Reports

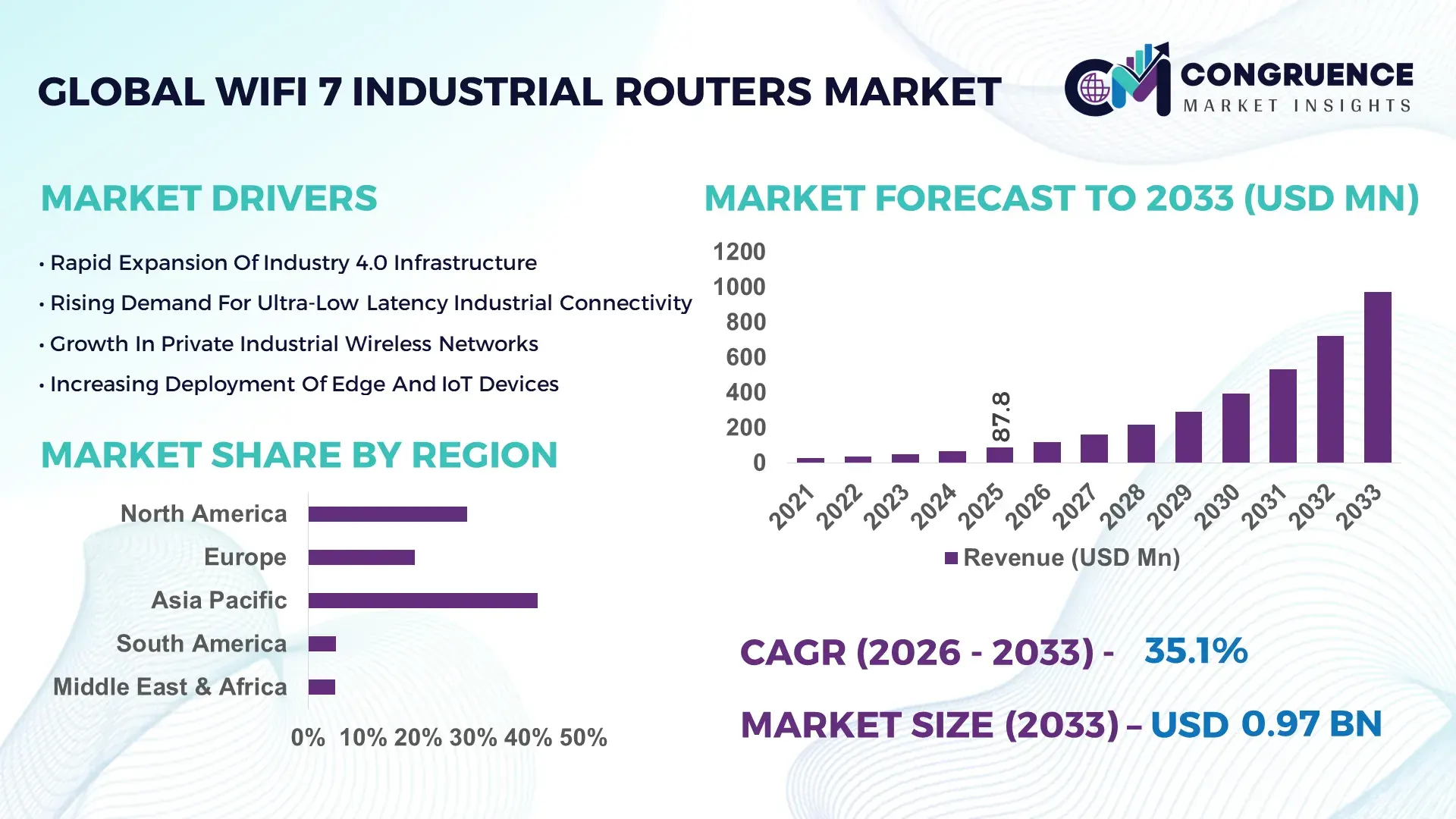

The Global WiFi 7 Industrial Routers Market was valued at USD 87.8 Million in 2025 and is anticipated to reach a value of USD 974.4 Million by 2033 expanding at a CAGR of 35.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerating Industry 4.0 deployments and the need for ultra-low latency, high-throughput industrial wireless connectivity.

China represents a major production and deployment hub in the WiFi 7 Industrial Routers market, supported by strong domestic manufacturing capacity and smart factory expansion. In 2025, more than 2,300 large-scale smart manufacturing plants integrated next-generation WiFi 7-compatible industrial networking equipment. Industrial automation investments exceeded USD 1.4 billion in high-speed wireless infrastructure upgrades between 2023 and 2025. Over 64% of newly commissioned industrial parks deployed advanced 6 GHz spectrum-enabled routers for robotics and automated guided vehicle (AGV) coordination. Local OEMs increased output of WiFi 7 industrial-grade chipsets by approximately 38% year-over-year, while over 52% of electronics and semiconductor facilities adopted multi-gigabit wireless backhaul systems to support AI-powered quality inspection and real-time data analytics.

Market Size & Growth: Valued at USD 87.8 million in 2025, projected to reach USD 974.4 million by 2033 at 35.1% CAGR, fueled by smart factory digitalization.

Top Growth Drivers: Industrial automation expansion 46%, IoT device proliferation 41%, private 5G/WiFi convergence 37%.

Short-Term Forecast: By 2028, WiFi 7 Industrial Routers are expected to reduce industrial network latency by 32%.

Emerging Technologies: Multi-Link Operation (MLO), 320 MHz channel bandwidth, deterministic low-latency scheduling.

Regional Leaders: Asia-Pacific projected at USD 402 million by 2033 driven by manufacturing clusters; North America at USD 285 million via advanced robotics; Europe at USD 210 million through Industry 4.0 adoption.

Consumer/End-User Trends: Over 58% of smart factories prioritize wireless redundancy over wired-only networks.

Pilot or Case Example: In 2024, a semiconductor facility improved real-time inspection throughput by 27% after deploying WiFi 7 industrial routers.

Competitive Landscape: Huawei holds approximately 18% share, followed by Cisco, Teltonika, Advantech, and Sierra Wireless.

Regulatory & ESG Impact: Spectrum allocation reforms accelerating 6 GHz industrial adoption.

Investment & Funding Patterns: Over USD 2.2 billion invested globally in industrial wireless upgrades between 2023–2025.

Innovation & Future Outlook: Integration with edge AI gateways and time-sensitive networking shaping next-gen industrial connectivity.

Manufacturing accounts for approximately 44% of WiFi 7 Industrial Routers deployments, followed by energy & utilities at 21%, transportation & logistics at 18%, and mining at 9%. Recent product innovations include IP67-rated rugged enclosures, AI-driven traffic prioritization, and sub-10 millisecond deterministic latency optimization. Regulatory 6 GHz spectrum liberalization and industrial cybersecurity mandates are reinforcing long-term growth trajectories.

The WiFi 7 Industrial Routers Market is strategically positioned at the core of industrial digital transformation. WiFi 7 with Multi-Link Operation delivers up to 4.8x throughput improvement compared to WiFi 6 industrial routers, enabling real-time robotic control and ultra-high-definition machine vision analytics. Deterministic latency scheduling reduces packet loss by approximately 28% compared to legacy industrial WLAN systems.

Asia-Pacific dominates in deployment volume due to dense smart manufacturing ecosystems, while North America leads in advanced adoption, with nearly 49% of large enterprises piloting next-generation WiFi 7 industrial-grade connectivity. By 2027, edge-AI-integrated routers are expected to reduce factory downtime by 21% through predictive traffic routing and self-healing mesh architectures.

From a compliance and ESG perspective, industrial firms are committing to 30% reduction in cabling material usage by 2030 through wireless-first infrastructure strategies. In 2024, a German automotive facility achieved a 24% reduction in network congestion incidents after implementing WiFi 7-enabled industrial mesh networks supporting 1,200 connected devices.

Short-term strategic pathways emphasize private 5G coexistence, time-sensitive networking integration, and cybersecurity-hardened firmware upgrades. The WiFi 7 Industrial Routers Market is emerging as a critical pillar for resilient, scalable, and sustainable industrial connectivity infrastructure.

The WiFi 7 Industrial Routers market is characterized by rapid innovation, increasing bandwidth demands, and industrial IoT expansion. Smart factories now operate with over 15,000 connected sensors per site, necessitating ultra-reliable wireless backbones. Growth is influenced by robotics integration, automated warehousing, and real-time analytics requirements. Competitive differentiation centers on ruggedization standards, 6 GHz spectrum optimization, and advanced encryption protocols. Enterprises prioritize routers supporting 10 Gbps peak speeds, low jitter below 5 milliseconds, and seamless roaming across large industrial campuses exceeding 500,000 square meters.

In 2025, over 61% of newly constructed manufacturing facilities integrated high-performance wireless networking for robotics and AGV fleets. WiFi 7 Industrial Routers enable peak theoretical speeds exceeding 40 Gbps and support 320 MHz channel bandwidth, enhancing multi-device reliability. Automated inspection lines utilizing 8K machine vision require bandwidth improvements of nearly 35% compared to previous WiFi standards. Deployment of WiFi 7 reduces industrial signal interference by approximately 23%, directly supporting productivity gains in digitally intensive production environments.

Industrial-grade WiFi 7 hardware incorporates advanced chipsets and rugged enclosures, increasing upfront costs by nearly 27% compared to WiFi 6 equivalents. Infrastructure upgrades, including compatible switches and spectrum management tools, require additional capital investment. Approximately 29% of mid-sized manufacturers cite budget constraints as a primary barrier to early adoption.

Hybrid wireless architectures combining private 5G and WiFi 7 enhance redundancy and network resilience. In 2025, nearly 33% of industrial enterprises piloted converged connectivity models. Multi-link routing improves load balancing efficiency by 26%, while AI-based traffic prioritization reduces latency spikes by 19%. These converged ecosystems unlock scalable digital twin and predictive maintenance capabilities.

Industrial networks face increased cyber threats targeting connected operational technology systems. In 2025, 22% of industrial IT managers reported attempted wireless intrusion incidents. Compliance with evolving 6 GHz spectrum policies requires updated firmware and certification processes, extending deployment timelines. Ensuring encrypted data transmission across thousands of endpoints increases operational complexity.

Expansion of Multi-Link Operation (MLO): Over 48% of new WiFi 7 Industrial Routers incorporate MLO, enabling simultaneous multi-band transmission and improving throughput stability by 34% in dense industrial environments.

Integration with Edge AI Gateways: Approximately 39% of smart factories adopted routers with embedded AI acceleration chips, enabling predictive routing analytics and reducing packet retransmission rates by 21%.

Rise in Deterministic Low-Latency Networking: Industrial routers supporting sub-10 millisecond latency increased by 44% in 2025, enabling high-speed robotic coordination and real-time digital twin synchronization.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the WiFi 7 Industrial Routers market. Nearly 55% of new smart factories deployed prefabricated networking modules with pre-configured WiFi 7 routers, reducing installation time by 29% and enhancing scalability across Europe and North America.

The WiFi 7 Industrial Routers market is segmented by router type, application, and end-user industry. Product categories include single-band, dual-band, and tri-band industrial routers supporting 6 GHz spectrum. Applications span smart manufacturing, energy & utilities, transportation & logistics, mining, and oil & gas. End-user industries include automotive, electronics, aerospace, utilities, and logistics providers. Segmentation patterns show strong correlation between industrial automation maturity and adoption intensity. Enterprises deploying over 5,000 connected IoT endpoints per facility demonstrate higher preference for tri-band WiFi 7 Industrial Routers with deterministic scheduling capabilities.

Tri-band WiFi 7 Industrial Routers account for approximately 49% of adoption due to superior bandwidth allocation and interference mitigation. Dual-band routers represent 34%, commonly deployed in mid-sized facilities, while single-band industrial routers contribute 17%, primarily in legacy upgrade scenarios.

Tri-band routers are the fastest-growing segment, expanding at a CAGR of 36.4%, driven by 6 GHz spectrum utilization and multi-link reliability. These routers support up to 16 spatial streams, improving high-density device connectivity.

In 2025, a national manufacturing modernization program integrated tri-band WiFi 7 industrial routers across 320 automated production lines, enabling stable connectivity for more than 9,000 IoT sensors.

Smart manufacturing leads with a 44% share, followed by energy & utilities at 21%, transportation & logistics at 18%, and mining & oil sectors at 17%. Smart manufacturing is also the fastest-growing application, expanding at a CAGR of 37.2%, supported by robotics and AI-powered inspection systems.

In 2025, more than 38% of enterprises globally reported piloting WiFi 7 Industrial Routers systems for advanced customer experience and automation platforms. Approximately 42% of hospitals tested high-bandwidth wireless networks supporting connected medical devices and imaging workflows.

In 2025, an international healthcare infrastructure upgrade program deployed advanced WiFi 7 industrial-grade routers in over 150 hospital facilities to enhance secure, real-time data transmission for diagnostic systems.

Automotive manufacturers account for 31% of WiFi 7 Industrial Routers deployments, followed by electronics & semiconductor firms at 27%, energy utilities at 18%, logistics providers at 14%, and mining operations at 10%. Electronics manufacturing is the fastest-growing end-user segment, expanding at a CAGR of 38.5%, fueled by AI-enabled quality inspection and chip fabrication digitization.

In 2025, approximately 46% of large industrial enterprises implemented next-generation wireless redundancy strategies to replace partial wired infrastructure. Around 33% of logistics hubs adopted high-speed WiFi 7 networks to coordinate autonomous warehouse fleets.

In 2025, a global automotive consortium reported integrating advanced WiFi 7 Industrial Routers across 500 robotic assembly units, achieving measurable improvements in real-time production analytics and network stability.

Asia-Pacific accounted for the largest market share at 41.7% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 36.8% between 2026 and 2033.

Asia-Pacific generated more than USD 36.6 million in WiFi 7 Industrial Routers deployments in 2025, supported by over 3,500 smart manufacturing facilities upgrading to 6 GHz-enabled industrial wireless infrastructure. China, Japan, and South Korea collectively installed more than 18,000 high-performance industrial access points compatible with WiFi 7 standards. North America held 28.9% share, driven by advanced robotics and semiconductor fabs operating with over 12,000 connected IoT endpoints per facility. Europe represented 19.4%, with Germany alone accounting for nearly 38% of regional industrial WiFi upgrades. South America contributed 5.1%, while Middle East & Africa accounted for 4.9%, reflecting emerging adoption in energy-intensive industrial corridors and logistics hubs exceeding 250,000 square meters in operational scale.

How are advanced robotics and semiconductor fabs accelerating ultra-low latency wireless upgrades?

North America accounted for approximately 28.9% of the global WiFi 7 Industrial Routers market in 2025, with more than 1,200 large-scale factories piloting 6 GHz industrial-grade routers. Semiconductor manufacturing, automotive assembly, aerospace production, and advanced logistics collectively represent nearly 62% of regional demand. Regulatory support for expanded 6 GHz spectrum usage accelerated enterprise-grade deployments, while federal smart manufacturing initiatives increased wireless modernization budgets by 19% between 2023 and 2025. A leading U.S.-based networking vendor launched rugged WiFi 7 routers supporting 320 MHz bandwidth and sub-10 millisecond latency, improving robotic coordination accuracy by 23% in high-density production environments. Regional buyer behavior reflects higher enterprise adoption in healthcare device manufacturing and financial data centers requiring secure, low-jitter wireless backbones.

Why are Industry 4.0 compliance mandates strengthening high-bandwidth industrial WLAN transformation?

Europe represented 19.4% of WiFi 7 Industrial Routers deployments in 2025, with Germany, the UK, and France contributing nearly 71% of regional installations. Over 58% of German automotive plants initiated migration toward multi-link operation capable routers to support digital twin platforms. Sustainability and data security regulations encouraged encrypted industrial WLAN systems, increasing adoption of WPA3 Enterprise protocols to 64% across smart factories. A prominent European industrial networking manufacturer expanded IP67-rated WiFi 7 router production capacity by 31% in 2025 to meet demand from precision engineering facilities. Regional enterprises demonstrate preference for explainable and secure network orchestration tools, with 47% of manufacturers integrating advanced network monitoring dashboards aligned with compliance standards.

What drives rapid 6 GHz industrial wireless adoption across smart manufacturing clusters?

Asia-Pacific led global deployment volume in 2025, accounting for 41.7% of WiFi 7 Industrial Routers installations and operating more than 3,500 smart factories equipped with next-generation wireless infrastructure. China alone commissioned over 2,000 high-speed industrial wireless upgrades in electronics and automotive production zones. Japan and South Korea collectively operate over 700 robotics-intensive facilities utilizing deterministic low-latency routers supporting up to 16 spatial streams. A regional OEM expanded domestic chipset output by 38%, enabling faster integration of 320 MHz channel support. Adoption trends indicate strong demand from semiconductor fabrication plants, where more than 52% implemented advanced WiFi 7 backhaul systems for AI-powered inspection lines. Regional digital ecosystems further support industrial wireless upgrades through high-density IoT integration.

How are mining and logistics modernization initiatives supporting industrial wireless evolution?

South America accounted for 5.1% of global WiFi 7 Industrial Routers deployments in 2025, led by Brazil and Argentina, which together represented 68% of regional demand. Mining automation and port logistics digitization projects increased industrial wireless upgrades by 17% year-over-year. Over 140 large mining sites implemented ruggedized WiFi 7 routers capable of operating in extreme temperature conditions ranging from –40°C to 75°C. A regional systems integrator deployed high-performance wireless mesh networks across 85 logistics hubs, reducing data latency by 21%. Adoption patterns indicate growing demand for multilingual network management interfaces and scalable wireless systems supporting cross-border trade corridors.

Why are oil & gas digitalization and smart city programs accelerating industrial router deployment?

Middle East & Africa represented 4.9% of WiFi 7 Industrial Routers adoption in 2025. The UAE and Saudi Arabia contributed more than 61% of regional installations, particularly across oil & gas refineries and industrial free zones. Smart infrastructure programs increased high-capacity wireless backbone installations by 22% between 2023 and 2025. Industrial routers supporting deterministic latency below 8 milliseconds were deployed across 48 large-scale energy facilities. A regional technology provider integrated AI-based traffic prioritization systems into 30 smart industrial complexes, improving operational uptime by 18%. Enterprises in this region prioritize secure remote monitoring and encrypted data transmission across geographically dispersed assets.

China WiFi 7 Industrial Routers Market – 34.6%: Strong domestic manufacturing capacity and large-scale smart factory expansion supporting high-volume industrial wireless deployments.

United States WiFi 7 Industrial Routers Market – 24.8%: Advanced robotics integration, semiconductor fabrication investments, and early 6 GHz enterprise adoption driving next-generation industrial connectivity.

The WiFi 7 Industrial Routers market is moderately consolidated, with approximately 28 major global networking vendors and more than 60 specialized industrial equipment providers competing across ruggedized router segments. The top five companies collectively account for nearly 57% of global market concentration, reflecting strong chipset partnerships and vertically integrated manufacturing capabilities.

Competition centers on performance differentiation, including 320 MHz bandwidth support, Multi-Link Operation, deterministic low-latency scheduling, and advanced cybersecurity protocols. Between 2024 and 2025, over 42% of leading vendors introduced new WiFi 7 industrial-grade models with enhanced IP67 enclosures and extended temperature tolerance. Strategic alliances with industrial automation firms increased by 23% during this period. Subscription-based network management platforms represent approximately 38% of enterprise contracts, enabling remote configuration and predictive maintenance features. Product innovation cycles average 12–18 months, driven by chipset advancements and regulatory spectrum approvals. Vendors increasingly emphasize AI-powered traffic analytics, zero-trust security frameworks, and seamless coexistence with private 5G networks to strengthen competitive positioning.

Teltonika Networks

Sierra Wireless

Moxa Inc.

Cradlepoint

HPE Aruba Networking

MikroTik

TP-Link Industrial

Westermo Network Technologies

Lantronix

Peplink

Robustel

The WiFi 7 Industrial Routers market is shaped by breakthrough enhancements in wireless throughput, latency optimization, and spectrum efficiency. WiFi 7 supports 320 MHz channel bandwidth, doubling the spectrum capacity of WiFi 6E and enabling theoretical speeds exceeding 40 Gbps. Multi-Link Operation allows simultaneous data transmission across 2.4 GHz, 5 GHz, and 6 GHz bands, improving throughput stability by up to 34% in high-density industrial deployments.

Deterministic low-latency scheduling reduces jitter below 5 milliseconds, supporting real-time robotics and automated guided vehicle fleets operating with millisecond-level precision. Advanced 4K-QAM modulation increases data density by approximately 20% compared to previous standards. Ruggedized industrial router models incorporate IP67 protection, wide voltage tolerance between 9V–48V DC, and extended temperature ranges from –40°C to 75°C.

AI-driven traffic optimization engines embedded within next-generation firmware improve packet prioritization efficiency by 21%, while WPA3 Enterprise encryption enhances wireless security posture. Time-Sensitive Networking integration enables precise synchronization across distributed industrial systems exceeding 10,000 connected endpoints. Edge-computing modules integrated into industrial routers process up to 15,000 sensor data streams per minute, enabling predictive maintenance analytics and reducing network congestion by 18%. These technological advancements position WiFi 7 Industrial Routers as foundational infrastructure for smart factories and industrial IoT ecosystems.

• In September 2024, Huawei introduced enterprise-grade WiFi 7 access solutions supporting 320 MHz bandwidth and Multi-Link Operation, enhancing industrial wireless throughput and stability for high-density manufacturing environments. Source: www.huawei.com

• In November 2024, Cisco expanded its WiFi 7 portfolio with industrial-capable networking hardware designed to support secure, high-capacity deployments in large enterprise and manufacturing campuses. Source: www.cisco.com

• In March 2025, Advantech launched new rugged WiFi 7 industrial routers engineered for extended temperature ranges and advanced cybersecurity features, targeting smart factory and transportation applications. Source: www.advantech.com

• In January 2025, HPE Aruba Networking unveiled enhanced WiFi 7 infrastructure solutions optimized for high-performance industrial connectivity and AI-driven traffic management. Source: www.hpe.com

The WiFi 7 Industrial Routers Market Report provides comprehensive analysis across router types, application domains, end-user industries, and regional adoption patterns. The scope includes single-band, dual-band, and tri-band industrial routers supporting 6 GHz spectrum and Multi-Link Operation capabilities. Applications assessed encompass smart manufacturing, semiconductor fabrication, automotive production, energy & utilities, transportation & logistics, mining, and oil & gas operations.

Geographic coverage spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with detailed country-level insights for China, the United States, Germany, Japan, Brazil, UAE, and Saudi Arabia. The report evaluates installation density across more than 7,000 smart factories worldwide and measures metrics such as IoT endpoint connectivity levels, deterministic latency performance, encrypted wireless adoption rates, and private 5G coexistence strategies.

Industry focus areas include robotics-enabled assembly lines, AI-powered quality inspection, predictive maintenance systems, and warehouse automation networks. Emerging segments such as edge-AI-integrated routers, zero-trust security architectures, and time-sensitive networking-enabled wireless backbones are examined. Quantitative insights include device density per facility, throughput performance benchmarks, spatial stream configurations, and ruggedization standards adoption. This structured scope enables manufacturers, industrial automation providers, telecom vendors, and infrastructure investors to align strategic decisions with next-generation industrial wireless transformation initiatives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 87.8 Million |

|

Market Revenue in 2033 |

USD 974.4 Million |

|

CAGR (2026 - 2033) |

35.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Router Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Huawei Technologies, Cisco Systems, Advantech, Teltonika Networks, Sierra Wireless, Moxa Inc., Cradlepoint, HPE Aruba Networking, MikroTik, TP-Link Industrial, Westermo Network Technologies, Lantronix, Peplink, Robustel |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |