophisticated system design, combining multiple vehicle functions into a single architecture, increasing engineering complexity by nearly 30% compared to traditional systems. Additionally, the global semiconductor supply chain remains vulnerable, with automotive-grade chip shortages impacting over 20% of vehicle production schedules in recent years. The need for high-performance processors and reliable networking components further increases costs and limits scalability for mid-range vehicle segments. Cybersecurity risks also present a major concern, as centralized systems increase vulnerability points, requiring advanced security protocols. Furthermore, interoperability challenges between legacy ECUs and new zonal systems complicate transition processes, slowing adoption among traditional OEMs.

The rapid expansion of electric vehicles presents significant opportunities for Zone Control Units. EV platforms are inherently more compatible with centralized electronic architectures, enabling seamless integration of ZCUs. By 2025, electric vehicles account for over 18% of global vehicle sales, with projections indicating continued growth. ZCUs help reduce vehicle weight by up to 15%, directly enhancing battery efficiency and driving range, a key consideration for EV manufacturers. Additionally, EVs require advanced battery management systems and real-time monitoring capabilities, which are efficiently supported by zonal architectures. The increasing deployment of autonomous driving features, with over 40% of EVs equipped with Level 2 or higher autonomy, further drives demand for high-performance control systems. Emerging markets are also witnessing rapid EV adoption, creating new growth avenues for ZCU deployment.

Cybersecurity and lack of standardization remain critical challenges for the Zone Control Units market. Centralized architectures increase the risk of cyberattacks, with automotive cybersecurity incidents rising by over 35% in recent years. ZCUs handle multiple vehicle functions, making them a high-value target for malicious attacks, necessitating robust encryption and security frameworks. Additionally, the absence of universal standards for zonal architectures creates compatibility issues across different OEM platforms, leading to increased development time and costs. Integration of legacy systems further complicates standardization efforts, as older vehicles are not designed to support centralized architectures. The need for continuous software updates and maintenance adds operational complexity, requiring OEMs to invest heavily in cybersecurity infrastructure and software validation processes, which can slow overall market adoption.

Rapid Adoption of Automotive Ethernet Networking: Over 65% of next-generation vehicles are integrating automotive Ethernet systems, enabling high-speed data transmission exceeding 1 Gbps. This shift is supporting real-time communication across ZCUs, improving latency by nearly 30% and enhancing system responsiveness for ADAS and autonomous features.

Increasing Integration in Electric Vehicle Platforms: Nearly 58% of newly launched EV platforms in 2025 incorporate zonal architectures, with ZCUs reducing wiring harness weight by up to 25%. This contributes to an overall 10–12% improvement in vehicle energy efficiency and extended battery range.

Growth in Software-Defined Vehicle Architectures: More than 60% of automotive OEMs are transitioning toward SDV platforms, with centralized computing systems improving software update efficiency by 40%. ZCUs play a critical role in enabling OTA updates and real-time system diagnostics across connected vehicles.

Rising Demand for Lightweight and Energy-Efficient Systems: ZCU implementation is reducing vehicle weight by 10–15% by minimizing wiring complexity. Approximately 50% of manufacturers report improved manufacturing efficiency and reduced assembly time by integrating zonal systems into production lines.

The Zone Control Units for Automotive Electronics Market is segmented based on type, application, and end-user, reflecting diverse deployment strategies across modern vehicle architectures. By type, the market includes hardware-based ZCUs, software-integrated ZCUs, and hybrid systems combining both functionalities. Applications span across body control, powertrain management, infotainment systems, and advanced driver-assistance systems, with increasing integration across EV platforms. End-user segmentation primarily includes passenger vehicles, commercial vehicles, and electric vehicles, each exhibiting varying adoption rates based on technological readiness and cost considerations. Passenger vehicles dominate due to higher production volumes and faster integration of advanced electronics, while EVs are emerging as a key growth segment driven by the need for centralized control systems and energy-efficient architectures.

The Zone Control Units market by type is categorized into hardware-based ZCUs, software-integrated ZCUs, and hybrid ZCU systems. Hardware-based ZCUs currently lead the market, accounting for approximately 46% of total adoption, primarily due to their reliability and widespread use in existing vehicle platforms. These systems provide dedicated control functions and are easier to integrate into traditional architectures. In comparison, software-integrated ZCUs hold around 32% adoption, offering enhanced flexibility and scalability for software-defined vehicles. However, hybrid ZCU systems are witnessing the fastest growth, expected to expand at a CAGR of approximately 12.5%, as they combine the strengths of hardware stability and software adaptability. Other niche types, including modular ZCUs and AI-enabled controllers, collectively account for around 22% of the market, catering to advanced vehicle platforms and premium segments. These systems are increasingly used in autonomous and connected vehicles requiring high computational power and real-time data processing.

• In 2025, a major automotive technology consortium implemented hybrid ZCU systems in next-generation EV platforms, enabling centralized control across over 80 vehicle functions and reducing system latency by 28%.

The application segment includes body control systems, powertrain systems, infotainment systems, and ADAS applications. Body control systems dominate the segment, accounting for nearly 38% of total adoption, as ZCUs efficiently manage lighting, HVAC, and door control functions. Powertrain applications contribute approximately 27%, particularly in EVs where centralized control enhances energy efficiency. Infotainment systems account for around 18%, driven by increasing demand for connected and personalized user experiences. ADAS applications are the fastest-growing segment, expected to grow at a CAGR of approximately 13.2%, supported by rising demand for autonomous driving features and safety systems. These applications require high-speed data processing and real-time communication, making ZCUs essential. In 2025, over 52% of new vehicles globally were equipped with at least one ADAS feature, while 41% of consumers preferred vehicles with integrated digital cockpit systems. Additionally, more than 35% of automakers reported deploying centralized architectures for infotainment and connectivity platforms.

• In 2025, a global automotive safety initiative enabled deployment of AI-powered ADAS systems across more than 200 vehicle models, improving collision avoidance efficiency by 22%.

End-users of Zone Control Units include passenger vehicles, commercial vehicles, and electric vehicles (EVs). Passenger vehicles dominate the segment with approximately 57% share, driven by high production volumes and increasing integration of advanced electronics. Commercial vehicles account for around 23%, benefiting from fleet optimization and telematics integration. EVs hold approximately 20% share but represent the fastest-growing segment, expanding at a CAGR of approximately 14.1%, fueled by increasing electrification and demand for efficient energy management systems. Adoption trends indicate that over 60% of EV manufacturers are implementing zonal architectures to improve battery performance and reduce system complexity. In the passenger vehicle segment, nearly 50% of premium vehicles now feature ZCU-based architectures, enhancing connectivity and automation capabilities. Additionally, 45% of logistics companies are investing in connected vehicle technologies, integrating ZCUs for fleet monitoring and predictive maintenance. More than 38% of global automakers reported piloting ZCU-enabled platforms to enhance vehicle diagnostics and performance monitoring.

• In 2025, a leading EV manufacturer deployed zonal architectures across its entire vehicle lineup, achieving a 30% reduction in wiring complexity and improving overall system efficiency by 18%.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

North America’s dominance is supported by high adoption of software-defined vehicles, with over 58% of OEMs integrating zonal architectures into EV platforms. Europe holds approximately 28% share, driven by stringent emission regulations and electrification targets, with over 65% of automotive R&D budgets directed toward digital vehicle platforms. Asia-Pacific contributes around 30% of global demand, supported by large-scale automotive production exceeding 50 million vehicles annually across China, Japan, and India. South America and the Middle East & Africa collectively account for nearly 8%, with gradual adoption driven by infrastructure improvements and increasing vehicle electrification. Globally, more than 55% of new vehicle platforms introduced in 2025 incorporate some level of zonal or domain-based architecture, highlighting a strong shift toward centralized electronic systems.

North America holds approximately 34% share of the global Zone Control Units for Automotive Electronics Market, driven by strong demand from EV manufacturers, ADAS integration, and connected vehicle technologies. The region benefits from a robust automotive ecosystem, with over 70% of premium vehicle production incorporating advanced electronic architectures. Regulatory support such as fuel efficiency standards and EV incentives has accelerated the adoption of lightweight and efficient vehicle systems, reducing wiring harness weight by up to 25%. Technological advancements including automotive Ethernet adoption exceeding 65% are enhancing real-time data processing capabilities. A key regional player, Aptiv, is actively deploying scalable zonal architectures across next-generation EV platforms, improving system efficiency by over 20%. Consumer behavior shows higher preference for connected and autonomous features, with more than 60% of buyers prioritizing vehicles with OTA updates and smart cockpit systems.

Europe accounts for nearly 28% of the global market, with leading countries such as Germany, the UK, and France driving innovation. The region’s automotive industry is heavily influenced by regulatory bodies enforcing strict emission reduction targets, pushing manufacturers to adopt efficient electronic architectures. Over 75% of new vehicles in Western Europe are equipped with advanced driver-assistance systems, increasing reliance on ZCUs. Sustainability initiatives such as carbon neutrality goals by 2035 are encouraging the use of lightweight vehicle components, reducing total vehicle weight by up to 12%. Companies like Bosch are investing in centralized computing platforms, enhancing integration across multiple vehicle domains. Consumer behavior in Europe reflects strong regulatory influence, with over 58% of buyers preferring eco-efficient vehicles equipped with advanced electronics and connectivity features.

Asia-Pacific represents the fastest-growing region and accounts for approximately 30% of global market volume. Major automotive markets such as China, India, and Japan collectively produce over 50 million vehicles annually, creating substantial demand for advanced electronic architectures. China alone contributes over 32% of global EV production, with more than 60% of new EV models integrating zonal systems. Infrastructure expansion and strong semiconductor manufacturing capabilities are supporting rapid adoption. Technology hubs in Japan and South Korea are leading innovation in automotive networking systems, with automotive Ethernet deployment exceeding 55% in next-generation vehicles. A regional leader, Denso, is advancing integrated ZCU platforms for hybrid and electric vehicles, improving system responsiveness by 18%. Consumer behavior indicates rising demand for connected mobility, with over 65% of urban buyers preferring smart vehicle features.

South America holds approximately 5% share of the global Zone Control Units market, with Brazil and Argentina being the key contributors. The region’s automotive sector is gradually modernizing, with increasing investments in vehicle assembly plants and electrification initiatives. Over 30% of new vehicle models introduced in Brazil now feature enhanced electronic systems, supporting gradual adoption of zonal architectures. Government incentives for fuel efficiency and trade agreements are encouraging local production of advanced vehicle components. Infrastructure improvements and rising demand for connected vehicle technologies are further driving growth. Regional players are focusing on integrating telematics and fleet management systems, particularly in commercial vehicles. Consumer behavior in South America shows increasing demand for cost-efficient vehicles with digital features, with over 40% of buyers prioritizing connectivity and safety enhancements.

The Middle East & Africa region accounts for approximately 3% of the global market, with growth driven by countries such as the UAE and South Africa. Demand is influenced by increasing adoption of connected vehicles and infrastructure modernization projects. Over 25% of new vehicles in the UAE are equipped with advanced digital features, supporting integration of ZCUs. Government initiatives promoting smart mobility and digital transformation are encouraging adoption of advanced automotive technologies. Trade partnerships and investments in automotive assembly are improving access to advanced electronic systems. Regional players are focusing on integrating vehicle connectivity solutions and telematics platforms. Consumer behavior highlights growing interest in premium vehicles with advanced electronics, with over 45% of buyers in urban areas prioritizing smart and connected vehicle features.

United States – 28% Market share: Dominates due to high EV production capacity and strong investment in software-defined vehicle technologies.

China – 24% Market share: Leads in large-scale manufacturing and rapid adoption of zonal architectures across electric vehicle platforms.

The Zone Control Units for Automotive Electronics Market is moderately consolidated, with the top five companies accounting for approximately 55% of the total market share. The competitive landscape includes over 25 active global and regional players focusing on advanced automotive electronics, semiconductor integration, and vehicle networking systems. Key players are increasingly investing in research and development, with more than 60% of leading companies allocating significant budgets toward software-defined vehicle platforms and centralized computing technologies.

Strategic initiatives such as partnerships, mergers, and acquisitions are shaping competition. Over 40% of major automotive technology firms have entered collaborations with semiconductor companies to develop scalable zonal architectures. Product innovation is a key differentiator, with companies introducing high-performance ZCUs capable of managing over 100 vehicle functions simultaneously. Additionally, the integration of AI-based control systems and automotive Ethernet technologies is intensifying competition, as firms aim to deliver enhanced processing speed and system reliability.

The market is also witnessing increased competition from new entrants specializing in EV platforms and autonomous driving technologies. Approximately 35% of emerging companies are focusing on niche applications such as battery management and real-time vehicle diagnostics. Overall, the competitive environment is characterized by rapid technological advancements, strategic alliances, and increasing focus on scalable and energy-efficient vehicle architectures.

Continental AG

Denso Corporation

Aptiv PLC

ZF Friedrichshafen AG

Valeo SA

Magna International Inc.

NXP Semiconductors N.V.

Infineon Technologies AG

Texas Instruments Incorporated

Renesas Electronics Corporation

STMicroelectronics N.V.

Hyundai Mobis

Panasonic Automotive Systems

The Zone Control Units for Automotive Electronics Market is being shaped by rapid technological advancements aimed at enhancing vehicle performance, reducing system complexity, and enabling next-generation mobility solutions. One of the most significant innovations is the adoption of automotive Ethernet, with over 65% of new vehicle platforms integrating high-speed communication networks capable of supporting data transfer rates above 1 Gbps. This technology enables seamless communication between ZCUs and centralized computing systems, improving latency by up to 30%.

Another critical development is the transition toward centralized computing architectures, where multiple electronic functions are consolidated into fewer high-performance processing units. This approach reduces wiring harness length by up to 40% and improves energy efficiency by approximately 12%. Additionally, AI-driven control systems are being integrated into ZCUs, enabling predictive maintenance, real-time diagnostics, and enhanced decision-making capabilities in autonomous driving scenarios.

Semiconductor advancements are also playing a crucial role, with the use of advanced system-on-chip (SoC) solutions increasing processing efficiency by over 25%. These chips support multi-domain control, allowing ZCUs to manage functions such as infotainment, powertrain, and safety systems simultaneously. Furthermore, over-the-air (OTA) update capabilities are being widely adopted, with more than 55% of connected vehicles supporting remote software updates, reducing maintenance costs and improving user experience.

Cybersecurity technologies are evolving alongside these advancements, with encryption protocols and secure communication frameworks being implemented to protect centralized vehicle architectures. Overall, the integration of AI, high-speed networking, and advanced semiconductor technologies is driving innovation and positioning ZCUs as a core component of future automotive ecosystems.

• In June 2024, Bosch announced at its Tech Day the development of a vehicle-centric, zone-oriented E/E architecturebuilt around high-performance cross-domain computers integrating cockpit and ADAS functions on a single platform, reducing cabling and enabling scalable zonal systems for next-generation vehicles. Source: www.bosch-presse.de

• In 2024, Bosch showcased its central vehicle computer with a single system-on-chip (SoC)capable of combining infotainment and driver assistance functions, reducing the number of ECUs and lowering hardware complexity in software-defined vehicles.

• In September 2025, Bosch highlighted at IAA Mobility its Vehicle Motion Management software platform, already adopted by over two dozen OEMs globally, enabling centralized control across braking, steering, and powertrain systems, supporting zonal architectures and improving system coordination.

• In 2025, Bosch confirmed continued development of zone-oriented E/E architectures, where a reduced number of powerful vehicle computers connect to sensors and actuators via zone ECUs, achieving up to 20% reduction in control units and approximately 10% lower system costs.

The Zone Control Units for Automotive Electronics Market Report provides a comprehensive analysis of the evolving automotive electronics landscape, focusing on the transition from traditional ECU-based systems to advanced zonal architectures. The report covers key segments including hardware-based, software-integrated, and hybrid ZCU systems, offering insights into their adoption across various vehicle platforms. Applications analyzed in the report include body control systems, powertrain management, infotainment systems, and advanced driver-assistance systems, with detailed insights into their functional integration and performance benefits.

Geographically, the report examines major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional production trends, adoption rates, and technological advancements. The study also explores end-user segments such as passenger vehicles, commercial vehicles, and electric vehicles, providing insights into their respective adoption patterns and technological requirements.

Additionally, the report covers key technological developments such as automotive Ethernet, centralized computing architectures, AI-driven control systems, and semiconductor innovations. It evaluates industry trends including software-defined vehicles, OTA updates, and cybersecurity measures. The scope further includes competitive analysis, highlighting strategic initiatives such as partnerships, product launches, and innovation pipelines.

Emerging areas such as autonomous driving integration, battery management optimization, and connected mobility platforms are also examined, offering forward-looking insights into future market evolution. The report serves as a strategic resource for stakeholders, enabling informed decision-making by providing a detailed understanding of market structure, technological progress, and industry dynamics.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 260.0 Million |

| Market Revenue (2033) | USD 541.3 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Robert Bosch GmbH; Continental AG; Denso Corporation; Aptiv PLC; ZF Friedrichshafen AG; Valeo SA; Magna International Inc.; NXP Semiconductors N.V.; Infineon Technologies AG; Texas Instruments Incorporated; Renesas Electronics Corporation; STMicroelectronics N.V.; Hyundai Mobis; Panasonic Automotive Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |