Reports

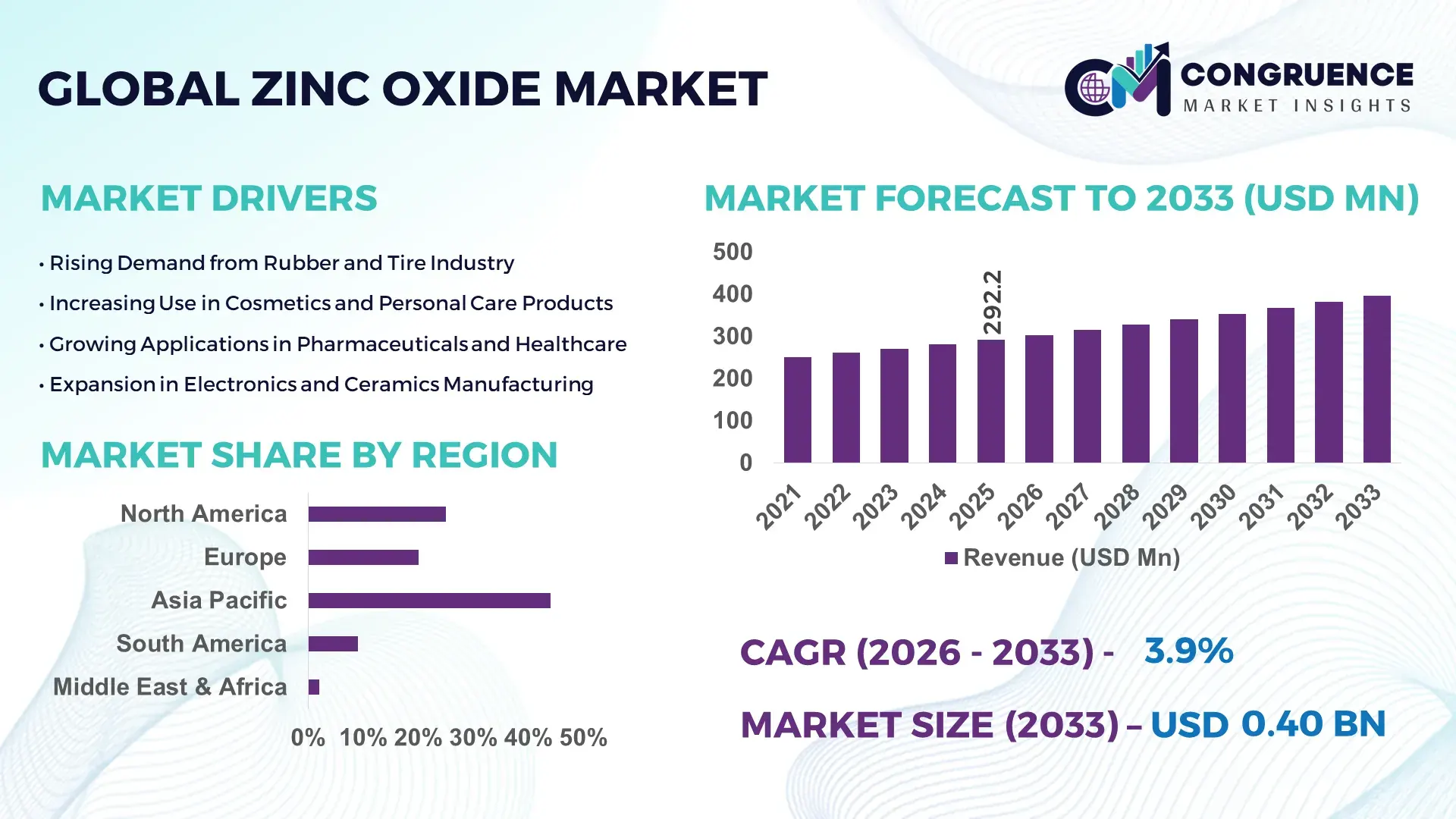

The Global Zinc Oxide Market was valued at USD 292.16 Million in 2025 and is anticipated to reach a value of USD 396.48 Million by 2033 expanding at a CAGR of 3.89% between 2026 and 2033. The growth is primarily driven by rising demand from the rubber, cosmetics, and pharmaceutical industries due to zinc oxide’s multifunctional properties such as UV protection, antibacterial performance, and chemical stability.

China continues to dominate the global zinc oxide market with an annual production capacity exceeding 1.2 million metric tons, supported by strong investments in advanced smelting technologies and integrated supply chains. The country accounts for over 45% of global zinc consumption across industries such as tire manufacturing, ceramics, and electronics. Chinese manufacturers are increasingly adopting high-purity nano zinc oxide production techniques, improving efficiency by nearly 20% in industrial coatings and rubber vulcanization processes. Additionally, over 60% of domestic tire manufacturers utilize zinc oxide in rubber formulations, reinforcing its industrial significance and technological integration.

Zinc oxide plays a critical role across multiple industries, with the rubber sector contributing approximately 50% of total demand, followed by ceramics at around 15% and personal care products at nearly 10%. Technological advancements such as nano-sized zinc oxide particles have enhanced UV-blocking efficiency by up to 30%, making them increasingly popular in sunscreens and coatings. Regulatory frameworks promoting eco-friendly materials are encouraging manufacturers to adopt low-carbon production techniques, particularly in Europe and North America. Meanwhile, Asia-Pacific continues to lead consumption due to expanding industrial output and infrastructure development, while emerging applications in electronics and biomedical sectors are shaping future growth trajectories.

The zinc oxide market holds strategic relevance due to its critical role in enhancing product performance across key industries such as automotive, healthcare, construction, and electronics. With over 50% of zinc oxide consumption attributed to rubber manufacturing, particularly in tire production, its importance in global supply chains remains significant. Advanced nano zinc oxide technology delivers up to 30% higher UV absorption efficiency compared to conventional zinc oxide, making it a preferred material in high-performance coatings and skincare formulations.

Asia-Pacific dominates in production volume, while North America leads in technological adoption with over 65% of manufacturers integrating advanced zinc oxide formulations into specialty applications. By 2028, smart material integration and nanotechnology-driven processing are expected to improve product efficiency by nearly 18%, particularly in coatings and electronics.

From a sustainability perspective, firms are committing to ESG targets such as reducing carbon emissions by 25% and increasing recycling rates of zinc-based materials by 20% by 2030. In 2024, a leading chemical manufacturer in Germany achieved a 17% reduction in energy consumption through the adoption of energy-efficient zinc oxide production processes. The future pathways of the zinc oxide market are increasingly aligned with innovation in green chemistry, advanced material science, and circular economy models. With continuous improvements in performance, sustainability, and regulatory compliance, the zinc oxide market is positioned as a critical pillar supporting resilient industrial ecosystems and long-term sustainable growth.

The rubber industry remains the largest consumer of zinc oxide, accounting for nearly half of total global demand. Zinc oxide plays a critical role in the vulcanization process, improving elasticity, durability, and heat resistance of rubber products. With global tire production exceeding 2 billion units annually, the demand for high-performance rubber compounds continues to rise. Zinc oxide enhances curing efficiency by up to 25%, reducing production time and improving product quality. The growth of the automotive sector, particularly in emerging economies, is further driving the need for durable tires and industrial rubber products. Additionally, the increasing adoption of electric vehicles is boosting demand for specialized tires, further strengthening zinc oxide consumption in advanced rubber formulations.

Environmental concerns related to zinc emissions and waste disposal are posing significant challenges to the zinc oxide market. Regulatory authorities in regions such as Europe and North America have imposed strict limits on zinc discharge levels due to its potential impact on aquatic ecosystems. Studies indicate that excessive zinc concentrations can disrupt marine biodiversity, leading to tighter compliance requirements for manufacturers. As a result, companies are required to invest in advanced filtration and waste management systems, increasing operational costs by approximately 15–20%. Furthermore, the shift toward alternative materials and eco-friendly substitutes in certain applications is limiting market expansion. These regulatory pressures are compelling manufacturers to adopt sustainable production processes while maintaining product performance standards.

Nanotechnology is unlocking significant growth opportunities in the zinc oxide market by enhancing material properties and expanding application areas. Nano zinc oxide offers superior UV-blocking capabilities, with up to 30% higher efficiency compared to conventional forms, making it highly desirable in sunscreens, coatings, and textiles. In the electronics sector, nano zinc oxide is being used in sensors, semiconductors, and optoelectronic devices due to its high electron mobility and conductivity. The global demand for advanced materials in wearable electronics and smart devices is further driving innovation. Additionally, biomedical applications such as antibacterial coatings and drug delivery systems are gaining traction, with research indicating a 20% improvement in antimicrobial performance. These advancements are positioning nanotechnology as a key enabler of future market growth.

Fluctuating raw material prices, particularly zinc metal, present a major challenge for the zinc oxide market. Zinc prices are influenced by global mining output, geopolitical factors, and supply chain disruptions, leading to price volatility of up to 25% in certain periods. This volatility directly impacts production costs for zinc oxide manufacturers, making it difficult to maintain stable pricing strategies. Additionally, energy-intensive production processes further amplify cost pressures, especially in regions with high electricity tariffs. Small and medium-sized manufacturers are particularly vulnerable, as they often lack the financial capacity to absorb cost fluctuations. These challenges necessitate strategic sourcing, long-term supply agreements, and investment in energy-efficient technologies to ensure operational stability and competitiveness.

• Nano Zinc Oxide Adoption Surges by 30% in High-Performance Applications:

The adoption of nano zinc oxide has increased by over 30% across industries such as cosmetics, coatings, and electronics due to its enhanced UV-blocking and antimicrobial properties. Particle sizes below 100 nm improve transparency by nearly 25%, making it ideal for premium sunscreen formulations where over 70% of new product launches now incorporate nano-based materials. In coatings, nano zinc oxide enhances corrosion resistance by approximately 20%, particularly in marine and industrial environments, while in electronics, its superior conductivity is supporting growth in sensors and optoelectronic devices.

• Rubber Industry Utilization Exceeds 50% of Total Zinc Oxide Demand:

The rubber industry continues to dominate zinc oxide consumption, accounting for more than 50% of total global demand. Over 2 billion tires are produced annually worldwide, with zinc oxide improving vulcanization efficiency by nearly 25% and extending product lifespan by up to 15%. Demand for high-performance tires, especially in electric vehicles, has increased zinc oxide usage per tire by approximately 8–10%. Industrial rubber applications such as conveyor belts and seals also contribute significantly, with usage growing by nearly 12% in heavy manufacturing sectors.

• Sustainable Production Methods Reduce Emissions by 25%:

Sustainability-focused innovations are transforming zinc oxide production, with green synthesis techniques reducing carbon emissions by up to 25% in pilot and commercial-scale facilities. Around 40% of manufacturers are transitioning to energy-efficient kiln technologies and low-temperature processing methods. Recycling-based zinc recovery processes have improved material recovery rates by nearly 20%, reducing dependency on primary zinc extraction. In Europe, over 60% of zinc oxide producers have adopted environmentally compliant production systems aligned with strict emission regulations, driving industry-wide sustainability adoption.

• Digitalization and Automation Improve Manufacturing Efficiency by 35%:

The integration of automation and AI-driven quality control systems has improved production efficiency by more than 35% across leading zinc oxide manufacturing plants. Smart sensors and predictive maintenance technologies have reduced equipment downtime by approximately 18%, ensuring consistent output quality. Automated process control systems are enabling real-time monitoring of particle size and purity, achieving precision levels above 99.5% in high-grade zinc oxide production. Digital transformation initiatives are particularly prominent in North America and Asia-Pacific, where over 50% of large-scale facilities have implemented advanced manufacturing technologies.

The zinc oxide market is segmented based on type, application, and end-user industries, each contributing distinctively to overall demand dynamics. By type, standard zinc oxide continues to dominate due to its widespread industrial use, while nano and surface-treated variants are gaining traction in specialized applications. In terms of application, the rubber industry remains the largest segment, supported by tire manufacturing and industrial rubber goods, followed by ceramics, chemicals, and pharmaceuticals. End-user segmentation highlights automotive, healthcare, construction, and electronics sectors as primary contributors, with automotive alone accounting for a substantial portion of demand. Increasing diversification into advanced materials and electronics is reshaping segmentation trends, with emerging applications contributing nearly 15% of incremental demand.

The zinc oxide market by type includes standard zinc oxide, nano zinc oxide, and surface-treated zinc oxide, each catering to specific industrial requirements. Standard zinc oxide holds the leading position, accounting for approximately 65% of total market share due to its extensive use in rubber processing, ceramics, and general industrial applications. Its cost-effectiveness and consistent performance make it the preferred choice in high-volume manufacturing sectors.

Nano zinc oxide represents around 20% of the market but is the fastest-growing segment, expanding at an estimated CAGR of 6.2%, driven by increasing demand in cosmetics, electronics, and advanced coatings. Compared to standard zinc oxide at 65% and surface-treated variants at 15%, nano zinc oxide adoption is accelerating due to its superior UV absorption and antimicrobial efficiency, which improves product performance by up to 30%. Surface-treated zinc oxide accounts for approximately 15% of the market, primarily used in specialized applications requiring enhanced dispersion and compatibility with polymers and coatings. These variants improve material durability by nearly 20% in high-performance environments.

The application segmentation of the zinc oxide market is led by the rubber industry, which accounts for approximately 50% of total usage due to its critical role in vulcanization processes. Zinc oxide enhances elasticity, heat resistance, and durability, improving tire performance by nearly 15%. Ceramics and chemicals follow with a combined share of around 25%, where zinc oxide is used for glazing, pigmentation, and chemical synthesis.

Pharmaceutical and personal care applications collectively contribute approximately 15%, with increasing demand for dermatological products and UV-protective formulations. Compared to rubber at 50% and ceramics/chemicals at 25%, the personal care segment is the fastest-growing, expanding at an estimated CAGR of 5.8%, supported by rising consumer awareness of skin protection and increasing use of mineral-based ingredients in cosmetics. Other applications, including electronics and coatings, account for the remaining 10%, with growth driven by advancements in semiconductors and corrosion-resistant materials.

The zinc oxide market by end-user is dominated by the automotive sector, which accounts for approximately 45% of total demand, primarily due to its reliance on rubber components such as tires, seals, and hoses. The sector benefits from zinc oxide’s ability to improve durability and performance, particularly in high-stress applications. Construction and infrastructure industries follow with around 20% share, driven by demand for coatings and corrosion-resistant materials.

Healthcare and pharmaceuticals represent approximately 15% of the market, while electronics and consumer goods contribute another 10%. Compared to automotive at 45% and construction at 20%, healthcare is the fastest-growing segment, expanding at an estimated CAGR of 6.0%, supported by increasing demand for dermatological treatments and antibacterial products. Other end-users, including agriculture and energy sectors, account for the remaining 10%, with adoption rates increasing by nearly 12% in specialized applications such as fertilizers and energy storage systems.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by an annual consumption exceeding 1.5 million metric tons, driven by large-scale rubber and tire manufacturing across China, India, and Japan. China alone contributes over 55% of regional production, while India accounts for nearly 18% of regional demand due to expanding automotive and infrastructure sectors. North America holds approximately 22% of the global zinc oxide market, with increasing demand from pharmaceuticals and advanced coatings. Europe represents around 20% share, supported by stringent environmental regulations and sustainable production initiatives. South America and the Middle East & Africa collectively contribute close to 10%, with Brazil and the UAE emerging as key consumption hubs. Regional demand is further influenced by industrial output growth, technological adoption, and regulatory compliance across manufacturing sectors.

How is advanced material innovation shaping industrial demand patterns?

North America accounts for approximately 22% of the global zinc oxide market, with demand primarily driven by the automotive, pharmaceutical, and personal care industries. The region consumes over 400,000 metric tons annually, with the United States contributing nearly 75% of total regional demand. Regulatory frameworks such as stringent environmental compliance standards from agencies like the EPA are pushing manufacturers toward sustainable production processes, reducing emissions by up to 18%. Technological advancements include the integration of nano zinc oxide in high-performance coatings and medical formulations, improving UV protection efficiency by nearly 30%. A key player, U.S. Zinc, has expanded its production capacity by over 12% through advanced refining technologies. Consumer behavior reflects higher adoption in healthcare and premium skincare segments, with over 65% of sunscreen products incorporating zinc oxide-based formulations.

Why are sustainability-driven regulations transforming industrial material adoption?

Europe holds nearly 20% of the global zinc oxide market, with key markets including Germany, the UK, and France contributing over 60% of regional consumption. The region processes approximately 350,000 metric tons annually, largely driven by automotive, ceramics, and cosmetics industries. Regulatory bodies such as the European Chemicals Agency (ECHA) enforce strict environmental standards, encouraging the adoption of eco-friendly zinc oxide production methods that reduce carbon emissions by up to 25%. Emerging technologies such as surface-treated zinc oxide are gaining traction, enhancing product performance in coatings and rubber applications. A prominent regional player, EverZinc, has invested in sustainable production facilities, improving energy efficiency by nearly 15%. Consumer behavior is heavily influenced by regulatory compliance, with increasing demand for environmentally safe and transparent material formulations.

What factors are accelerating industrial-scale production and consumption trends?

Asia-Pacific leads the global zinc oxide market in both volume and consumption, exceeding 1.5 million metric tons annually. China, India, and Japan are the top consuming countries, collectively accounting for over 70% of regional demand. China alone produces more than 1.2 million metric tons annually, supported by strong manufacturing infrastructure and export-oriented industries. Rapid industrialization, expanding automotive production exceeding 30 million vehicles annually, and infrastructure development are key growth drivers. Technological innovation hubs in China and Japan are advancing nano zinc oxide applications, improving efficiency in electronics and coatings by up to 25%. A leading regional manufacturer, Zochem (Asia operations), has enhanced production output by 20% through automation. Consumer behavior reflects strong demand from manufacturing and e-commerce-driven personal care sectors, particularly in emerging economies.

How are industrial expansion and trade policies influencing material demand?

South America accounts for approximately 6% of the global zinc oxide market, with Brazil and Argentina representing over 70% of regional consumption. The region consumes nearly 120,000 metric tons annually, driven by growth in automotive, construction, and agriculture sectors. Infrastructure development projects have increased demand for coatings and rubber products by approximately 14% in recent years. Government incentives promoting industrial manufacturing and favorable trade policies have improved import-export dynamics for zinc-based materials. A regional player in Brazil has expanded its processing capacity by 10% to meet rising domestic demand. Consumer behavior is influenced by localized industrial needs, with demand closely tied to construction activities and agricultural equipment manufacturing.

What role do industrial diversification and infrastructure investments play in demand growth?

The Middle East & Africa region contributes around 4% of the global zinc oxide market, with key growth countries including the UAE and South Africa. Regional demand is estimated at over 80,000 metric tons annually, largely driven by construction, oil & gas, and coatings industries. Infrastructure investments exceeding USD 500 billion across Gulf countries are boosting demand for corrosion-resistant materials such as zinc oxide. Technological modernization in manufacturing processes is improving production efficiency by nearly 12%. Trade partnerships and regulatory reforms are facilitating easier import of raw materials and finished products. A regional manufacturer in South Africa has increased output capacity by 8% to support industrial demand. Consumer behavior is characterized by a preference for durable materials in construction and industrial applications.

China – 38% Zinc Oxide market share: Dominance driven by large-scale production capacity exceeding 1.2 million metric tons and strong demand from rubber and manufacturing industries.

United States – 18% Zinc Oxide market share: Growth supported by advanced applications in pharmaceuticals, coatings, and high-performance materials across multiple industries.

The zinc oxide market exhibits a moderately fragmented competitive structure with over 60 active global and regional manufacturers competing across industrial and specialty segments. The top five companies collectively account for approximately 45% of the total market share, indicating a balanced mix of consolidation and competitive diversity. Leading players are focusing on capacity expansion, technological innovation, and strategic partnerships to strengthen their market positions. For instance, several manufacturers have increased production capacities by 10–20% through investments in automated and energy-efficient facilities. Product differentiation is increasingly driven by advancements in nano zinc oxide, which offers up to 30% improved performance in UV protection and antimicrobial applications.

Mergers and acquisitions have also gained momentum, with companies targeting regional expansion and vertical integration to secure raw material supply chains. Additionally, firms are investing in sustainable production technologies to comply with environmental regulations, reducing emissions by up to 25%. Innovation trends such as surface modification and high-purity zinc oxide formulations are further intensifying competition. The market is also witnessing increased R&D spending, with leading players allocating nearly 5–7% of their operational budgets toward product development and process optimization. These strategic initiatives are shaping a dynamic and innovation-driven competitive landscape.

U.S. Zinc

EverZinc

Zochem Inc.

Rubamin Ltd.

Pan-Continental Chemical Co., Ltd.

Sakai Chemical Industry Co., Ltd.

Silox SA

Weifang Longda Zinc Industry Co., Ltd.

Upper India Smelting & Refinery Works

American Chemet Corporation

Technological advancements in the zinc oxide market are increasingly centered on improving material efficiency, purity levels, and application-specific performance. One of the most significant developments is the rise of nano zinc oxide, which offers particle sizes below 100 nanometers and enhances UV absorption efficiency by up to 30% compared to conventional zinc oxide. This technology is widely adopted in high-performance coatings, sunscreens, and advanced electronics due to its superior optical transparency and antimicrobial properties. The indirect (French) process remains the dominant production method, accounting for over 70% of global output, delivering purity levels above 99.5%. However, direct (American) process technologies are gaining traction in cost-sensitive markets, especially in developing regions, where production costs can be reduced by nearly 15%. Emerging hybrid processes are combining both methods to optimize energy consumption and output quality.

Surface modification technologies, including coated and doped zinc oxide particles, are enabling improved dispersion and compatibility in rubber and polymer matrices, enhancing durability by approximately 20%. In addition, advancements in green synthesis methods using low-temperature chemical precipitation and bio-based reducing agents are reducing environmental impact, with emissions lowered by up to 25% in pilot-scale facilities. Digital transformation is also influencing production, with automation and AI-driven quality control systems improving defect detection rates by over 35%. Furthermore, zinc oxide is increasingly being integrated into semiconductor and optoelectronic applications, where its high electron mobility supports efficient energy transfer. These technological innovations are positioning zinc oxide as a critical material in next-generation industrial and consumer applications.

• In March 2025, EverZinc announced the expansion of its European production facility to enhance capacity for specialty zinc oxides used in rubber and battery applications. The project focuses on improving energy efficiency and reducing emissions through advanced kiln technologies. Source: www.everzinc.com

• In September 2024, Zochem Inc. upgraded its North American manufacturing operations with automated process control systems, increasing production efficiency and reducing energy consumption. The initiative also improved product consistency for high-purity zinc oxide used in pharmaceutical and cosmetic applications. Source: www.zochem.com

• In May 2025, U.S. Zinc introduced a new line of ultra-fine zinc oxide products designed for high-performance coatings and electronics. The innovation enhances UV resistance and conductivity, supporting advanced industrial and consumer applications. Source: www.uszinc.com

• In November 2024, Rubamin Ltd. expanded its sustainable zinc recycling operations in India, increasing the recovery rate of zinc materials by over 20%. The initiative supports circular economy practices and reduces dependency on primary zinc extraction. Source: www.rubamin.com

The zinc oxide market report provides a comprehensive analysis of key industry segments, applications, and regional dynamics shaping global demand. The scope includes detailed segmentation by application, where the rubber industry accounts for approximately 50% of total consumption, followed by ceramics at around 15%, chemicals at 12%, pharmaceuticals at 10%, and other applications such as electronics and coatings contributing the remaining share. The report also examines product types, including standard zinc oxide, nano zinc oxide, and surface-treated variants, highlighting their respective industrial applications and performance characteristics.

Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with Asia-Pacific leading in production volume exceeding 1.5 million metric tons annually. The study further analyzes country-level insights for key markets such as China, the United States, Germany, India, and Japan, focusing on industrial output, consumption patterns, and regulatory frameworks.

Technological coverage includes traditional manufacturing processes such as the indirect and direct methods, along with emerging innovations in nanotechnology, green synthesis, and digitalized production systems. The report also explores niche segments such as zinc oxide in biomedical applications, semiconductor devices, and energy storage systems.

Additionally, the scope incorporates analysis of supply chain dynamics, including raw material sourcing, production capacity distribution, and end-user demand trends. It evaluates industry-specific drivers such as automotive production exceeding 90 million units globally and increasing demand for UV-resistant materials in personal care products. The report is designed to provide actionable insights for stakeholders, enabling strategic decision-making across manufacturing, investment, and product development domains.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.89% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

U.S. Zinc, EverZinc, Zochem Inc., Rubamin Ltd., Pan-Continental Chemical Co., Ltd., Sakai Chemical Industry Co., Ltd., Silox SA, Weifang Longda Zinc Industry Co., Ltd., Upper India Smelting & Refinery Works, American Chemet Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |