Reports

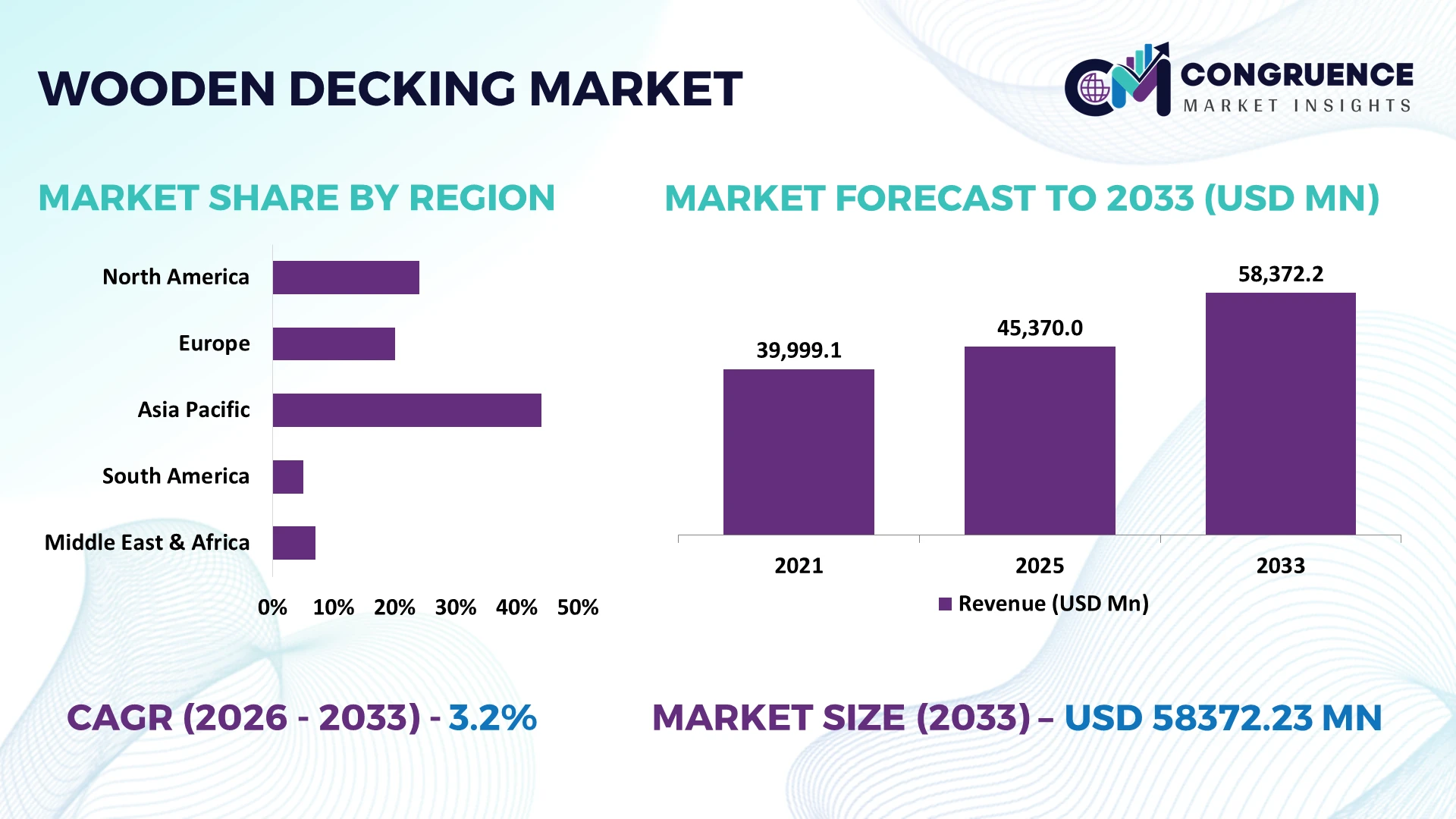

The Global Wooden Decking Market was valued at USD 45370 Million in 2025 and is anticipated to reach a value of USD 58372.23 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033. Growth is driven by rising outdoor living projects, engineered wood adoption, sustainable construction standards, and renovation activity across residential and commercial properties.

The United States remains a leading wooden decking market, accounting for nearly 35% of global consumption through residential remodeling and hospitality applications. North America invests over USD 20 billion annually in outdoor improvement projects, while Europe emphasizes certified timber solutions with more than 70% of new decking projects incorporating sustainability criteria. Compared with Asia-Pacific, which shows faster urban expansion, North America maintains higher premium decking adoption.

Strategic implication: Companies prioritizing sustainable materials, regional supply chains, and premium decking solutions are positioned to capture long-term market value.

Market Size & Growth: USD 45.37 billion (2025) to USD 58.37 billion (2033), 3.2% CAGR driven by sustainable outdoor construction trends.

Top Growth Drivers: Residential renovation 40%, hospitality projects 25%, eco-friendly materials 20% shaping market expansion.

Short-Term Forecast: By 2028, advanced wood treatment reduces maintenance costs by 15% and improves durability efficiency.

Emerging Technologies: AI-assisted design, automated manufacturing, and advanced wood coatings improve decking customization.

Regional Leaders: North America USD 20B+, Europe USD 14B+, Asia-Pacific USD 12B+ supported by renovation and urban projects.

Consumer Trends: Over 60% of buyers prioritize low-maintenance and sustainable decking options for outdoor spaces.

Pilot Example: 2025 modular decking projects achieved 20% faster installation through prefabricated wooden components.

Competitive Landscape: Leading suppliers hold approximately 30% share, with competition from major timber and decking manufacturers.

Regulatory & ESG Impact: Sustainable forestry compliance influences nearly 70% of premium decking procurement decisions globally.

Investment & Funding: Over USD 1 billion directed toward timber processing, recycling, and sustainable material expansion.

Innovation & Future Outlook: Next-generation decking focuses on hybrid materials, circular production, and climate-resistant solutions.

The Wooden Decking Market is expanding through demand for durable outdoor structures, premium residential spaces, and sustainable architectural designs. Recent innovations include pressure-treated wood, composite-enhanced timber solutions, and digital design tools improving project efficiency. Around 60% of buyers prioritize environmentally responsible materials, while supply-chain shifts toward certified timber networks support reliable procurement across global construction markets.

The Wooden Decking Market is becoming strategically important as builders, property developers, and timber suppliers compete around sustainable materials, faster installation, and premium outdoor infrastructure solutions. The shift toward certified wood sourcing and localized supply chains is reshaping procurement strategies, especially after global logistics disruptions exposed dependency risks.

Advanced wood treatment technologies now improve moisture resistance and lifecycle performance by nearly 30% compared with untreated traditional decking systems, reducing maintenance requirements for commercial projects. The United States leads in renovation-driven adoption, while Germany and Scandinavian countries emphasize certified timber standards and circular construction practices. Over the next 2–3 years, manufacturers are increasing automation, digital design integration, and regional processing capacity.

For example, North American decking producers are investing in automated cutting facilities and supplier partnerships to reduce material waste and improve delivery reliability. Companies strengthening sustainable sourcing networks, product customization, and operational efficiency will gain stronger competitive positioning in the evolving construction materials landscape.

Growing preference for sustainable outdoor infrastructure is accelerating wooden decking adoption across residential and commercial projects. Demand is supported by green building practices, with certified timber usage increasing by more than 20% in premium construction applications. The United States renovation sector and Australia’s outdoor living market are major contributors to adoption. New treatment technologies extend wood lifespan by nearly 30%, improving lifecycle economics. Companies are responding through investments in certified forestry partnerships, advanced coating facilities, and regional manufacturing expansion to secure reliable supply and meet evolving environmental standards.

Wooden decking manufacturers face pressure from timber price fluctuations, transportation constraints, and certification requirements. Global timber supply disruptions have increased material procurement costs by approximately 15–20% in recent cycles, affecting project margins. Canada and European suppliers are adapting through localized sourcing agreements and inventory optimization strategies. Regulatory requirements for responsible forestry also increase compliance expenses for manufacturers. Companies are reducing exposure by diversifying supplier networks, expanding treated wood production, and developing alternative material blends to maintain pricing stability and operational continuity.

Opportunities are emerging through digital planning tools, modular decking systems, and high-performance wood technologies. Automated design platforms can reduce project planning time by nearly 25%, enabling contractors to deliver customized outdoor solutions faster. Japan and the United States are witnessing increased adoption of premium residential decking with integrated design services. Manufacturers are expanding research into weather-resistant coatings, prefabricated components, and recyclable materials. Strategic partnerships between timber producers, construction firms, and technology providers are creating new business models focused on efficiency, customization, and sustainable product development.

The industry faces execution challenges related to consistent timber availability, skilled labor shortages, and maintaining sustainable sourcing standards. Approximately 30% of construction companies report difficulties in managing material availability during large-scale projects. European markets face stricter forestry regulations, while emerging markets require stronger processing infrastructure. Companies must improve supply forecasting, invest in workforce training, and develop transparent sourcing systems. Long-term competitiveness depends on balancing production scalability with environmental compliance, operational reliability, and consistent product quality across diverse markets.

Sustainable Timber Certification Shift: Certified wood adoption is increasing as builders respond to stricter forestry standards and buyer preferences. More than 70% of premium decking projects now prioritize traceable materials, while companies in Canada and Germany are expanding certified supply partnerships to improve compliance, procurement reliability, and brand positioning.

Prefabrication and Modular Adoption: Modular wooden decking systems are changing installation workflows, reducing project timelines by nearly 25% and minimizing onsite labor requirements by 15%. Construction firms in the United States are adopting prefabricated components, while manufacturers are scaling automated cutting and assembly facilities to improve delivery speed.

Smart Coating Technology Growth: Advanced protective coatings are improving decking durability, with treated surfaces extending maintenance cycles by approximately 30% compared with traditional wood applications. Companies are investing in weather-resistant formulations and partnering with material technology providers to address moisture exposure, climate variability, and long-term performance requirements.

Digital Planning Integration: Digital visualization and design platforms are gaining traction among contractors, improving customer customization rates by nearly 20% and reducing design revisions. Australian and European suppliers are integrating digital tools into sales workflows, creating faster quotation processes and supporting personalized decking solutions for residential and commercial buyers.

Pressure-Treated Wood remains the dominant segment, accounting for approximately 45% of wooden decking demand due to its cost efficiency, durability improvements, and widespread availability across residential projects. Its resistance to decay and insects supports large-scale adoption in the United States and Canada, where renovation activity drives consistent consumption. Cedar and Redwood maintain strong positions in premium applications, capturing around 25% combined share through aesthetic appeal and natural resistance properties. Tropical Hardwood serves specialized luxury projects but faces supply limitations due to sustainability requirements.

Composite Wood is the fastest-growing segment, expanding through demand for low-maintenance alternatives and improved lifecycle value. Adoption is increasing by nearly 15% annually in premium outdoor applications as homeowners and developers prioritize reduced maintenance. Companies are increasing investment in hybrid materials, improved wood-plastic formulations, and sustainable production methods to compete with traditional timber solutions.

Residential Decks represent the leading application segment with nearly 50% market share, supported by home renovation projects, outdoor lifestyle upgrades, and property value improvement initiatives. The United States remains a major demand center, where homeowners increasingly invest in functional outdoor spaces. Commercial Spaces and Hospitality Areas contribute significant demand through hotels, restaurants, and mixed-use developments, while Outdoor Landscaping is becoming the fastest-growing application with adoption rising around 18% through urban beautification projects.

Public Spaces continue to develop through municipal landscaping programs and infrastructure improvements, although procurement cycles remain longer. Companies are adapting by offering customized decking solutions, installation services, and modular products that reduce construction complexity. The shift toward integrated outdoor design is creating stronger demand for suppliers capable of handling large-scale and specialized projects.

Homeowners represent the largest end-user group, contributing approximately 55% of wooden decking demand due to renovation spending, aesthetic upgrades, and outdoor space expansion. Residential buyers prioritize durability, appearance, and maintenance reduction, encouraging manufacturers to develop premium treated wood and customized decking options. Construction Companies and Real Estate Developers are increasing adoption as housing projects integrate outdoor amenities, with developer-led demand growing nearly 20% through premium residential developments.

The Hospitality Industry is emerging as a high-value end-user segment as hotels and resorts upgrade outdoor areas to enhance customer experiences. Landscaping Companies are also expanding usage through urban projects and commercial landscaping contracts. Companies are targeting these segments through contractor partnerships, bulk pricing strategies, and product customization programs to improve market penetration and strengthen long-term customer relationships.

North America accounted for the largest market share at 35% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Premium Renovation Demand and Sustainable Timber Transition

North America remains the largest wooden decking market, supported by strong residential renovation activity, outdoor living investments, and established timber processing infrastructure. The region contributes nearly 35% of global demand, with the United States representing the majority of regional consumption. Adoption is concentrated in suburban housing projects, hospitality upgrades, and premium landscaping applications. More than 60% of new decking installations emphasize durability-enhanced or certified wood solutions. Manufacturers are expanding local processing capacity and supplier networks to reduce logistics exposure after recent timber supply disruptions. Companies are also integrating automated cutting systems and digital design platforms to improve installation efficiency and customization capabilities.

United States Market Outlook: The United States dominates regional deployment through a mature remodeling ecosystem and strong contractor networks. Residential outdoor improvement projects represent a major demand source, with over 70% of decking buyers prioritizing low-maintenance and sustainable materials. Manufacturers are increasing treated wood production and expanding partnerships with construction companies to capture premium renovation demand.

Sustainable Forestry Standards Reshaping Product Strategies

Europe’s wooden decking market is influenced by strict sustainability regulations, certified timber adoption, and demand for environmentally responsible construction materials. Countries including Germany, Sweden, and France are driving adoption through green building initiatives and urban outdoor development projects. Nearly 70% of premium decking applications in Europe incorporate certified sourcing requirements, encouraging manufacturers to strengthen traceable supply chains. The region shows higher preference for durable wood treatments and lifecycle-focused solutions rather than low-cost alternatives. Companies are investing in sustainable forestry partnerships, advanced coatings, and regional manufacturing capabilities to comply with evolving environmental standards while maintaining product competitiveness.

Germany Market Outlook: Germany remains a strategic European market due to strong construction standards, sustainable building practices, and advanced timber processing capabilities. More than 60% of commercial construction projects emphasize environmentally compliant materials. Manufacturers are focusing on certified wood supply networks and precision processing technologies to meet demanding architectural requirements.

Manufacturing Expansion and Urban Outdoor Development

Asia-Pacific is emerging as the fastest-transforming wooden decking market due to rapid urban development, expanding hospitality infrastructure, and increasing residential improvement projects. China, Japan, Australia, and Southeast Asian countries are driving regional demand through construction modernization and outdoor lifestyle adoption. The region contributes nearly 25% of global consumption, while China remains a major manufacturing hub for processed wood products. Export-oriented suppliers are increasing production efficiency through automation, with advanced facilities improving processing output by approximately 20%. Companies are expanding partnerships with developers and landscaping firms to address growing demand for customized decking solutions.

China Market Outlook: China holds a significant position through large-scale wood processing capacity and strong manufacturing infrastructure. The country’s timber processing sector supports both domestic construction and export markets. Manufacturers are adopting automated production systems and improving supply-chain coordination to enhance efficiency and meet increasing demand from urban development projects.

Premium Wood Resources Supporting Export and Construction Demand

South America benefits from abundant forestry resources, expanding tourism infrastructure, and growing demand for premium outdoor spaces. Brazil and Chile are key contributors due to established timber industries and export capabilities. The region accounts for approximately 10% of global wooden decking consumption, with demand concentrated in residential developments, resorts, and landscaping projects. Sustainable forestry certification is becoming increasingly important, with exporters improving compliance systems to access international markets. Companies are investing in processing upgrades and strategic distribution partnerships to overcome transportation challenges and improve market reach across domestic and international customers.

Brazil Market Outlook: Brazil maintains a strong position through extensive forestry resources and established wood-processing operations. Certified timber production has expanded significantly, with more than 50% of export-focused producers adopting responsible forestry practices. Companies are improving processing technology and logistics networks to strengthen competitiveness in premium decking markets.

Hospitality Infrastructure and Luxury Development Expansion

The Middle East & Africa wooden decking market is shaped by hospitality projects, luxury residential developments, and large-scale urban modernization programs. Countries such as the UAE and Saudi Arabia are increasing demand through tourism infrastructure and premium outdoor construction. The region represents a smaller global share but demonstrates strong project-based opportunities, particularly in resorts and mixed-use developments. More than 40% of new premium outdoor projects incorporate customized decking solutions, encouraging suppliers to develop climate-resistant products. Companies are strengthening regional partnerships, improving distribution networks, and introducing treated wood solutions designed for challenging environmental conditions.

United Arab Emirates Market Outlook: The UAE is a leading regional market due to luxury hospitality expansion, high-end residential projects, and advanced construction activity. Developers increasingly integrate outdoor living areas into premium properties, with more than 30% of luxury projects including customized landscaping solutions. Suppliers are expanding local partnerships to improve project execution and delivery reliability.

The Wooden Decking Market features competition between global timber suppliers, premium decking brands, regional manufacturers, and specialized treatment providers. Companies such as major international wood producers compete with regional processors by balancing supply reliability, pricing, and sustainability credentials. The top five players collectively account for approximately 25–30% of market influence, reflecting a fragmented structure with strong local participation. Competition is driven by certified sourcing, product durability, customization, and installation efficiency, with advanced treatment solutions improving lifespan by nearly 30% and automation reducing production waste by around 15%. Leading companies are expanding through forestry partnerships, regional manufacturing hubs, and integrated supply chains. The market is shifting toward sustainable materials, traceable sourcing, and premium solutions as regulatory pressure increases. High-quality timber access and compliance capabilities remain major entry barriers. Winning players must combine supply control, innovation, and customer-focused solutions to outperform established competitors.

Trex Company

UPM-Kymmene Corporation

Weyerhaeuser Company

West Fraser Timber Co.

Boral Limited

Fiberon

Barrette Outdoor Living

Advantage Trim & Lumber Co.

Kebony

Dasso Group

Cali Bamboo

Thermory

MoistureShield

TimberTech

Technology adoption in the Wooden Decking Market is shifting toward advanced wood treatments, automated manufacturing, and digital planning platforms. Pressure-treatment innovations improve resistance against moisture and biological damage by nearly 30% compared with conventional untreated wood. Automated cutting and finishing systems reduce material waste by approximately 15%, helping manufacturers improve production consistency and operational efficiency. Leading suppliers are integrating these technologies to strengthen quality control and reduce dependency on manual processes.

Emerging solutions include AI-supported design visualization, modular decking systems, and enhanced protective coatings. Digital design tools improve project customization speed by nearly 20%, while modular components reduce installation time by around 25%. These technologies benefit manufacturers, contractors, and developers by enabling faster project execution and more predictable cost management.

Between 2026 and 2028, competitive advantage will increasingly depend on combining sustainable materials with intelligent production systems. Companies adopting automated workflows and data-driven inventory management will gain stronger supply-chain flexibility. New-generation decking technologies are positioning premium manufacturers ahead of traditional cost-focused suppliers by improving durability, customization, and lifecycle performance.

August 2025 Trex Company expanded its Western U.S. distribution partnership with International Wood Products, adding exclusive stocking through a new Salt Lake City facility and six distribution centers. The expansion strengthened regional availability and channel efficiency.

August 2024 Trex Company advanced its Little Rock, Arkansas manufacturing campus with a USD 400 million investment to increase production capability. The facility expansion supports supply reliability, regional manufacturing strength, and future decking demand with improved operational capacity.

June 2026 Trex Company released its sustainability report highlighting composite decking innovation using 95% recycled and reclaimed materials. The initiative reinforced circular manufacturing strategies and strengthened competitive positioning among environmentally focused outdoor living product suppliers.

October 2024 Trex Company reported progress on its Arkansas production facility, targeting completion with approximately USD 550 million capital expenditure. The expansion strategy improves manufacturing resilience and is designed to reduce logistics pressure through additional domestic production capability. Source: (Trex Company Inc – IR Site)

The Wooden Decking Market Report evaluates industry dynamics across key segments including Pressure-Treated Wood, Cedar, Redwood, Tropical Hardwood, and Composite Wood. The analysis covers applications such as residential decks, commercial spaces, hospitality areas, outdoor landscaping, and public infrastructure. It also examines end-user demand from homeowners, construction companies, real estate developers, hospitality operators, and landscaping firms.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing trends, sustainable sourcing practices, advanced treatment technologies, and digital construction adoption. Covering competitive strategies, supply-chain developments, and innovation priorities, the study supports investment planning, market expansion decisions, and positioning strategies for companies preparing for evolving decking demand through 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 45370 Million |

Market Revenue in 2033 | USD 58372.23 Million |

CAGR (2026 - 2033) | 3.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Trex Company, UPM-Kymmene Corporation, Weyerhaeuser Company, West Fraser Timber Co., Boral Limited, Fiberon, Barrette Outdoor Living, Advantage Trim & Lumber Co., Kebony, Dasso Group, Cali Bamboo, Thermory, MoistureShield, TimberTech |

Customization & Pricing | Available on Request (10% Customization is Free) |