Reports

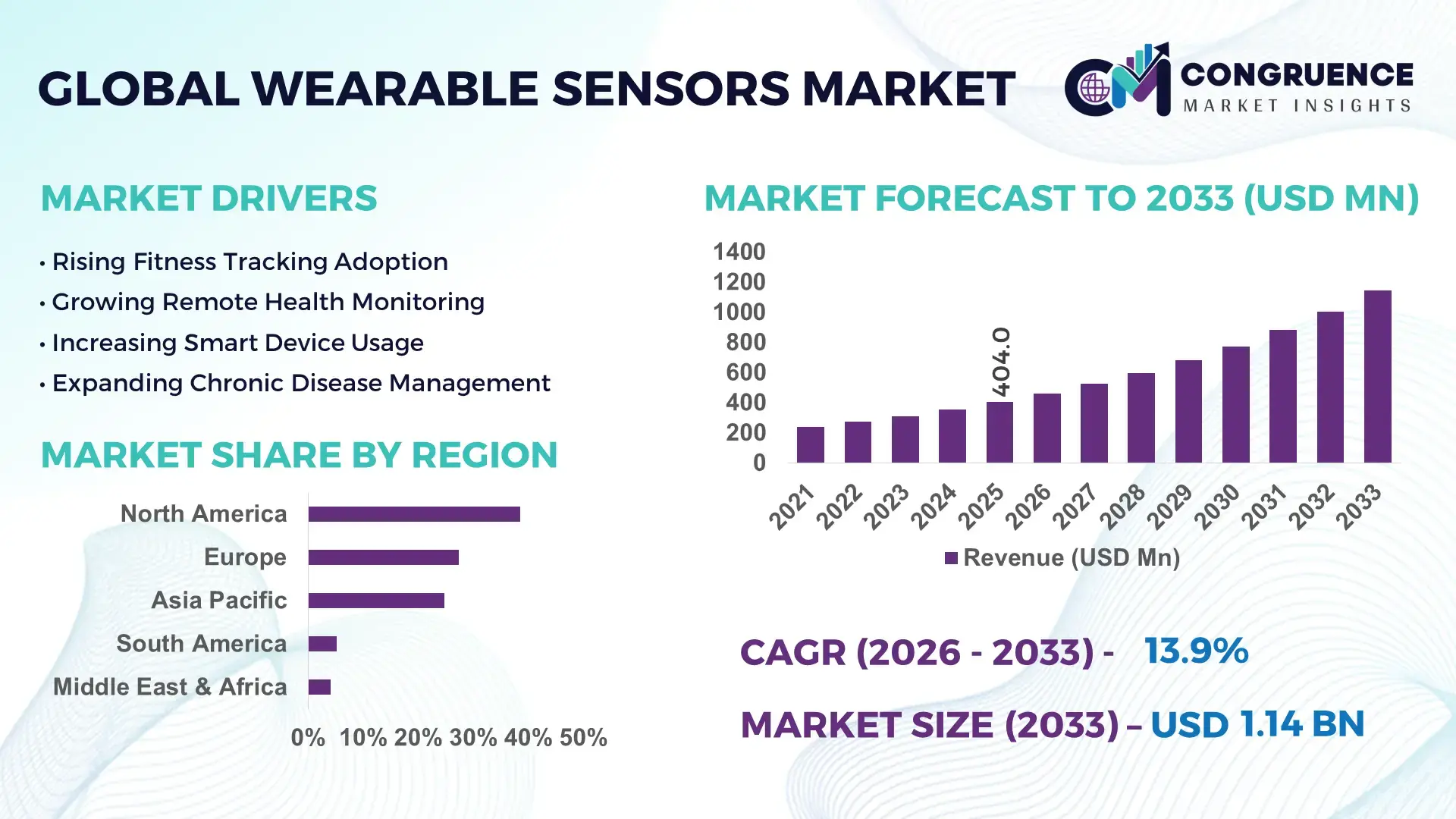

The Global Wearable Sensors Market was valued at USD 404.0 Million in 2025 and is anticipated to reach a value of USD 1,144.4 Million by 2033 expanding at a CAGR of 13.9% between 2026 and 2033. Growth is being driven by rapid integration of biosensing technologies in continuous health monitoring devices, increasing adoption of AI-enabled wearables, and expanding deployment of sensor-based remote patient management platforms.

The United States remains the dominant country in the wearable sensors ecosystem, accounting for nearly 34% of global demand, supported by over USD 8 billion in annual digital health investments and strong adoption across healthcare, fitness, and defense applications. Compared with Germany, where wearable healthcare penetration remains below 28%, U.S. adoption exceeds 43% among adults. Ongoing digital health initiatives and post-pandemic remote monitoring expansion continue to accelerate sensor integration across medical-grade wearable platforms.

Strategically, companies that combine advanced sensing accuracy, AI analytics, and healthcare interoperability standards are positioned to secure long-term competitive advantage across high-value wearable ecosystems.

Market Size & Growth: USD 404.0 Million in 2025, reaching USD 1,144.4 Million by 2033 at 13.9% CAGR, supported by expanding medical-grade wearable deployments and AI-driven health analytics.

Top Growth Drivers: Remote patient monitoring adoption (+41%), fitness wearable penetration (+37%), and biosensor integration across healthcare devices (+32%) continue reshaping demand patterns.

Short-Term Forecast: By 2028, sensor power efficiency is projected to improve by 25% while device calibration costs decline by nearly 18%.

Emerging Technologies: AI-enabled biosensors, flexible printed electronics, and edge-computing wearables are improving diagnostic precision by over 30%.

Regional Leaders: North America (~USD 390 Million by 2030), Asia-Pacific (~USD 320 Million), and Europe (~USD 250 Million), each benefiting from digital healthcare adoption and manufacturing expansion.

Consumer/End-User Trends: More than 45% of wearable users actively track health metrics beyond fitness, accelerating demand for multi-parameter sensing.

Pilot/Case Example: In 2024, hospital remote-monitoring programs using wearable biosensors reduced patient readmissions by approximately 22%.

Competitive Landscape: Leading suppliers control nearly 38% of market activity, with key participants including Apple, Fitbit, Garmin, Medtronic, and Philips.

Regulatory & ESG Impact: Medical wearable compliance programs improved device validation efficiency by roughly 20% across regulated healthcare applications.

Investment & Funding: Digital health and wearable technology investments exceeded USD 10 billion globally, supported by strategic partnerships and manufacturing localization.

Innovation & Future Outlook: Next-generation sweat-sensing, non-invasive glucose monitoring, and advanced biometric platforms are strengthening high-growth wearable ecosystems amid global supply-chain diversification.

Wearable sensors are becoming central to preventive healthcare, sports performance monitoring, industrial worker safety, and connected wellness applications. Recent innovations include flexible biosensors, skin-integrated electronics, and AI-powered biometric analytics that improve real-time data accuracy. More than 40% of new wearable product launches now incorporate advanced health-monitoring functions. Simultaneously, semiconductor localization initiatives and stricter healthcare data standards are reshaping product development strategies, setting the stage for broader strategic market evolution.

Wearable sensors have evolved from consumer fitness accessories into critical components of digital healthcare, workforce safety, and connected industrial ecosystems. Organizations increasingly view wearable-generated data as a strategic asset for improving operational visibility, patient outcomes, and personalized service delivery. Simultaneously, healthcare digitization programs and semiconductor supply-chain restructuring are encouraging broader adoption of advanced sensing platforms across multiple industries.

Modern wearable sensors deliver significantly higher functionality than legacy monitoring systems. Continuous biometric monitoring solutions can improve health-data collection frequency by more than 60% while reducing manual intervention requirements by approximately 35%. The United States leads commercialization through strong digital health infrastructure and large-scale deployments, while China is accelerating manufacturing scale and component integration through extensive electronics production capabilities. This contrast highlights the growing importance of balancing innovation leadership with production efficiency.

Over the next two to three years, adoption of multi-sensor wearable platforms is expected to accelerate across remote patient monitoring, occupational safety, and sports analytics applications. Healthcare providers increasingly deploy wearable-based monitoring programs to reduce unnecessary hospital visits and improve care continuity. In response, technology companies are expanding partnerships with healthcare institutions, semiconductor manufacturers, and software providers. Organizations that secure advanced sensing capabilities, interoperable data platforms, and scalable deployment networks will strengthen competitive positioning and establish long-term relevance in the evolving connected-device landscape.

The increasing deployment of continuous health monitoring platforms is creating strong momentum for wearable sensor adoption. More than 43% of U.S. adults now use at least one connected health-tracking device, while remote patient monitoring utilization has expanded by over 35% since healthcare digitization initiatives accelerated. Advanced biosensors capable of tracking heart rate variability, oxygen saturation, and sleep quality are becoming standard features in next-generation devices. The expansion of telehealth infrastructure and reimbursement support for remote monitoring programs has further strengthened demand. In response, leading manufacturers are investing in AI-enabled sensing technologies, expanding clinical partnerships, and developing medical-grade wearable solutions. A notable strategic shift involves integrating healthcare analytics directly into wearable ecosystems, enabling companies to move beyond hardware sales toward recurring data-driven service models.

Wearable sensor deployment continues to face structural limitations linked to component pricing volatility and fragmented interoperability standards. Sensor modules and advanced semiconductor components can represent over 30% of total device production costs, while certification requirements extend commercialization timelines by nearly 20%. Dependence on specialized chip manufacturing remains concentrated in a limited number of supply hubs, creating procurement vulnerabilities during periods of geopolitical uncertainty. Data compatibility issues across healthcare platforms and operating systems also reduce deployment efficiency for enterprise users. To mitigate these constraints, manufacturers are localizing supply chains, negotiating long-term semiconductor procurement agreements, and adopting standardized communication protocols. Companies that successfully reduce integration complexity gain a measurable advantage in deployment speed and ecosystem scalability.

The convergence of artificial intelligence, biosensing, and predictive healthcare presents a significant opportunity for wearable sensor providers. AI-assisted analytics can improve anomaly detection accuracy by more than 30%, while preventive healthcare programs have demonstrated reductions in avoidable clinical interventions exceeding 20%. Countries such as India and Brazil are rapidly expanding digital health infrastructure, creating untapped demand for affordable wearable monitoring solutions. Emerging technologies including non-invasive glucose monitoring, sweat-based biochemical sensing, and flexible electronic skin platforms are opening new application areas beyond traditional fitness tracking. Companies are increasing R&D investments, forming healthcare partnerships, and building integrated digital ecosystems to capitalize on these opportunities. A notable strategic advantage lies in combining sensor hardware with subscription-based analytics services, creating higher-value recurring revenue streams and stronger customer retention.

As wearable sensors generate increasing volumes of sensitive biometric information, maintaining secure, scalable, and reliable data infrastructure has become a critical challenge. Healthcare-related wearable data traffic has increased by more than 45% over the past few years, while cybersecurity incidents targeting connected medical devices continue to rise. Regulatory frameworks governing health-data privacy are becoming more stringent, increasing compliance complexity for multinational deployments. In addition, ensuring consistent sensor performance across diverse user environments requires substantial validation and calibration efforts. Companies must invest in encryption technologies, cloud-security architectures, and advanced validation frameworks to maintain trust and deployment consistency. Organizations that successfully combine cybersecurity resilience, regulatory compliance, and data interoperability will establish a durable operational advantage in the increasingly connected wearable technology landscape.

AI-Powered Health Analytics Expansion Wearable sensor platforms are increasingly embedding edge AI capabilities to process biometric data directly on devices, reducing cloud dependency by nearly 30% and improving response times by over 40%. Healthcare providers in the United States are integrating AI-enabled wearables into remote monitoring workflows, while device manufacturers are expanding software partnerships to strengthen predictive analytics. The shift is improving diagnostic efficiency and lowering data-processing costs across connected health ecosystems.

Flexible Electronics Gaining Traction Flexible and skin-integrated sensors are moving from pilot programs into commercial deployment, with adoption across healthcare and sports applications increasing by approximately 25% over the past two years. Improvements in stretchable materials have enhanced sensor durability by nearly 35%, enabling longer operating cycles. Companies are scaling advanced manufacturing capabilities and collaborating with materials specialists to accelerate commercialization while addressing comfort and usability requirements.

Localized Semiconductor Sourcing Strategies Supply-chain diversification has become a major operational trend as geopolitical tensions and semiconductor shortages encourage manufacturers to reduce sourcing concentration. More than 20% of wearable device producers have expanded supplier networks beyond traditional manufacturing hubs. This restructuring improves component availability, shortens procurement lead times, and strengthens production resilience. Companies are responding through regional partnerships, dual-sourcing agreements, and localized assembly operations.

Industrial Workforce Monitoring Adoption Enterprise deployment of wearable sensors for worker safety and productivity management is accelerating, particularly across manufacturing, logistics, and energy sectors. Workplace monitoring implementations have increased by roughly 28%, while real-time incident detection capabilities have improved operational response times by nearly 32%. Labor shortages and stricter workplace safety standards are driving adoption, prompting companies to integrate wearable data into broader operational intelligence platforms.

Motion sensors represent the leading segment within the wearable sensors market, accounting for an estimated 38% of overall deployment activity due to their broad integration across fitness trackers, smartwatches, industrial wearables, and rehabilitation devices. Their dominance stems from low power consumption, proven scalability, and seamless integration into multi-sensor platforms. Accelerometers and gyroscopes remain essential components for activity tracking, motion analysis, and navigation applications. Companies continue prioritizing motion-sensing innovation through miniaturization programs and enhanced power-efficiency designs, improving device performance while extending battery life.Biosensors are emerging as the fastest-growing type as healthcare systems increasingly prioritize continuous physiological monitoring. Adoption of advanced biosensing platforms has increased by more than 30% across remote patient monitoring deployments. Temperature sensors and pressure sensors maintain strategic importance in clinical monitoring and industrial safety applications, while environmental sensors are gaining traction within specialized occupational health applications. Manufacturers are increasing investment in multi-modal sensor architectures, strategic healthcare collaborations, and AI-enabled sensing platforms to strengthen differentiation and expand addressable use cases.

Healthcare remains the leading application segment, representing approximately 42% of wearable sensor utilization due to rising deployment of remote patient monitoring systems, chronic disease management programs, and digital health platforms. Healthcare organizations increasingly rely on wearable-generated biometric data to improve patient engagement and reduce manual monitoring workloads. Sensor-enabled monitoring workflows have contributed to operational efficiency gains exceeding 20% in several large healthcare networks. Device manufacturers are responding through clinical-grade product development, healthcare partnerships, and regulatory-focused product enhancements. Sports and fitness applications continue to maintain strong adoption levels, while industrial monitoring is emerging as the fastest-growing application area. Industrial deployments have expanded by nearly 28% as enterprises seek real-time worker safety monitoring and operational visibility. Consumer wellness applications remain highly relevant as over 45% of wearable users actively monitor multiple health indicators beyond physical activity tracking. Companies are increasingly integrating AI analytics, cloud connectivity, and enterprise software platforms to support evolving application requirements and expand deployment opportunities.

Healthcare providers constitute the dominant end-user group due to extensive deployment of wearable sensors across hospitals, clinics, telehealth networks, and chronic care management programs. This segment accounts for roughly 40% of wearable sensor implementation activity, supported by increasing demand for continuous patient monitoring and data-driven clinical decision-making. Large healthcare systems are investing in integrated monitoring platforms capable of supporting thousands of connected devices simultaneously. Vendors are strengthening relationships with healthcare institutions through customized solutions, interoperability enhancements, and service-based delivery models. Industrial enterprises represent the fastest-growing end-user category as manufacturers, logistics operators, and energy companies increasingly adopt wearable technologies to improve workforce visibility and safety compliance. Adoption within industrial environments has increased by more than 25%, supported by operational efficiency initiatives and workplace safety modernization efforts. Consumer end-users remain a substantial market base driven by personal health monitoring trends, while sports organizations continue adopting advanced performance-tracking solutions. Companies are tailoring product portfolios through industry-specific functionality, subscription-based analytics, and ecosystem partnerships to capture shifting demand patterns.

North America accounted for the largest market share at 38.5% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2026 and 2033.

North America maintains its leadership position through advanced healthcare infrastructure, strong digital health ecosystems, and high wearable device penetration. The region contributes approximately 38.5% of global market activity, supported by large-scale deployment of remote patient monitoring systems and enterprise wellness programs. More than 45% of connected healthcare initiatives in the region now incorporate wearable sensor technologies for continuous biometric monitoring. Healthcare providers, insurers, and technology firms are increasingly collaborating to improve data interoperability and patient engagement. Recent investments in AI-enabled healthcare analytics platforms have accelerated wearable integration into clinical workflows, improving operational efficiency and expanding deployment across both consumer and institutional environments.

United States Market Outlook: The United States serves as the primary innovation and commercialization hub for wearable sensors, supported by extensive healthcare digitization and technology investment. More than 43% of adults actively use wearable health-tracking devices, creating a substantial installed base for advanced sensing technologies. Strong venture capital activity, regulatory support for remote care delivery, and partnerships between healthcare providers and technology companies continue to strengthen adoption. Leading device manufacturers are expanding medical-grade wearable portfolios while integrating predictive analytics and cloud-based monitoring capabilities to enhance long-term patient management.

Europe accounts for approximately 27.4% of global wearable sensor adoption, supported by growing healthcare modernization initiatives and stringent medical device standards. Regulatory frameworks emphasizing patient safety and data protection are encouraging deployment of validated wearable monitoring technologies across healthcare systems. Germany, France, and the United Kingdom remain key deployment centers, while enterprise wellness and occupational safety applications continue expanding. More than 30% of newly introduced digital health programs across major European economies include wearable monitoring components. Companies are investing in certified biosensor platforms and expanding healthcare partnerships to meet evolving compliance and interoperability requirements.

Germany Market Outlook: Germany remains the region's most strategically significant market due to its advanced healthcare infrastructure, industrial technology leadership, and strong digital health policy framework. The country's hospital modernization programs continue supporting wider deployment of connected patient-monitoring solutions. More than one-quarter of healthcare providers have expanded digital monitoring capabilities in recent years. German manufacturers are also strengthening wearable sensor innovation through collaborations between medical technology firms, research institutions, and advanced electronics suppliers, supporting both domestic deployment and export opportunities.

Asia-Pacific represents approximately 24.8% of global market activity and continues to strengthen its position through large-scale electronics manufacturing capabilities and rapidly expanding healthcare digitization programs. The region benefits from strong consumer electronics production, rising health awareness, and growing investment in connected healthcare infrastructure. More than 60% of global wearable device manufacturing capacity is concentrated within Asia-Pacific supply chains. Countries across the region are accelerating deployment of wearable-enabled monitoring systems while expanding semiconductor and sensor manufacturing investments. Companies are increasing local production capacity and forming strategic partnerships to secure component availability and improve supply-chain resilience.

China Market Outlook: China remains the dominant country within Asia-Pacific due to its extensive electronics manufacturing ecosystem and rapidly growing digital health sector. The country accounts for a significant share of global wearable device production and benefits from strong semiconductor, sensor, and consumer electronics integration capabilities. More than 35% of domestic wearable shipments now include advanced health-monitoring features. Chinese manufacturers continue investing in AI-enabled wearables, flexible electronics, and vertically integrated production strategies, strengthening competitiveness across both domestic and international markets.

South America accounts for approximately 5.2% of global wearable sensor demand, with adoption primarily concentrated in healthcare, fitness, and corporate wellness applications. Growing investment in digital healthcare infrastructure is improving awareness and accessibility of wearable technologies across urban centers. Healthcare providers increasingly utilize wearable-enabled monitoring solutions to improve patient engagement and reduce resource constraints. However, uneven infrastructure development and reimbursement limitations continue influencing deployment speed. Several regional healthcare organizations have expanded remote monitoring programs by more than 20%, creating new opportunities for sensor manufacturers and healthcare technology providers seeking long-term market penetration.

Brazil Market Outlook: Brazil represents the largest wearable sensor market in South America due to its sizable healthcare sector, growing technology adoption, and expanding digital health ecosystem. Major private healthcare providers are increasingly integrating wearable monitoring solutions into chronic disease management programs. Rising smartphone penetration and consumer interest in health tracking continue supporting adoption. Local technology distributors and international device manufacturers are strengthening partnerships to improve product availability, while healthcare organizations focus on expanding remote monitoring capabilities to address capacity and accessibility challenges.

The Middle East & Africa region contributes approximately 4.1% of global wearable sensor activity and is increasingly benefiting from healthcare modernization programs and smart infrastructure investments. Governments are prioritizing digital healthcare transformation, creating opportunities for wearable-enabled monitoring platforms within both public and private healthcare networks. Smart city initiatives and workforce safety programs are also encouraging broader deployment across industrial environments. Several healthcare digitization projects launched across the Gulf region have expanded connected monitoring capabilities by more than 15%, supporting greater integration of wearable technologies into care delivery systems and operational workflows.

Saudi Arabia Market Outlook: Saudi Arabia has emerged as the region's most strategically important market due to substantial healthcare infrastructure investment and ongoing digital transformation initiatives. National healthcare modernization programs continue supporting adoption of connected medical technologies and remote patient monitoring solutions. Large healthcare institutions are expanding digital care platforms and integrating wearable-generated data into clinical decision-making processes. Strong government-backed technology investments, combined with growing private-sector participation, are accelerating deployment of advanced wearable sensor solutions across healthcare and workforce management applications.

The wearable sensors market is led by technology innovators such as Apple, Medtronic, Garmin, Philips, and STMicroelectronics, competing against specialized sensor developers, healthcare device manufacturers, and cost-focused Asian electronics suppliers. The top five players collectively account for approximately 42% of market activity, creating a moderately concentrated competitive structure. Competition is increasingly centered on sensor accuracy, AI-enabled analytics, battery efficiency, and healthcare integration rather than device pricing alone. Advanced biosensor platforms deliver up to 30% higher monitoring precision, while low-power sensor architectures reduce energy consumption by nearly 25%. Global leaders compete through ecosystem control and software integration, whereas regional manufacturers focus on manufacturing scale and cost optimization. Companies are expanding through healthcare partnerships, semiconductor collaborations, and vertical integration strategies. Recent competition has shifted toward medical-grade wearable monitoring, AI-powered predictive health insights, and supply-chain resilience. Access to proprietary health datasets, regulatory approvals, and sensor miniaturization capabilities remain major entry barriers. Winning requires superior sensing performance, validated healthcare outcomes, scalable manufacturing, interoperable software ecosystems, and sustained investment in next-generation biosensing technologies.

Medtronic plc

Garmin Ltd.

Philips

STMicroelectronics

Analog Devices, Inc.

Texas Instruments Incorporated

Infineon Technologies AG

NXP Semiconductors N.V.

Honeywell International Inc.

TE Connectivity Ltd.

ams-OSRAM AG

Abbott Laboratories

Dexcom, Inc.

Wearable sensor technology is rapidly advancing beyond traditional motion tracking toward multi-parameter health intelligence. Current deployments increasingly combine photoplethysmography (PPG), electrocardiography (ECG), temperature sensing, and blood oxygen monitoring within a single device. More than 45% of newly launched premium wearables now integrate three or more physiological sensing functions. These platforms improve health-monitoring accuracy by approximately 25% while enabling continuous biometric assessment. Healthcare providers and device manufacturers benefit from enhanced diagnostic visibility and stronger patient engagement.

Emerging technologies include AI-driven behavioral analytics, flexible biosensors, and edge-computing architectures. Compared with legacy cloud-dependent systems, on-device AI processing can reduce response latency by over 40% and lower data-transmission requirements by nearly 30%. Flexible sensor materials improve wearer comfort and extend device utilization across medical and industrial environments. Adoption of advanced biosensing solutions continues expanding across remote patient monitoring, workforce safety, and performance analytics applications.

Disruptive innovation is increasingly focused on non-invasive glucose monitoring, neural sensing interfaces, and ultra-low-power sensor architectures. Advanced event-based wearable sensing platforms demonstrate up to 25x lower power consumption than conventional vision-based approaches while maintaining strong performance levels. Between 2026 and 2028, organizations investing in AI-enabled multi-sensor ecosystems, edge intelligence, and predictive health analytics will secure meaningful operational and competitive advantages as wearable platforms evolve into continuous decision-support systems.

May 2025 – Medtronic expanded its patient-monitoring portfolio through an exclusive Western Europe distribution agreement with Corsano Health for multi-parameter wearable monitoring devices. The solution enables continuous vital-sign tracking across hospital and hospital-at-home settings, strengthening remote care deployment and accelerating healthcare wearable adoption. Source: www.news.medtronic.com

January 2025 – Pison and STMicroelectronics announced commercialization of neural-sensor technology with Timex as a wearable partner. Sensor miniaturization significantly reduced device integration costs while enabling neurocognitive monitoring and gesture-control functionality, opening new wearable categories and expanding advanced biosensor deployment opportunities.

July 2025 – Apple Research published findings from a wearable behavioral foundation model trained on more than 2.5 billion hours of wearable data from 162,000 users. The development improves health-condition prediction capabilities and strengthens AI-driven wearable healthcare analytics applications.

March 2025 – Research consortium behind Helios 2.0 demonstrated an ultra-low-power wearable gesture-recognition platform delivering approximately 25x lower power consumption and over 20% accuracy improvement versus prior approaches. The advancement supports next-generation smart glasses and energy-efficient wearable computing applications.

The report provides comprehensive coverage of the wearable sensors industry across major sensor types, applications, end-user categories, and key geographic markets. It evaluates demand patterns across motion sensors, biosensors, temperature sensors, pressure sensors, and emerging sensing technologies while assessing adoption across healthcare, fitness, industrial monitoring, consumer wellness, and specialized enterprise applications. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level strategic analysis.

The study examines technology adoption trends, competitive positioning, deployment patterns, supply-chain developments, and innovation priorities shaping market evolution between 2026 and 2033. More than 40% of current demand is concentrated in healthcare-oriented use cases, while industrial and remote-monitoring deployments continue expanding. The report supports investment evaluation, product development planning, partnership strategies, geographic expansion decisions, and competitive benchmarking by identifying high-priority growth segments, emerging technology opportunities, operational risks, and future industry transformation pathways.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 404.0 Million |

| Market Revenue (2033) | USD 1,144.4 Million |

| CAGR (2026–2033) | 13.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Apple Inc.; Medtronic plc; Garmin Ltd.; Philips; STMicroelectronics; Analog Devices, Inc.; Texas Instruments Incorporated; Infineon Technologies AG; NXP Semiconductors N.V.; Honeywell International Inc.; TE Connectivity Ltd.; ams-OSRAM AG; Abbott Laboratories; Dexcom, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |