Reports

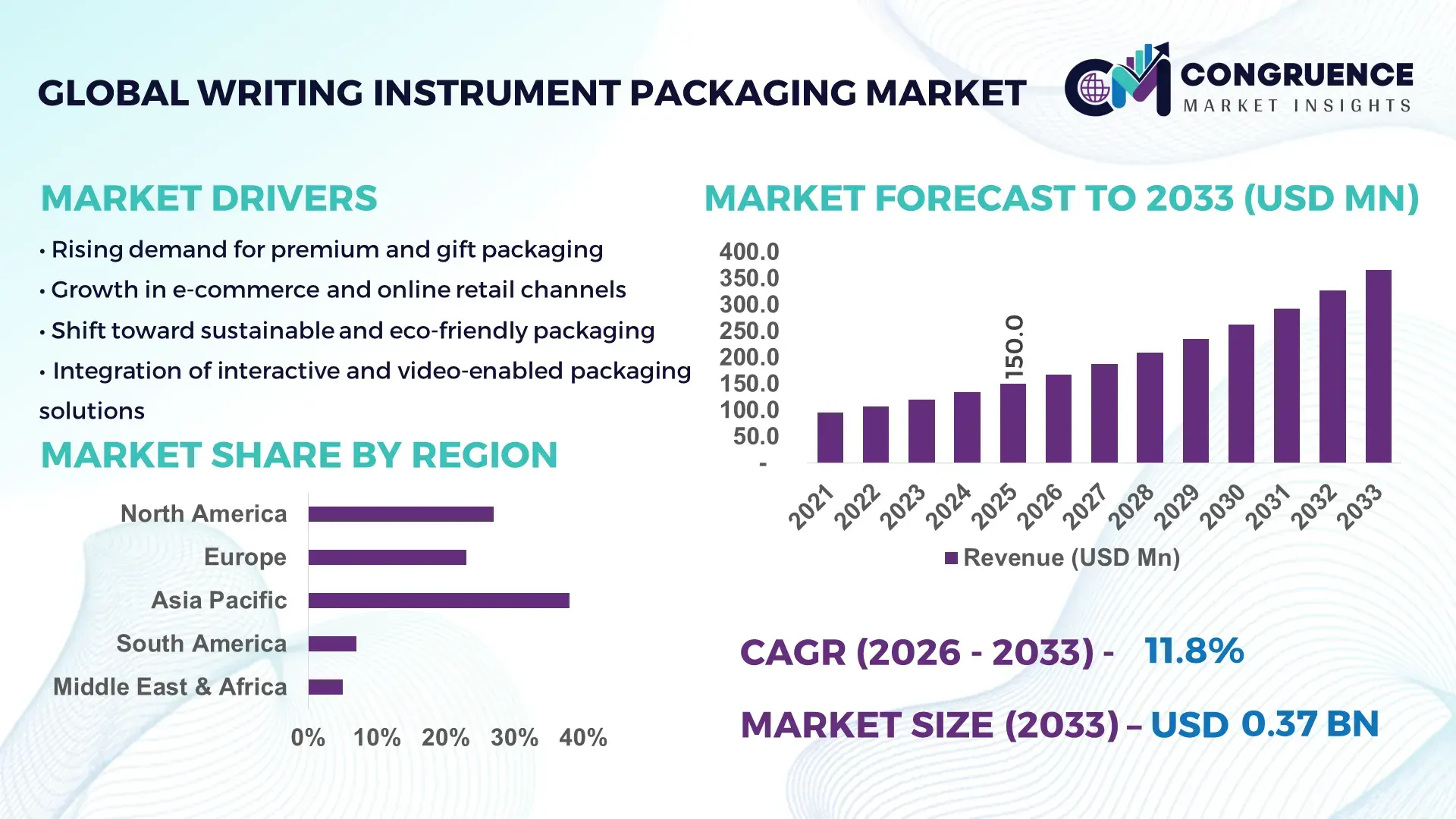

The Global Writing Instrument Packaging Market was valued at USD 150.0 Million in 2025 and is anticipated to reach a value of USD 366.1 Million by 2033, expanding at a CAGR of 11.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising consumer demand for premium, durable, and sustainable packaging solutions across stationery and corporate gifting sectors.

India plays a pivotal role in the Writing Instrument Packaging Market, hosting over 120 production units specializing in innovative packaging solutions. Investment in automated packaging lines has increased by 35% over the past five years, enhancing efficiency and reducing manual handling. Key applications include high-end pen packaging, school and office stationery sets, and eco-friendly gift packaging. Technological advancements such as laser cutting and 3D-printed inserts have enabled customized, precision packaging. Consumer adoption of premium packaging is notable, with 62% of users preferring branded, aesthetically designed writing instrument packages in urban markets.

Market Size & Growth: Valued at USD 150.0 Million in 2025, projected to reach USD 366.1 Million by 2033, driven by rising demand for sustainable and premium packaging.

Top Growth Drivers: Increased automation efficiency 40%, adoption of eco-friendly materials 55%, enhanced customization options 48%.

Short-Term Forecast: By 2028, packaging production efficiency expected to improve by 30% with reduced material wastage.

Emerging Technologies: Smart packaging sensors, 3D-printed inserts, automated laser cutting.

Regional Leaders: North America projected at USD 120.0 Million, Europe USD 95.0 Million, Asia Pacific USD 140.0 Million by 2033, with unique adoption trends in sustainable packaging.

Consumer/End-User Trends: Key end-users include corporate gifting, educational institutions, and premium stationery buyers with growing preference for customizable packages.

Pilot or Case Example: In 2024, a pilot in India achieved 25% reduction in production downtime through automated packaging lines.

Competitive Landscape: Market leader: Pelikan (~18%), followed by Faber-Castell, Reynolds, Camlin, and Pilot.

Regulatory & ESG Impact: Firms are adopting biodegradable materials and complying with local packaging regulations.

Investment & Funding Patterns: Total recent investment exceeds USD 50 Million, focused on automation and green packaging initiatives.

Innovation & Future Outlook: Integration of AI in production, precision laser cutting, and sustainable packaging solutions driving future market growth.

Recent developments in the Writing Instrument Packaging Market highlight investments in automated folding and cutting machinery, with educational and corporate gifting sectors contributing over 65% of consumption. New eco-friendly inks, biodegradable plastics, and laser-cut inserts are reshaping production. Regional consumption in Asia Pacific is growing at a faster pace due to urban adoption of premium stationery products, while regulatory initiatives encourage sustainable packaging practices and reduce environmental impact.

The Writing Instrument Packaging Market is strategically significant for manufacturers and distributors seeking to enhance operational efficiency and sustainability. Advanced automated lines deliver up to 30% higher throughput compared to traditional semi-manual setups. North America dominates in production volume, while Asia Pacific leads in adoption with 68% of enterprises integrating eco-friendly packaging solutions. By 2028, AI-enabled quality inspection is expected to reduce material defects by 22%, enhancing profitability. Firms are committing to ESG improvements such as 40% reduction in plastic usage by 2030. In 2025, an Indian packaging company achieved a 25% increase in output efficiency through robotic folding systems. Forward-looking investments in smart packaging, automation, and sustainable materials position the Writing Instrument Packaging Market as a pillar of resilience, compliance, and sustainable growth, offering long-term opportunities for industry players to capitalize on evolving consumer and environmental demands.

The Writing Instrument Packaging Market is experiencing a rapid transformation driven by the need for premium, customized, and environmentally sustainable packaging solutions. Key market dynamics include the adoption of automated machinery, growth in corporate gifting, and rising demand for aesthetically appealing school and office stationery packages. The market is influenced by material innovations, regulatory pressures, and technological integration in packaging lines, which collectively enhance productivity, reduce errors, and align with sustainability objectives. Shifts toward eco-friendly plastics, biodegradable inserts, and laser-cut designs are redefining market standards and influencing consumer preferences globally.

Consumer preference for durable, aesthetically appealing, and sustainable packaging has surged, particularly in educational and corporate gifting sectors. About 62% of urban buyers now choose premium packaging for writing instruments. This trend incentivizes manufacturers to invest in laser cutting, automated folding, and 3D-printed inserts, which improve precision and reduce production time by approximately 20–25%. Adoption of eco-friendly materials, such as biodegradable plastics and recycled paperboard, further drives innovation and positions firms competitively.

Fluctuations in raw material costs, particularly paperboard, plastics, and sustainable alternatives, impact production planning and profitability. Global supply chain disruptions have led to delays in packaging components, raising operational costs by up to 18% in some regions. Small- and medium-sized manufacturers face challenges adopting high-cost automated machinery. Additionally, stringent environmental compliance measures, while beneficial long-term, require upfront investment that can slow adoption of new packaging technologies.

The rise of personalized packaging, including customizable branding and QR-enabled smart inserts, offers significant opportunities. About 40% of premium stationery buyers prefer packages tailored to corporate or educational clients. Implementation of 3D printing and smart sensor integration can reduce waste by 15% and enhance customer engagement. Expansion into digital printing and automated customization allows manufacturers to tap niche sectors, such as limited-edition stationery and promotional gifting, creating higher-value offerings.

Increasing environmental regulations demand the use of biodegradable, recyclable, or eco-friendly materials, which can be costlier and require new production processes. Non-compliance risks fines and reputational damage. Manufacturers must invest in R&D for material substitution and redesign processes. Labor training for automated, eco-friendly production systems adds additional complexity. These challenges, combined with fluctuating raw material costs, slow overall market agility despite high consumer demand for sustainable packaging solutions.

Surge in Eco-Friendly Materials Adoption: Manufacturers are replacing conventional plastics with biodegradable and recycled alternatives, with 52% of packaging lines in Asia Pacific utilizing eco-friendly materials in 2025.

Automated Precision Production: Deployment of automated laser cutting and folding machinery has improved production accuracy by 28% and reduced labor dependency by 35% across North American and European markets.

Personalized and Smart Packaging Expansion: About 40% of premium stationery buyers now demand personalized packaging, including QR-enabled inserts and customizable compartments, creating higher-value offerings and improving brand engagement.

Regional Consumption Patterns and Technological Integration: Europe leads in adopting high-precision packaging technologies, while Asia Pacific shows accelerated growth in premium stationery packaging, with 68% of enterprises implementing automated systems to enhance efficiency and reduce production errors.

The Global Writing Instrument Packaging Market is segmented across multiple dimensions, enabling detailed insights into product types, applications, and end-user behavior. By type, the market encompasses rigid boxes, folding cartons, blister packs, and eco-friendly packaging solutions, each catering to different product protection and presentation requirements. In terms of application, the segments include corporate gifting, educational stationery, office supplies, and promotional merchandise, reflecting the diverse demand drivers. End-user insights highlight preferences among schools, colleges, office environments, and premium consumer buyers. Increasing demand for sustainable and customizable packaging, along with adoption of advanced automated production techniques, is shaping purchasing patterns and influencing procurement decisions across regions, highlighting the strategic importance of segmentation for supply chain planning and innovation deployment.

Rigid boxes currently lead the market, accounting for approximately 45% of adoption, driven by their durability, premium feel, and ability to accommodate high-end writing instruments securely. Folding cartons represent 28% of the market, favored for cost efficiency and lightweight shipping, while blister packs contribute 15%, offering visibility and protection for retail display. Eco-friendly packaging solutions currently make up 12%, gaining traction due to regulatory and consumer sustainability initiatives.

Video packaging solutions are emerging fastest, projected to surpass 30% adoption by 2033 due to demand for interactive unboxing experiences and digital integration in corporate gifting.

Corporate gifting leads applications with 40% adoption, driven by demand for premium, branded packaging in promotional campaigns and high-end office stationery sets. Educational stationery accounts for 30%, addressing school and college kit packaging requirements, while office supplies cover 20%, including standard pens, markers, and sets for enterprise procurement. Promotional merchandise contributes the remaining 10%, often tied to event-specific branding initiatives.

The fastest-growing application is educational stationery, fueled by rising adoption of sustainable and customizable kits for students, expected to expand rapidly across urban and semi-urban regions.

Consumer trends highlight that in 2025, more than 38% of institutions globally reported upgrading packaging for stationery kits to enhance brand engagement. Additionally, over 60% of Gen Z consumers show higher preference for eco-friendly and visually appealing educational packaging.

Premium consumer buyers dominate end-users, representing 42% of the market, preferring branded, durable, and customizable writing instrument packages for personal or gifting purposes. Educational institutions follow with 28%, integrating standardized kits for students. Office environments account for 20%, while corporate buyers and promotional use cover 10%.

The fastest-growing end-user segment is corporate gifting, driven by increasing investment in premium employee recognition programs and event marketing. Adoption of automated packaging solutions and interactive inserts is enhancing engagement, while 55% of companies are piloting limited-edition packaging initiatives.

Other contributing end-users include e-commerce platforms and retail outlets, collectively holding 10%, leveraging innovative packaging for direct-to-consumer shipments.

Asia Pacific accounted for the largest market share at 38% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2026 and 2033.

Asia Pacific’s dominance is supported by over 120 production units in India, China, and Japan, coupled with rising demand for sustainable and premium writing instrument packaging. India alone produces more than 45 million premium stationery packages annually. Urban consumer adoption is high, with over 62% of buyers preferring eco-friendly and customizable packages. Expansion of automated manufacturing lines, integration of laser-cut inserts, and investments exceeding USD 50 million are driving production efficiency and innovation in the region.

North America holds approximately 27% of the market volume, with demand driven by corporate gifting, educational institutions, and office supplies. Key industries, including healthcare and finance, are rapidly adopting premium and sustainable packaging for internal and client-facing purposes. Regulatory changes encouraging biodegradable and recyclable materials have prompted manufacturers to invest in green packaging technologies. Technological advancements such as automated folding, laser-cutting systems, and digital print integration are modernizing production lines. Companies like Pelikan North America are expanding operations by introducing smart packaging options for corporate clients. Consumers in this region favor functional, branded, and interactive packaging experiences.

Europe accounts for roughly 23% of the market, with Germany, the UK, and France as key contributors. Regulatory bodies are enforcing stringent sustainability and recycling initiatives, promoting biodegradable and recyclable packaging solutions. Adoption of advanced automated machinery, 3D inserts, and high-precision digital printing supports efficiency and quality. Local players such as Faber-Castell Germany are implementing eco-friendly production lines to meet regulatory demands and consumer preferences. European buyers prioritize compliance with environmental standards, while premium stationery consumers increasingly demand customizable and durable packages, boosting regional innovation and technology deployment.

Asia Pacific leads the market with a 38% volume share, driven by high consumption in India, China, and Japan. Manufacturing infrastructure expansion, including automated folding lines and precision cutting machines, supports large-scale production. Regional technology trends focus on 3D-printed inserts, smart packaging sensors, and sustainable materials. Local companies such as Camlin India have introduced laser-cut, eco-friendly packages for corporate and educational applications, enhancing operational efficiency. Consumer behavior favors premium, sustainable, and visually appealing packaging, with 62% of urban buyers selecting customized or environmentally responsible products, fueling adoption and innovation.

South America accounts for approximately 7% of the market, with Brazil and Argentina as leading contributors. Growth is supported by the expansion of retail and office supply infrastructure, alongside government incentives for sustainable packaging adoption. Companies like Staedtler Brazil are developing eco-friendly and high-visibility packaging solutions for schools and corporate gifting. Regional consumers show strong demand for multilingual labeling and customized designs to meet cultural and language-specific preferences. Investment in production modernization and sustainable materials is gradually increasing, aligning with regional environmental regulations and enhancing consumer appeal.

The Middle East & Africa region represents 5% of the global market, with major growth countries including UAE and South Africa. Demand is fueled by office, education, and corporate gifting sectors. Technological modernization trends include automated packaging lines and precision laser-cut inserts. Local regulations promote recyclable and biodegradable packaging, while trade partnerships facilitate cross-border distribution. Companies such as Pilot UAE are introducing interactive and sustainable packaging products. Regional consumers favor high-quality, durable packaging with branding appeal, supporting increased adoption of advanced and eco-friendly solutions.

India – 20% Market Share: High production capacity with over 45 million premium stationery packages produced annually.

China – 18% Market Share: Strong end-user demand supported by automated manufacturing and urban consumer adoption of sustainable packaging.

The competitive environment within the Writing Instrument Packaging Market is moderately fragmented yet progressively consolidating, with an estimated 50+ active competitors ranging from global packaging giants to specialized regional firms. Leading players like Sonoco Products Company, Graphic Packaging International, Amcor (including Berry Global), and Avery Dennison Corporation leverage extensive manufacturing footprints, diversified product portfolios, and sustainable material innovations to solidify their positions across key regions. Asia Pacific and North America host concentrated networks of packaging converters and contract manufacturers supporting demand in stationery, corporate gifting, and retail segments. Combined, the top 5 companies command approximately 30–35% of global volume, underscoring competitive intensity where mid‑tier players and niche specialists remain influential. Strategic initiatives such as product launches, sustainability partnerships, leadership in recyclable substrate development, and automated production line deployments are shaping market rivalry. Major firms are enhancing capability in high‑precision blister cards, rigid boxes, and eco‑friendly paperboard solutions to meet stricter regulatory mandates and consumer expectations. Innovation trends include digital print integration on packaging runs, smart inspection technologies to reduce defects, and supply‑chain synergies arising from regional mergers and capacity expansions. Overall, competition blends traditional production strengths with forward‑looking sustainability and digitization efforts, making agility and technological adoption key differentiators.

Amcor Plc

Berry Global

Pregis

Pregis LLC

WestRock

Smurfit Kappa

Mondi Group

Sealed Air

TC Transcontinental

Huhtamaki

Ahlstrom

AptarGroup

Technological transformation within the Writing Instrument Packaging Market is driven by the need for higher productivity, sustainability, and enhanced functionality. Automation remains at the forefront, with packaging lines increasingly adopting robotic assembly, precision laser cutting, and automated inspection systems to reduce manual labor dependency and maintain consistent quality across high‑volume runs. Digital printing technologies — including variable data printing — enable dynamic branding and customization, allowing brands to tailor packaging designs to specific promotional campaigns without extensive inventory. Across material science, innovations in recycled paperboard, biodegradable films, and adhesives engineered for recyclability are pivotal in meeting evolving regulatory and consumer sustainability expectations. Smart packaging concepts — such as QR code integration and embedded sensors — are gradually gaining relevance for interactive consumer engagement, enhanced supply‑chain traceability, and product authentication. RFID and machine‑vision systems are also being integrated into quality and orientation inspection routines, enabling up to 80% accuracy in automated material sensing for package integrity checks. Energy‑efficient curing and drying technologies further support eco‑friendly operations by lowering energy consumption and minimizing emissions. Collectively, these technological advancements not only streamline production but support strategic differentiation in a market where material performance, environmental compliance, and digital engagement are increasingly crucial.

• In November 2025, Sonoco Products Company announced it is consolidating its Metal Packaging and Rigid Paper Containers businesses under two geographic structures—Consumer Packaging EMEA/APAC and the Americas—to create a simpler, more efficient operating model that is expected to spur innovation, collaboration and growth opportunities across global packaging operations. Source: www.investor.sonoco.com

• In September 2025, Avery Dennison Corporation launched a series of new labeling and packaging solutions at Labelexpo Europe 2025 focused on advancing recycling, connectivity and safety, including expanded AD CleanGlass™ and AD CleanFiber™ solutions and premium materials that improve packaging performance and supply chain transparency. Source: www.label.averydennison.com

• In April 2025, Avery Dennison inaugurated a new RFID inlay and label manufacturing facility in Pune, India, strengthening regional smart labeling capabilities and accelerating innovation and supply chain efficiency for intelligent packaging solutions across multiple industries. Source: www.sustainabilitymea.com

• In December 2025, Graphic Packaging International expanded its news and events portfolio featuring new innovations such as its next‑generation Boardio™ technology, multi‑footprint capabilities for sustainable paperboard solutions, and partnerships to drive forest restoration initiatives under its social impact programs. Source: www.graphicpkg.com

The Writing Instrument Packaging Market Report encompasses a broad and detailed examination of product formats, end‑use applications, geographic reach, and technological advancements shaping the industry landscape. It covers key product segments including blister cards, rigid boxes, folding cartons, eco‑friendly formats, and bespoke rigid presentation packages, each tailored to address protection, display aesthetics, and retail readiness. The report’s geographic segmentation spans North America, Europe, Asia Pacific, South America, and Middle East & Africa, offering insights into regional production capacities, consumer preferences, regulatory influences, and infrastructure development. Application assessments profile demand in corporate gifting, educational stationery, office supplies, and promotional merchandise, highlighting usage patterns and procurement behavior across diverse end‑users. The technology section evaluates automation, digital print integration, smart inspection systems, and sustainable material innovations that drive production efficiency and environmental compliance. Special focus areas include sustainability transitions to recyclable and biodegradable substrates, interactive packaging features, and material handling advancements to reduce waste. Emerging niche segments such as customized luxury packaging and digitally enhanced packaging experiences are also articulated to illustrate future opportunities. Collectively, the report serves as a comprehensive guide for decision‑makers, delineating strategic priorities across market structure, innovation trends, regulatory landscapes, and competitive positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 150.0 Million |

| Market Revenue (2033) | USD 366.1 Million |

| CAGR (2026–2033) | 11.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sonoco Products Company, Graphic Packaging International, Avery Dennison Corporation, Amcor Plc, Berry Global, Pregis, Pregis LLC, WestRock, Smurfit Kappa, Mondi Group, Sealed Air, TC Transcontinental, Huhtamaki, Ahlstrom, AptarGroup |

| Customization & Pricing | Available on Request (10% Customization Free) |