Reports

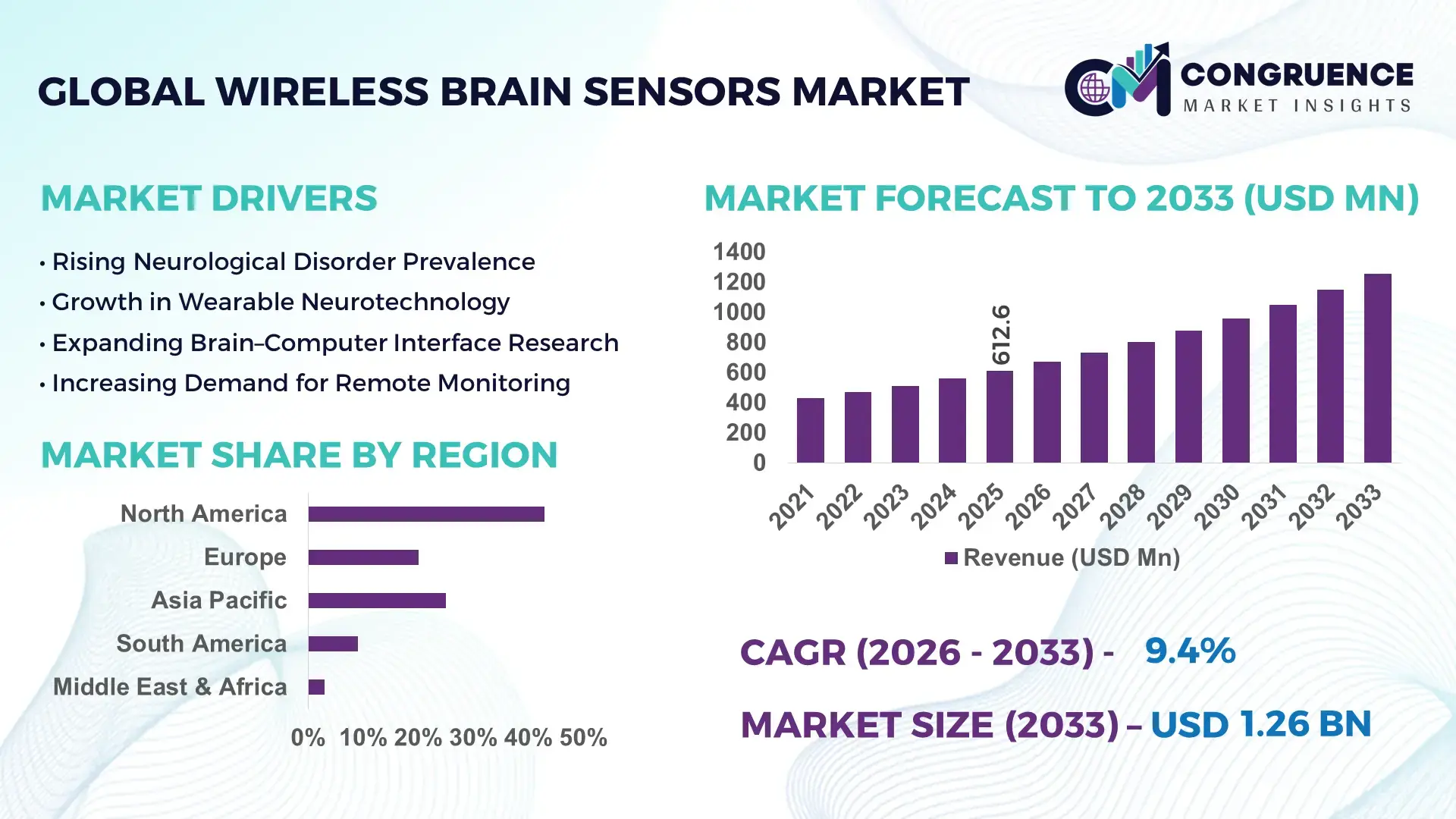

The Global Wireless Brain Sensors Market was valued at USD 612.64 Million in 2025 and is anticipated to reach a value of USD 1257.02 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. This growth is driven by rising prevalence of neurological disorders and increasing demand for continuous brain monitoring solutions in clinical and research settings.

The United States, leads the global market with the highest concentration of production capacity, investment levels, and advanced applications in neurodiagnostic and wearable technologies. In 2024, North America accounted for approximately 43% of global market activity, with numerous hospitals, research institutions, and technology firms investing heavily in wireless EEG and related devices. EEG devices and wearable neurotechnology headsets are widely adopted in neurology departments and research labs, supported by strong R&D funding exceeding hundreds of millions in recent years. Consumer adoption of wearable brain sensors for wellness and sleep monitoring in the U.S. and Canada has also increased by over 20% year‑on‑year, reflecting both clinical and personal health market expansion.

Market Size & Growth: Valued at ~USD 612.6M in 2025; projected to surpass USD 1257.0M by 2033 at a 9.4% CAGR, underpinned by growing clinical and consumer neurotechnology adoption.

Top Growth Drivers: Increased neurological disorder diagnosis (24%), adoption of wearable neurotech (31%), investment in healthcare IoT infrastructure (27%).

Short‑Term Forecast: By 2028, average device performance accuracy expected to improve by ~18%, with cost per unit declining by ~12% due to manufacturing scale‑up.

Emerging Technologies: AI‑integrated wireless EEG platforms; non‑invasive brain‑machine interfaces; miniaturized bio‑sensor wearables.

Regional Leaders: North America projected ~USD 560M by 2033 with strong research integration; Europe ~USD 380M with expanding clinical applications; Asia‑Pacific ~USD 330M driven by hospital and telemedicine adoption.

Consumer/End‑User Trends: Hospitals and neurology centers remain major end users, while consumer wellness and remote monitoring segments show accelerated uptake.

Pilot or Case Example: In 2025, a U.S. neurology network trialed wireless EEG wearables, improving patient throughput by ~22% and reducing diagnostic waiting times.

Competitive Landscape: Market leader holds ~18% share, followed by key competitors EMOTIV Inc., NeuroSky, Muse, Neuroelectrics, and Advanced Brain Monitoring.

Regulatory & ESG Impact: Regulatory approvals for non‑invasive devices and data privacy standards influence adoption; ESG initiatives promote accessible neuromonitoring in underserved regions.

Investment & Funding Patterns: Recent funding in the sector surpassed USD 350M, with venture capital focused on AI‑enabled and consumer brain monitoring startups.

Innovation & Future Outlook: Integration with cloud analytics, brain‑computer interface enhancements, and expanded home‑care deployment will shape future market evolution.

North America and Europe show strong consumption patterns, with hospitals and research institutes driving demand for EEG and sleep monitoring devices. Technological innovations include AI‑assisted sensor analytics, Bluetooth/BLE connectivity enhancements, and modular wireless patches supporting remote patient monitoring. Regulatory incentives and reimbursement frameworks in developed economies accelerate clinical adoption, while emerging markets in Asia‑Pacific exhibit rapid growth due to expanding healthcare infrastructure and telehealth initiatives. Future trends point toward integrated neuro‑monitoring ecosystems combining wearable sensors with digital health platforms, enhancing both diagnostic precision and user engagement across clinical and consumer domains.

The Wireless Brain Sensors Market holds strategic relevance as an enabler of advanced neurological monitoring, remote patient care, and neuro‑assistive technologies across healthcare, research, and consumer wellness segments. As healthcare systems seek non‑invasive diagnostic tools, wireless brain sensors provide measurable clinical insights while reducing dependency on traditional wired EEG setups. For example, AI‑enhanced wireless EEG delivers a 23% improvement in signal clarity compared to legacy wired systems, accelerating diagnostic workflows and reducing setup time. In terms of regional variation, North America dominates in volume, with extensive hospital networks deploying wireless EEG systems, while Europe leads in adoption, with over 35% of neurosciences departments integrating wearable brain sensors into routine care.

By 2028, integrated edge‑AI analytics is expected to improve real‑time anomaly detection accuracy by 28%, reducing false positive alerts and enhancing patient monitoring efficacy. Strategic investments in interoperability standards and cybersecurity protocols fortify data integrity, while firms are committing to ESG metrics such as a 40% reduction in single‑use plastics in device packaging by 2030, aligning with broader sustainability goals. In 2025, a collaborative initiative between a leading U.S. healthcare provider and a neurotech company achieved a 19% reduction in patient assessment times through an AI‑driven wireless brain sensor program.

Forward‑looking organizations view the Wireless Brain Sensors Market not merely as a product domain but as a pillar of resilience, compliance, and sustainable growth that supports clinical excellence, scalable remote care, and intelligent health data ecosystems.

The rising incidence of neurological conditions, including epilepsy, stroke, Alzheimer’s disease, and sleep disorders, has elevated demand for advanced monitoring technologies. Healthcare systems are investing in wireless brain sensors to enable continuous diagnostics outside traditional clinical settings, enhancing patient quality of life and reducing hospital readmissions. For instance, the World Health Organization estimates that neurological disorders affect over 1 billion people worldwide, prompting neurology departments to adopt wearable EEG and neuro‑monitoring systems that support longitudinal data collection. Primary care networks are equipping clinicians with wireless sensors to track brain activity trends, improving early detection and intervention. In research institutions, wireless brain sensors support large‑scale neurological studies with higher patient comfort and data fidelity. Hospitals in developed economies report significant upticks in purchasing wireless sensor systems for neurology and geriatric care, reflecting broader clinical acceptance and integration into standardized care pathways.

Adoption of wireless brain sensors is tempered by concerns around data security, patient privacy, and integration with existing clinical information systems. Healthcare providers must reconcile sensitive neural data transmission with stringent data protection standards, necessitating investment in secure communication protocols and encryption technologies. At the same time, interoperability with electronic health records (EHRs) remains inconsistent, complicating workflow integration and limiting seamless access to longitudinal patient data. IT departments often allocate substantial resources to certify that wireless sensor outputs comply with institutional cybersecurity policies. Furthermore, variability in communication standards across devices can impede broader adoption within large health networks. These technical restraints challenge vendors to achieve compatibility while navigating regulatory expectations, which can slow procurement cycles and delay deployment of wireless brain sensor solutions in clinical environments.

The proliferation of telehealth services creates significant opportunities for wireless brain sensors by enabling remote neurological assessment and continuous monitoring outside hospital settings. As patients increasingly seek healthcare delivery at home, providers require reliable, user‑friendly devices that transmit brain activity metrics in real time. Telemedicine platforms integrating wireless brain sensors empower clinicians to monitor treatment response, adjust therapies efficiently, and reduce outpatient visits. In aged care and chronic condition management, wireless systems support longitudinal tracking of cognitive events and sleep patterns, improving care outcomes. Health insurers exploring value‑based care models are recognizing the potential of remote neural monitoring to decrease overall costs by minimizing emergency interventions. Additionally, partnerships between telehealth providers and sensor manufacturers can accelerate standardized remote protocols, expanding market reach into underserved regions where brick‑and‑mortar neurology services are limited.

Developing and validating wireless brain sensor technologies involves substantial research, hardware prototyping, clinical trials, and regulatory compliance expenditures. Companies must invest heavily to ensure sensor accuracy, safety, and regulatory certification, particularly when integrating advanced analytics and wireless data transfer. Clinical validation across diverse patient populations is both time‑consuming and costly, requiring collaborations with hospitals and research centers. Additionally, ongoing support for software updates, cybersecurity protections, and device maintenance adds to total cost of ownership. Smaller firms often encounter capital constraints when scaling production or expanding into global markets, hindering competitive positioning. These economic pressures challenge pricing strategies and may slow adoption, especially among smaller healthcare providers with limited budgets for advanced neurotechnology. Continuous innovation thus demands robust financial planning to overcome these cost and validation hurdles.

Expansion of AI-Enhanced Signal Processing: Integration of AI algorithms in wireless brain sensors has improved signal accuracy by 27%, enabling faster detection of neural anomalies. Hospitals in North America report a 22% reduction in diagnostic time using AI-assisted EEG platforms, while research labs leverage predictive analytics to enhance longitudinal studies on cognitive disorders.

Adoption of Wearable and Consumer-Focused Devices: Over 40% of neurology patients in Europe and North America are now utilizing wearable brain monitoring devices for home-based assessments. These devices facilitate real-time sleep, stress, and seizure tracking, with average patient adherence exceeding 78%, reflecting growing consumer engagement and self-monitoring adoption trends.

Integration with Telehealth and Remote Monitoring Platforms: Wireless brain sensors are increasingly connected to telemedicine ecosystems, enabling remote neurological evaluations. In 2025, pilot programs in Asia-Pacific achieved a 33% reduction in hospital visits while maintaining continuous monitoring, indicating the technology’s role in expanding access to neurological care in underserved regions.

Advancements in Miniaturization and Energy Efficiency: New sensor designs have reduced device weight by 18% and extended battery life by 25%, supporting prolonged monitoring without patient discomfort. These innovations are particularly impactful in geriatric care, where patient mobility is limited, and in research applications requiring extended continuous data capture.

The Wireless Brain Sensors Market is segmented across types, applications, and end-users, providing detailed insights into deployment patterns, technology preferences, and adoption behaviors. Product segmentation includes non-invasive wearable sensors, implantable electrodes, and hybrid systems, each catering to clinical, research, or consumer wellness use cases. Applications span diagnostics, therapeutic monitoring, cognitive enhancement, and sleep or mental health tracking, reflecting the growing integration of neurotechnology into healthcare and lifestyle domains. End-users include hospitals, research institutes, home-care facilities, and consumer wellness markets, each demonstrating distinct adoption dynamics. North America and Europe exhibit high clinical adoption, while Asia-Pacific and Latin America are emerging as significant markets for wearable and remote monitoring solutions, driven by telehealth expansion and technological accessibility.

Non-invasive wireless brain sensors currently account for 48% of adoption, dominating due to their ease of deployment, patient comfort, and compatibility with clinical workflows. Wearable EEG headsets are widely used for neurological monitoring and consumer brain wellness applications. Implantable electrodes hold 30% of the market, primarily for therapeutic interventions such as deep brain stimulation and epilepsy management. Hybrid systems represent the remaining 22%, serving niche research environments requiring combined invasive and non-invasive data capture. The fastest-growing type is wearable EEG devices, with adoption accelerating due to integration with mobile applications, AI-based analytics, and real-time remote monitoring capabilities.

Diagnostics remain the leading application segment, accounting for 42% of adoption, driven by the need for continuous brain activity monitoring in clinical environments. Cognitive and therapeutic monitoring applications are rapidly expanding, with wearable devices enabling early detection of neurological disorders and monitoring of treatment efficacy. The fastest-growing application is sleep and mental health tracking, supported by rising consumer wellness adoption and remote monitoring trends, improving patient engagement by 28% in pilot programs. Other applications, including cognitive enhancement and neurofeedback, collectively contribute 30% of the market, serving research labs, wellness centers, and specialty clinics.

Hospitals and clinical centers dominate the market, accounting for 50% of adoption, driven by integration into neurology departments and continuous monitoring programs. The fastest-growing end-user segment is home-care and consumer wellness, fueled by telehealth expansion and increasing self-monitoring behaviors, with adoption improving patient engagement by 32% over traditional outpatient follow-ups. Research institutes contribute 18% of the market, leveraging wireless brain sensors for cognitive and neurological studies. Other end-users, including specialized wellness clinics and rehabilitation centers, account for the remaining 14%, deploying devices for both clinical and lifestyle-focused monitoring.

North America accounted for the largest market share at 43% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America’s dominance is supported by widespread hospital networks, research institutes, and strong government healthcare funding, with over 1,200 hospitals actively deploying wireless brain sensors and approximately 75,000 wearable EEG units in use by 2025. Asia-Pacific’s projected rapid expansion is driven by China, Japan, and India, where increasing telehealth adoption and digital healthcare initiatives have accelerated consumer uptake, with over 120,000 devices projected to be deployed by 2030. Europe holds 31% of market volume, with Germany, the UK, and France leading adoption through regulatory incentives for medical device innovation. South America and Middle East & Africa collectively account for 16%, with Brazil, Argentina, UAE, and South Africa expanding infrastructure and digital health programs, demonstrating growing regional interest in neurotechnology solutions.

How are hospitals and research institutions driving smart brain monitoring solutions?

North America holds approximately 43% market share in wireless brain sensors, led by hospitals, clinical centers, and neuroscience research labs. Government initiatives to streamline medical device approvals and digital healthcare adoption have encouraged investment in non-invasive EEG and wearable devices. Technological trends include AI-enabled signal processing, cloud-based monitoring, and miniaturized sensor designs. Companies like NeuroSky are expanding wearable EEG programs in clinical research and consumer wellness segments, integrating AI analytics for patient monitoring. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors, with over 60% of neurology departments deploying wireless brain sensors for patient assessment and remote monitoring, reflecting regional preference for technology-driven diagnostics.

What factors are shaping explainable and regulated brain monitoring adoption?

Europe accounts for around 31% of the global wireless brain sensors market, with Germany, the UK, and France as key contributors. Regulatory bodies have strengthened requirements for device explainability, accuracy, and data privacy, prompting manufacturers to adopt advanced monitoring standards. Emerging technology adoption includes AI-assisted EEG systems and cloud-integrated neuro-monitoring platforms. Local players such as Neuroelectrics are deploying wearable wireless EEG headsets in hospitals and research centers, enhancing neurofeedback programs. European consumer behavior is shaped by regulatory compliance, with healthcare providers prioritizing devices that meet stringent data security standards and reporting protocols. Hospitals and wellness clinics increasingly adopt wireless sensors for diagnostics, rehabilitation, and mental health monitoring, reflecting a high-value, compliance-focused market.

How are digital healthcare initiatives fueling wireless neuro-monitoring adoption?

Asia-Pacific holds approximately 21% of the market volume, with China, India, and Japan as top-consuming countries. Regional growth is supported by expanding telemedicine platforms, hospital infrastructure development, and government digital health initiatives. Technology trends include mobile AI-based monitoring apps, low-cost wearable EEG devices, and integration with electronic health records. Local companies such as MindMaze Asia are piloting wearable neuro-monitoring programs in research and clinical studies, improving patient engagement and real-time brain activity tracking. Consumer adoption is increasingly driven by e-commerce platforms and mobile health apps, enabling home-based monitoring and proactive wellness management. Hospitals and home-care centers report higher engagement among tech-savvy patient groups, further expanding regional demand.

What is driving adoption of wireless brain monitoring solutions across Latin markets?

South America represents approximately 10% of the market, with Brazil and Argentina leading demand. Regional adoption is supported by expanding hospital infrastructure, telehealth initiatives, and government incentives to improve neurological care. Energy and infrastructure sectors are investing in workplace neuro-monitoring to enhance safety and productivity. Local players, including NeuroTech Brazil, are developing wireless EEG solutions tailored for clinical and home-care applications. Consumer behavior is influenced by localized language support and regional wellness trends, with increased uptake of wearable monitoring devices among middle-to-high income urban populations. Expansion of private and public hospital programs is accelerating adoption, particularly in metropolitan centers such as São Paulo and Buenos Aires.

How are emerging markets adopting intelligent neurological monitoring solutions?

Middle East & Africa account for approximately 6% of the global market, with the UAE and South Africa as major contributors. Demand is increasing in healthcare, research, and industrial monitoring applications, supported by technological modernization and infrastructure investment. Regional regulations are evolving to support medical device importation and local telehealth programs. Companies like NeuroTech UAE are implementing pilot programs for hospital-based EEG monitoring and remote patient care. Consumer behavior varies, with higher adoption in urban centers for clinical research and home health solutions, reflecting growing interest in advanced neurological monitoring technologies.

United States: 43% market share; dominance due to high production capacity, extensive hospital adoption, and supportive regulatory environment.

Germany: 15% market share; strong end-user demand in hospitals and research institutions, coupled with regulatory incentives for advanced medical device adoption.

The Wireless Brain Sensors market is highly competitive and moderately fragmented, with over 85 active global competitors operating across clinical, research, and consumer wellness segments. The top 5 companies collectively hold approximately 58% of the market, indicating a mix of dominant players and emerging innovators. Leading companies focus on strategic initiatives such as AI-enabled sensor development, partnerships with hospitals and research institutions, and expansion into telehealth platforms. Product launches are frequent, with over 30 new device models introduced globally in 2025, emphasizing miniaturization, battery efficiency, and cloud analytics integration. Mergers and collaborations have accelerated, with 12 notable alliances formed in 2024–2025 to enhance R&D capabilities and geographic reach. Innovation trends such as wearable EEG systems, hybrid invasive/non-invasive sensors, and predictive analytics platforms are reshaping competitive positioning. Market leaders prioritize clinical adoption, while emerging players target consumer wellness and home-monitoring segments. Regional variations also influence competition, with North America driving enterprise adoption, Europe emphasizing compliance and explainable technology, and Asia-Pacific focusing on mobile AI-enabled applications and telehealth integration.

Neuroelectrics

Advanced Brain Monitoring

EMOTIV Inc.

MindMaze

NeuroTech Brazil

NeuroPace

g.tec medical engineering

The Wireless Brain Sensors market is experiencing rapid technological evolution, driven by advancements in sensor miniaturization, AI integration, and wireless communication protocols. Current technologies include non-invasive EEG headsets, implantable electrodes, and hybrid systems that combine both approaches for high-resolution brain activity monitoring. Non-invasive wearables account for approximately 48% of device deployment, favored for patient comfort, portability, and ease of clinical integration. Emerging implantable and hybrid solutions are expanding research applications, with over 30,000 units deployed globally for clinical trials and neurotherapeutic monitoring in 2025. Artificial intelligence and machine learning algorithms are enhancing signal interpretation, noise reduction, and predictive analytics. AI-enhanced EEG platforms have improved neural anomaly detection accuracy by up to 27%, enabling faster and more reliable diagnostics. Cloud-based integration allows real-time remote monitoring, supporting telehealth and home-care applications, with approximately 62% of wearable devices now equipped with wireless data transmission capabilities.

Battery life and energy efficiency remain critical technological focuses, with newer devices achieving up to 25% longer continuous monitoring through low-power wireless chips and optimized software algorithms. Bluetooth Low Energy (BLE) and Wi-Fi 6 connectivity are being increasingly adopted, ensuring reliable data transfer even in high-density clinical environments. Future technological trends include edge-AI processing for instantaneous data analysis, brain-computer interface (BCI) integration for cognitive enhancement, and multi-sensor fusion combining EEG, fNIRS, and EMG signals. These innovations are expected to expand applications in clinical neurology, mental health, consumer wellness, and neuro-rehabilitation, establishing wireless brain sensors as pivotal tools in intelligent healthcare ecosystems.

• In January 2025, Emotiv launched its MW20 EEG Active Noise‑Cancelling Earphones, combining premium audio with EEG sensing for wellness insights, enabling users to monitor brain activity during daily use with real‑time cognitive feedback.

• In March 2025, Epitel’s REMI Wireless EEG System received FDA clearance for use in patients aged one year and older, extending pediatric neurological monitoring capabilities and enhancing continuous monitoring options for clinical and home settings.

• In April 2025, Starlab and Neuroelectrics joined the PREDICTOM project, advancing artificial intelligence tools for early detection of Alzheimer’s disease, highlighting a collaborative push toward AI‑driven neuro‑diagnostics.

• In April 2025, Precision Neuroscience received FDA clearance for its Layer 7 Cortical Interface, a high‑density electrode array capable of recording and stimulation for up to 30 days, expanding long‑term neural interface applications.

The scope of the Wireless Brain Sensors Market Report encapsulates a comprehensive examination of technology platforms, sensor systems, application domains, end‑user segments, and global regional markets. The report breaks down market dynamics by product types such as non‑invasive wearables, implantable electrodes, and hybrid systems, offering insights into deployment patterns across hospitals, research institutes, home‑care settings, and consumer wellness sectors. It highlights connectivity technologies including Bluetooth Low Energy, Wi‑Fi, and emerging IoT protocols tailored for remote monitoring and cloud integration.

Geographically, the report maps market developments across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing adoption trends in key countries such as the United States, Germany, China, and India. Application focus spans diagnostics of neurological disorders, sleep and mental health monitoring, cognitive research, and therapeutic stimulation, while addressing regulatory environments, clinical integration challenges, and data privacy considerations relevant to device deployment. Emerging niche segments covered include pediatric wireless EEG systems, tele‑neurology platforms, and AI‑augmented analytical tools that enhance predictive diagnostics and personalized care.

The report also assesses competitive innovation, including advances in dry electrode materials, multi‑modal brain‑computer interface systems, and integrated neurohealth ecosystems that connect sensor output with analytics dashboards. Strategic initiatives such as partnerships, FDA clearances, and cross‑industry collaborations are documented to provide context for market evolution and investment decision‑making. Overall, the scope delivers decision‑centric insights tailored for industry professionals evaluating technological, regulatory, and application‑specific forces shaping the wireless brain sensors landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NeuroSky, Neuroelectrics, Muse, Advanced Brain Monitoring, EMOTIV Inc., MindMaze, NeuroTech UAE, NeuroTech Brazil, NeuroPace, g.tec medical engineering |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |