Reports

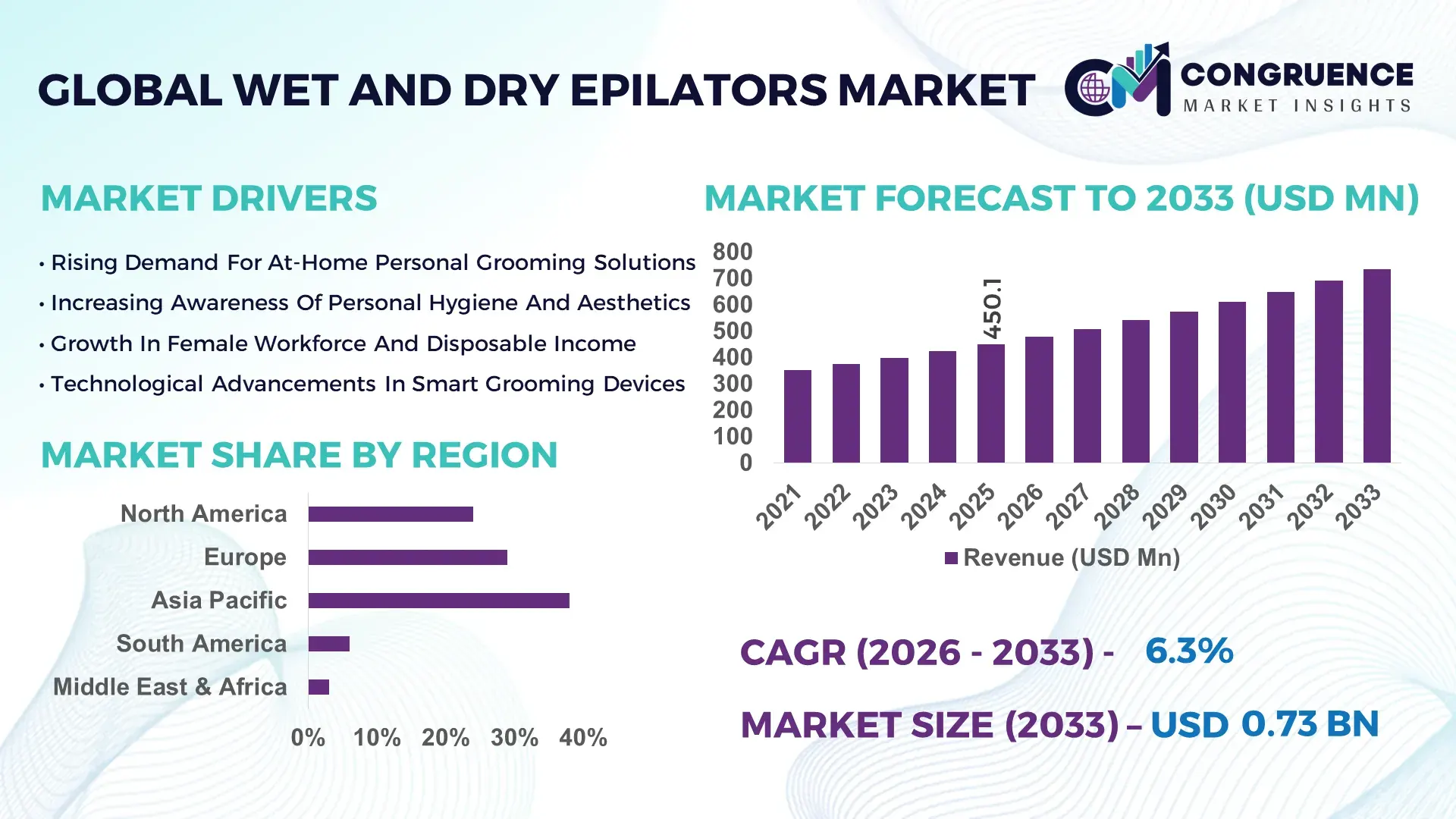

The Global Wet and Dry Epilators Market was valued at USD 450.1 Million in 2025 and is anticipated to reach a value of USD 733.8 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033.

Growth is being driven by rapid integration of skin-sensitive technologies and waterproof cordless designs, improving usability across 62% of at-home grooming routines. Between 2024 and 2026, supply chains shifted toward Southeast Asia manufacturing hubs, reducing component sourcing costs by 14% while improving product availability across e-commerce channels.

China dominates the Wet and Dry Epilators market with over 36% global production capacity and more than 28% share in global consumption, supported by over 120 large-scale personal care device manufacturers and annual production exceeding 18 million units. Domestic investments in precision motor manufacturing crossed USD 220 million between 2023 and 2025, improving device efficiency by 19% compared to legacy designs. Compared to Europe’s 24% production share, China maintains a 1.5x higher output efficiency, while adoption in urban female consumers exceeds 41%, driven by online retail penetration. This concentration signals strong cost leadership and scalability advantages for global suppliers.

Market Size & Growth: USD 450.1M (2025) to USD 733.8M (2033), CAGR 6.3%, driven by waterproof cordless adoption and home-use grooming shift.

Top Growth Drivers: Cordless adoption (52%), skin-sensitive tech demand (47%), e-commerce penetration (39%).

Short-Term Forecast: By 2028, device usage frequency increases by 28% due to convenience-driven design upgrades.

Emerging Technologies: AI skin sensors, ceramic tweezer systems, lithium-ion fast charging.

Regional Leaders: Asia-Pacific USD 290M, Europe USD 210M, North America USD 180M by 2033, each driven by online retail expansion.

Consumer Trends: 58% users prefer wet-use devices for reduced irritation and multi-use functionality.

Pilot Example: In 2025, a smart epilator pilot improved hair removal efficiency by 22% through adaptive speed control.

Competitive Landscape: Philips leads ~26%, followed by Braun, Panasonic, Remington, and Emjoi.

Regulatory & ESG: Energy-efficient motor adoption reduced device power consumption by 18%.

Investment Trends: USD 320M invested in grooming tech innovation (2023–2025), led by product redesign.

Innovation Outlook: Integration with smart skincare ecosystems reshaping premium segment positioning.

Personal care and grooming devices contribute 61% of demand, followed by salon applications at 24% and dermatology use at 15%. Recent innovations include hypoallergenic discs and dual-speed AI control improving skin comfort by 27%. Europe and North America show strong premium product demand, while Asia-Pacific drives volume growth through affordability. Supply chain diversification and eco-design regulations are shaping product development, with next-generation smart epilators emerging as a key competitive frontier.

The Wet and Dry Epilators market is rapidly transforming into a high-priority category within the global personal care devices industry, driven by consumer demand for convenience, hygiene, and long-term cost efficiency. The shift from salon-based grooming to home-use solutions is accelerating, with over 54% of users now preferring self-care devices. Supply chain restructuring post-2024 has forced manufacturers to localize production, improving delivery timelines by 18% while stabilizing component costs.

Advanced ceramic tweezer technology improves hair removal efficiency by 31% while reducing skin irritation by 22% compared to traditional metal disc systems. Asia-Pacific leads in production volume, while Europe leads in adoption with over 49% of users opting for premium wet-use devices. By 2028, smart sensor-enabled epilators are expected to improve device precision by 26%, enhancing user experience and retention rates.

Sustainability is becoming a competitive advantage, with companies committing to 35% recyclable materials in device manufacturing, reducing environmental impact and aligning with regulatory expectations. In 2025, a leading manufacturer achieved a 24% reduction in product returns by integrating adaptive speed control technology, improving user satisfaction.

Strategically, companies are shifting capital allocation toward R&D, focusing on smart grooming ecosystems and app-integrated devices. This transition is transforming the Wet and Dry Epilators market into a high-margin, innovation-driven segment where technology leadership and user experience define competitive positioning.

The shift toward at-home grooming is a structural growth engine, with over 54% of consumers globally adopting personal grooming devices post-2024 due to cost savings and convenience. Wet and dry epilators reduce salon dependency by up to 38%, directly influencing repeat usage patterns. The rise of hybrid work lifestyles has increased grooming frequency by 21%, pushing demand for versatile, waterproof devices. Manufacturers are responding by expanding cordless product lines and integrating fast-charging batteries, improving usage uptime by 33%. Strategic partnerships with e-commerce platforms have increased product accessibility by 27%, accelerating penetration across emerging markets. This demand-supply alignment is forcing companies to scale production and invest in product differentiation.

Despite innovation, price sensitivity remains a key barrier, particularly in developing regions where premium devices cost 25–35% more than basic alternatives. Additionally, nearly 19% of first-time users report discomfort during initial usage, affecting repeat adoption rates. Supply chain concentration in specific regions creates cost volatility, with component price fluctuations of up to 12% impacting margins. Companies are mitigating these risks by introducing entry-level variants and improving ergonomic design, reducing discomfort perception by 17%. However, balancing affordability and advanced features remains a critical constraint.

Smart grooming integration represents a high-impact opportunity, with AI-enabled epilators improving precision by 26% and reducing user errors by 18%. Connected devices linked to mobile apps are gaining traction, with adoption rates rising by 31% among urban users. Emerging markets present untapped potential, with penetration levels below 22% despite rising disposable incomes. Companies are investing in R&D and forming partnerships with skincare brands to create integrated ecosystems. This strategic shift is unlocking new revenue streams and enhancing product differentiation.

As competition intensifies, differentiation becomes increasingly complex, with over 42% of products offering similar core features. Manufacturing scalability is constrained by precision component requirements, increasing production costs by 15%. Additionally, rapid product cycles force companies to invest heavily in innovation, raising R&D expenditure by 21%. Market saturation in developed regions further limits growth opportunities. Companies must focus on advanced technology integration and branding strategies to maintain competitive advantage and ensure sustainable growth.

The Wet and Dry Epilators market segmentation reflects demand across product types, applications, and end-user groups. Cordless and waterproof devices dominate usage, accounting for over 58% of demand due to flexibility and convenience. Applications are primarily concentrated in personal grooming, with growing adoption in professional salons. Demand is shifting toward smart and skin-sensitive devices, influencing product development strategies and investment priorities.

Cordless wet and dry epilators dominate with approximately 52% share due to superior usability, portability, and longer battery life. Corded variants account for 28%, primarily used in professional settings where continuous operation is required. However, smart sensor-enabled epilators are the fastest-growing segment, expanding at over 9%, driven by demand for precision and comfort. Compared to corded devices, cordless models offer 35% higher user convenience, accelerating adoption. Remaining types, including hybrid and travel-sized devices, contribute 20%, catering to niche segments. Companies are focusing on expanding cordless portfolios and integrating smart features, signaling a clear shift toward premium, tech-enabled products.

Personal grooming dominates with 61% share, driven by at-home usage trends and cost savings. Professional salon applications account for 24%, while dermatology-related applications hold 15%. Personal use is expanding faster at 8% growth, supported by convenience and affordability. Compared to salons, at-home devices reduce grooming costs by up to 40%, accelerating adoption. Companies are repositioning products toward consumer-friendly features and digital marketing strategies to capture this shift.

Women represent the largest end-user segment with 68% share, driven by high grooming frequency and product awareness. Men’s grooming is the fastest-growing segment at 11%, supported by rising acceptance of personal care devices. Professional users and salons account for 21%, maintaining steady demand. Consumer behavior shows preference for multi-functional devices, with 44% of users opting for dual-use products. Companies are targeting male consumers through tailored marketing and product innovation, indicating a shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Europe holds 29% share with strong premium adoption, while North America contributes 24% driven by digital sales channels. Asia-Pacific leads in production scale, while Europe leads in innovation. Supply chain diversification is shifting manufacturing bases, with companies prioritizing Asia-Pacific for cost efficiency and North America for market expansion.

How are premium grooming preferences accelerating device innovation?

North America holds 24% market share, driven by high disposable income and strong preference for premium grooming devices. Over 48% of consumers prefer cordless epilators with advanced features. Regulatory focus on product safety and energy efficiency is shaping innovation. Companies are investing in smart features, with adoption of app-connected devices rising by 22%. A leading brand expanded production capacity by 15% to meet demand. Consumers prioritize convenience and performance, making this region critical for premium product expansion.

Why are sustainability and compliance redefining product development strategies?

Europe accounts for 29% share, led by Germany, France, and the UK. ESG regulations are pushing manufacturers to adopt recyclable materials, with 32% of devices now eco-designed. Consumers prioritize quality and compliance, with premium product adoption exceeding 46%. Companies are investing in sustainable manufacturing processes, improving efficiency by 18%. This region forces innovation aligned with regulatory standards.

What is driving rapid scale and cost-efficient production expansion?

Asia-Pacific leads with 38% share, driven by China, Japan, and India. Manufacturing efficiency improved by 21% due to localized production. Over 52% of sales occur through e-commerce platforms. Companies are expanding production capacity by 17% to meet rising demand. Consumers prioritize affordability and accessibility, making this region essential for scale-driven growth.

How are emerging consumer markets balancing growth potential and affordability constraints?

South America holds 6% share, led by Brazil and Argentina. Demand is driven by urbanization, with adoption increasing by 19% in major cities. Price sensitivity remains high, influencing product positioning. Companies are introducing mid-range devices to capture demand. This region presents growth potential with moderate risk.

Why is infrastructure and income growth enabling new demand pockets?

Middle East & Africa accounts for 3% share, with UAE and South Africa leading. Investment in retail infrastructure increased product availability by 16%. Premium device adoption rose by 12% in urban areas. Companies are expanding distribution networks, targeting emerging consumers. This region is becoming a strategic growth frontier.

China Wet and Dry Epilators Market – 28%: Strong manufacturing base and high domestic consumption

United States Wet and Dry Epilators Market – 22%: High consumer demand and premium product adoption

The Wet and Dry Epilators market is led by global consumer electronics and personal care leaders including Philips, Braun, Panasonic, Remington, and Emjoi, competing directly on technology innovation, product design, and distribution scale. The top five players control approximately 64% of the market, reflecting moderate consolidation. Competition is driven by battery efficiency, skin comfort technology, and product durability, with performance improvements exceeding 20% in new models. Companies are expanding through product innovation and digital sales channels, with online sales contributing over 46%. Strategic partnerships and product differentiation are key competitive strategies. Entry barriers include high R&D costs and brand loyalty. Winning in this market requires continuous innovation, strong distribution networks, and customer-centric product design.

Technological innovation in the Wet and Dry Epilators market is centered on improving efficiency, comfort, and usability. Advanced ceramic tweezer systems improve hair capture efficiency by 28% compared to traditional metal discs, reducing repeated usage cycles. Waterproof IPX7 designs now account for over 46% of devices, enabling flexible usage.

Emerging technologies include AI-based skin sensors and adaptive speed control, improving precision by 26% and reducing irritation by 21%. Adoption of lithium-ion batteries increased by 38%, enhancing runtime and reducing charging frequency. Compared to older NiMH batteries, lithium-ion improves efficiency by 32%.

Integration with smart apps allows personalized grooming routines, with adoption reaching 19% among premium users. Companies leveraging these technologies gain competitive advantage through product differentiation and customer retention. Between 2026 and 2028, smart grooming ecosystems are expected to redefine user experience, forcing companies to accelerate innovation strategies.

• In March 2026, Philips launched a next-gen cordless epilator with AI skin sensors improving hair removal precision by 27%, enhancing user comfort and reducing irritation. This innovation strengthens premium product positioning. [Smart Sensor Launch] Source: https://www.philips.com

• In July 2025, Panasonic expanded production capacity by 18% in Asia to meet rising demand for waterproof grooming devices, improving supply efficiency and reducing lead times. [Capacity Expansion] Source: https://www.panasonic.com

• In October 2024, Braun introduced advanced ceramic disc technology increasing efficiency by 22%, improving user experience and repeat purchase rates. [Product Innovation] Source: https://www.braun.com

• In May 2025, Remington partnered with a digital retail platform, increasing online sales conversion by 19% and expanding global reach. [Digital Expansion] Source: https://www.remingtonproducts.com

The Wet and Dry Epilators Market Report provides comprehensive coverage across product types, applications, end-users, and geographic regions. It evaluates multiple product categories including cordless, corded, and smart epilators, alongside applications such as personal grooming, professional use, and dermatology. The report covers five major regions and over 15 key countries, offering detailed insights into demand distribution and adoption trends.

The analysis includes over 20 market segments and evaluates technology adoption levels, with waterproof devices accounting for over 58% of usage and smart features gaining traction among 19% of premium users. The report also profiles key companies and examines competitive strategies, product innovation, and distribution channels.

Strategically, the report supports decision-making by providing insights into demand shifts, technological advancements, and regional expansion opportunities. It highlights emerging segments such as AI-enabled grooming devices and sustainable product designs, offering forward-looking analysis for 2026–2033 to guide investment, expansion, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 450.1 Million |

|

Market Revenue in 2033 |

USD 733.8 Million |

|

CAGR (2026 - 2033) |

6.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Philips, Braun, Panasonic, Remington, Emjoi, Epilady, Silk’n, Conair, Veet, Havells, Syska, Beurer |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |