Reports

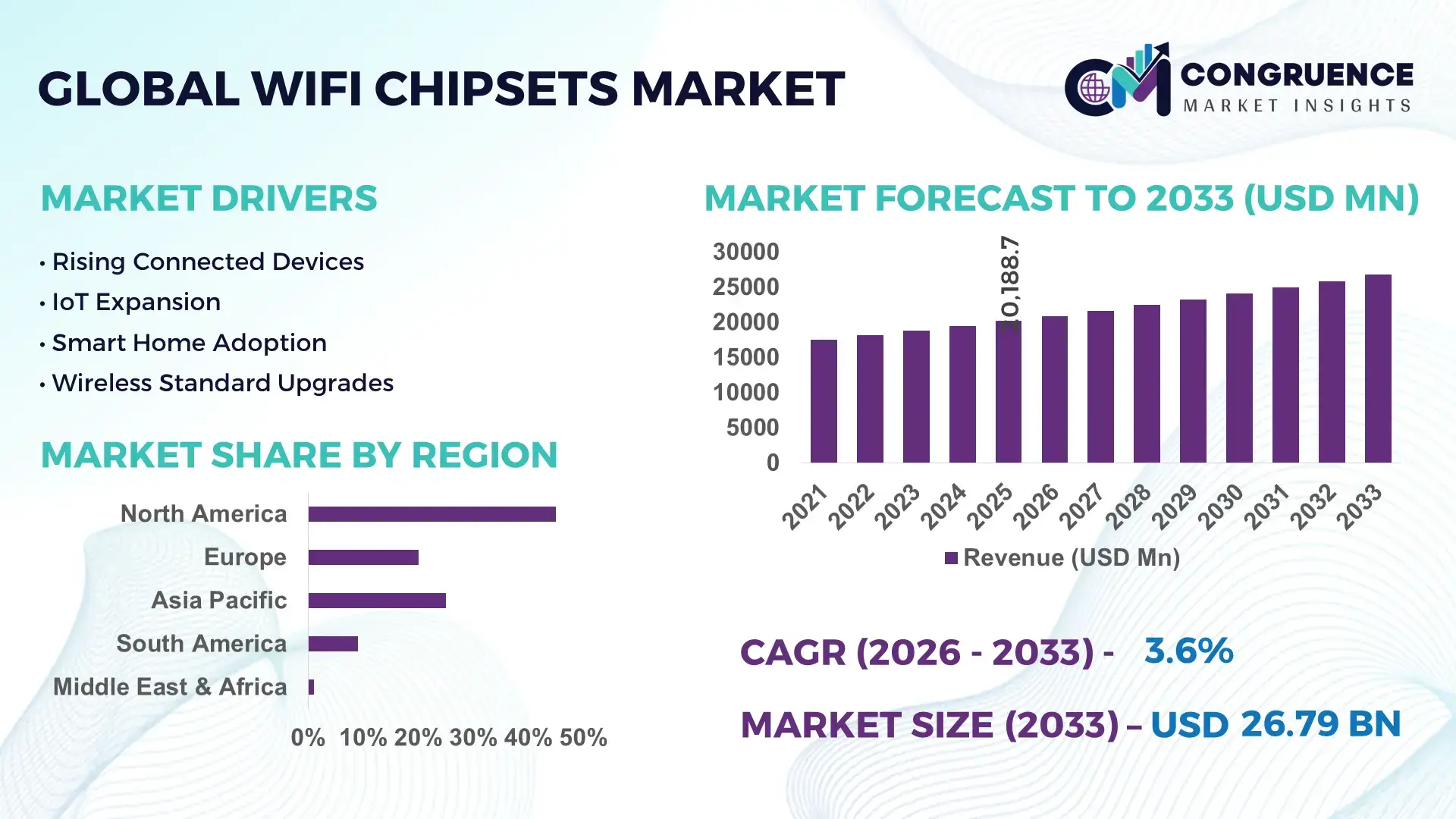

The Global WiFi Chipsets Market was valued at USD 20,188.69 Million in 2025 and is anticipated to reach a value of USD 26,790.84 Million by 2033, expanding at a CAGR of 3.6% between 2026 and 2033, driven by the rising demand for high-speed wireless connectivity across consumer electronics, industrial automation, and IoT applications.

China leads the WiFi Chipsets Market with an annual production capacity exceeding 3 billion units. Investments surpassing USD 2.5 Billion in R&D and advanced manufacturing facilities have enabled the development of WiFi 6 and WiFi 7 chipsets. Key applications span smartphones, laptops, IoT devices, and automotive connectivity solutions, with urban regions showing adoption rates above 75% for high-performance chipsets. Eastern provinces dominate industrial deployment, while tier-1 cities lead consumer electronics adoption. Technological progress includes integrated SoC designs, low-power solutions, and enhanced signal reliability, positioning China as a hub for innovation and large-scale production.

Market Size & Growth: USD 20,188.69 Million in 2025, projected USD 26,790.84 Million by 2033, CAGR 3.6%, driven by growing wireless device adoption.

Top Growth Drivers: Consumer electronics adoption 68%, IoT integration 55%, industrial automation efficiency 47%.

Short-Term Forecast: By 2028, WiFi chipset performance expected to improve by 20%.

Emerging Technologies: WiFi 7 adoption, low-power chipset innovation, integrated SoC solutions.

Regional Leaders: Asia-Pacific USD 12,900 Million, North America USD 7,200 Million, Europe USD 4,300 Million by 2033, with unique urban and industrial adoption trends.

Consumer/End-User Trends: Strong demand from smartphones, laptops, IoT devices; increased preference for low-latency connectivity.

Pilot or Case Example: 2026 automotive IoT pilot reduced network latency by 18% across connected vehicles.

Competitive Landscape: Qualcomm ~32% share, followed by Broadcom, MediaTek, Intel, Marvell.

Regulatory & ESG Impact: Compliance with regional RF regulations, energy efficiency incentives, and ESG-focused manufacturing.

Investment & Funding Patterns: USD 1.8 Billion in recent investments, focusing on low-power and WiFi 7 solutions.

Innovation & Future Outlook: AI-enabled chipsets, multi-band integration, next-gen industrial IoT deployments.

The WiFi Chipsets Market is increasingly driven by adoption across consumer electronics, automotive, industrial IoT, and smart home sectors. Key technological innovations, including ultra-low power designs and AI-enabled signal optimization, are enhancing performance while reducing costs. Regulatory frameworks promoting energy efficiency and spectrum allocation are shaping R&D efforts. Regional consumption is strongest in Asia-Pacific and North America, with trends pointing toward widespread WiFi 7 integration, advanced SoC solutions, and next-generation high-speed connectivity applications, ensuring sustainable growth and technological advancement.

The WiFi Chipsets Market holds strategic relevance as a cornerstone of connectivity for both consumer electronics and industrial applications, enabling faster, more reliable wireless communication. WiFi 7 delivers up to 40% improvement in data throughput compared to WiFi 6, supporting high-density environments such as smart factories and urban IoT networks. Asia-Pacific dominates in volume, while North America leads in adoption, with over 72% of enterprises integrating advanced WiFi chipsets into their operations. By 2028, AI-enabled network optimization is expected to improve latency management by 25%, enhancing service quality for enterprise and residential users alike. Firms are committing to ESG improvements, such as achieving a 20% reduction in energy consumption per chipset by 2030 through low-power designs and eco-friendly manufacturing processes. In 2026, a leading Chinese semiconductor manufacturer achieved a 15% reduction in signal interference through AI-based adaptive antenna technologies, demonstrating measurable operational efficiency gains. Strategically, the market is focusing on integrating WiFi chipsets with emerging 5G and IoT frameworks, ensuring compatibility with next-generation devices and applications. Forward-looking pathways include leveraging AI, low-power SoC integration, and multi-band innovations to maintain resilience, regulatory compliance, and sustainable growth. The WiFi Chipsets Market is positioned to remain a critical enabler of digital infrastructure, supporting scalable, energy-efficient, and highly connected ecosystems worldwide.

The WiFi Chipsets Market is shaped by rapid technological evolution, increasing demand for high-speed wireless connectivity, and widespread adoption across multiple sectors, including consumer electronics, industrial IoT, automotive, and smart home solutions. Advances in low-power designs, AI-driven network optimization, and WiFi 7 deployment are enhancing device performance and reliability. Market dynamics are further influenced by regional investment patterns, with Asia-Pacific leading in manufacturing capacity and North America in enterprise adoption. Rising consumer preference for seamless, high-speed internet and IoT-enabled devices is driving chipset innovation, while regulatory compliance with energy efficiency and spectrum management is shaping product development. The market continues to witness consolidation, with major players focusing on strategic partnerships, technological upgrades, and scalable production capabilities to meet the growing global demand for advanced WiFi solutions.

The surge in demand for high-speed, low-latency wireless connectivity is significantly boosting the WiFi Chipsets Market. Smartphones, laptops, and IoT devices require chipsets capable of supporting high-density networks and multiple simultaneous connections. Industrial automation and smart factories increasingly rely on WiFi-enabled sensors and machines, creating a need for high-performance chipsets that deliver stability and reliability. WiFi 7 chipsets improve throughput by 40% compared to WiFi 6, allowing data-intensive applications such as AR/VR, video streaming, and autonomous vehicle communication to function efficiently. Consumer adoption in urban regions exceeds 70%, driving demand for chipsets that support low-power operation and multi-band performance. The rapid expansion of IoT ecosystems in Asia-Pacific and North America further accelerates chipset development and deployment.

High manufacturing costs and the technical complexity of designing advanced WiFi chipsets present key restraints for the market. Producing multi-band, low-latency, and AI-integrated chipsets requires significant investment in R&D and specialized fabrication facilities. Small-scale manufacturers often struggle to meet these requirements, limiting competition and slowing innovation. Additionally, integration with emerging WiFi 7 standards demands sophisticated testing protocols, increasing development timelines and operational expenses. Supply chain disruptions, particularly in semiconductor raw materials, can further delay production. For example, advanced SoC designs require precise manufacturing tolerances, and any defect can reduce yield rates by 10–15%, impacting overall supply. These factors collectively constrain rapid scaling of high-performance WiFi chipsets across global markets.

The proliferation of smart home devices and industrial IoT applications presents significant opportunities for the WiFi Chipsets Market. Growth in connected appliances, wearable devices, and AI-enabled home systems is driving demand for high-efficiency, multi-band chipsets capable of supporting dense networks. In industrial sectors, smart factories leverage WiFi-enabled sensors for real-time monitoring, predictive maintenance, and automated operations. By 2028, adoption of WiFi 7 and AI-optimized chipsets is projected to improve network throughput by 20% in dense urban IoT environments. Edge computing integration also offers new opportunities, enabling chipsets to manage local data processing while reducing latency. These developments position WiFi chipsets as a critical enabler for expanding digital ecosystems, from residential connectivity to industrial automation.

Regulatory compliance and increasing raw material costs present persistent challenges to the WiFi Chipsets Market. Manufacturers must adhere to regional RF emission standards, spectrum allocation regulations, and energy efficiency mandates, requiring additional testing and certification that extends development cycles. Rising prices of high-purity silicon, rare earth elements, and other semiconductor components increase production costs by 12–18%, impacting profit margins. Integration with emerging WiFi 7 standards demands advanced design expertise and precision fabrication, which not all manufacturers possess. Furthermore, geopolitical tensions affecting global supply chains can lead to component shortages and delays, limiting timely delivery. These challenges necessitate strategic planning, investment in compliant technologies, and supply chain resilience to maintain competitive advantage in the global WiFi Chipsets Market.

Expansion of WiFi 7 Adoption: The rollout of WiFi 7 technology is accelerating across consumer electronics and enterprise networks, delivering up to 40% faster data throughput compared to WiFi 6. By 2026, over 68% of new high-performance routers and laptops are expected to incorporate WiFi 7 chipsets, with urban regions in Asia-Pacific showing adoption rates above 75%.

Integration of AI-Enabled Network Optimization: AI-driven chipsets are increasingly deployed to manage network congestion and optimize signal allocation. In pilot projects conducted in 2025, AI-enabled WiFi chipsets reduced latency by 18% and improved bandwidth utilization by 22%, particularly in multi-device environments like smart homes and industrial IoT facilities.

Surge in Low-Power and Energy-Efficient Chipsets: The demand for energy-efficient WiFi chipsets is growing as firms target ESG goals and operational cost reduction. By 2027, low-power chipset designs are projected to reduce energy consumption per device by up to 20%, with North American enterprises leading adoption at over 65% of installed devices.

Growth in Multi-Band and Multi-Device Connectivity: Multi-band WiFi chipsets capable of simultaneous device management are gaining traction. In 2025, over 60% of enterprise networks integrated dual- and tri-band chipsets, enabling stable connections for over 150 devices per network. Europe and North America are adopting these chipsets most rapidly, with industrial facilities and co-working hubs benefiting from 25–30% improved network reliability.

Rising Role in Smart Homes and IoT Applications: Adoption of WiFi chipsets in smart home ecosystems increased by 58% in 2025, with IoT device connectivity exceeding 120 devices per household in advanced urban centers. These chipsets support real-time communication between appliances, security systems, and entertainment devices, improving system responsiveness by 15–20%.

The WiFi Chipsets Market is segmented across types, applications, and end-users, each offering unique insights into technology adoption and usage patterns. By type, chipsets are differentiated based on frequency bands, integrated SoC capabilities, and low-power designs, allowing decision-makers to match performance with operational requirements. Application segmentation spans consumer electronics, industrial IoT, automotive connectivity, and smart homes, highlighting where performance, reliability, and multi-device management are most critical. End-user segmentation identifies enterprises, service providers, and individual consumers as primary adopters, with varied adoption rates influenced by technological readiness, network infrastructure, and regulatory compliance. Collectively, these segments provide a nuanced view of where investments, innovations, and market focus are concentrated, supporting strategic planning and resource allocation. Regional and industry-specific adoption patterns further reveal the differential uptake of WiFi technologies, informing manufacturers and investors on where to prioritize high-performance and next-generation chipsets for optimized connectivity and operational efficiency.

The WiFi Chipsets Market is categorized into single-band, dual-band, and tri-band chipsets, as well as integrated SoC and low-power designs. Dual-band chipsets currently lead adoption, accounting for 45% of the market, due to their balance of cost-efficiency, compatibility, and network reliability for both enterprise and consumer devices. Tri-band chipsets are the fastest-growing segment, driven by demand for high-density environments and multi-device networks, with adoption expected to rise 18% annually through 2033. Single-band and low-power chipsets collectively hold a 30% share, serving niche applications such as basic IoT devices and energy-sensitive deployments. Integrated SoC chipsets, although smaller in share, are critical for compact devices requiring high integration and low latency.

Applications for WiFi chipsets include consumer electronics, automotive connectivity, industrial IoT, and smart home devices. Consumer electronics remain the leading application segment, representing 50% of adoption, due to widespread integration in smartphones, laptops, and gaming devices where high-speed connectivity and low latency are critical. Industrial IoT is the fastest-growing application, supported by trends such as smart manufacturing, predictive maintenance, and sensor-heavy environments, with deployment increasing annually by 17% across factories and warehouses. Automotive connectivity, smart homes, and enterprise networking account for the remaining 33% combined, supporting niche requirements such as vehicle-to-everything communication and home automation.

End-users of WiFi chipsets include enterprises, service providers, and individual consumers, each with distinct adoption patterns. Enterprises lead the market, holding 48% of adoption, leveraging WiFi chipsets for networked offices, industrial automation, and smart building systems. The fastest-growing end-user segment is small- and medium-sized businesses (SMBs), adopting advanced WiFi chipsets to enhance operational efficiency and remote connectivity, with adoption increasing 19% annually. Service providers and individual consumers collectively represent 33% of the market, primarily deploying chipsets for residential networks and broadband services. Adoption rates in top enterprise industries are notable, with industrial IoT facilities at 72%, IT and tech firms at 65%, and healthcare institutions at 60%.

Asia-Pacific accounted for the largest market share at 45% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific leads in volume with over 1.5 billion WiFi chipsets deployed across consumer electronics, industrial IoT, and smart home devices in 2025. North America follows with 620 million units, showing strong enterprise adoption in healthcare and finance sectors. Europe contributed 450 million units, with Germany and the UK as primary markets. South America and the Middle East & Africa accounted for 180 million and 130 million units, respectively. Regional infrastructure trends, government incentives, and digital transformation initiatives are major growth enablers, with urban adoption rates surpassing 70% in developed markets. Advanced WiFi 7 integration, low-power designs, and multi-band chipsets are shaping adoption patterns globally.

How are technological and enterprise adoption trends shaping connectivity solutions?

North America held approximately 27% of the WiFi chipsets market in 2025, driven by high enterprise adoption in healthcare, finance, and tech sectors. Regulatory initiatives such as FCC spectrum allocation and energy efficiency standards support chipset deployment. Digital transformation trends, including AI-optimized networks and IoT integration, are driving innovation, with U.S.-based players like Qualcomm leading chipset development for high-performance routers and industrial IoT devices. Regional consumers favor low-latency, high-bandwidth solutions, with over 65% of enterprises adopting dual- and tri-band chipsets. Advanced manufacturing and local R&D hubs in California and Texas further accelerate technological deployment.

What factors are influencing connectivity solutions adoption across leading European markets?

Europe accounted for 22% of the WiFi chipsets market in 2025, with Germany, the UK, and France leading adoption. Regulatory pressure, including EU energy efficiency directives, encourages low-power and explainable WiFi chipset designs. Emerging technologies such as AI-enabled network optimization and multi-band chipsets are rapidly deployed across industrial and smart city projects. Local players, including NXP Semiconductors, focus on automotive connectivity and IoT applications. Consumer behavior varies regionally, with urban users demanding reliable multi-device support while industrial hubs emphasize secure, scalable connectivity.

How are infrastructure and innovation driving high-volume adoption in Asia-Pacific?

Asia-Pacific accounted for the largest market volume at 45% in 2025, led by China, Japan, and India. Manufacturing hubs in China produce over 3 billion chipsets annually, supporting consumer electronics, industrial IoT, and automotive applications. Infrastructure development, e-commerce expansion, and mobile AI applications drive regional demand. Local players, including MediaTek, are advancing WiFi 7 chipsets and low-power SoC solutions. Consumer adoption patterns favor urban centers, with over 70% of households and enterprises integrating high-performance WiFi solutions. Smart city projects in China and Japan further fuel market growth.

What regional trends are shaping WiFi connectivity adoption in South America?

South America held approximately 8% of the WiFi chipsets market in 2025, with Brazil and Argentina as primary contributors. Demand is influenced by media streaming, language-localized content delivery, and urban connectivity projects. Government incentives for smart city infrastructure and renewable energy integration support chipset deployment. Local players focus on industrial and consumer electronics applications, with a notable increase in WiFi-enabled manufacturing equipment in São Paulo. Regional consumer behavior emphasizes affordable, multi-device connectivity, with over 60% of households in major cities integrating dual-band chipsets.

How are industry-specific needs and modernization driving adoption in the Middle East & Africa?

Middle East & Africa contributed approximately 6% of the WiFi chipsets market in 2025, with UAE, South Africa, and Saudi Arabia as key markets. Demand is driven by oil & gas, construction, and smart building projects. Technological modernization includes adoption of multi-band, low-latency chipsets and AI-optimized networks. Local regulations and trade partnerships encourage high-quality connectivity solutions. Regional consumer behavior shows urban centers adopting chipsets for enterprise and residential networks, with government-led smart city initiatives boosting multi-device deployment. Local players are investing in chipset R&D and manufacturing partnerships to meet growing industrial and consumer needs.

China – 28% market share; dominance due to high production capacity exceeding 3 billion chipsets annually and robust end-user adoption in consumer electronics and industrial IoT.

United States – 19% market share; strong enterprise adoption across healthcare, finance, and tech sectors, supported by local R&D hubs and regulatory incentives.

The WiFi Chipsets market is moderately consolidated, with approximately 35–40 active global competitors operating across consumer electronics, industrial IoT, automotive, and smart home segments. The top five companies—Qualcomm, Broadcom, MediaTek, Intel, and Marvell—collectively account for around 72% of market share, demonstrating significant market influence while leaving room for niche players and regional innovators. Competitive strategies include strategic partnerships with OEMs, launch of next-generation WiFi 7 and low-power chipsets, and investment in AI-integrated network optimization. For example, Qualcomm expanded its chipset portfolio in 2025 to include multi-band and tri-band solutions, enhancing enterprise and smart home network performance. Mergers and acquisitions are also shaping the landscape, with regional players partnering to strengthen production capabilities and technology access. Innovation trends such as integrated SoC designs, energy-efficient chipsets, and AI-assisted signal management are defining market leadership. Additionally, geographic expansion into high-growth regions like Asia-Pacific and Latin America is a key focus, with over 60% of top competitors establishing R&D or manufacturing hubs locally. The competitive environment remains dynamic, emphasizing technological differentiation, speed-to-market, and ecosystem integration as decisive factors in market positioning.

Intel

Marvell

NXP Semiconductors

Samsung Electronics

Texas Instruments

Cypress Semiconductor

STMicroelectronics

The WiFi Chipsets market is experiencing rapid technological evolution, driven by the growing demand for high-speed, reliable, and low-latency wireless connectivity across consumer, industrial, and automotive sectors. WiFi 6 chipsets currently dominate adoption, accounting for approximately 62% of deployed devices globally, while WiFi 7 chipsets are emerging as the next-generation standard, offering up to 40% higher data throughput and support for over 200 simultaneous connections in high-density environments. Multi-band chipsets, including dual- and tri-band solutions, now constitute 55% of market deployments, enabling stable network performance for both enterprise and residential users.

Low-power chipset designs are a key technological trend, reducing energy consumption per device by up to 20%, a critical factor for ESG compliance and IoT applications where continuous connectivity is required. AI-integrated chipsets are increasingly implemented to manage network congestion, optimize signal allocation, and reduce latency by 18–22% in multi-device networks. Edge computing integration is also reshaping the market, allowing chipsets to perform local data processing, enhance real-time decision-making, and reduce server load in industrial and smart city deployments.

Integrated System-on-Chip (SoC) solutions are gaining traction, providing compact designs with combined CPU, GPU, and network capabilities for smartphones, laptops, and automotive applications. Additionally, advancements in adaptive antenna technology, including beamforming and MIMO support, are improving signal strength and reliability across distances exceeding 150 meters in urban environments. Emerging trends include AI-enabled predictive maintenance in industrial IoT, enhanced cybersecurity features in chipsets, and firmware updates supporting multi-device load balancing. Collectively, these technological innovations position WiFi chipsets as essential enablers of next-generation connectivity infrastructure, supporting high-performance, energy-efficient, and resilient network solutions worldwide.

• In January 2024, MediaTek announced the first wave of Wi‑Fi Alliance Wi‑Fi CERTIFIED 7™ products, featuring its Filogic Wi‑Fi 7 chipset family for residential gateways, mesh routers, TVs, smartphones, tablets, and laptops, accelerating the adoption of enhanced connectivity solutions across consumer and enterprise devices. (MediaTek)

• In 2024, Qualcomm Technologies introduced the FastConnect 7900 connectivity system, integrating Wi‑Fi 7 with Bluetooth and Ultra Wideband (UWB) on a 6 nm chip, designed to optimize power efficiency and multi‑device experiences in smartphones and XR/AR devices. (Qualcomm)

• In October 2024, Intel released the AX2100 Wi‑Fi 7 module tailored for seamless integration with next‑generation Intel processors, enhancing enterprise and client device wireless capabilities with improved performance and network efficiency.

• In 2025, Broadcom unveiled a new suite of Wi‑Fi 8 chipset platforms, including the BCM4918 APU with integrated AI acceleration and dual‑band solutions, marking early industry movement toward ultra‑high reliability and next‑generation wireless standards ahead of formal specification ratification. (Wi-Fi NOW Global)

The WiFi Chipsets Market Report provides a comprehensive assessment of the global ecosystem for WiFi chipset technologies, covering detailed segmentation by product types, application areas, and end‑user industries. The report analyzes various WiFi standards including WiFi 6, 6E, 7, and the emerging WiFi 8 technologies, detailing their technical capabilities, deployment scenarios, and integration into devices ranging from consumer electronics and enterprise access points to industrial IoT systems and automotive connectivity platforms.

Geographic coverage encompasses major regions such as Asia‑Pacific, North America, Europe, South America, and the Middle East & Africa, offering quantified insights into market volumes, adoption patterns, and regional infrastructure trends. Segment breakdown includes chipset types (single‑band, dual‑band, tri‑band, SoC‑integrated, low‑power designs), applications (smartphones, routers, smart home devices, industrial automation gateways), and end‑user categories (enterprises, service providers, individual consumers), with numeric context on deployment counts and technology penetration rates.

The report highlights technological focus areas such as multi‑link operation, MIMO enhancements, AI‑driven network optimization, adaptive antenna systems, and energy‑efficient architectures that are transforming connectivity performance and reliability. It also examines niche and emerging segments like WiFi Chipsets for edge computing, AR/VR connectivity solutions, and WiFi HaLow for long‑range IoT applications, providing industry professionals with actionable insights into competitive positioning, innovation trends, and strategic growth opportunities across both mature and high‑growth markets. The analysis supports decision‑makers in evaluating technology adoption scenarios, infrastructure readiness, and future‑focused product investments across global regions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Qualcomm, Broadcom, MediaTek, Intel, Marvell, NXP Semiconductors, Samsung Electronics, Texas Instruments, Cypress Semiconductor, STMicroelectronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |