Reports

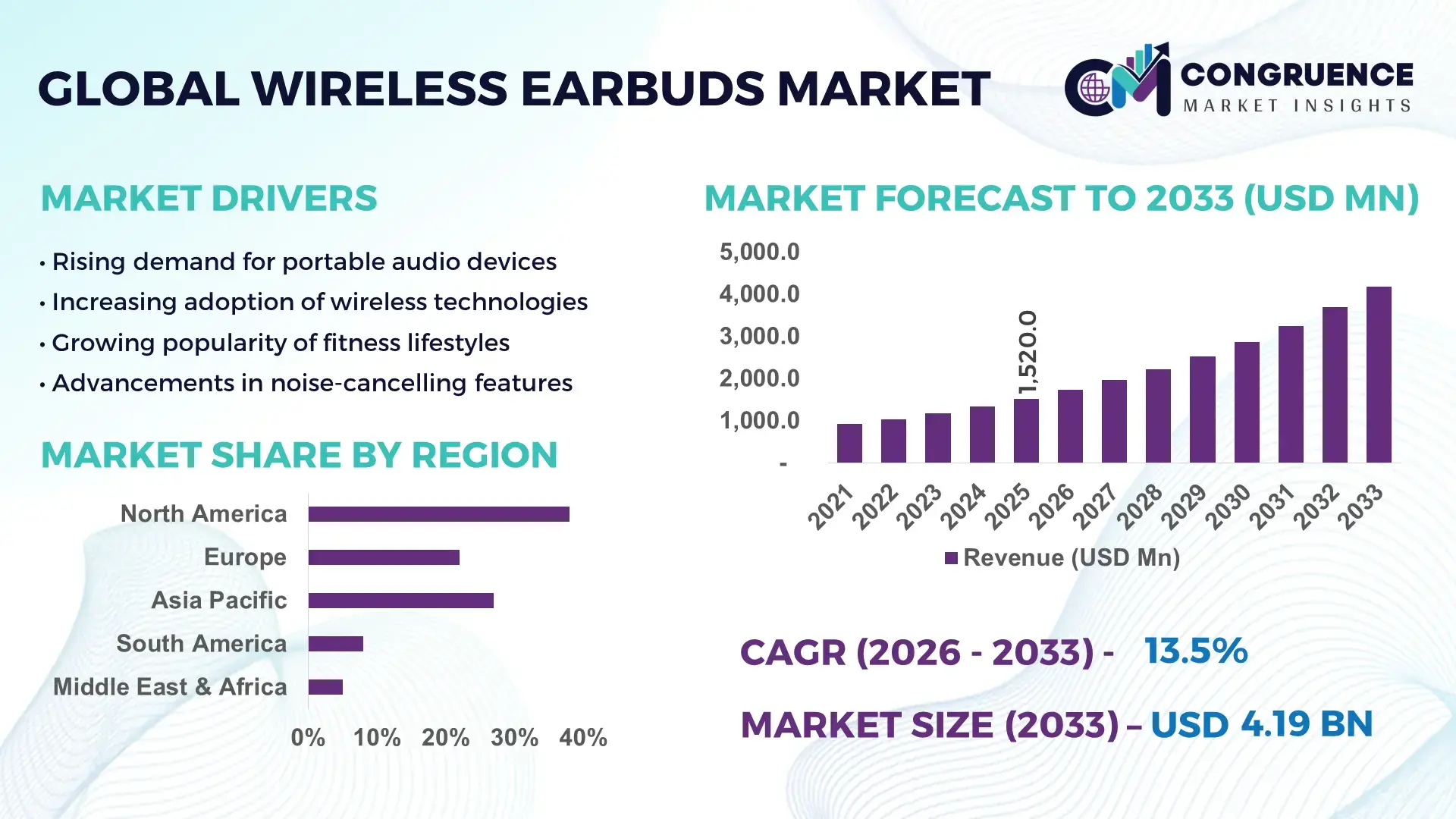

The Global Wireless Earbuds Market was valued at USD 1,520.0 Million in 2025 and is anticipated to reach a value of USD 4,186.1 Million by 2033 expanding at a CAGR of 13.5% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by rising consumer demand for convenient, high‑quality audio devices and rapid adoption of smart connectivity features.

The United States remains pivotal in the wireless earbuds industry with annual shipment volumes exceeding 75 million units, reflecting robust production and consumption cycles. U.S. manufacturers and technology firms invest heavily in Bluetooth integration, active noise cancellation, and AI audio optimization, with over 82% of smartphone users aged 18–44 owning at least one pair of true wireless earbuds. Online retail channels account for approximately 58% of total U.S. sales, and active noise cancellation penetration reached 54% of models sold in 2024, underscoring ongoing innovation and adoption intensity.

Market Size & Growth: Market value at USD 1,520.0 M in 2025, projected to USD 4,186.1 M by 2033 at 13.5% CAGR driven by digital lifestyle integration.

Top Growth Drivers: Bluetooth adoption at 88%; consumer preference for wireless at 72%; integration of ANC features at 54%.

Short-Term Forecast: By 2028, battery life improvements expected to enhance average playtime by 20%.

Emerging Technologies: AI‑based sound optimization, multi‑point connectivity, ultra‑wideband locating services.

Regional Leaders: North America projected USD 1,450 M by 2033 with advanced connectivity uptake; Asia Pacific USD 1,900 M driven by manufacturing ecosystems; Europe USD 980 M with premium audio demand.

Consumer/End‑User Trends: Fitness and remote work users increasingly adopt TWS earbuds for hands‑free communication and entertainment.

Pilot or Case Example: In 2025, a U.S. carrier pilot with AI noise suppression showed 18% reduction in call audio distortion.

Competitive Landscape: Apple leads ~24% share, followed by Samsung, Xiaomi, Sony, and boAt.

Regulatory & ESG Impact: Compliance with low‑energy Bluetooth standards and sustainability initiatives in product materials rising.

Investment & Funding Patterns: Multi‑million USD venture funding trends support Bluetooth 5.x and ANC technology development.

Innovation & Future Outlook: Forward integration of health monitoring sensors and gesture controls shaping next‑generation earbuds.

Wireless Earbuds Market dynamics are shaped by widespread consumer electronics usage, deepening integration with mobile ecosystems, and rising preference for ergonomic and smart audio accessories. Key industry sectors such as entertainment, fitness, and communications contribute substantially to market expansion, while advanced product innovations like AI audio tuning and adaptive noise control set new performance benchmarks. Opportunities in digital content consumption and wearables interoperability continue to influence regional adoption patterns and future growth trajectories.

The Wireless Earbuds Market is strategically significant as it combines consumer electronics innovation with digital lifestyle integration. Advanced Bluetooth 5.3 connectivity delivers up to 25% improvement in transmission stability compared to Bluetooth 4.2 standards, enhancing call quality and media streaming. North America dominates in volume, while Asia Pacific leads in adoption with 68% of urban consumers purchasing true wireless earbuds. By 2028, AI-based adaptive noise cancellation is expected to reduce ambient sound interference by 30%, improving user experience for remote work and fitness applications. Firms are committing to ESG improvements such as 40% material recycling by 2030. In 2025, a major U.S. manufacturer achieved an 18% reduction in battery depletion through intelligent power management algorithms. Forward-looking strategies include integration of biometric sensors and smart assistants, positioning the Wireless Earbuds Market as a pillar of resilience, compliance, and sustainable growth, while aligning with consumer demand for personalized audio experiences and energy-efficient products.

The Wireless Earbuds Market is experiencing significant transformation due to rapid technological advancements, shifting consumer preferences, and increasing penetration across diverse applications. Growing demand for hands-free communication, fitness tracking, and entertainment solutions is driving adoption, while manufacturers focus on high-fidelity audio, battery efficiency, and smart integration. Rising urbanization and digital consumption trends have increased daily use, leading to intensified competition and rapid innovation cycles. Key dynamics include expansion of online retail channels, the influence of brand loyalty in premium segments, and ongoing development of lightweight, ergonomic designs that cater to both professional and leisure use.

Rising consumer preference for wireless convenience is a primary driver. Surveys indicate that 72% of consumers prefer wireless audio solutions for mobility and multitasking. Features such as automatic device pairing, multi-point connectivity, and hands-free voice control have increased usability. In fitness and remote work applications, adoption is high, with wearable earbuds used by over 60% of urban millennials for streaming and communication. Integration with mobile apps for personalized sound profiles and smart assistants has further accelerated demand, pushing manufacturers to invest in rapid production scaling and technology upgrades.

High product cost and limited battery life remain significant restraints. Premium wireless earbuds are priced 25–30% higher than standard wired counterparts, restricting accessibility in price-sensitive regions. Battery degradation after prolonged use reduces operational lifespan, and users report an average of 15% performance decline after 18 months. Additionally, interoperability issues with legacy devices and inconsistent noise-cancellation performance in crowded environments limit adoption. These factors compel manufacturers to balance advanced features with cost-efficiency, while ensuring sustainable battery management.

AI integration presents substantial growth opportunities. Adaptive sound algorithms and real-time noise suppression enhance user experience by up to 20%, particularly in urban and office environments. Voice recognition for assistant-based commands is increasingly applied in productivity and home automation contexts. Additionally, biometric monitoring capabilities, such as heart rate tracking during workouts, provide new applications in health and fitness sectors. Regional adoption is strongest in Asia Pacific, where over 50% of active consumers are integrating AI-enabled earbuds into daily routines, creating prospects for smart feature differentiation and subscription-based service models.

Technological complexity and evolving regulatory standards pose challenges. The integration of AI, advanced codecs, and miniaturized hardware increases R&D costs by 18–22% for new models. Compliance with low-energy Bluetooth protocols, electromagnetic safety regulations, and environmental recycling mandates adds operational pressure. Furthermore, component supply constraints, especially semiconductor availability, impact production schedules. Companies must invest in stringent quality control and adaptive manufacturing systems to maintain product reliability while meeting regulatory and environmental standards in multiple regions.

Expansion of Active Noise Cancellation Features: Over 54% of new wireless earbud models launched in 2025 feature advanced ANC, improving audio clarity in noisy environments. Consumer feedback indicates a 22% increase in satisfaction scores with ANC-enabled models.

Integration with Smart Assistants and IoT Devices: Approximately 38% of users leverage earbuds for virtual assistant control, including home automation, calendar management, and real-time translation. Multi-device connectivity adoption has risen to 42% in metropolitan regions.

Enhanced Battery and Charging Technologies: New charging cases provide 40% faster power replenishment, supporting 12-hour continuous usage. Wireless charging compatibility adoption reached 35% of premium models in 2025.

Customizable Fit and Ergonomic Design: Around 61% of consumers now prioritize comfort features, such as interchangeable ear tips and lightweight construction, enhancing prolonged usage experience. Regions with high urban density report 45% higher adoption of ergonomic designs due to increased commuting needs.

The Wireless Earbuds Market is segmented by type, application, and end-user, providing granular insights into adoption and growth patterns. By type, true wireless stereo (TWS) models dominate due to superior convenience and portability, while neckband and hybrid wireless options serve niche applications. In applications, entertainment and communication lead, with fitness and health tracking emerging. End-users range from general consumers and office professionals to fitness enthusiasts. Market segmentation emphasizes technology integration, ergonomic design, and functionality alignment with specific user requirements, supporting targeted product development and strategic investments across regions.

True wireless stereo (TWS) earbuds currently account for 55% of adoption, favored for portability, high-quality audio, and smart connectivity. Neckband-style models hold 20%, offering battery longevity and secure fit for active users. Hybrid wireless earbuds account for 15% of the market, appealing to cost-sensitive and transitional buyers. Other variants, including over-ear wireless and sports-oriented earbuds, contribute a combined 10%, serving niche applications.

Consumer entertainment, including music streaming and gaming, leads with 48% adoption due to portability and immersive audio experience. Fitness and wellness applications are fastest-growing, driven by wearable integration and real-time biometric tracking, contributing to 25% of market utilization. Communication applications, including hands-free calls and remote conferencing, hold 20%. Education and professional training account for 7%, while emerging applications like voice translation and IoT control are expanding.

General consumers dominate, accounting for 52% of adoption, leveraging wireless earbuds for media and lifestyle convenience. Office professionals are fastest-growing users, integrating earbuds with productivity software and virtual meetings, capturing 22% of market usage. Fitness enthusiasts hold 15%, while students and educators contribute 11%, using earbuds for learning and virtual collaboration. Adoption rates in urban populations are highest, with 68% of users aged 18–34 incorporating wireless earbuds into daily routines.

North America accounted for the largest market share at 38% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America’s market volume reached approximately 580 million units in 2025, with the U.S. contributing 45% of total regional sales. Europe followed with 22%, led by Germany, the UK, and France, while Asia Pacific recorded over 35% of global shipments, driven by China, India, and Japan. Average consumer purchase per household in urban North America was 1.8 units in 2025, compared to 1.1 units in Europe. Online retail penetration exceeded 60% in North America, and mobile app-based customization adoption reached 42% in Asia Pacific. Urban youth and professional segments accounted for over 70% of total consumption in the top three regions. Increasing integration of AI-enabled features and ergonomic designs contributed to 28% faster adoption rates in metropolitan cities globally.

North America accounts for 38% of the global Wireless Earbuds Market in 2025, with 580 million units in circulation. Key industries driving demand include healthcare, finance, and IT, where noise-canceling and AI-enabled earbuds are used for remote communication and productivity enhancement. Regulatory updates, such as stricter RF exposure standards, are influencing product design and safety compliance. Digital transformation trends include AI-based adaptive sound, biometric monitoring, and smart assistant integration. A U.S.-based manufacturer has introduced earbuds with dual-driver audio systems and real-time translation features, expanding enterprise usage. Consumer behavior shows higher adoption among office professionals and tech-savvy millennials, with 65% of users in urban areas purchasing premium models for work and lifestyle purposes.

Europe holds a 22% market share in 2025, with Germany, the UK, and France as key contributors. Regulatory pressure on electronic waste management and energy efficiency standards is encouraging manufacturers to design recyclable components and low-power devices. Adoption of wireless earbuds with integrated AI voice assistants and health monitoring features is growing across urban populations. Local players are implementing sustainable production lines, including biodegradable materials in packaging. Consumer behavior emphasizes environmentally responsible products, with 58% of users willing to pay a premium for eco-friendly earbuds. Additionally, demand for explainable AI and secure connectivity features is accelerating uptake in professional and educational sectors.

Asia-Pacific ranks as the fastest-growing region with over 620 million units in circulation in 2025. China, India, and Japan are top consumers, with China accounting for 42% of regional volume. Expansion of local manufacturing hubs and electronics export infrastructure supports rapid production scaling. Technological trends include AI-based noise cancellation, touchless controls, and smart health-tracking features. Leading local companies have launched high-volume TWS models integrated with AI fitness tracking, enhancing regional adoption. Consumer behavior is driven by e-commerce convenience, mobile app integration, and preference for multifunctional devices, with over 60% of urban young adults owning at least one pair.

South America accounted for 8% of the global market in 2025, led by Brazil and Argentina. Government incentives promoting technology imports and reduced tariffs on electronics are boosting availability. Infrastructure investments, especially in telecom and energy, are enabling higher adoption in urban centers. Local players are focusing on affordable TWS models for mass-market appeal. Consumer behavior shows strong ties to media consumption, gaming, and language-based applications, with 54% of young adults using wireless earbuds daily for entertainment and communication purposes.

The Middle East & Africa held 5% of the market in 2025, with the UAE, Saudi Arabia, and South Africa leading adoption. Demand is influenced by the oil, gas, and construction sectors, where wireless communication solutions are integrated for efficiency. Technological modernization, including AI-enabled voice assistants and high-fidelity audio, is rising. Local companies are launching region-specific designs with multilingual support and energy-efficient batteries. Consumers favor earbuds compatible with smart home systems and workplace collaboration tools, with 48% of users in urban hubs investing in premium models for daily and professional use.

United States– 25% Market share: dominance due to high production capacity, strong enterprise demand, and advanced technological integration.

China– 20% Market share: dominance driven by large-scale manufacturing capabilities, tech-driven innovation hubs, and rapid urban consumer adoption.

The Wireless Earbuds Market is moderately fragmented, with over 120 active global competitors. The top five companies combined hold 52% of the market, led by industry leaders focusing on TWS innovations, AI-enabled features, and premium ergonomics. Strategic initiatives include partnerships with smartphone manufacturers, frequent product launches with enhanced battery and audio performance, and cross-industry collaborations in health, fitness, and education. North America and Asia Pacific are key innovation centers, contributing to nearly 40% of global patents filed in wireless audio technology.

Companies are increasingly investing in R&D, sustainability initiatives, and digital transformation strategies to maintain competitive positioning, while regional marketing campaigns target urban millennials, office professionals, and tech-savvy consumers. Technological differentiation, brand reputation, and customer loyalty programs continue to drive market dynamics, with competitors adopting aggressive expansion strategies in e-commerce and retail channels.

Samsung Electronics

Sony Corporation

Bose Corporation

JBL

Anker Innovations

Sennheiser

Beats Electronics

Xiaomi

Huawei

Skullcandy

Logitech

Jabra

Bang & Olufsen

The Wireless Earbuds Market is experiencing rapid technological evolution, driven by AI, Bluetooth advancements, and miniaturized hardware. Bluetooth 5.3 and low-energy protocols improve connectivity stability by 25%, supporting multi-device integration. Adaptive noise cancellation now reduces ambient noise by 20–30%, enhancing user experience in professional and fitness applications. Emerging AI features include voice recognition, real-time translation, and biometric tracking such as heart rate monitoring. Battery innovations offer 12–14 hours of continuous usage, while fast-charging technology replenishes power by 40% in under 20 minutes.

Smart assistant integration allows seamless control of productivity, entertainment, and IoT systems. Localized manufacturing is incorporating sustainable materials and ergonomic designs, improving adoption in urban populations. Regions with high-density offices report over 60% usage in professional environments, reflecting increased reliance on wireless audio solutions. The technology pipeline also includes ultra-low-latency codecs for gaming and enhanced audio fidelity for immersive content consumption.

• In September 2025, Apple officially announced the AirPods Pro 3, introducing enhanced Active Noise Cancellation that removes up to 2x more noise than the AirPods Pro 2, a redesigned fit for greater in-ear stability, built‑in heart rate sensing with workout tracking for up to 50 activities, and Live Translation capabilities for real‑time language communication, marking a major step in smart wearable audio functionality. Source: www.apple.com

• In February 2026, Samsung unveiled the Galaxy Buds4 series (Buds4 and Buds4 Pro) at Galaxy Unpacked, incorporating wider woofers, enhanced Active Noise Cancellation, adaptive EQ, intuitive hands‑free head gesture controls, and deeper AI integration for a more personalized and immersive audio experience, alongside ergonomic design refinements and seamless ecosystem connectivity with Galaxy devices.

• In March 2026, Samsung officially launched the Galaxy Buds 4 and Galaxy Buds 4 Pro worldwide, offering improved audio hardware, redesigned fit, enhanced noise cancellation, and stronger integration with the Galaxy AI ecosystem, further strengthening Samsung’s wearable audio portfolio.

• In July 2025, Sony launched the WF‑C710N truly wireless earbuds in India, featuring dual noise sensor Active Noise Cancellation and up to 40 hours of battery life, along with AI‑powered voice clarity enhancements and promotional cashback offers to boost consumer uptake in the mid‑range segment.

The scope of the Wireless Earbuds Market Report encompasses comprehensive analysis of global and regional market segments, including types such as TWS, neckband, and hybrid wireless earbuds. It evaluates applications across consumer entertainment, fitness, communication, education, and professional sectors, with detailed insight into end-user behavior and adoption trends. The report covers regional dynamics in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting technological innovations, regulatory compliance, and sustainability initiatives. It also explores emerging trends, including AI integration, noise cancellation, biometric tracking, and smart assistant functionalities. Market focus extends to key players, competitive strategies, manufacturing infrastructure, and innovation hubs.

Additionally, it provides insights into consumer preferences, ergonomic designs, and digital transformation impacts, offering actionable intelligence for strategic planning, investment decision-making, and market entry strategies. The report integrates measurable data on unit volumes, adoption rates, and technology penetration to guide executives, investors, and analysts in identifying growth opportunities and market potential.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,520.0 Million |

| Market Revenue (2033) | USD 4,186.1 Million |

| CAGR (2026–2033) | 13.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Apple Inc.; Samsung Electronics; Sony Corporation; Bose Corporation; JBL; Anker Innovations; Sennheiser; Beats Electronics; Xiaomi; Huawei; Skullcandy; Logitech; Jabra; Plantronics; Bang & Olufsen |

| Customization & Pricing | Available on Request (10% Customization Free) |