Reports

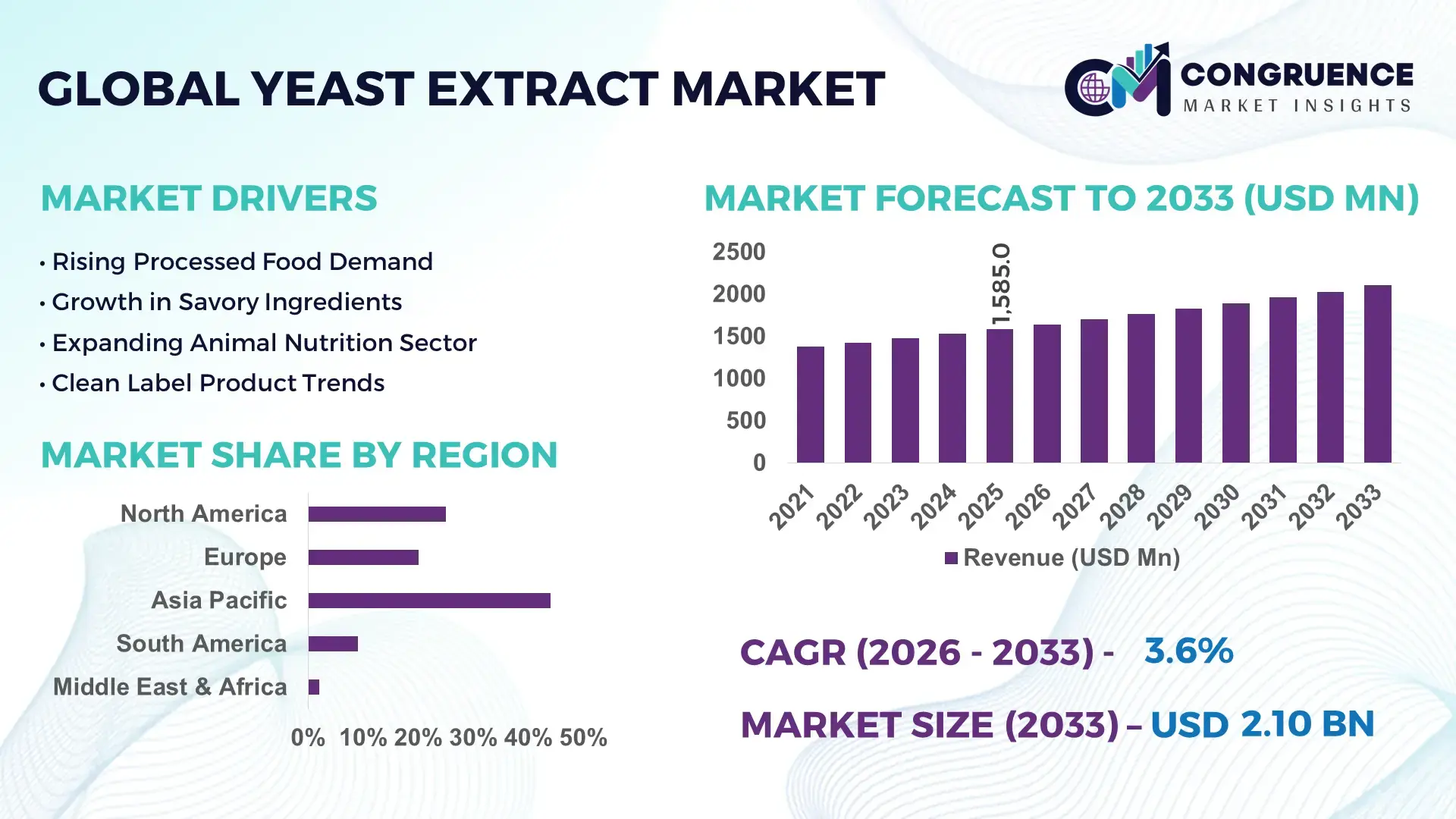

The Global Yeast Extract Market was valued at USD 1585 Million in 2025 and is anticipated to reach a value of USD 2103.32 Million by 2033 expanding at a CAGR of 3.6% between 2026 and 2033.

Rising adoption of clean-label savory ingredients in processed foods, plant-based protein formulations, and functional nutrition products is accelerating yeast extract utilization, with automated fermentation technologies improving production efficiency by nearly 18% compared to conventional extraction systems. Between 2024 and 2026, global food manufacturers shifted ingredient sourcing strategies due to Red Sea shipping disruptions and tightening sodium-reduction regulations across Europe and North America, increasing localized yeast extract processing investments and contract manufacturing activity.

China dominates the global yeast extract market with an estimated 31% production share, supported by large-scale fermentation infrastructure, expanding food processing exports, and over USD 450 million in ingredient manufacturing upgrades between 2024 and 2026. The country’s processed food sector increased yeast-derived flavor enhancer integration by nearly 22%, particularly across instant noodles, ready meals, and plant-based meat applications. Compared with smaller Southeast Asian producers, Chinese manufacturers operate at approximately 15–20% lower processing costs due to integrated molasses supply chains and high-capacity fermentation systems exceeding 12,000 tons annually in leading facilities.

The market increasingly rewards vertically integrated producers capable of balancing cost-efficient fermentation capacity, regulatory compliance, and customized flavor development for high-growth food and nutrition applications.

Market Size & Growth: USD 1585 million in 2025 is projected to reach USD 2103.32 million by 2033, supported by clean-label food reformulation and high-efficiency fermentation expansion.

Top Growth Drivers: Processed food demand contributes 34% growth momentum, plant-based nutrition adoption adds 27%, and sodium-reduction reformulations account for 21% market acceleration.

Short-Term Forecast: By 2027, automated fermentation systems are expected to reduce production downtime by 16% while improving extraction yield efficiency by 13%.

Emerging Technologies: AI-based fermentation monitoring, precision nutrient dosing, and advanced enzymatic extraction technologies improve flavor consistency by over 19%.

Regional Leaders: Asia-Pacific exceeds USD 860 million with rapid convenience food adoption, Europe surpasses USD 520 million through clean-label demand, and North America crosses USD 410 million driven by protein innovation.

Consumer/End-User Trends: More than 48% of processed food manufacturers increased yeast extract usage in low-sodium and plant-based formulations during 2025–2026.

Pilot/Case Example: In 2025, a large-scale Asian fermentation upgrade improved batch productivity by 17% and reduced energy consumption by 11% amid supply chain localization efforts.

Competitive Landscape: The top five companies collectively control nearly 44% market share, with major competition centered on customized flavor systems and scalable fermentation capacity.

Regulatory & ESG Impact: European sodium-reduction initiatives accelerated demand for natural flavor enhancers, while energy-efficient fermentation systems lowered operational emissions by approximately 14%.

Investment & Funding: More than USD 700 million in global expansion investments supported new fermentation plants, regional partnerships, and ingredient innovation programs between 2024 and 2026.

Innovation & Future Outlook: Next-generation yeast strains, bio-based nutrient recovery, and precision fermentation platforms are strengthening high-margin specialty ingredient strategies worldwide.

Yeast extract demand remains heavily concentrated in processed foods, functional nutrition, and animal feed applications, contributing approximately 52%, 21%, and 14% of total industry consumption respectively. Recent innovations include precision fermentation systems and low-sodium flavor enhancement solutions that improve extraction efficiency by nearly 18%. Asia-Pacific continues leading volume demand, while Europe records faster adoption of clean-label savory formulations following stricter food ingredient regulations. Supply chain regionalization and localized ingredient manufacturing are reshaping procurement strategies, while advanced bio-fermentation capabilities are positioning specialized producers for stronger long-term competitive expansion.

The yeast extract market is rapidly transforming into a strategic ingredient ecosystem driven by clean-label reformulation, sodium reduction targets, and precision fermentation investments. Global food manufacturers are accelerating integration of yeast-derived flavor systems as processed food optimization and plant-based protein expansion intensify competitive pressure across packaged nutrition categories. Between 2024 and 2026, ingredient sourcing diversification and tighter European food additive regulations forced companies to regionalize fermentation operations and secure localized molasses supply chains. Precision fermentation technology improves production efficiency by 24% while reducing operating costs by 16% compared to legacy batch extraction systems, strengthening scalability and flavor consistency.

Asia-Pacific leads in production volume with nearly 46% global capacity share, while Europe leads in clean-label adoption and advanced ingredient innovation with more than 39% of food manufacturers reformulating low-sodium products using yeast-based enhancers. Over the next three years, automated fermentation facilities are projected to reduce energy intensity by 14% and improve extraction yield performance by 18%. ESG-focused manufacturing is becoming a direct competitive advantage, with water recovery systems lowering processing waste by 12% while improving compliance access across export-driven markets.

In 2025, a multinational ingredient producer upgraded its fermentation analytics platform, improving batch consistency by 21% and shortening production cycles by 11%. Major companies are shifting capital allocation toward specialty savory ingredients, regional expansion, and bio-based fermentation optimization to secure long-term pricing power and supply resilience. The competitive landscape is increasingly favoring vertically integrated producers capable of optimizing technology, sustainability, and customized formulation capabilities simultaneously.

Food manufacturers are aggressively increasing yeast extract utilization as sodium-reduction mandates and clean-label reformulations reshape processed food production worldwide. More than 48% of packaged food companies expanded natural flavor enhancer integration during 2025, while low-sodium product launches increased by 26% across Europe and North America. Red Sea shipping disruptions and ingredient supply concentration in Asia accelerated regional fermentation investments and localized sourcing strategies. This structural shift is forcing manufacturers to replace synthetic additives with yeast-derived savory systems that improve flavor retention by nearly 18% in reformulated products. Companies are responding through fermentation capacity expansion, strategic molasses procurement agreements, and automation investments that reduce batch variability by 15%, strengthening supply security and accelerating premium ingredient differentiation in competitive food manufacturing ecosystems.

The yeast extract market faces significant operational pressure from molasses price volatility, concentrated fermentation infrastructure, and tightening environmental compliance costs. Global sugar byproduct price fluctuations exceeded 19% during 2025, directly increasing fermentation input expenses and compressing processor margins. Nearly 41% of production capacity remains concentrated in Asia, creating supply chain vulnerability during shipping disruptions and regional energy shortages. Regulatory pressure surrounding industrial wastewater discharge is further constraining scalability, with treatment compliance costs increasing by approximately 13% across major export markets. These limitations are forcing manufacturers to diversify feedstock sourcing, negotiate long-term procurement contracts, and invest in energy-efficient extraction systems. Companies are also accelerating adoption of alternative nutrient recovery technologies to reduce dependency on volatile agricultural inputs and stabilize long-term production economics.

Precision fermentation and functional nutrition expansion are unlocking high-margin opportunities across the global yeast extract ecosystem. Demand for protein-enriched and immunity-support food formulations increased by 28% during 2025, while plant-based savory ingredient integration rose by 24% in premium food applications. Advanced strain engineering technologies now improve extraction efficiency by nearly 22% while reducing nutrient loss compared to conventional fermentation processes. A major future signal is the accelerating convergence between bio-based flavor systems and personalized nutrition manufacturing. Companies are positioning for long-term dominance through R&D investment, regional application laboratories, and partnerships with alternative protein manufacturers. Emerging markets in Southeast Asia and Latin America are also creating new demand pockets as processed food penetration and packaged nutrition consumption continue expanding rapidly across urban populations.

Scaling advanced yeast extract production remains challenging due to infrastructure intensity, regulatory fragmentation, and rising sustainability expectations across export markets. Industrial energy costs for fermentation operations increased by nearly 17% between 2024 and 2026, while cross-border compliance requirements expanded testing and certification timelines by approximately 14%. Many mid-sized producers continue facing limited access to automated fermentation systems, reducing operational consistency and constraining global competitiveness. Water-intensive extraction processes are also attracting stricter environmental scrutiny, particularly across Europe and developed Asian economies. These pressures are impacting long-term supply reliability and margin stability. To remain competitive, companies must accelerate investment in closed-loop processing systems, AI-driven fermentation monitoring, and strategic partnerships that strengthen regional manufacturing resilience while ensuring compliance with evolving global food ingredient standards.

More Than 42% of Food Manufacturers Are Reformulating Low-Sodium Products Using Yeast Extract Systems. Food processors are rapidly replacing synthetic flavor enhancers with yeast-derived alternatives to meet tightening sodium regulations and clean-label standards. Reformulated packaged foods increased by 26% across Europe during 2025, while fermentation-based flavor systems reduced additive dependency by nearly 18%. Companies are restructuring procurement models and expanding regional ingredient blending facilities to stabilize supply consistency amid shipping disruptions and rising compliance pressure.

Automated Fermentation Deployment Has Increased by 31%, Reshaping Production Efficiency Standards. Advanced sensor-driven fermentation monitoring and AI-assisted nutrient optimization are reducing batch inconsistency by 21% while lowering processing downtime by 14%. Large manufacturers are integrating closed-loop extraction systems to reduce water usage and energy intensity simultaneously. A non-obvious shift is emerging as mid-sized producers increasingly partner with contract fermentation operators instead of investing directly in large-scale infrastructure, accelerating market consolidation and operational specialization.

Asia-Pacific Export Processing Volumes Rose 24% While European Specialty Demand Shifted Toward Premium Functional Formulations. Asian producers are optimizing high-volume manufacturing for processed food applications, whereas European manufacturers are prioritizing customized savory and nutritional blends with higher-margin positioning. More than 37% of premium plant-based food launches now incorporate yeast-derived flavor systems. Companies are responding through regional product customization, localized warehousing, and strategic partnerships with alternative protein brands to capture faster-moving demand categories.

Subscription-Based Ingredient Supply Agreements Expanded by 19%, Redefining Commercial Procurement Models. Food ingredient buyers are increasingly securing multi-year sourcing contracts to reduce raw material volatility and logistics disruptions. Integrated suppliers shortened delivery lead times by nearly 16% through decentralized distribution networks and predictive inventory systems. Labor shortages across fermentation operations are also forcing companies to increase process automation and digital quality monitoring, optimizing operational continuity while strengthening long-term customer retention through service-based supply partnerships.

The yeast extract market is segmented by type, application, and end-user, with powder variants accounting for nearly 44% demand due to scalability and processing efficiency advantages. Food processing remains the dominant application segment with over 46% consumption share, driven by clean-label reformulations and sodium-reduction initiatives. Demand is increasingly shifting toward organic and nutritional product categories as premium food manufacturing expands across Europe and North America. Food and beverage companies continue leading end-user adoption, while nutraceutical and biotechnology segments are accelerating faster through functional ingredient integration and precision fermentation deployment. Strategic investments are increasingly concentrated in high-purity formulations, customized blends, and automated fermentation capacity expansion.

Powder yeast extract dominates the global market with approximately 44% share due to its superior shelf stability, lower transportation costs, and seamless integration into large-scale food processing operations. Manufacturers prefer powder formats because they improve dosing precision by nearly 18% and reduce storage complexity compared to liquid alternatives. Organic yeast extract is emerging as the fastest-growing segment, with adoption expanding by approximately 23% during 2025 as clean-label and non-GMO product positioning accelerates across Europe and North America. Compared to paste variants, organic formats command higher margins and stronger penetration within premium nutrition applications. Paste and liquid yeast extracts collectively account for nearly 38% market share, maintaining strategic relevance in sauces, ready meals, and industrial fermentation applications where flavor intensity and rapid solubility remain critical. Companies are increasingly shifting product portfolios toward specialty powder and organic variants while expanding automated drying and precision extraction capacity. Investment focus is clearly concentrating on scalable, export-oriented formulations with stronger regulatory alignment and premium pricing advantages.

Food Processing remains the leading application segment, accounting for nearly 46% of total yeast extract utilization due to rising demand for savory enhancement, sodium reduction, and clean-label reformulation. Usage concentration is strongest across processed snacks, instant meals, and plant-based foods where flavor retention and formulation stability are critical. Nutritional Products represent the fastest-growing application segment, with adoption increasing by approximately 24% during 2025 as functional nutrition and protein-enriched food demand intensifies globally. Compared with mature food processing applications, biotechnology deployment is shifting toward high-value precision fermentation and nutrient media optimization. Animal Feed, Pharmaceuticals, and Biotechnology collectively contribute nearly 41% market share, supported by increasing focus on gut health, microbial cultivation, and bio-based production systems. Companies are repositioning portfolios toward customized nutritional blends, fermentation-grade extracts, and specialty formulations optimized for performance-sensitive applications. Strategic expansion is increasingly targeting high-margin nutrition and biotechnology ecosystems where technical differentiation and application-specific functionality are becoming critical competitive advantages.

Food and Beverage companies dominate the yeast extract market with nearly 49% demand share, driven by large-scale dependency on flavor optimization, sodium reduction, and clean-label ingredient integration. Major processors are increasing procurement volumes as reformulated packaged foods and plant-based products continue expanding globally. Nutraceuticals represent the fastest-growing end-user segment, recording approximately 25% adoption growth during 2025 due to rising demand for functional nutrition, immunity-focused formulations, and protein-enhanced supplements. Compared with the established Food and Beverage sector, Biotechnology buyers prioritize high-purity extracts and customized nutrient profiles for precision fermentation applications. Animal Nutrition, Pharmaceutical, and Biotechnology sectors collectively account for around 39% market demand, supported by expanding microbial feed solutions and bio-based product development. Companies are increasingly targeting these segments through premium pricing models, strategic formulation partnerships, and specialized product customization. Demand is clearly shifting toward technically advanced, application-specific yeast extracts that deliver stronger performance consistency and regulatory compliance advantages.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific leads global yeast extract production through large-scale fermentation infrastructure, cost-efficient molasses supply chains, and high processed food demand across China, India, and Southeast Asia. Europe contributes nearly 29% of global demand and is accelerating adoption through sodium-reduction regulations, clean-label reformulation mandates, and premium nutritional applications. North America maintains approximately 18% market share, driven by advanced food processing technologies and rising plant-based product integration. Supply chain regionalization following Red Sea logistics disruptions is reshaping global manufacturing strategies, forcing companies to localize production and diversify procurement networks. Global players are increasingly prioritizing Asia-Pacific for scalable manufacturing capacity while expanding innovation-focused formulation and specialty ingredient investments across Europe and North America.

North America accounts for nearly 18% of global yeast extract demand, supported by large-scale processed food manufacturing, plant-based nutrition expansion, and sodium-reduction initiatives. More than 43% of packaged food companies increased usage of natural flavor enhancement systems during 2025 as regulatory scrutiny surrounding artificial additives intensified. Advanced fermentation automation reduced batch processing downtime by approximately 15%, accelerating operational efficiency across ingredient facilities. U.S. manufacturers are expanding localized production networks to reduce dependency on imported fermentation inputs following supply chain disruptions and freight cost volatility. Enterprise buyers increasingly prioritize formulation consistency, traceability, and rapid customization capabilities over low-cost sourcing alone. Companies are strategically investing in precision fermentation platforms and specialty savory ingredient portfolios to strengthen long-term competitive positioning across high-margin food innovation ecosystems.

Europe contributes approximately 29% of global yeast extract demand, with Germany, France, and the Netherlands leading advanced fermentation and clean-label ingredient adoption. Sodium-reduction mandates and stricter additive labeling regulations accelerated natural flavor enhancer integration by nearly 31% across processed food applications during 2025. Food manufacturers are deploying energy-efficient extraction systems that lower water consumption by approximately 14% while strengthening ESG compliance performance. Premium food producers increasingly prioritize organic and non-GMO yeast extract formulations as consumer preference shifts toward transparency-driven purchasing behavior. Regional suppliers are expanding specialty ingredient partnerships and investing in low-emission fermentation infrastructure to secure long-term retail and export access. Europe is forcing global producers to adapt faster toward sustainable processing, premium formulation capabilities, and compliance-led operational transformation.

Asia-Pacific dominates the global yeast extract market with nearly 46% share, led by China, India, and Japan through large-scale fermentation capacity and rapidly expanding processed food production. China alone contributes over 31% of global manufacturing output due to integrated molasses supply chains and lower operational costs. Regional manufacturers increased automated fermentation deployment by approximately 28% during 2025 to improve extraction consistency and accelerate export scalability. Processed food demand and instant meal production continue reshaping ingredient procurement priorities across urban consumer markets. Companies are aggressively expanding regional production hubs and localized warehousing networks to shorten delivery cycles by nearly 17%. Enterprise buyers across Asia-Pacific prioritize cost efficiency, speed, and scalable supply reliability, making the region strategically critical for global production expansion and high-volume ingredient sourcing.

South America represents approximately 7% of global yeast extract demand, with Brazil and Argentina leading regional consumption through expanding processed food and animal nutrition industries. Rising urban food consumption increased industrial savory ingredient adoption by nearly 19% during 2025, particularly across packaged snacks and convenience foods. However, infrastructure limitations and currency volatility continue constraining fermentation equipment imports and long-term capital expansion. Regional manufacturers are increasingly focusing on localized production partnerships and flexible supply agreements to stabilize procurement risks and reduce import dependency. Price-sensitive buyers prioritize functional performance and cost optimization over premium ingredient positioning, forcing suppliers to balance affordability with quality consistency. The region presents strong medium-term expansion potential, but operational resilience and localized supply chain investment remain critical for sustainable competitive growth.

The Middle East & Africa region contributes nearly 6% of global yeast extract demand, driven by expanding food processing investments across the UAE, Saudi Arabia, and South Africa. Processed food manufacturing capacity increased by approximately 16% during 2025 as governments accelerated food security and industrial diversification initiatives. Regional producers are increasingly adopting automated blending and fermentation technologies to improve product consistency and reduce import dependency. Strategic partnerships between ingredient suppliers and local food manufacturers are strengthening regional distribution infrastructure and shortening procurement timelines by nearly 12%. Enterprise buyers prioritize scalable supply access, shelf-life optimization, and affordable flavor enhancement solutions for rapidly urbanizing consumer markets. The region is emerging as a strategic expansion zone where localized manufacturing investment and infrastructure modernization are reshaping long-term ingredient demand patterns.

China Yeast Extract Market – 31% market share: Dominates through large-scale fermentation capacity, integrated molasses supply chains, and strong processed food manufacturing demand.

United States Yeast Extract Market – 17% market share: Leads through advanced food processing innovation, high clean-label adoption, and expanding plant-based nutrition applications.

The yeast extract market is dominated by global ingredient leaders including Lesaffre, Angel Yeast, Kerry Group, DSM-Firmenich, and Lallemand competing against regional fermentation specialists and low-cost Asian manufacturers. The top five players collectively control nearly 44% of global market share, with competition centered on fermentation efficiency, customized savory formulations, and supply chain integration. Premium producers are improving extraction efficiency by approximately 18% through AI-assisted fermentation systems, while cost-focused manufacturers reduce operating expenses by nearly 14% via integrated molasses sourcing and high-capacity processing facilities. Competition is rapidly shifting toward specialty nutrition, clean-label ingredients, and precision flavor systems rather than commodity-based pricing alone. Companies are expanding through regional production hubs, strategic partnerships, and vertical integration to secure raw material stability and shorten delivery cycles. High infrastructure costs, regulatory compliance complexity, and fermentation scalability remain major entry barriers. Winning increasingly depends on combining technology optimization, supply resilience, and application-specific formulation expertise.

Lesaffre

Angel Yeast

Kerry Group

DSM-Firmenich

Lallemand

Ohly

Biospringer

AB Mauri

Synergy Flavors

Leiber GmbH

Alltech

KOHJIN Life Sciences

Oriental Yeast Co., Ltd.

Specialty Biotech Co., Ltd.

Autolyzed yeast extraction remains the dominant production technology in 2026, particularly in savory food, bakery, and plant-based formulations. Manufacturers are integrating enzyme-assisted extraction systems with automated fermentation controls to improve amino acid recovery and flavor consistency. Advanced membrane filtration technologies are reducing processing waste by nearly 18% while improving protein concentration efficiency by 12%. Around 58% of large-scale producers now use digitally monitored fermentation platforms to optimize nutrient utilization and batch stability. Compared with conventional thermal extraction methods, modern low-temperature enzymatic processing delivers nearly 22% higher flavor retention and lower sodium formulation capability, creating a competitive advantage for suppliers serving clean-label and reduced-MSG food applications.

Emerging technologies between 2026 and 2028 are centered on precision fermentation, circular bio-processing, and AI-driven bioreactor optimization. Companies are increasingly converting brewery by-products into high-value yeast proteins and beta-glucan-rich extracts, improving raw material utilization by nearly 30%. Integrated AI fermentation systems are reducing contamination risks by 15% while shortening production cycles by 10%. Adoption of smart inline sensors has crossed 40% among premium ingredient manufacturers focused on pharmaceutical nutrition and vegan food segments. Producers investing early in sustainable fermentation infrastructure are strengthening supply security and gaining faster regulatory acceptance in export-driven markets.

Disruptive innovation is shifting toward customized yeast extract functionality for alternative proteins, pet nutrition, and nutraceutical formulations. High-nucleotide yeast extracts designed for umami enhancement are improving flavor performance in plant-based meat systems by nearly 25% compared with older extract blends. Microencapsulation technologies are also increasing shelf stability by 14% in fortified beverages and clinical nutrition products. Large fermentation specialists and biotechnology-led ingredient firms benefit most from these developments because scalable precision extraction capabilities are becoming a major competitive differentiator. Through 2028, companies delaying automation and sustainable extraction upgrades risk higher processing costs, lower formulation flexibility, and slower response to evolving clean-label demand.

June 2024 – dsm-firmenich announced the sale of its yeast extract business to Lesaffre, including a technology partnership focused on savory ingredient development. The divested business represented approximately €120 million in annual sales, strengthening Lesaffre’s global fermentation portfolio and supply capabilities in clean-label food applications. [Savory Portfolio Shift] Source: Perfumer & Flavorist

June 2025 – Lesaffre finalized a 70% acquisition stake in Biorigin from Zilor to expand yeast-derived savory and nutritional ingredient production. The joint venture combined vertically integrated supply operations across food and feed sectors, improving scalability for natural flavor and fermentation-based ingredient manufacturing across international markets. [Fermentation Scale Alliance] Source: Food Business MEA

December 2025 – Yeastup launched an industrial-scale upcycling facility in Switzerland capable of processing 40 hectoliters of spent brewer’s yeast per hour. Production capacity increased from 1,600 liters to 4,000 liters hourly, accelerating commercial supply of yeast-derived proteins and beta-glucan ingredients for functional nutrition applications. [Circular Protein Expansion] Source: Protein Report

December 2025 – Yeastup confirmed regular industrial-scale production would begin in early 2026 following a CHF 10 million investment into advanced extraction infrastructure and food-grade processing operations. The 1,700 m² facility supports continuous production models, strengthening Europe’s capacity for sustainable yeast-based ingredient manufacturing and specialty nutrition supply chains. [Industrial Upcycling Capacity] Source: Baking & Biscuit

The yeast extract market report delivers comprehensive coverage across autolyzed, hydrolyzed, and specialty yeast extract categories used in food processing, pharmaceuticals, nutraceuticals, feed nutrition, and biotechnology applications. The analysis evaluates more than 15 application segments, including plant-based foods, savory formulations, bakery products, clinical nutrition, pet food, and microbial media systems. Geographic assessment spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level evaluation for high-growth manufacturing hubs. The report also examines core technologies such as enzyme-assisted extraction, precision fermentation, membrane filtration, bio-upcycling systems, and AI-enabled fermentation monitoring. Approximately 58% of industrial manufacturers are analyzed for automation adoption trends and process-efficiency improvements.

The study profiles over 25 major companies and tracks measurable indicators including sodium reduction performance, flavor enhancement efficiency, production utilization rates, and clean-label adoption levels. Around 62% of analyzed food manufacturers now prioritize natural savory enhancers over synthetic additives, increasing demand for customized yeast-derived ingredients. The report further evaluates emerging segments including beta-glucan-rich extracts, high-nucleotide formulations, and sustainable brewery-waste upcycling technologies expected to influence competitive positioning between 2026 and 2033.

Strategically, the report supports expansion planning, product portfolio optimization, supplier benchmarking, and investment prioritization. It helps decision-makers identify high-demand application clusters, technology transition risks, regional production advantages, and innovation gaps shaping future competition in the global yeast extract industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1585 Million |

|

Market Revenue in 2033 |

USD 2103.32 Million |

|

CAGR (2026 - 2033) |

3.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lesaffre, Angel Yeast, Kerry Group, DSM-Firmenich, Lallemand, Ohly, Biospringer, AB Mauri, Synergy Flavors, Leiber GmbH, Alltech, KOHJIN Life Sciences, Oriental Yeast Co., Ltd., Specialty Biotech Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |