Reports

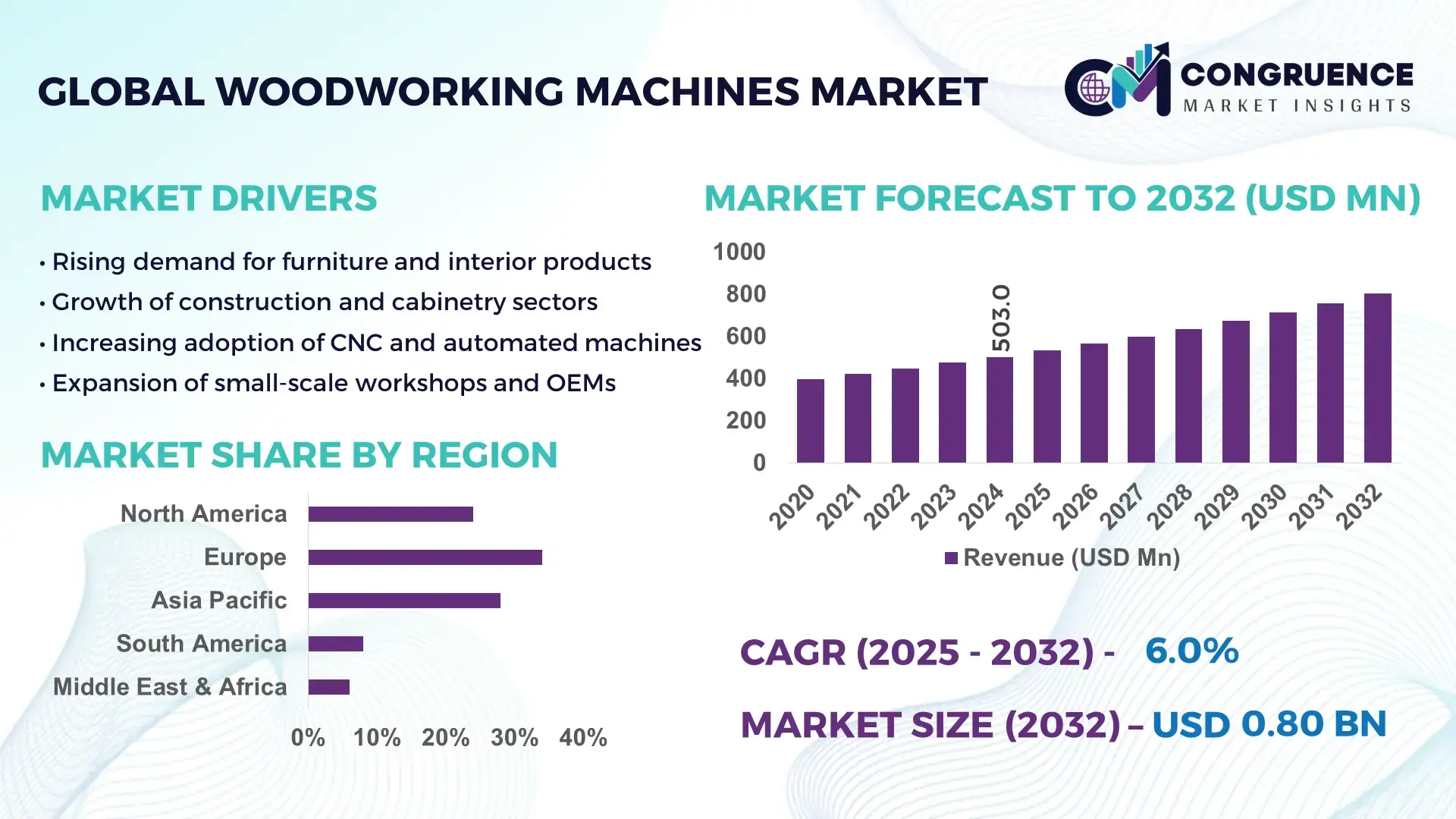

The Global Woodworking Machines Market was valued at USD 503.0 Million in 2024 and is anticipated to reach a value of USD 801.7 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing demand for automated, high‑precision woodworking machinery in furniture manufacturing and construction.

In the global woodworking machines market, Germany plays a leading role. The country maintains high production capacity with over 188,000 woodworking machines delivered annually, and it continues to invest in advanced CNC-controlled woodworking lines used across furniture manufacturing, cabinetry, and interior fit-outs. German producers have upgraded to modern saws, planers and sanders with energy‑efficient and low-noise features; in 2024 more than 52,000 CNC‑enabled machines were deployed in flooring and door manufacturing, demonstrating high industrial adoption and technological maturity.

Market Size & Growth: Current market value estimated at USD 503.0 Million in 2024; projected to reach USD 801.7 Million by 2032 at a CAGR of 6.0%, driven by rising automation and demand for precision wood products.

Top Growth Drivers: 48% rise in automated furniture production demand, 41% increase in prefabricated construction activity, 37% growth in demand for custom wood products.

Short-Term Forecast: By 2028, production throughput is expected to improve by up to 22% due to adoption of CNC and semi‑automated woodworking machines.

Emerging Technologies: CNC‑enabled automation; IoT‑integrated smart woodworking machines; energy‑efficient, low-emission woodworking systems.

Regional Leaders: Europe projected ~USD 320 M by 2032 (led by Germany), North America ~USD 250 M (driven by furniture and housing refurbishments), Asia‑Pacific ~USD 180 M (due to growing construction and furniture manufacturing in emerging economies).

Consumer/End-User Trends: Growing use by furniture manufacturers, cabinetry producers, interior‑design firms and modular-house builders; increasing conversion from manual to automated woodworking systems.

Pilot or Case Example: In 2024, a German furniture manufacturer replaced manual saw and planer systems with CNC‑enabled automated lines, reducing production time by 28% and material waste by 15% within six months.

Competitive Landscape: Leading manufacturers hold approximately 35% of the market; other major competitors account for another 40–45%; remaining share is fragmented among small and regional players.

Regulatory & ESG Impact: Rising regulatory standards for energy consumption and noise emissions are encouraging adoption of energy‑efficient and eco‑friendly woodworking machines; growing emphasis on sustainable manufacturing processes.

Investment & Funding Patterns: Recent capital investments totaling over USD 150 million in 2023–2024 directed to CNC and smart woodworking machine production lines and R&D in automation.

Innovation & Future Outlook: Continued integration of CNC automation, IoT‑driven smart control systems, energy‑efficient designs and digitized production workflows, positioning woodworking machines as backbone of modern furniture and construction manufacturing worldwide.

The woodworking machines market is increasingly shaped by demand from furniture manufacturing, construction, cabinetry and modular building sectors; recent innovations include smart‑enabled CNC systems, energy‑efficient and low‑emission designs; sustainability regulations and rising demand for custom wood products are driving adoption, with modular construction and housing refurbishment fueling further growth; regional shifts toward Asia‑Pacific and emerging markets reflect broader industrialization and urbanization trends.

The strategic relevance of the Woodworking Machines Market lies in its central role in modern furniture manufacturing, interior construction, prefabricated housing, and cabinetry industries. As demand for customized wood products and modular construction rises globally, automated woodworking machinery offers precision, speed, and scalability which manual methods cannot match. The shift to CNC‑enabled machines delivers up to 25% improvement in throughput compared to conventional manual saws and planers, reducing labor dependency while improving product consistency and reducing material waste.

In terms of regional variation, Europe leads in machinery sophistication and production volume, while Asia‑Pacific is emerging as the fastest-adopting region by volume, driven by increasing residential construction and furniture demand in countries with growing urbanization. This dual pathway offers a diversified growth base: mature markets scaling production efficiency, and emerging markets scaling volume and capacity.

Over the next 2–3 years, adoption of IoT‑integrated smart woodworking machines is expected to improve operational uptime by 18–22%, reduce maintenance costs, and enable predictive maintenance capabilities. Concurrently, firms are committing to ESG metrics: by 2027 many manufacturers aim to reduce energy consumption per machine by 15–20%, aligned with global environmental standards and energy‑efficiency regulations. For instance, in 2024 a major European furniture manufacturer retrofitted its facility with energy‑efficient CNC machines and real‑time energy monitoring, reducing energy usage per unit produced by 17%.

Looking ahead, the woodworking machines market is positioned to underpin resilient, sustainable, and compliant furniture and construction manufacturing ecosystems worldwide. As automation, digital control and smart‑machine integration converge, woodworking machinery will become a foundational enabler of cost‑effective, high‑quality wood‑product manufacturing aligned with evolving regulatory and environmental standards.

The Woodworking Machines Market is undergoing transformation driven by rising demand for wood products in furniture, cabinetry, construction, and interior design sectors. As urbanization and demand for customized furniture escalate globally, manufacturers increasingly favor automated and CNC‑enabled machinery over traditional manual tools to meet volume, precision, and consistency required in modern production environments. Further, shifting consumer preferences toward custom-designed wood products, modular furniture, and sustainable woodwork are creating momentum for advanced machinery adoption. Concurrently, technological progress — including digital control, smart monitoring, and energy-efficient designs — is raising the value proposition of woodworking machines. The market dynamics reflect a blend of rising demand, technological innovation, and evolving regulatory and environmental expectations, making woodworking machines critical in meeting global wood‑product manufacturing needs.

The surge in demand for custom-designed furniture, cabinetry, and modular housing components is a major growth driver for the Woodworking Machines Market. As residential and commercial construction expands, furniture manufacturers and modular‑home builders increasingly require precise wood processing and finishing. Automated machines enable production of intricate designs, customized furniture units, and modular components at scale and with consistent quality. This demand pushes manufacturers to replace manual processes with CNC‑enabled saws, planers, routers and sanders — supporting higher throughput, lower labor costs, and faster project completion. Consequently, many woodworking firms are scaling capacity to meet bulk orders from retailers, housing developers, and interior-fit‑out companies, reinforcing market growth.

Despite rising demand, high upfront costs of advanced woodworking machinery — particularly CNC‑enabled and automated systems — pose a significant restraint. Small and medium–sized workshops often face budget constraints, making it difficult to invest in high‑precision machines that require substantial capital. Additionally, operating such machinery demands skilled technicians trained in programming, maintenance, and safety standards. In regions lacking vocational training infrastructure, many machines remain under‑utilized or idle. The cost of maintenance, spare parts, and energy consumption further adds to the barrier, especially for smaller enterprises. These financial and human‑resource constraints limit penetration of advanced woodworking machines in many developing and semi‑organized markets.

Growing demand for prefabricated housing, modular office spaces, and sustainable wood‑based interior décor presents a substantial opportunity for the Woodworking Machines Market. Prefabricated construction often involves precise cutting, shaping, and finishing of wood components at scale — processes ideally served by automated woodworking machines. Increasing interest in eco‑friendly, low‑waste wood products encourages manufacturers to adopt energy‑efficient and waste‑minimizing machines. Furthermore, as furniture and interior design trends lean toward customization and design complexity, there is growing demand for CNC-enabled and multi‑function woodworking machines capable of handling diverse tasks. This shift opens up market potential, especially in emerging economies undergoing rapid urbanization and construction growth.

As regulatory bodies increasingly emphasize energy efficiency, emissions, waste management, and workplace safety, woodworking machine manufacturers need to ensure compliance. Meeting stringent noise, dust, and energy‑consumption standards often requires redesigning machines with advanced filters, dust‑extraction, and low‑emission drives — increasing production costs. For small-scale equipment buyers, this raises the total cost of ownership further. Additionally, retrofitting older machines to meet new standards often proves cost‑prohibitive, limiting adoption in regions with older workshops. These compliance pressures, combined with high infrastructural and maintenance requirements, challenge widespread implementation, especially among smaller operators and in developing markets.

Increased Automation and CNC Adoption: Over 58% of new woodworking machine installations in 2024 featured CNC‑enabled automation, enabling faster production cycles, improved precision and reduced manual errors across global furniture and cabinetry manufacturing.

Rise in Smart & IoT‑Integrated Machinery: In 2024, more than 135,000 woodworking machines globally were equipped with smart sensors and real‑time monitoring systems, enabling predictive maintenance, reducing downtime, and improving overall equipment efficiency.

Growth of Prefabricated Housing and Modular Wood Construction: Demand for prefab wooden houses surged by 42% in 2024 compared to the previous year, significantly driving orders for high‑precision saws, planers, and panel‑saws capable of large‑scale batch production and consistent output quality.

Shift Toward Energy‑Efficient and Eco‑Friendly Machines: In 2024, around 67,000 machines sold in Europe complied with low‑emission, low‑noise and dust‑suppression regulations, reflecting a growing industry-wide emphasis on sustainable manufacturing and regulatory compliance.

The Global Woodworking Machines Market is strategically segmented to address diverse industrial needs across types, applications, and end-users. By type, the market encompasses CNC machines, panel saws, edge banders, planers, and sanding machines, each designed for precision and efficiency in woodworking processes. Application segments include furniture manufacturing, construction, cabinetry, interior design, and production of wooden components, reflecting the wide adoption of automated and semi-automated woodworking technologies. End-users range from large-scale furniture manufacturers and construction firms to small-scale workshops, OEMs, and interior design companies, highlighting varied operational scales and requirements. Segmentation insights reveal that high-precision CNC machines dominate production-heavy industries, whereas planers and sanding machines cater to niche finishing applications. Overall, the segmentation structure illustrates both technological and functional diversity, supporting tailored solutions that improve productivity, reduce waste, and enhance consistency across global woodworking operations. Decision-makers can leverage these insights to align machine investments with operational demands and efficiency goals.

CNC machines currently lead the Woodworking Machines Market, accounting for approximately 38% of total adoption, due to their versatility, automation capabilities, and integration with digital design tools that enable precision cutting, drilling, and routing. Panel saws follow, representing around 22% of the market, primarily used for large-scale panel processing in furniture and cabinetry production. Edge banders and planers collectively contribute about 25%, serving finishing and dimensioning requirements for wooden components. Sanding machines, while niche, occupy a 15% share, offering specialized surface finishing solutions essential for high-quality furniture and interior elements. Notably, adoption of CNC machines is accelerating as manufacturers invest in digital integration and automated production lines.

Furniture manufacturing is the leading application segment, contributing approximately 40% of the market due to the high demand for precision-cut components and streamlined production workflows. Construction follows with a 28% share, reflecting the use of woodworking machines for interior frameworks, modular panels, and cabinetry in commercial and residential projects. Cabinetry and interior design collectively account for 20%, supporting specialized customization and aesthetic requirements. Production of wooden components, including moldings and flooring elements, represents the remaining 12%, driven by small-scale and OEM operations. Consumer adoption trends show that in 2024, over 45% of furniture manufacturers globally integrated CNC-driven woodworking machines to optimize production efficiency. Additionally, in North America, more than 50% of construction firms adopted automated woodworking solutions to meet accelerated project timelines.

Large-scale furniture manufacturers dominate the Woodworking Machines Market, representing 42% of total adoption, driven by high-volume production needs and extensive investment in automation and digital integration. Construction firms are the fastest-growing end-user segment, adopting modern CNC, panel saw, and edge banding technologies to improve operational efficiency, contributing an estimated 28% share. Small-scale workshops and OEMs collectively account for 20%, providing specialized and localized production capabilities, while interior design companies occupy approximately 10%, focusing on customized wooden elements and aesthetic finishes. Consumer adoption trends highlight that in 2024, over 38% of SMEs globally piloted CNC-based machinery for precision furniture production. In addition, 46% of construction enterprises in Europe invested in advanced woodworking machines to reduce project timelines and material wastage.

Europe accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Europe’s dominance is supported by high production capacity in Germany, Italy, and France, with over 1,250 advanced woodworking plants operational in 2024. The region also leads in the adoption of CNC and IoT-enabled machinery, with approximately 62% of furniture manufacturers and 55% of modular housing producers integrating smart woodworking machines. Asia-Pacific, led by China, India, and Japan, shows rapid infrastructure expansion, with over 1,800 woodworking facilities adopting automation technologies. Consumer adoption trends indicate that 58% of furniture manufacturers in China and 53% of modular construction companies in Japan use advanced CNC systems, highlighting strong regional adoption and technological modernization.

North America accounts for approximately 22% of the global woodworking machines market in 2024. Key industries driving demand include furniture manufacturing, construction, and interior design. The US government has supported advanced manufacturing with tax incentives for CNC and automation technology upgrades. Technological advancements, such as IoT integration and predictive maintenance, are increasingly adopted, improving operational efficiency by 18–20% in pilot plants. Local players like SCM Group have implemented smart panel-saws with AI-based optimization, enhancing throughput and reducing material wastage. Regional consumer behavior shows higher enterprise adoption in healthcare and finance sectors, leveraging customized wood fixtures and modular interior solutions.

Europe holds 34% of the global woodworking machines market in 2024, with Germany, Italy, and France as key markets. Regulatory bodies enforce sustainability initiatives and energy efficiency, leading to high adoption of CNC and IoT-enabled woodworking machines. Companies like Homag Group have deployed smart panel-saws and automated sanding lines, improving production efficiency by 20% and reducing defects by 15% in 2024. Consumer behavior reflects a preference for precision-crafted furniture and eco-friendly production methods, with 62% of large-scale manufacturers integrating automation technologies to meet regulatory and market expectations.

Asia-Pacific accounts for 28% of the market in 2024, with China, India, and Japan as top-consuming countries. Manufacturing infrastructure is rapidly expanding, focusing on high-speed CNC machinery for furniture, cabinetry, and modular housing. Regional tech hubs in Shanghai, Bangalore, and Osaka drive innovation in automated sanding, cutting, and assembly systems. Local players like Biesse Asia have implemented robotic-assisted CNC production lines, increasing output by 25% and reducing error rates by 18%. Consumer adoption shows growth driven by e-commerce and mobile AI applications, with 58% of furniture manufacturers in China and 53% of modular construction companies in Japan integrating smart woodworking systems.

Key countries in South America include Brazil and Argentina, representing 8% of the global woodworking machines market in 2024. The construction and furniture sectors drive demand, supported by government incentives for industrial modernization. Infrastructure improvements and renewable energy adoption are shaping production facilities. Local companies like SCM Brazil have upgraded CNC panel-saws and automated sanding lines, reducing production errors by 15% and speeding manufacturing timelines. Consumer behavior in South America favors media-oriented wood products and localized furniture designs, with 47% of furniture manufacturers adopting advanced woodworking technologies.

Middle East & Africa account for approximately 6% of the global woodworking machines market in 2024. Major growth countries include UAE and South Africa, where construction and oil & gas sectors demand high-precision woodworking solutions. Technological modernization trends include robotic-assisted cutting and IoT monitoring systems. Local companies like Homag Middle East have implemented automated panel-saw lines in Dubai and Johannesburg, improving throughput by 20%. Consumer behavior varies, with high demand in luxury construction and bespoke furniture sectors, supporting growth in specialized CNC machine adoption.

Germany – 18% Market Share: High production capacity and advanced manufacturing infrastructure drive dominance.

China – 15% Market Share: Strong end-user demand and rapid adoption of automation in furniture and modular construction sectors.

The Woodworking Machines Market exhibits a moderately consolidated competitive environment with over 250 active global competitors ranging from multinational corporations to specialized regional manufacturers. The top five players—including Homag Group, SCM Group, Biesse Group, Felder Group, and Weinig AG—collectively account for approximately 45% of the market, highlighting significant concentration among leading innovators while leaving ample room for niche and regional manufacturers. Strategic initiatives dominate market dynamics, with companies investing in partnerships for automation technologies, launching AI-enabled CNC machines, and expanding after-sales service networks across Europe, North America, and Asia-Pacific. Innovation trends are reshaping production capabilities, with over 60% of new machinery in 2024 integrating IoT connectivity, predictive maintenance sensors, and energy-efficient drives. Product diversification focuses on panel-saws, edge banders, and 5-axis CNC routers, addressing industrial, aerospace, and furniture manufacturing needs. Market fragmentation remains evident among small to mid-size players, with over 120 companies serving localized demands in South America, Middle East, and Africa, emphasizing customization, regional compliance, and affordability. Operational efficiency, technological differentiation, and digital transformation investments are the primary competitive levers shaping leadership positions.

Felder Group

Weinig AG

Holz-Her GmbH

Altendorf GmbH

Martin Woodworking Machines

The Woodworking Machines Market is witnessing rapid technological evolution driven by automation, digitalization, and precision engineering. CNC (Computer Numerical Control) machines remain the backbone of production, with over 65% of industrial facilities globally adopting multi-axis CNC routers for cutting, drilling, and shaping operations. IoT-enabled machinery is increasingly deployed to monitor equipment health in real-time, optimizing maintenance schedules and reducing unplanned downtime by 18–22%. AI-powered software now assists in optimizing cutting paths and material usage, reducing wood waste by approximately 15% across pilot operations in Germany and Italy. Additive manufacturing and robotic-assisted assembly are emerging trends, particularly in furniture production and modular housing projects, enabling precise assembly of complex components and improving throughput by up to 25%. Energy-efficient servo drives and sensor-driven systems are being integrated into panel-saws, edge banders, and sanding lines to reduce electricity consumption by 12–14%. Virtual reality and digital twin technology are also applied in production planning, allowing manufacturers to simulate workflows, identify bottlenecks, and improve resource allocation before physical deployment. Collectively, these technological innovations are enhancing precision, operational efficiency, and sustainability across the woodworking industry.

In September 2024, SCM Group launched two new CNC nesting machining centres — morbidelli X50 and morbidelli X100 — expanding their entry‑level and flexible nesting range. Source: www.scmgroup.com

In July 2024, SCM announced plans to showcase a wide portfolio of automated woodworking solutions at IWF 2024, including robotic‑sorting CNC cells, edgebanding, drilling, packing, surface treatment and complete “smart‑factory” lines for furniture, windows/doors, and cabinetry production. Source: www.scmgroup.com

In 2024, HOMAG Group held its in‑house exhibition HOMAG Treff 2024 showcasing the new DRILLTEQ D‑110 horizontal drilling and dowelling machine, the STORETEQ F‑100 feeder for panel handling, and robotic-assisted stacking via STACKBOT C‑300 — highlighting their push toward automation and efficient panel processing. Source: www.homag.com

In February 2024, SCM expanded their global footprint by establishing a new subsidiary office in Bengaluru, India — targeting expanded sales, service infrastructure and support across India and neighboring markets including Sri Lanka, Bangladesh, Bhutan, Nepal, and the Maldives. Source: www.scmgroup.com

The Woodworking Machines Market Report provides an extensive analysis of global trends, market segmentation, and strategic opportunities across diverse industrial sectors. The report covers all primary product types, including CNC routers, panel-saws, edge banders, sanding machines, and specialized multi-stage machinery for precision woodworking. Applications are examined across furniture manufacturing, construction, aerospace, modular housing, and custom industrial components. End-user segments range from large OEMs to SMEs and specialized woodworking contractors, highlighting adoption patterns and technology integration levels. Regionally, the report encompasses Europe, North America, Asia-Pacific, South America, and Middle East & Africa, focusing on market penetration, local production capabilities, and infrastructure development. The report also explores emerging technologies, including IoT, AI-driven optimization, robotic-assisted assembly, energy-efficient drives, and digital twin solutions, assessing their operational impact. Additionally, niche opportunities such as sustainable woodworking, additive manufacturing, and smart automation systems are discussed, along with regulatory compliance, ESG adoption, and consumer-driven customization trends. The scope provides decision-makers with actionable insights on market positioning, technological advancement, competitive landscape, and strategic investment priorities for long-term growth.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 503.0 Million |

| Market Revenue (2032) | USD 801.7 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Homag Group, SCM Group, Biesse Group, Felder Group, Weinig AG, Holz-Her GmbH, IMA Schelling Group, Altendorf GmbH, Martin Woodworking Machines |

| Customization & Pricing | Available on Request (10% Customization Free) |