Reports

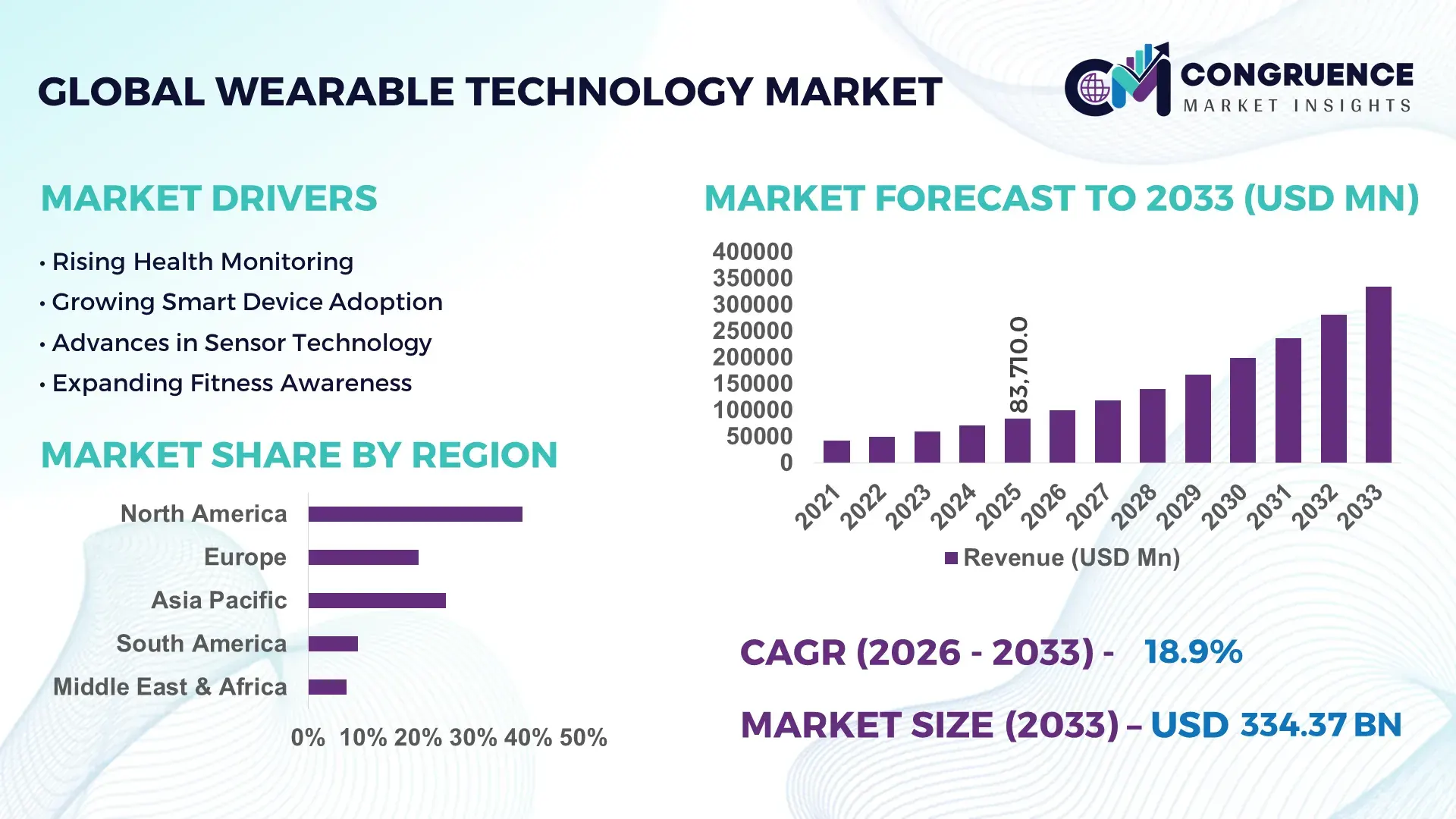

The Global Wearable Technology Market was valued at USD 83710 Million in 2025 and is anticipated to reach a value of USD 334373.75 Million by 2033 expanding at a CAGR of 18.9% between 2026 and 2033. AI-enabled health monitoring, advanced biometric sensing, enterprise wearable deployments, and growing integration with digital healthcare platforms are driving sustained market expansion.

The United States dominates the global wearable technology landscape with approximately 34% market share, supported by strong adoption across healthcare, consumer electronics, and connected fitness applications. More than 65% of premium wearable device usage is concentrated in North America, while China accounts for over 40% of global manufacturing capacity through its extensive electronics supply chain and semiconductor ecosystem. Ongoing U.S.-China technology competition continues to accelerate innovation in AI-powered sensors, low-power processors, and next-generation health monitoring capabilities.

Organizations investing in advanced wearable ecosystems, AI-driven analytics, and diversified production networks are strengthening competitive positioning across global high-growth opportunities.

Market Size & Growth: USD 83,710 Million in 2025 reaching USD 334,373.75 Million by 2033 at a CAGR of 18.9%, supported by AI-enabled health monitoring and connected healthcare ecosystems.

Top Growth Drivers: Health-monitoring adoption (+60%), enterprise wearable deployment (+25%), and AI sensor integration (+30%) remain the primary growth catalysts.

Short-Term Forecast: By 2028, battery efficiency is projected to improve by 20% while real-time data processing latency declines by 15%.

Emerging Technologies: AI analytics, edge computing, and advanced biosensors are improving monitoring accuracy by 25% and operational performance by 18%.

Regional Leaders: North America exceeds USD 110 Billion, Asia-Pacific surpasses USD 125 Billion, and Europe approaches USD 65 Billion with expanding digital health adoption.

Consumer/End-User Trends: More than 58% of wearable users actively track health metrics weekly, while ecosystem-based device usage exceeds 45%.

Pilot/Case Example: In 2026, enterprise wearable implementations improved workforce safety monitoring by 22% and reduced response times by 17%.

Competitive Landscape: Leading vendors collectively account for over 55% of global market share, focusing on premium health-centric wearable portfolios.

Regulatory & ESG Impact: Energy-efficiency requirements have improved device power performance by 12%, supporting longer product lifecycles.

Investment & Funding: Global investments exceed USD 18 Billion, driven by AI innovation, healthcare partnerships, and regional manufacturing expansion.

Innovation & Future Outlook: Smart rings, non-invasive biosensors, and AI health assistants are expected to increase user engagement by more than 30%.

Wearable technology adoption is expanding across digital health monitoring, fitness analytics, remote patient management, industrial workforce safety, and connected consumer electronics. Product innovation is centered on AI-powered biometric sensing, non-invasive diagnostic capabilities, and advanced low-power semiconductor architectures that improve performance by nearly 20%. Increasing supply-chain diversification and evolving digital health compliance standards are influencing product development priorities, creating a strong foundation for the strategic market analysis that follows.

Wearable technology has evolved from a consumer electronics category into a strategic platform supporting digital healthcare, workforce productivity, industrial safety, and connected ecosystems. Its importance is increasing as enterprises seek continuous real-time data collection and predictive insights to improve operational outcomes. A notable market shift is the growing localization of electronics manufacturing and component sourcing, reducing exposure to geopolitical disruptions while strengthening supply-chain resilience across key production hubs.

Technology advancement is improving device value propositions. AI-enabled wearable platforms can deliver health-monitoring accuracy improvements of nearly 25% compared with conventional fitness trackers while reducing manual data interpretation requirements by more than 30%. The United States leads premium wearable innovation and healthcare integration, whereas China maintains scale advantages through extensive manufacturing networks and sensor production capabilities. This contrast is accelerating competition in semiconductor optimization, battery efficiency, and advanced biosensing technologies.

Over the next two to three years, enterprise deployments are expected to expand significantly, with workforce safety monitoring and remote patient management among the fastest-growing applications. Companies are increasing investments in AI partnerships, digital health ecosystems, and specialized sensor development. Organizations that successfully integrate wearables into broader data-driven operating models will strengthen competitive positioning through improved decision-making, operational visibility, and long-term customer engagement.

The rapid adoption of AI-powered health monitoring is becoming the primary structural driver for wearable technology deployment. More than 60% of new premium wearable devices now include advanced biometric sensing capabilities, while health-focused applications account for over 45% of active device usage. In the United States, healthcare providers are increasingly integrating wearable-generated data into remote patient monitoring programs, improving clinical visibility and reducing routine intervention requirements. The emergence of digital health regulations and reimbursement frameworks is further accelerating adoption. In response, technology companies are expanding sensor innovation programs, forming healthcare partnerships, and investing in AI analytics platforms. A key operational insight is that data interoperability is becoming a competitive differentiator, allowing vendors to create higher-value ecosystems rather than competing solely on hardware performance.

Wearable technology manufacturers continue to face structural constraints related to semiconductor sourcing, advanced sensor availability, and battery component costs. Specialized sensors and low-power chipsets represent nearly 35% of device production costs, while supply disruptions can extend procurement lead times by 20% or more. China remains a critical supplier of several wearable components, creating exposure to trade policy changes and logistics volatility. These pressures directly affect product pricing strategies, inventory planning, and margin stability. Companies are mitigating risks through supplier diversification, localized assembly operations, and long-term procurement agreements. A notable strategic insight is that firms with vertically integrated component sourcing are achieving stronger operational predictability and faster product launch cycles than competitors dependent on fragmented supply networks.

Advanced biosensing technologies are opening high-value opportunities beyond traditional fitness tracking. Non-invasive health monitoring solutions are improving diagnostic capabilities by approximately 20%, while enterprise wearable adoption in industrial environments has increased by more than 25% over recent years. Japan and South Korea are accelerating investment in precision sensors, edge AI processing, and compact medical-grade wearable platforms. Emerging policy support for digital healthcare infrastructure is creating additional pathways for remote diagnostics and preventive care applications. Companies are expanding R&D programs, forming healthcare technology alliances, and building integrated software ecosystems around wearable data services. A non-obvious opportunity lies in subscription-based analytics models, where recurring software revenues can create stronger long-term profitability than device sales alone.

Long-term market expansion depends on solving data governance, cybersecurity, and interoperability challenges across increasingly connected device ecosystems. More than 70% of wearable deployments generate continuous personal or operational data streams, while cyber incidents targeting connected devices have increased by over 15% in recent years. In Germany and the United States, evolving data privacy requirements are raising compliance obligations for manufacturers and software providers. Integration complexity also increases when wearable platforms must communicate with healthcare systems, enterprise software, and cloud infrastructure. Companies are responding through encryption investments, cybersecurity partnerships, and standardized data architectures. A critical strategic insight is that trust, compliance readiness, and seamless ecosystem integration will become as important as hardware innovation in sustaining long-term competitive advantage.

AI-Powered Health Analytics Expansion: More than 55% of newly launched wearable devices now integrate AI-driven health analytics, while predictive monitoring accuracy has improved by nearly 25%. Healthcare providers in the United States are increasingly incorporating wearable-generated data into remote care workflows, reducing manual assessment requirements by over 15%. Companies are responding through software acquisitions, AI partnerships, and platform integration strategies that enhance data utility beyond traditional activity tracking.

Smart Ring Adoption Accelerates: Smart rings are emerging as a high-growth category, with shipment volumes increasing by over 35% and enterprise wellness deployments rising by approximately 20%. Miniaturized sensors and improved battery efficiency are enabling broader adoption among users seeking discreet monitoring solutions. Manufacturers are expanding production capacity, forming semiconductor partnerships, and diversifying product portfolios to capture demand as consumers shift toward lightweight wearable form factors.

Localized Supply Chain Strategies: Following component sourcing disruptions and ongoing geopolitical trade pressures, more than 30% of major wearable manufacturers have expanded regional assembly or supplier diversification programs. Companies are reducing dependency on single-country sourcing models while improving procurement resilience and inventory visibility. This operational shift is shortening lead-time volatility and helping firms maintain product availability during fluctuations in semiconductor and sensor supply conditions.

Enterprise Workforce Deployment Growth: Industrial wearable deployments have expanded by nearly 28% as manufacturers prioritize worker safety, operational visibility, and productivity optimization. Connected wearables are reducing incident response times by over 15% in monitored environments while supporting real-time workforce management. Organizations are scaling deployments through cloud-based platforms, automation integration, and strategic partnerships with software providers, transforming wearables into operational infrastructure rather than standalone hardware products.

Smartwatches remain the leading segment, accounting for approximately 45% of wearable technology deployments due to broad functionality, ecosystem integration, and strong compatibility with smartphones, health platforms, and enterprise applications. Their scalability and software-driven upgrade cycle continue to support sustained demand across both consumer and professional environments. Fitness Trackers retain relevance in cost-sensitive markets, particularly where basic activity monitoring and battery longevity remain priorities. Smart Glasses are gaining traction in industrial and field-service applications, where hands-free data access improves operational efficiency by nearly 20%.

Wearable Medical Devices represent the fastest-growing segment as healthcare providers increasingly adopt continuous monitoring solutions and remote patient management tools. Adoption rates for connected medical wearables have expanded by more than 30% in digitally advanced healthcare systems. Smart Clothing is progressing through sports performance and rehabilitation applications, supported by embedded sensor innovation. In response, companies are prioritizing medical-grade validation, AI integration, and strategic healthcare partnerships, shifting investment toward higher-value data ecosystems rather than standalone hardware differentiation.

Fitness & Wellness remains the largest application segment, supported by widespread consumer adoption of activity tracking, sleep monitoring, and personalized health insights. More than 60% of wearable device users actively engage with wellness-related features, making this category the primary demand center. Consumer Electronics continues to provide significant deployment scale through integration with broader connected-device ecosystems. Sports Performance applications are expanding steadily as professional organizations and athletes utilize real-time biometric monitoring to improve training outcomes and recovery management.

Healthcare Monitoring is the fastest-growing application as healthcare systems increasingly deploy wearables for chronic disease management, remote diagnostics, and preventive care initiatives. Adoption of connected patient-monitoring solutions has increased by over 25%, while data-driven clinical workflows continue to gain acceptance. Industrial Safety applications are becoming operationally critical within manufacturing and energy sectors, where wearable-enabled monitoring improves workforce visibility and incident management. Military & Defense deployments are also advancing through soldier monitoring and situational awareness programs. Companies are expanding cloud integration, analytics capabilities, and healthcare interoperability to support these evolving application requirements.

Consumer Electronics remains the dominant end-user segment due to extensive deployment scale, established retail channels, and continuous product innovation cycles. Nearly 65% of wearable device shipments are linked to consumer-oriented ecosystems, supported by demand for health tracking, connectivity, and lifestyle applications. Sports & Fitness users continue to represent a strong customer base as performance analytics and recovery monitoring become increasingly sophisticated. Retail & E-commerce channels are also expanding their influence through direct-to-consumer sales models and personalized product recommendations.

Healthcare is emerging as the fastest-growing end-user segment, driven by remote patient monitoring adoption, digital healthcare modernization, and increasing use of connected diagnostic tools. Healthcare-related wearable deployments have expanded by more than 30% in several advanced healthcare markets. Manufacturing organizations are integrating wearables into workforce management and safety programs, while Defense Organizations continue investing in mission-critical monitoring technologies. Companies are adapting through sector-specific product customization, healthcare partnerships, subscription-based analytics services, and integrated platform development to strengthen long-term customer retention and competitive differentiation.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.2% between 2026 and 2033.

Healthcare-Centric Digital Wearable Expansion

North America maintains leadership through strong healthcare digitization, premium consumer electronics adoption, and enterprise wearable integration. The region represents approximately 38% of global wearable deployments, supported by mature cloud infrastructure and widespread AI-enabled health monitoring adoption. More than 65% of connected health wearable implementations are concentrated across the United States and Canada. Healthcare providers are increasingly integrating wearable-generated data into remote care workflows, while enterprise users continue expanding workforce safety monitoring programs. Strategic partnerships between device manufacturers, software providers, and healthcare networks are accelerating ecosystem development. Continued investment in advanced biosensors and digital health platforms is strengthening the region’s position in high-value wearable applications.

United States Market Outlook: The United States remains the largest country market due to its advanced healthcare infrastructure, strong technology ecosystem, and high consumer adoption rates. More than 70% of premium wearable device usage within North America originates from the country. Digital health programs, remote patient monitoring initiatives, and enterprise wellness deployments continue expanding. Technology firms are prioritizing AI-powered analytics, healthcare interoperability, and medical-grade wearable development, creating a competitive environment focused on long-term ecosystem value rather than hardware differentiation alone.

Regulatory-Led Health Technology Integration

Europe is strengthening its position through digital healthcare modernization, strict data governance frameworks, and increasing adoption of connected wellness technologies. The region accounts for nearly 25% of global wearable deployments and demonstrates strong demand for medical-grade monitoring solutions. Healthcare institutions are accelerating wearable integration into preventive care and chronic disease management programs. Sustainability considerations are also influencing product design, battery optimization, and lifecycle management strategies. Cross-border technology collaborations and healthcare innovation programs are supporting wider deployment across major European economies, creating favorable conditions for advanced wearable ecosystems.

Germany Market Outlook: Germany leads the European market through its strong healthcare technology infrastructure, industrial digitization initiatives, and advanced manufacturing capabilities. Connected health deployments continue to expand across hospitals and outpatient care networks, while industrial organizations increasingly adopt wearable-enabled workforce monitoring solutions. The country's emphasis on data security and regulatory compliance supports demand for high-quality wearable platforms. Continued investment in medical technology innovation and precision engineering strengthens Germany’s role as a key hub for wearable technology development and deployment.

Manufacturing Scale and Mass Adoption Leadership

Asia-Pacific is the fastest-expanding wearable technology market, supported by extensive electronics manufacturing capacity, rising consumer adoption, and rapid digitalization initiatives. The region accounts for more than 35% of global wearable device production, with China, South Korea, and Japan serving as critical manufacturing and innovation centers. Production efficiency improvements and localized supply-chain networks continue supporting large-scale deployment. Increasing smartphone penetration, digital healthcare investment, and affordable device availability are expanding addressable demand. Companies are scaling regional manufacturing facilities and strengthening semiconductor partnerships to improve competitiveness and supply resilience.

China Market Outlook: China remains the most influential country market due to its dominant electronics manufacturing ecosystem and extensive component supply chain. The country contributes more than 40% of global wearable device production capacity and continues investing in sensor technologies, AI integration, and semiconductor development. Domestic brands are expanding aggressively across health monitoring and smart lifestyle applications. Strong manufacturing efficiency, export capability, and technology innovation provide China with a significant operational advantage across the global wearable technology value chain.

Consumer Health Adoption Drives Demand

South America is experiencing steady wearable technology adoption as digital health awareness, fitness engagement, and connected consumer electronics usage increase. The region represents a smaller share of global deployments but demonstrates rising demand for affordable health-monitoring solutions. Improvements in mobile connectivity and digital payment infrastructure are supporting broader device accessibility. Market participants are expanding distribution partnerships and localized sales channels to improve penetration. Infrastructure constraints and import dependency continue influencing pricing structures; however, growing interest in preventive healthcare and wellness applications supports long-term market development.

Brazil Market Outlook: Brazil leads the South American market through its large consumer base, expanding digital ecosystem, and growing healthcare technology adoption. Wearable device usage is increasing across urban centers, particularly in fitness monitoring and connected wellness applications. E-commerce platforms are improving product accessibility, while healthcare providers are exploring remote monitoring initiatives. Technology vendors are strengthening local partnerships and distribution networks to improve affordability and accelerate adoption across both consumer and healthcare segments.

Digital Transformation and Healthcare Modernization

The Middle East & Africa market is advancing through healthcare modernization programs, smart city initiatives, and increasing investment in connected technologies. Adoption remains concentrated in higher-income economies where digital infrastructure development supports wearable integration. Healthcare organizations are deploying connected monitoring solutions to improve patient engagement and operational efficiency. Enterprise demand is also increasing within workforce safety and productivity applications. Strategic investments in digital transformation programs are supporting broader adoption while creating opportunities for technology providers focused on healthcare and enterprise solutions.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market within the region due to strong digital transformation investments and healthcare modernization objectives. Government-backed technology initiatives are accelerating deployment of connected healthcare solutions and smart infrastructure projects. Wearable technology adoption is increasing across health monitoring, wellness management, and enterprise applications. Continued investment in digital healthcare ecosystems, cloud infrastructure, and AI-enabled services is positioning the country as a leading regional adopter of advanced wearable technologies.

The wearable technology market is characterized by competition between Apple, Samsung Electronics, Garmin, Huawei, Xiaomi, and Fitbit-focused ecosystem providers, alongside specialized medical wearable innovators and cost-efficient device manufacturers. The top five players collectively control approximately 58% of global market activity, creating a moderately concentrated structure. Competition is centered on ecosystem integration, AI-enabled health analytics, battery efficiency, sensor accuracy, and supply-chain control. Premium vendors compete through technology differentiation, where health-monitoring accuracy improvements exceeding 20% and battery performance gains above 15% directly influence purchasing decisions. Chinese manufacturers challenge established leaders through rapid product cycles and cost advantages, while healthcare-focused companies compete through clinical-grade functionality and regulatory compliance. Strategic partnerships with healthcare providers, semiconductor suppliers, and cloud platform operators are increasingly shaping competitive positioning. Vertical integration and localized manufacturing expansion are strengthening operational resilience. Success depends on combining advanced analytics, trusted health data ecosystems, efficient production networks, and continuous innovation that delivers measurable user value.

Apple Inc.

Samsung Electronics Co., Ltd.

Garmin Ltd.

Huawei Technologies Co., Ltd.

Xiaomi Corporation

Google LLC

Sony Group Corporation

Polar Electro Oy

Suunto Oy

Oura Health Ltd.

Withings SA

Amazfit (Zepp Health Corporation)

Dexcom Inc.

Masimo Corporation

Wearable technology is increasingly defined by AI-enabled biometric sensing, edge computing, and advanced health-monitoring platforms. More than 55% of newly launched premium wearables incorporate AI-driven analytics that improve health-data interpretation accuracy by approximately 20% while reducing manual data review requirements by 15%. Continuous monitoring sensors for heart rate, sleep quality, blood oxygen, and activity tracking are now deployed across over 60% of connected wearable ecosystems. This technology shift is enabling healthcare providers, employers, and consumer brands to generate actionable insights, creating stronger user engagement and recurring software-driven value beyond hardware sales.

Emerging technologies are centered on non-invasive biosensing, smart rings, and low-power semiconductor architectures. Compared with conventional fitness trackers, next-generation AI-enabled wearables deliver nearly 25% higher predictive monitoring accuracy and approximately 18% greater operational efficiency through real-time analytics. Adoption of compact wearable form factors has increased by more than 30% as users prioritize continuous monitoring without sacrificing comfort. Companies are responding through sensor innovation partnerships, healthcare ecosystem integration, and specialized chip development that improves battery performance and data-processing speed.

Between 2026 and 2028, disruptive technologies including digital biomarkers, AI health assistants, and medical-grade wearable platforms will reshape competitive dynamics. Organizations with proprietary sensor technology and healthcare interoperability capabilities are expected to gain significant advantages as enterprise and clinical deployments expand. Firms that act now through AI investment, ecosystem partnerships, and advanced biosensor development will secure stronger long-term positioning in data-driven wearable technology markets.

September 2025 – Apple Inc. introduced Apple Watch Series 11 featuring hypertension notifications, sleep score capabilities, and a display engineered to be 2x more scratch-resistant. The upgrade strengthened Apple’s position in premium health-focused wearables while expanding advanced monitoring functionality. Source: apple.com

September 2025 – Apple Inc. launched Apple Watch Ultra 3 with satellite communications, enhanced health insights, and 42-hour battery life, extending performance for outdoor and professional users. The development reinforced competitive differentiation through safety-focused connectivity and endurance-oriented wearable innovation.

March 2026 – Garmin Ltd. announced integration with Natural Cycles, enabling compatible smartwatches to provide fertility insights through skin-temperature tracking across five supported device families. The partnership expanded Garmin’s presence in digital health applications and strengthened healthcare ecosystem relevance. Source: garmin.com

September 2025 – Apple Inc. introduced Apple Watch SE 3 with an Always-On display, fast charging, and advanced health capabilities powered by the S10 chipset platform. The launch improved accessibility to premium wearable functionality and broadened market reach across value-focused consumer segments.

This report provides comprehensive analysis of the wearable technology market across major device categories including Smartwatches, Fitness Trackers, Smart Glasses, Smart Clothing, and Wearable Medical Devices. The study evaluates deployment trends across Fitness & Wellness, Healthcare Monitoring, Consumer Electronics, Industrial Safety, Sports Performance, and Military & Defense applications. End-user assessment covers Healthcare, Consumer Electronics, Sports & Fitness, Manufacturing, Defense Organizations, and Retail & E-commerce sectors, where health-focused and connected-device deployments account for more than 60% of current adoption activity.

The report delivers detailed regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining technology developments such as AI-enabled analytics, advanced biosensors, edge computing, and non-invasive monitoring platforms. Analysis includes competitive positioning, operational deployment patterns, product innovation strategies, and evolving ecosystem partnerships. Strategic insights support investment prioritization, expansion planning, product development decisions, and identification of emerging opportunities expected to influence market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 83710 Million |

|

Market Revenue in 2033 |

USD 334373.75 Million |

|

CAGR (2026 - 2033) |

18.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple Inc., Samsung Electronics Co., Ltd., Garmin Ltd., Huawei Technologies Co., Ltd., Xiaomi Corporation, Google LLC, Sony Group Corporation, Polar Electro Oy, Suunto Oy, Oura Health Ltd., Withings SA, Amazfit (Zepp Health Corporation), Dexcom Inc., Masimo Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |