Reports

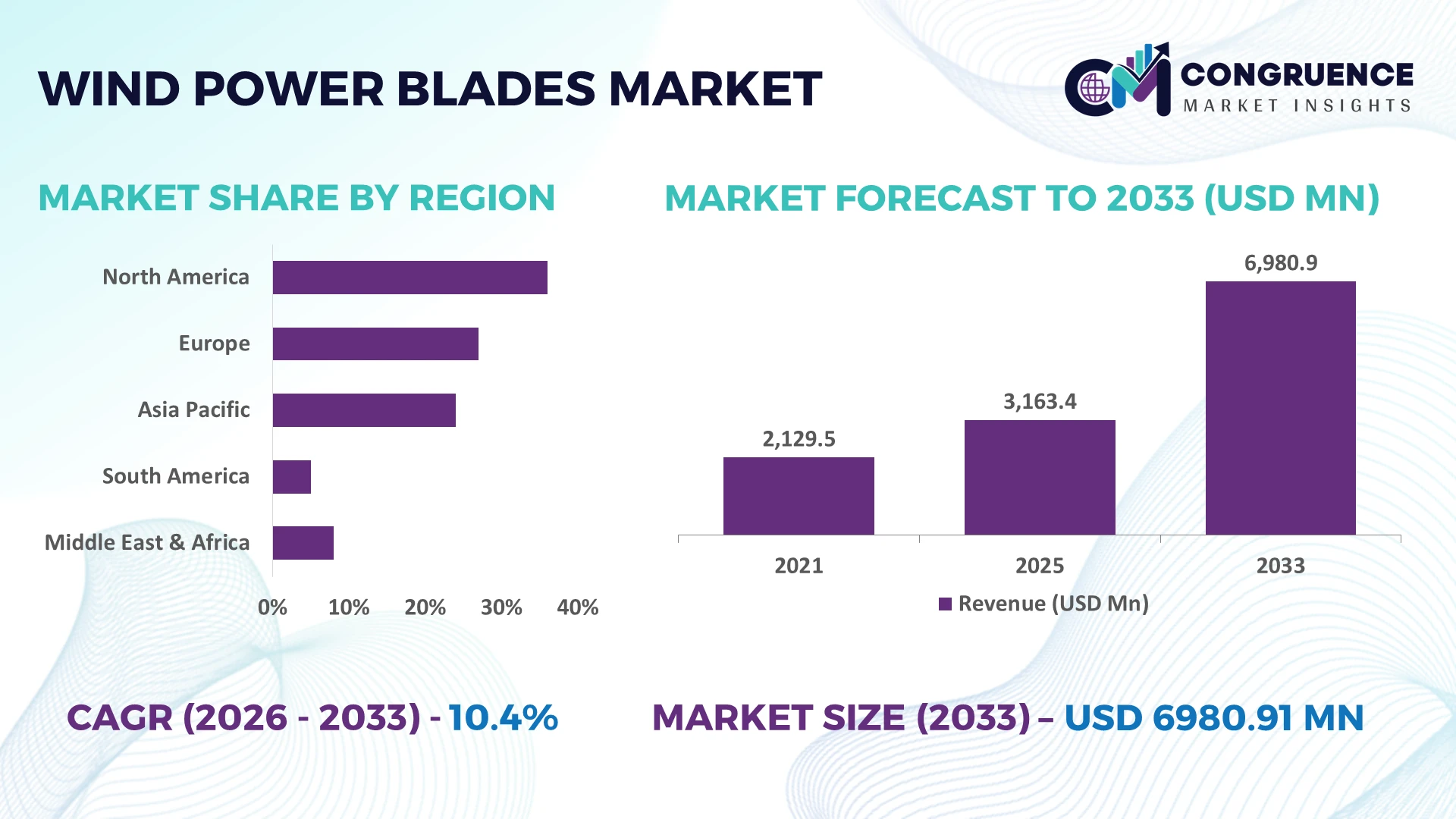

The Global Wind Power Blades Market was valued at USD 3163.44 Million in 2025 and is anticipated to reach a value of USD 6980.91 Million by 2033 expanding at a CAGR of 10.4% between 2026 and 2033. Growth is driven by large-rotor turbine deployment, carbon-fiber blade engineering, offshore wind expansion, and automated composite manufacturing that improves blade durability while reducing production cycle times.

China remains the dominant manufacturing and deployment hub, accounting for approximately 55% of global wind turbine installations while expanding offshore capacity beyond 50 GW through sustained infrastructure investment. Europe maintains leadership in advanced blade engineering and recycling technologies, whereas the United States accelerates domestic manufacturing through industrial policy support. Ongoing energy security priorities following geopolitical supply-chain realignments continue to strengthen localized blade production and material sourcing strategies.

Manufacturers prioritizing regional production capacity, recyclable blade technologies, and automated composite processing are positioned to secure long-term competitive advantage.

Market Size & Growth: USD 3163.44 million in 2025, reaching USD 6980.91 million by 2033 at 10.4% CAGR, supported by larger offshore turbines and advanced composite manufacturing.

Top Growth Drivers: Offshore installations exceed 35% of new capacity, recyclable blade adoption advances above 20%, and manufacturing automation improves production efficiency by nearly 18%.

Short-Term Forecast: By 2028, blade manufacturing cycle times decline approximately 15% through robotics, digital quality inspection, and optimized resin infusion processes.

Emerging Technologies: AI-enabled blade monitoring, automated composite layup, and recyclable thermoplastic materials improve lifecycle performance while reducing maintenance requirements.

Regional Leaders: Asia-Pacific surpasses USD 3400 million, Europe exceeds USD 1800 million, and North America approaches USD 1200 million, driven by localized manufacturing expansion.

Consumer/End-User Trends: More than 60% of new utility-scale projects prioritize longer blades to maximize annual energy production and improve project economics.

Pilot/Case Example: A 2025 offshore wind project achieved nearly 12% higher energy output through next-generation blade aerodynamics and digital performance optimization.

Competitive Landscape: The leading manufacturer holds approximately 18% global share, while major participants include LM Wind Power, TPI Composites, Siemens Gamesa, Vestas, and Nordex.

Regulatory & ESG Impact: Blade recycling initiatives reduce composite waste by over 25%, supported by stricter sustainability targets and regional manufacturing localization.

Investment & Funding: More than USD 8 billion supports factory expansion, automation, and supply-chain resilience as manufacturers diversify regional production networks.

Innovation & Future Outlook: Next-generation modular blades, recyclable composites, and AI-driven predictive maintenance accelerate the transition toward high-performance, resilient wind energy infrastructure.

Rising demand for longer, lightweight, and recyclable wind power blades is reshaping procurement strategies across onshore and offshore projects. Automated composite fabrication, digital blade inspection, and predictive maintenance platforms improve operational reliability, while recyclable material adoption exceeds 20% across new development programs. Continued localization of manufacturing amid evolving trade and industrial policies strengthens supply resilience, setting the stage for broader strategic market assessment.

The Wind Power Blades Market has become strategically important as governments and manufacturers accelerate energy infrastructure modernization while reducing dependence on imported fossil fuels. Supply-chain restructuring is shifting blade manufacturing closer to installation hubs, lowering logistics costs for oversized components and improving project delivery reliability. This transition is intensifying competition among composite manufacturers, turbine OEMs, and material suppliers seeking long-term production partnerships and localized manufacturing capacity.

Advanced carbon-fiber composite blades now deliver approximately 8–12% higher annual energy capture than conventional glass-fiber designs while reducing structural weight by nearly 15%, improving turbine efficiency and lowering maintenance frequency. China leads large-scale manufacturing through integrated production ecosystems, whereas Denmark and Germany continue advancing blade aerodynamics, recyclable materials, and digital engineering capabilities. Over the next two to three years, automated blade inspection and digital manufacturing are expected to increase production efficiency by nearly 20%, supporting faster deployment across utility-scale wind projects.

A recent offshore wind deployment incorporating predictive blade monitoring and automated quality inspection reduced maintenance interventions by roughly 18% while improving operational availability. Manufacturers are expanding regional composite facilities, investing in recyclable blade technologies, and strengthening material partnerships to improve supply resilience. Companies securing advanced manufacturing capabilities, localized production networks, and lifecycle service expertise will establish stronger competitive positioning as turbine capacities continue expanding.

Deployment of larger onshore and offshore turbines is accelerating demand for longer, lightweight, and higher-strength wind power blades. Offshore installations now represent more than 35% of annual turbine capacity additions in several leading markets, while blade lengths exceeding 100 meters improve annual energy production by approximately 10–15%. China's expanding domestic manufacturing ecosystem and India's increasing localization initiatives are strengthening composite supply chains. Manufacturers are investing in automated layup systems, advanced resin technologies, and strategic partnerships with material suppliers to increase production consistency and reduce manufacturing lead times. This industrial transition enables companies to secure higher-value utility-scale projects while improving operational efficiency and competitive differentiation.

Blade manufacturers continue facing structural pressure from fluctuating carbon fiber, fiberglass, and epoxy resin costs, with raw-material price movements frequently exceeding 15% during supply disruptions. Transportation expenses for oversized blades can account for nearly 20% of total project logistics costs, particularly where specialized infrastructure remains limited. Delays in port handling and heavy-load transportation reduce installation efficiency and increase project scheduling complexity. Companies operating in the United States and Europe are responding by localizing component production, expanding long-term supplier contracts, and diversifying raw-material sourcing to improve procurement stability. These actions strengthen production continuity while reducing exposure to international supply-chain volatility.

Thermoplastic composite blades, AI-assisted production systems, and digital twin technologies are creating new opportunities for manufacturers seeking operational and sustainability advantages. Automated manufacturing can improve production efficiency by nearly 20%, while predictive quality systems reduce material waste by approximately 12%. Japan and the Netherlands are accelerating research into recyclable blade materials that support circular manufacturing objectives. Companies are increasing R&D investment, collaborating with composite innovators, and developing lifecycle service ecosystems that combine manufacturing, monitoring, and end-of-life recycling. This integrated approach creates differentiated business models while addressing emerging procurement requirements from utilities prioritizing sustainable infrastructure assets.

Expanding production for next-generation wind power blades requires specialized engineering expertise, precision manufacturing, and high-capacity industrial infrastructure that remain unevenly distributed across global markets. Quality deviations of only 2–3% during composite curing can significantly affect long-term blade performance, while installation delays exceeding 10% disrupt project commissioning schedules. Germany and the United States continue investing in workforce development and automated quality assurance to address manufacturing complexity. Companies must integrate robotics, digital inspection platforms, standardized certification practices, and specialized technical training to maintain consistent production quality, improve deployment reliability, and sustain long-term competitiveness in increasingly advanced wind energy projects.

Advanced Blade Automation Manufacturers are integrating robotic composite layup, AI-enabled defect detection, and automated resin infusion across production facilities. Automated workflows improve manufacturing throughput by nearly 18%, reduce material waste by around 12%, and shorten inspection cycles by 25%. Labor shortages and quality consistency requirements are accelerating factory modernization, prompting companies to expand digital manufacturing capabilities and standardize production across multiple facilities.

Localized Supply Networks Blade manufacturers are restructuring supply chains by establishing production closer to turbine assembly hubs, reducing oversized transport distances by approximately 20% and improving delivery reliability by nearly 15%. Industrial policy incentives and logistics disruptions continue influencing sourcing strategies. Companies are expanding domestic composite sourcing, forming regional supplier partnerships, and redesigning procurement models to strengthen operational resilience and project execution.

Recyclable Composite Adoption Thermoplastic composites and recyclable blade components are moving from pilot projects toward commercial deployment, lowering end-of-life composite waste by nearly 25% while reducing processing time by approximately 10%. Sustainability requirements and evolving procurement standards are influencing purchasing decisions. Manufacturers are collaborating with material innovators, investing in circular manufacturing processes, and redesigning blade architectures for improved lifecycle management.

Digital Lifecycle Optimization Wind farm operators increasingly deploy digital twins, predictive maintenance platforms, and embedded blade sensors that reduce unplanned maintenance events by roughly 18% and improve turbine availability by almost 6%. Offshore asset management requirements and expanding turbine capacities are driving adoption. Companies are integrating monitoring software with long-term service agreements, creating recurring operational value beyond blade manufacturing alone.

Glass Fiber Blades remain the leading segment because they provide an optimal balance between structural strength, manufacturing scalability, and cost efficiency for utility-scale deployment. They account for approximately 60% of installed blade production due to mature supply chains and proven compatibility with high-capacity turbines. Thermoset Blades continue supporting large-scale manufacturing through established composite processes, while Hybrid Blades improve structural performance by combining material advantages without significantly increasing production complexity. Manufacturers continue optimizing resin systems and automated fabrication to improve consistency and reduce production waste.

Carbon Fiber Blades represent the fastest-growing segment as turbine ratings continue increasing and lightweight structures become essential for offshore deployment. Carbon fiber reduces blade weight by approximately 20–30% while enhancing stiffness for longer rotor designs. Thermoplastic Blades are gaining strategic importance because recyclable composite technologies align with circular manufacturing objectives. Companies are expanding advanced composite facilities, strengthening supplier partnerships, and increasing investment in lightweight blade engineering to improve long-term competitiveness and manufacturing flexibility.

Utility Projects represent the dominant application because they require large turbine fleets, standardized procurement, and continuous infrastructure investment. More than 65% of blade demand is associated with utility-scale developments where longer blades improve energy capture and operational efficiency. Onshore Wind Farms continue representing the largest deployment base because of established transmission infrastructure and faster construction schedules. Manufacturers are expanding production capacity and improving logistics planning to support large-volume project execution.

Offshore Wind Farms are the fastest-growing application as next-generation turbines require blades exceeding 100 meters for higher generation efficiency. Offshore installations improve annual energy production by approximately 12%, while advanced monitoring systems reduce maintenance interventions by nearly 18%. Commercial Projects continue expanding through corporate renewable procurement, whereas Community Projects strengthen localized clean-energy deployment. Companies are adapting through digital quality control, modular manufacturing, and long-term service partnerships that enhance operational reliability across multiple deployment environments.

Wind Farm Operators remain the largest end-user segment because they directly manage turbine performance, maintenance strategies, and long-term asset optimization. Approximately 55% of blade procurement decisions originate from operators seeking higher efficiency and lower lifecycle maintenance costs. Utilities continue investing in standardized turbine fleets to strengthen grid reliability, while EPC Contractors influence blade selection through integrated project delivery and construction planning. Manufacturers increasingly customize blade specifications and maintenance services to strengthen long-term customer relationships.

Renewable Energy Developers represent the fastest-growing end-user group as large project pipelines and cross-border investment accelerate new installations. Independent Power Producers continue expanding renewable portfolios, increasing demand for advanced blade technologies that improve operational performance by approximately 10–15%. Companies are responding through strategic partnerships, localized manufacturing agreements, flexible commercial models, and digital lifecycle support services that differentiate offerings beyond equipment supply and strengthen long-term competitive positioning.

Asia-Pacific accounted for the largest market share at 51.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 12.6% between 2026 and 2033.

Advanced Manufacturing Strengthens Domestic Supply Chains

North America maintains a strong position through expanding domestic blade manufacturing, utility-scale wind deployment, and increasing localization of composite supply chains. The region contributes approximately 22% of global blade demand, supported by large onshore developments and growing offshore planning activity. Manufacturers continue investing in automated composite production and digital quality assurance to improve manufacturing consistency while reducing production lead times by nearly 18%. Industrial policy encouraging domestic component sourcing has accelerated factory modernization and supplier partnerships. Companies are also integrating predictive manufacturing systems that enhance production efficiency and reduce operational waste, strengthening long-term competitiveness across utility-scale wind infrastructure projects.

United States Market Outlook: The United States leads the regional market through extensive wind farm infrastructure, established turbine manufacturing, and continued investment in domestic component production. More than 150 GW of installed wind capacity supports sustained replacement and new blade demand. Manufacturers continue expanding composite manufacturing facilities, deploying automated inspection technologies, and strengthening long-term procurement partnerships with utilities and renewable developers to improve supply resilience and project execution efficiency.

Circular Manufacturing Drives Competitive Advantage

Europe remains a technology leader through advanced blade engineering, offshore wind deployment, and sustainable composite innovation. The region accounts for approximately 24% of global blade deployment while maintaining leadership in recyclable blade development and lifecycle optimization. Offshore projects increasingly utilize blades exceeding 100 meters, improving energy capture by approximately 12%. Manufacturers continue collaborating with research institutions to commercialize recyclable thermoplastic composites while expanding automated production facilities. Modernized port infrastructure and specialized installation capabilities further strengthen Europe's position in high-capacity offshore wind deployment.

Germany Market Outlook: Germany remains the region's industrial anchor through advanced composite engineering, precision manufacturing, and strong turbine supply chains. Continuous investment in offshore infrastructure and automated blade production enhances operational efficiency across domestic manufacturing facilities. German enterprises also lead collaborative research on recyclable blade materials and digital manufacturing platforms, supporting higher product quality and long-term sustainability objectives across the European wind energy sector.

Large-Scale Manufacturing Accelerates Global Supply

Asia-Pacific dominates global wind power blade production through integrated manufacturing ecosystems, extensive turbine deployment, and strong industrial capacity. The region represents nearly 52% of global market activity, supported by high-volume composite manufacturing and expanding offshore wind construction. Production automation improves factory throughput by approximately 20%, while localized raw-material sourcing strengthens operational resilience. Manufacturers continue expanding production facilities, investing in larger blade technologies, and enhancing export capabilities to support both domestic installations and international demand.

China Market Outlook: China leads global wind power blade manufacturing through vertically integrated supply chains, large-scale industrial clusters, and sustained renewable infrastructure investment. The country accounts for more than half of newly installed wind capacity worldwide and continues expanding offshore deployment. Domestic manufacturers strengthen competitiveness through robotics, advanced composite technologies, and continuous production expansion, enabling rapid delivery of next-generation blades for domestic and export markets.

Infrastructure Expansion Supports New Deployment

South America is strengthening its wind power blade market through expanding renewable infrastructure, favorable wind resources, and increasing industrial investment. The region contributes approximately 6% of global installations, with utility-scale developments driving procurement activity. Modern logistics corridors and improved transmission planning have shortened project implementation timelines by nearly 10%. Manufacturers are strengthening regional partnerships and evaluating localized assembly operations to reduce transportation complexity for oversized blade components while supporting long-term project execution.

Brazil Market Outlook: Brazil remains the leading market due to its extensive onshore wind resources, established renewable investment framework, and expanding turbine installation pipeline. The country's northeastern industrial corridor supports continued wind farm development and increasing blade demand. Developers are strengthening collaboration with turbine manufacturers while investing in localized logistics and maintenance capabilities that improve operational efficiency across large-scale renewable energy projects.

Energy Diversification Expands Wind Infrastructure

Middle East & Africa is transitioning from an emerging market toward strategic wind infrastructure development through national energy diversification initiatives and utility-scale renewable projects. The region currently contributes around 4% of global deployment but is rapidly expanding project pipelines supported by long-term infrastructure planning. Several utility-scale developments now exceed 500 MW, creating demand for advanced blade technologies and specialized installation capabilities. Companies are establishing engineering partnerships, strengthening local supply networks, and expanding technical service operations to support future deployment requirements.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's strategic growth center through ambitious renewable energy programs, industrial diversification, and expanding utility-scale wind developments. National infrastructure initiatives continue attracting international turbine manufacturers and engineering partners. Large renewable projects exceeding 400 MW are accelerating demand for advanced blade technologies, while localized industrial investment strengthens long-term manufacturing capability and operational support across the country's evolving clean energy sector.

The market is led by LM Wind Power, TPI Composites, Vestas, Siemens Gamesa, and Nordex, while regional composite manufacturers compete aggressively on localized production and delivery speed. Global OEM-integrated manufacturers challenge independent blade suppliers through technology ownership, whereas specialized composite firms compete using manufacturing flexibility and lower production costs. The top five players collectively control approximately 58% of global market activity. Competition centers on blade efficiency, automation, and supply-chain resilience, with automated manufacturing improving production efficiency by nearly 18% and advanced composite materials increasing blade performance by approximately 12%. Localized sourcing reduces logistics costs by around 15%, creating an operational advantage for manufacturers with regional facilities. Companies are expanding composite plants, securing long-term material partnerships, investing in recyclable blade technologies, and strengthening vertical integration across design, manufacturing, and lifecycle services. Competitive pressure is shifting toward technology leadership and supply control rather than pricing alone. High certification requirements, capital-intensive production, and advanced composite expertise remain major entry barriers. Sustainable innovation, manufacturing scale, and localized execution define long-term competitive success.

LM Wind Power

TPI Composites

Vestas Wind Systems

Siemens Gamesa Renewable Energy

Nordex SE

Suzlon Energy

ENERCON GmbH

Mingyang Smart Energy

Goldwind Science & Technology

Sinoma Wind Power Blade

Sany Renewable Energy

Dongfang Electric Corporation

Advanced composite engineering is redefining wind power blade performance through carbon-fiber reinforcement, automated resin infusion, and precision robotic manufacturing. Compared with conventional glass-fiber blade production, next-generation composite designs improve structural efficiency by approximately 10–15% while reducing blade weight by nearly 20%. More than 60% of newly developed utility-scale turbine platforms now integrate advanced composite optimization, enabling larger rotor diameters, improved fatigue resistance, and greater annual energy generation. Manufacturers adopting these technologies achieve stronger production consistency and lower lifecycle maintenance requirements.

Digital technologies are becoming equally important. AI-assisted quality inspection, digital twins, embedded structural sensors, and predictive maintenance platforms reduce manufacturing defects by around 15% while lowering unplanned maintenance interventions by approximately 18%. Blade manufacturers integrating real-time production analytics with automated inspection systems gain higher throughput and faster certification. Global OEMs benefit through shorter development cycles, while specialized composite suppliers strengthen competitiveness by offering customized blade engineering and lifecycle monitoring services.

Between 2026 and 2028, recyclable thermoplastic composites, modular blade architectures, and additive manufacturing for tooling will reshape production economics. Adoption of recyclable blade technologies is expected to exceed 25% across new development programs as sustainability requirements strengthen procurement decisions. Companies investing early in intelligent manufacturing, advanced materials, and digital lifecycle management will achieve superior operational efficiency, stronger customer retention, and long-term competitive differentiation.

October 2024 LM Wind Power announced the successful completion of the ZEBRA project's closed-loop blade recycling demonstration, achieving over 75% recycled resin recovery while validating recyclable composite blade manufacturing. The milestone accelerates commercial circular blade adoption and strengthens sustainable product differentiation. Source: https://www.lmwindpower.com

April 2024 WindEurope members, including leading blade manufacturers, adopted the Blade Material Passport specification to standardize recycling information for turbine blades, improving end-of-life material traceability across the industry. The initiative targets 100% standardized blade documentation, supporting scalable recycling value chains. Source: https://windeurope.org

December 2024 Siemens Gamesa completed installation of its recyclable RecyclableBlade technology at a commercial offshore wind project, enabling full blade material recovery at end of life while maintaining utility-scale performance. The innovation strengthens circular manufacturing strategies and customer sustainability commitments. Source: https://www.siemensgamesa.com

January 2026 Mingyang Smart Energy introduced the world's first fully recyclable carbon-fiber offshore wind turbine blade exceeding 110 meters in length for its MySE23X platform. The innovation supports larger offshore turbines with lower structural weight, reinforcing next-generation high-capacity wind deployment. Source: https://www.mingyang.com

This report provides comprehensive coverage of the Wind Power Blades Market across five blade types, five application categories, and five major end-user groups, delivering detailed analysis of manufacturing trends, deployment patterns, technology adoption, and competitive positioning. It evaluates operational developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while assessing advanced composites, recyclable blade materials, digital manufacturing, automation, and predictive maintenance technologies. More than 60% of current market activity is linked to utility-scale deployments and high-capacity blade platforms.

The study supports strategic decision-making through detailed segmentation, regional benchmarking, competitive assessment, technology evaluation, and investment analysis for the 2026–2033 period. It identifies deployment priorities, manufacturing localization trends, supply-chain restructuring, and emerging opportunities in offshore wind, recyclable composites, and intelligent blade lifecycle management. The report also highlights enterprise strategies, product innovation, partnership activity, and evolving procurement requirements that influence expansion planning, operational optimization, and long-term competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3163.44 Million |

Market Revenue in 2033 | USD 6980.91 Million |

CAGR (2026 - 2033) | 10.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | LM Wind Power, TPI Composites, Vestas Wind Systems, Siemens Gamesa Renewable Energy, Nordex SE, Suzlon Energy, ENERCON GmbH, Mingyang Smart Energy, Goldwind Science & Technology, Sinoma Wind Power Blade, Sany Renewable Energy, Dongfang Electric Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |