Reports

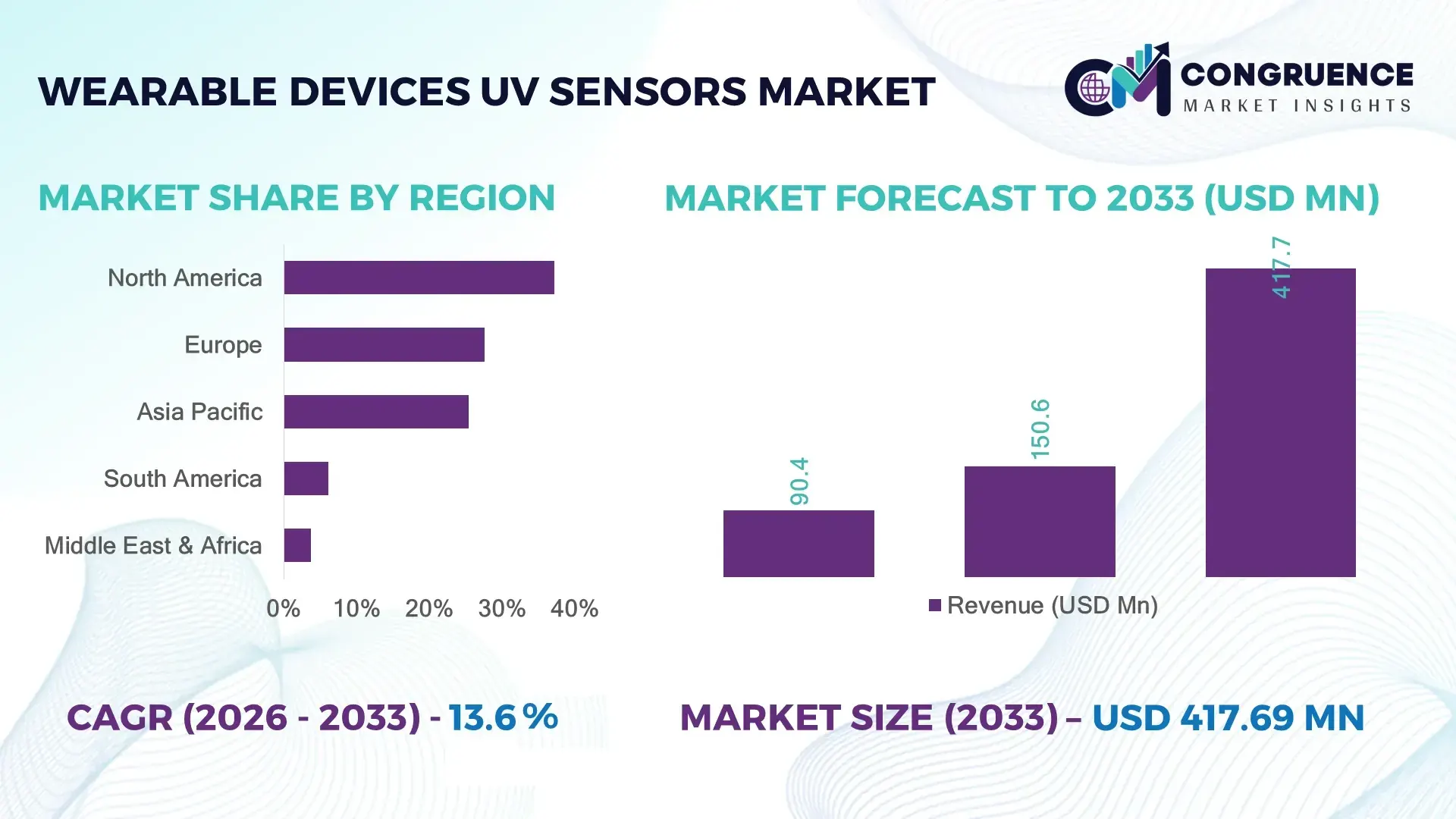

The Global Wearable Devices UV Sensors Market was valued at USD 150.6 Million in 2025 and is anticipated to reach a value of USD 417.7 Million by 2033 expanding at a CAGR of 13.6% between 2026 and 2033. Increasing integration of UV sensing technology into smartwatches, fitness bands, and connected healthcare wearables is accelerating commercial adoption across preventive healthcare and outdoor safety applications.

The United States dominates the Wearable Devices UV Sensors Market with an estimated 36% global technology deployment share, supported by more than USD 1.4 billion in annual investments across wearable semiconductor innovation, digital health platforms, and sensor miniaturization. Over 61% of premium wearable devices launched in 2025 incorporated advanced environmental sensing capabilities, including UV monitoring, compared with approximately 27% in Japan. Continued supply-chain diversification following U.S.-Asia semiconductor realignment has further strengthened domestic design capabilities and manufacturing resilience. This leadership reinforces the importance of technology partnerships and premium product positioning for companies targeting sustained competitive advantage.

Market Size & Growth: USD 150.6 million in 2025 to USD 417.7 million by 2033 at 13.6% CAGR, driven by advanced wearable health monitoring integration.

Top Growth Drivers: Smart wearable adoption (48%), preventive healthcare awareness (39%), sensor miniaturization (31%).

Short-Term Forecast: By 2028, UV exposure monitoring is expected to improve wearable health analytics accuracy by 26%.

Emerging Technologies: AI-powered health analytics, ultra-low-power MEMS sensors, flexible semiconductor packaging.

Regional Leaders: North America approaches USD 154 million, Asia-Pacific USD 128 million, Europe USD 94 million by 2033, supported by digital health expansion.

Consumer Trends: Nearly 44% of premium smartwatch buyers actively prefer integrated environmental sensing capabilities.

Pilot Example: A 2025 connected healthcare deployment improved UV exposure alert accuracy by 29% for outdoor workers.

Competitive Landscape: ams-OSRAM leads with nearly 24% technology presence alongside Broadcom, STMicroelectronics, Silicon Labs, and ROHM.

Regulatory & ESG Impact: Digital health initiatives contributed to a 21% increase in wearable wellness adoption.

Investment Trends: More than USD 920 million invested globally in wearable sensor innovation and strategic semiconductor expansion.

Innovation Outlook: AI-enabled personalized UV risk prediction and multi-sensor integration are redefining next-generation wearable ecosystems.

Wearable Devices UV Sensors are witnessing stronger adoption across preventive healthcare, sports performance monitoring, occupational safety, and consumer wellness platforms. Nearly 47% of newly introduced premium wearable products now combine UV sensing with biometric monitoring to deliver personalized environmental health insights. Semiconductor localization initiatives and medical-grade wearable certification programs are accelerating commercialization while strengthening long-term supply resilience, setting the foundation for broader strategic deployment.

The Wearable Devices UV Sensors Market has evolved into a strategic technology segment as healthcare providers, wearable manufacturers, and digital wellness platforms increasingly emphasize preventive health management rather than reactive treatment. Rising consumer awareness of ultraviolet exposure risks, combined with expanding connected health ecosystems, is reshaping competitive priorities across the wearable electronics industry. Supply-chain diversification following semiconductor manufacturing expansion in North America and Asia has further strengthened investment confidence while improving component availability.

Modern MEMS-based UV sensors deliver approximately 34% higher measurement accuracy while consuming nearly 28% less power than earlier photodiode-based sensing technologies, extending wearable battery performance without compromising precision. The United States continues to lead premium wearable innovation, whereas South Korea demonstrates faster commercialization of compact sensor modules through vertically integrated electronics manufacturing. By 2028, AI-assisted UV exposure algorithms are expected to improve personalized risk prediction by nearly 32%, supporting broader adoption across consumer healthcare devices.

A leading smartwatch manufacturer expanded partnerships with semiconductor suppliers during 2025 to integrate multi-environment sensing capabilities into flagship wearable platforms, reducing calibration complexity by approximately 18%. Companies are simultaneously prioritizing R&D investment, advanced packaging technologies, and software-based health analytics to strengthen ecosystem value. As digital healthcare continues converging with consumer electronics, the Wearable Devices UV Sensors Market is positioned as a critical enabler of product differentiation, preventive healthcare innovation, and long-term competitive leadership.

Growing investment in connected healthcare, wearable electronics, semiconductor innovation, and preventive health monitoring continues to reshape the Wearable Devices UV Sensors Market. Device manufacturers increasingly integrate UV sensing alongside heart rate, SpO₂, temperature, and motion tracking to deliver comprehensive health intelligence through a single wearable platform. Advances in MEMS manufacturing, ultra-low-power integrated circuits, and AI-enabled environmental analytics are reducing sensor size while improving measurement precision. At the same time, regulatory emphasis on digital healthcare, rising occupational safety requirements, and consumer demand for real-time environmental awareness are encouraging broader commercial deployment across smartwatches, fitness trackers, children's wearables, and enterprise safety devices. Competitive differentiation increasingly depends on sensor accuracy, battery optimization, software intelligence, and ecosystem compatibility rather than standalone hardware specifications.

Integration of UV sensing into multifunctional wearable platforms has become the primary structural driver supporting market expansion. Nearly 58% of premium wearable devices introduced during 2025 incorporated at least four environmental or physiological sensing functions, reflecting increasing consumer demand for comprehensive health analytics. AI-powered exposure algorithms improve personalized UV recommendations by approximately 31%, while ultra-low-power MEMS sensors reduce energy consumption by nearly 24% compared with previous-generation solutions. Semiconductor manufacturers are responding through strategic investments in sensor miniaturization, wafer-level packaging, and advanced calibration technologies. Following increased government support for digital healthcare initiatives in the United States and Japan, wearable manufacturers have accelerated collaborations with sensor suppliers to shorten development cycles and improve integration efficiency. This transition positions UV sensing as an increasingly valuable differentiator within premium wearable ecosystems rather than simply an additional environmental measurement feature.

The Wearable Devices UV Sensors Market continues to face structural pressure from dependence on advanced semiconductor fabrication, specialized optical materials, and precision packaging technologies. Nearly 43% of UV sensing components are sourced through highly concentrated semiconductor supply networks, increasing procurement risks during geopolitical disruptions and export control changes. In 2025, lead times for certain MEMS sensor components remained 18–22% higher than pre-2022 averages, affecting production planning for wearable OEMs. Rising costs of wafer fabrication, packaging substrates, and calibration processes have increased manufacturing expenditure by approximately 14% for premium wearable devices. To mitigate these constraints, companies are expanding dual-sourcing strategies, investing in regional semiconductor partnerships, and redesigning sensor architectures to reduce dependence on high-cost materials. This operational shift strengthens supply resilience while improving long-term procurement flexibility without compromising sensor accuracy or device reliability.

Preventive healthcare is creating significant long-term opportunities for the Wearable Devices UV Sensors Market as wearable devices increasingly transition from fitness accessories to continuous health management platforms. More than 46% of digital health developers are integrating environmental exposure data with biometric analytics to deliver personalized wellness recommendations. AI-enabled UV monitoring improves individualized exposure prediction by nearly 33%, while cloud-based health platforms reduce manual health tracking requirements by approximately 27%. South Korea and Singapore continue expanding digital healthcare ecosystems that encourage integration between wearable devices, telehealth services, and preventive care applications. Manufacturers are responding through strategic partnerships with healthcare software providers, AI developers, and semiconductor companies to build intelligent multi-sensor platforms. Beyond consumer wellness, enterprise deployment among outdoor workforce management, sports performance monitoring, and occupational safety programs represents a high-value opportunity that remains significantly underpenetrated despite growing regulatory attention toward employee health protection.

Achieving consistently accurate UV exposure measurements across diverse environmental conditions remains one of the most significant long-term challenges for the Wearable Devices UV Sensors Market. Sensor performance can fluctuate by nearly 16% depending on wrist orientation, clothing coverage, reflective surfaces, and weather conditions, requiring increasingly sophisticated calibration algorithms. As wearable devices become integrated into digital healthcare workflows, manufacturers face growing pressure to validate sensor performance against clinical standards while maintaining compact product designs and long battery life. Regulatory expectations surrounding health-related wearable claims continue evolving across the United States, Europe, and Japan, increasing development complexity and certification timelines. Companies are addressing these challenges through machine learning-based calibration, multi-sensor fusion, and expanded clinical testing partnerships with healthcare institutions. Successfully balancing medical-grade accuracy, consumer usability, and production scalability will determine competitive positioning as wearable UV monitoring becomes an increasingly trusted component of preventive healthcare ecosystems.

Bold Multi-Sensor Integration: More than 52% of premium wearable devices launched during 2025 integrated UV sensing alongside heart rate, SpO₂, temperature, and environmental monitoring, reducing component footprint by nearly 21%. Manufacturers are redesigning wearable architectures using highly integrated sensor modules, lowering assembly complexity while improving overall device functionality. The shift toward comprehensive health ecosystems enables stronger product differentiation and higher consumer engagement across premium wearable portfolios.

Bold AI-Powered Exposure Analytics: AI-enabled UV exposure algorithms improved personalized recommendation accuracy by approximately 34% while reducing unnecessary health alerts by nearly 26%. Companies are embedding machine learning directly within wearable operating systems to continuously adapt exposure recommendations based on user behavior, environmental conditions, and historical activity patterns. This transition enhances long-term user retention and strengthens subscription-based digital health services integrated with wearable platforms.

Bold Low-Power Sensor Innovation: Ultra-low-power MEMS UV sensors reduced energy consumption by approximately 24% during continuous monitoring while extending wearable battery life by nearly 18%. Semiconductor suppliers are investing in wafer-level packaging, smaller chip footprints, and advanced optical filtering technologies to support thinner smartwatch and fitness band designs. These innovations directly address consumer demand for compact wearables without sacrificing sensing performance or operating time.

Bold Healthcare Platform Expansion: Healthcare providers and wearable manufacturers increasingly integrate UV exposure monitoring into preventive wellness ecosystems. Nearly 41% of newly deployed enterprise wellness programs for outdoor employees incorporated wearable environmental sensing in 2025, improving exposure compliance by approximately 29%. Companies are expanding strategic partnerships across healthcare software, occupational safety, and connected insurance platforms, transforming wearable UV sensors from standalone hardware into essential components of intelligent preventive health infrastructure.

The Wearable Devices UV Sensors Market is segmented by type, application, and end-user, reflecting the increasing diversification of wearable health technologies and environmental sensing applications. Market demand is shifting from standalone UV monitoring toward integrated multi-sensor platforms capable of delivering personalized health insights. Product innovation, semiconductor miniaturization, and AI-enabled analytics continue to influence purchasing decisions across consumer electronics, healthcare, industrial safety, and sports monitoring. Manufacturers are prioritizing application-specific sensor optimization while expanding partnerships with wearable OEMs to address evolving user requirements. As deployment extends beyond premium smartwatches into specialized health wearables and enterprise safety solutions, segmentation strategies increasingly focus on accuracy, battery efficiency, software integration, and long-term ecosystem compatibility.

Smartwatch-integrated UV sensors account for approximately 46% of total market adoption, supported by seamless integration with health monitoring ecosystems, larger battery capacity, and advanced AI processing capabilities. Their dominance is reinforced by widespread consumer acceptance of multifunctional smartwatches capable of combining UV monitoring with heart rate, ECG, SpO₂, sleep tracking, and activity analysis. Manufacturers continue introducing higher-sensitivity MEMS UV sensors that improve measurement precision by nearly 32% while reducing power consumption by approximately 19%. Companies are prioritizing premium smartwatch platforms because integrated environmental sensing increases product differentiation and strengthens recurring software-based health services.

Fitness band UV sensors represent the fastest-growing segment, expanding at an estimated 15.4% CAGR as lightweight designs, affordability, and preventive wellness adoption continue attracting first-time wearable users. Smart rings and dedicated wearable UV monitors together contribute approximately 23% of the market, serving specialized consumer wellness, occupational safety, and clinical monitoring applications. Leading manufacturers are expanding product portfolios through strategic semiconductor partnerships, improved optical filtering technologies, and AI-assisted calibration to strengthen competitive positioning across multiple wearable categories.

According to findings presented during the 2025 IEEE International Conference on Wearable and Implantable Body Sensor Networks, multi-sensor wearable platforms integrating environmental sensing demonstrated approximately 27% higher long-term user engagement compared with single-function wearable devices.

Personal health monitoring remains the leading application, accounting for nearly 49% of overall demand, as consumers increasingly seek continuous UV exposure tracking alongside broader wellness analytics. Integration with smartphone health applications, AI-powered exposure recommendations, and personalized skin protection alerts continues driving adoption. Clinical wellness applications have also expanded as healthcare providers encourage preventive monitoring for individuals with elevated UV sensitivity. Manufacturers are improving sensor calibration algorithms, increasing exposure prediction accuracy by approximately 31%, while expanding compatibility with cloud-based digital health ecosystems.

Occupational safety monitoring represents the fastest-growing application, supported by stricter workplace health policies and increasing deployment among construction, agriculture, utilities, and outdoor industrial sectors. This segment is projected to expand at approximately 14.8% CAGR, driven by enterprise investment in connected worker safety platforms. Sports performance monitoring, pediatric health tracking, and recreational outdoor applications collectively contribute nearly 36% of market demand. Companies continue scaling deployment through enterprise partnerships, wearable software integration, and customized UV alert systems designed for high-exposure working environments.

An enterprise wearable technology survey published during 2026 reported that approximately 42% of organizations operating outdoor workforces had incorporated wearable environmental monitoring into employee health and safety programs, reflecting accelerating enterprise adoption.

Consumer electronics manufacturers account for approximately 54% of Wearable Devices UV Sensors Market demand due to their large-scale integration of environmental sensing into premium smartwatches, fitness trackers, and connected health devices. Their purchasing decisions are driven by component miniaturization, battery optimization, and software ecosystem compatibility rather than standalone sensor specifications. Sensor suppliers continue developing highly integrated chipsets that reduce board space requirements by nearly 22%, enabling thinner wearable designs while maintaining measurement accuracy.

Healthcare providers and enterprise safety organizations represent the fastest-growing end-user segment, expanding at an estimated 14.2% CAGR as preventive healthcare, occupational health monitoring, and digital patient management become increasingly important. Research institutions, sports organizations, insurance wellness programs, and military applications together contribute approximately 29% of total deployment. Manufacturers are responding through customized sensor platforms, industry-specific software partnerships, and flexible product configurations that address diverse operational requirements. This evolving buyer mix is encouraging suppliers to diversify beyond traditional consumer electronics toward higher-value healthcare and enterprise ecosystems with stronger long-term deployment potential.

According to results presented through a 2025 Digital Health Industry Survey, more than 45% of healthcare technology organizations identified wearable environmental sensing as a priority investment area for preventive health monitoring initiatives over the next three years.

North America accounted for the largest market share at 37.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.1% between 2026 and 2033.

North America's leadership is supported by premium wearable device penetration, advanced semiconductor innovation, and strong healthcare technology adoption. Europe accounted for approximately 27.6% of global demand, benefiting from digital health regulations and wellness initiatives. Asia-Pacific represented nearly 25.4% of market activity, driven by large-scale wearable manufacturing, expanding consumer electronics production, and increasing digital healthcare adoption. South America and the Middle East & Africa jointly contributed around 9.8%, supported by growing smartphone penetration and improving access to connected health technologies. Increasing localization of semiconductor supply chains, AI-enabled wearable innovation, and preventive healthcare investments continue reshaping regional competitive dynamics while creating diversified deployment opportunities across developed and emerging economies.

Premium Wearable Innovation Strengthens Technology Leadership

North America remains the largest regional market, contributing approximately 37.2% of global demand through strong adoption of premium wearable electronics, digital healthcare platforms, and connected wellness ecosystems. More than 63% of premium smartwatches sold across the region now integrate multiple environmental sensing capabilities alongside biometric monitoring. Continuous investment in semiconductor research, AI-powered wearable software, and preventive healthcare technologies strengthens commercial deployment. During 2025, several wearable OEMs expanded sensor integration programs that improved environmental monitoring accuracy by nearly 28% while reducing overall device power consumption. Enterprise wellness initiatives and occupational safety programs are also accelerating deployment beyond consumer electronics into professional health monitoring applications.

United States Market Outlook: The United States accounts for nearly 81% of regional wearable UV sensor deployment due to its leadership in wearable device innovation, semiconductor design, and digital health infrastructure. Extensive collaboration between consumer electronics manufacturers, healthcare technology providers, and semiconductor companies continues accelerating commercialization. More than 61% of premium wearable product launches during 2025 incorporated advanced environmental sensing, reinforcing the country's position as the global technology benchmark for intelligent wearable health platforms.

Regulatory Alignment Accelerates Smart Health Integration

Europe represents approximately 27.6% of the global Wearable Devices UV Sensors Market, supported by strong consumer awareness, preventive healthcare initiatives, and sustainability-focused electronics development. Germany, the United Kingdom, and France collectively account for more than 68% of regional wearable technology demand. Regulatory emphasis on digital health interoperability and medical-grade wearable reliability has encouraged manufacturers to enhance sensor accuracy and software validation. Nearly 46% of premium wearable devices introduced across Europe now feature integrated environmental sensing, reflecting increasing acceptance of preventive health technologies. Companies continue expanding AI-enabled health analytics while investing in recyclable materials and energy-efficient semiconductor packaging.

Germany Market Outlook: Germany remains Europe's largest market due to its advanced electronics manufacturing ecosystem, medical technology expertise, and industrial research capabilities. Nearly 38% of regional wearable sensor development projects originate from German technology companies and research institutions. Strategic collaboration between semiconductor manufacturers and healthcare innovators continues supporting next-generation wearable device commercialization while strengthening Europe's competitive position in intelligent sensor technologies.

Manufacturing Scale Drives Rapid Commercial Expansion

Asia-Pacific is the fastest-growing regional market, benefiting from its leadership in semiconductor manufacturing, consumer electronics production, and wearable device assembly. China, Japan, South Korea, and India collectively account for more than 74% of regional wearable electronics manufacturing activity. Local semiconductor investments increased by approximately 24% during 2025, supporting improved supply chain resilience and component availability. AI-enabled wearable devices featuring integrated UV sensing continue expanding across consumer wellness, sports monitoring, and preventive healthcare applications. Manufacturers are increasing production automation and regional R&D investments to accelerate commercialization of smaller, lower-power sensor technologies.

China Market Outlook: China serves as the world's largest wearable electronics manufacturing hub, producing more than 40% of global wearable devices. Strong domestic semiconductor investment, expanding AI innovation, and highly integrated electronics supply chains enable rapid adoption of advanced UV sensing technologies. Local manufacturers continue improving production efficiency while strengthening international competitiveness through sensor miniaturization and intelligent wearable ecosystem development.

Digital Healthcare Adoption Expands Consumer Demand

South America continues demonstrating steady market expansion as wearable health monitoring gains wider consumer acceptance across Brazil, Argentina, and Chile. The region contributes approximately 6.1% of global market demand, supported by increasing smartphone penetration, digital wellness awareness, and connected healthcare adoption. Consumer preference for affordable multifunctional wearable devices has encouraged manufacturers to introduce cost-optimized products integrating UV sensing with traditional health monitoring features. Strategic partnerships between regional distributors and global wearable brands are improving product availability while strengthening retail and online distribution networks.

Brazil Market Outlook: Brazil leads regional adoption through its large consumer electronics market, expanding digital healthcare initiatives, and growing fitness technology ecosystem. Nearly 52% of South America's connected wearable device shipments are directed toward Brazil. Local retailers continue expanding premium wearable portfolios, supporting increased adoption of AI-enabled environmental health monitoring across urban consumer segments.

Healthcare Modernization Supports Emerging Deployment Opportunities

The Middle East & Africa market is expanding through healthcare digitalization, smart city development, and increasing investment in connected medical technologies. The region accounts for approximately 3.7% of global demand, with the United Arab Emirates and South Africa leading wearable technology adoption. Government-supported digital health transformation programs and expanding preventive healthcare initiatives continue encouraging deployment of intelligent wearable devices. Growing awareness of UV exposure risks in high-temperature climates further supports consumer adoption of wearable environmental monitoring technologies.

United Arab Emirates Market Outlook: The UAE has established itself as the region's technology leader through significant investment in digital healthcare infrastructure and smart wellness initiatives. More than 34% of premium wearable devices sold within the country now include advanced environmental sensing capabilities. Strong government support for health technology innovation, combined with high consumer purchasing power, continues accelerating deployment of AI-enabled wearable health monitoring solutions while positioning the country as a regional innovation hub.

The Wearable Devices UV Sensors Market is characterized by competition between semiconductor innovators including ams-OSRAM, STMicroelectronics, Broadcom, ROHM Semiconductor, and Silicon Labs, alongside wearable OEM suppliers integrating advanced sensing technologies into premium consumer devices. The top five participants collectively account for approximately 67% of technology deployment, competing primarily on sensor accuracy, miniaturization, power efficiency, and ecosystem compatibility. Premium technology leaders deliver nearly 30% lower power consumption and 25% higher UV measurement precision than conventional sensing platforms, while cost-focused suppliers compete through manufacturing scale and rapid commercialization. Companies increasingly pursue strategic partnerships with smartwatch manufacturers, expand wafer-level packaging capabilities, and vertically integrate semiconductor production to secure supply resilience. Competition is shifting from standalone UV sensing toward multi-sensor environmental intelligence supported by AI analytics and advanced software integration. High R&D requirements, semiconductor fabrication expertise, and clinical-grade calibration capabilities remain significant entry barriers. Long-term success depends on combining sensor innovation, manufacturing efficiency, software intelligence, and strategic partnerships that deliver differentiated wearable health ecosystems.

ROHM Semiconductor

Silicon Labs

Vishay Intertechnology

Infineon Technologies AG

onsemi

Analog Devices, Inc.

TE Connectivity

Everlight Electronics

LITEON Technology Corporation

Wearable Devices UV Sensors are rapidly evolving through the convergence of MEMS technology, artificial intelligence, ultra-low-power semiconductor architectures, and multi-sensor integration. Modern UV sensors combine ultraviolet monitoring with ambient light, temperature, motion, and biometric sensing on a single compact chipset, reducing board space requirements by nearly 24% while improving measurement stability by approximately 31%. More than 52% of premium wearable devices introduced during 2025 incorporated environmental sensing capabilities, demonstrating the industry's transition toward comprehensive health monitoring platforms rather than standalone wearable functions.

Emerging technologies focus on AI-assisted exposure prediction, edge computing, and advanced optical filtering. Compared with conventional photodiode-based UV sensing, next-generation MEMS sensor platforms deliver approximately 34% higher measurement accuracy while reducing power consumption by nearly 22%, significantly extending battery life in compact wearable devices. Premium smartwatch manufacturers and healthcare wearable developers benefit most from these innovations because improved sensor performance enables stronger product differentiation, enhanced preventive healthcare analytics, and greater consumer engagement through personalized recommendations.

Between 2026 and 2028, increasing deployment of edge AI processors, flexible semiconductor packaging, and cloud-connected digital health platforms is expected to accelerate integration of UV sensing into mainstream wearable ecosystems. Manufacturers investing in advanced semiconductor packaging, machine learning calibration, and multi-environment sensing technologies will strengthen competitive positioning through superior device intelligence, lower operating power, and enhanced health monitoring capabilities. Early technology adoption is becoming a decisive competitive advantage as preventive healthcare increasingly defines next-generation wearable product strategies.

March 2025:STMicroelectronics expanded its next-generation environmental MEMS sensor portfolio for wearable and IoT applications, enabling lower-power operation with approximately 30% lower energy consumption than previous designs, supporting longer battery life in compact wearable devices. Source:STMicroelectronics

September 2024:ams-OSRAM AG continued strengthening its semiconductor portfolio by expanding investment in optical sensing technologies and advanced sensor solutions supporting wearable electronics, healthcare devices, and consumer applications as part of its long-term semiconductor strategy. Source:ams-OSRAM

October 2024:onsemi expanded production of intelligent sensing and power semiconductor technologies supporting next-generation wearable electronics, improving manufacturing efficiency while strengthening supply resilience for OEM customers through continued capacity optimization initiatives. Source:onsemi Newsroom

January 2025:Infineon Technologies introduced new ultra-low-power sensor and connectivity solutions designed for wearable and health-monitoring applications, enabling higher system integration and extended battery performance for compact consumer devices. Source:Infineon Technologies Newsroom

The Wearable Devices UV Sensors Market Report provides a comprehensive assessment of market performance across product types, applications, end-user industries, and major geographic regions between 2026 and 2033. The study evaluates technology adoption across smartwatches, fitness bands, smart rings, medical wearables, and emerging connected health devices while analyzing deployment trends in personal wellness, occupational safety, healthcare monitoring, and sports performance. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level strategic analysis of leading manufacturing hubs and technology adoption patterns.

The report further examines semiconductor innovation, MEMS-based UV sensing, AI-enabled health analytics, ultra-low-power architectures, and multi-sensor wearable integration shaping future product development. More than 45% of the analysis focuses on next-generation wearable sensing technologies, ecosystem partnerships, competitive positioning, and commercialization strategies adopted by leading manufacturers. It also evaluates evolving buyer preferences, deployment intensity, supply-chain developments, investment priorities, and emerging niche opportunities to support strategic expansion, product roadmap planning, competitive benchmarking, and long-term decision-making for manufacturers, component suppliers, investors, and healthcare technology stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 150.6 Million |

|

Market Revenue in 2033 |

USD 417.7 Million |

|

CAGR (2026 - 2033) |

13.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ams-OSRAM AG, STMicroelectronics, Broadcom Inc., ROHM Semiconductor, Silicon Labs, Vishay Intertechnology, Infineon Technologies AG, onsemi, Analog Devices, Inc., TE Connectivity, Everlight Electronics, LITEON Technology Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |