Reports

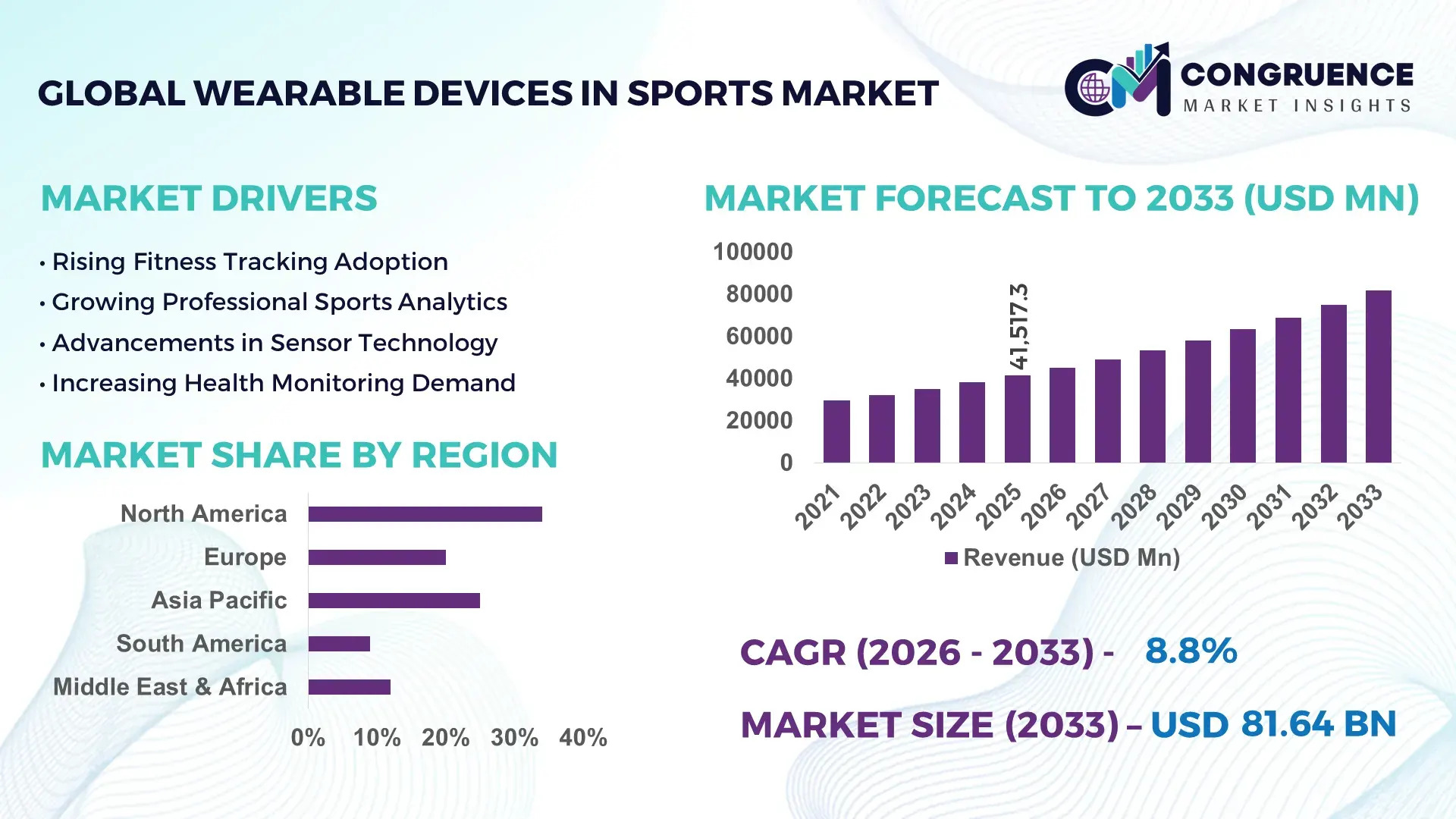

The Global Wearable Devices in Sports Market was valued at USD 41517.32 Million in 2025 and is anticipated to reach a value of USD 81639.27 Million by 2033 expanding at a CAGR of 8.82% between 2026 and 2033. Growth is being accelerated by rising adoption of injury prevention analytics, military-grade motion sensors in commercial sports wearables, and expanding partnerships between semiconductor manufacturers and sports technology platforms.

The United States dominates the global wearable devices in sports market with nearly 34% share, supported by over USD 5.8 Billion in connected fitness and athlete monitoring investments across professional sports organizations, universities, and consumer fitness brands. Advanced sensor manufacturing capacity and AI-driven sports analytics deployments remain significantly higher than in Europe, where adoption rates are approximately 18% lower across amateur sports ecosystems. The 2026 expansion of athlete data regulations and heightened focus on performance optimization after international sporting events have accelerated demand for secure cloud-integrated wearable infrastructure across North America.

Companies prioritizing AI-integrated performance ecosystems, regional manufacturing resilience, and athlete data security standards are securing stronger competitive positioning in the high-growth sports wearable industry.

Market Size & Growth: Market advances from USD 41517.32 Million in 2025 to USD 81639.27 Million by 2033 at 8.82% growth, driven by AI-powered athlete analytics and connected sports ecosystems.

Top Growth Drivers: Injury monitoring adoption contributes 31%, smart textile demand 27%, and cloud-based performance analytics 24% to market expansion.

Short-Term Forecast: By 2027, real-time biometric tracking improves athlete recovery efficiency by 33% while reducing manual performance assessment costs by 21%.

Emerging Technologies: AI wearables, flexible biosensors, and edge-computing sports trackers improve data processing speeds by 42% across advanced training environments.

Regional Leaders: North America exceeds USD 28 Billion with high collegiate adoption, Europe surpasses USD 19 Billion through football analytics integration, and Asia-Pacific crosses USD 16 Billion with expanding smart fitness manufacturing.

Consumer/End-User Trends: More than 58% of fitness-focused consumers now prefer wearable devices with continuous hydration, sleep, and stress monitoring capabilities.

Pilot/Case Example: In 2026, a professional football training deployment reduced soft tissue injury incidents by 26% using AI-enabled motion tracking wearables.

Competitive Landscape: Top five players control nearly 48% market share, with competition centered on sensor accuracy, battery efficiency, and connected software ecosystems.

Regulatory & ESG Impact: Sustainable component sourcing initiatives lowered wearable device material waste by 17% amid tighter global electronics compliance standards.

Investment & Funding: Global investments exceeded USD 9.4 Billion in 2026, led by semiconductor partnerships, AI analytics acquisitions, and regional manufacturing expansion strategies.

Innovation & Future Outlook: Advanced neural sensing wearables and non-invasive biometric patches are reshaping elite sports analytics with 35% faster physiological response tracking.

Professional sports organizations account for nearly 41% of total wearable device deployments, followed by fitness and wellness applications at 36%, while rehabilitation-focused sports technologies contribute close to 15% of demand. AI-based fatigue detection systems, graphene-enabled biosensors, and sweat-monitoring smart patches are becoming core innovation areas across high-performance athletics. North America and Asia-Pacific remain the strongest demand centers due to expanding semiconductor manufacturing and connected fitness adoption. Supply chain diversification across Southeast Asia is also reshaping device production strategies amid tightening electronics compliance standards. Companies are increasingly aligning wearable ecosystems with predictive analytics platforms to strengthen long-term athlete performance optimization strategies.

Wearable devices in sports are becoming strategically critical as professional teams, fitness platforms, and healthcare-linked sports programs shift toward data-centric performance ecosystems. The market is no longer limited to fitness tracking; organizations are integrating biometric analytics, injury prediction engines, and AI-driven coaching systems to improve athlete durability and operational efficiency. In 2026, digital athlete monitoring deployments increased by 39% across high-performance training centers, while stricter athlete data governance standards in the United States and Europe accelerated investment in secure cloud-based wearable infrastructure. Semiconductor supply-chain restructuring across Taiwan and Vietnam is also reducing sensor procurement lead times by nearly 18%.

Advanced AI-integrated wearables now deliver approximately 31% faster physiological data interpretation compared with legacy GPS-only systems, reducing manual assessment workloads across sports science teams. The United States maintains higher deployment intensity through collegiate and professional league investments, while Japan and South Korea are expanding compact biosensor manufacturing for commercial fitness ecosystems. Over the next two years, smart textile adoption in competitive sports training environments is projected to exceed 44% penetration as battery efficiency and edge-computing capabilities improve.

Professional football clubs and Olympic training facilities are increasingly deploying connected recovery platforms combining hydration monitoring, fatigue analytics, and motion capture technologies within unified dashboards. Companies are responding through semiconductor partnerships, AI analytics acquisitions, and localized manufacturing expansion to strengthen product reliability and compliance readiness. Businesses capable of integrating secure analytics, athlete personalization, and scalable wearable ecosystems will secure stronger long-term competitive positioning across the global sports technology value chain.

Professional sports organizations and fitness technology providers are accelerating adoption of AI-enabled wearable ecosystems to improve injury prevention, training precision, and athlete recovery management. In 2026, nearly 64% of elite sports programs incorporated continuous biometric monitoring, while AI-assisted fatigue analysis reduced soft tissue injury incidence by approximately 26% across high-performance training environments. The integration of low-latency edge computing has also improved real-time coaching response efficiency by 29% compared with cloud-dependent legacy systems. Following stricter athlete welfare protocols introduced across European football and North American collegiate sports, companies are expanding sensor accuracy investments and cloud-security partnerships. Manufacturers in the United States and South Korea are prioritizing smart textile innovation and miniaturized biosensor production to strengthen premium device positioning and secure long-term contracts with professional leagues and sports medicine providers.

The wearable devices in sports market continues to face structural limitations linked to fragmented software ecosystems, semiconductor dependency, and cross-platform interoperability gaps. Nearly 41% of sports organizations report compatibility challenges between wearable hardware, analytics dashboards, and third-party athlete management systems, increasing operational integration costs and deployment delays. Battery material price fluctuations and advanced sensor chip shortages in Taiwan and China also raised premium wearable component procurement costs by approximately 17% during recent supply-chain disruptions. These constraints directly affect scalability for mid-sized sports academies and fitness operators seeking enterprise-grade monitoring capabilities. Companies are mitigating exposure through localized assembly expansion, multi-supplier semiconductor contracts, and proprietary software ecosystem development. Firms controlling both hardware and analytics infrastructure are gaining stronger operational leverage by reducing integration complexity and improving deployment consistency across training environments.

The expansion of smart textiles and predictive performance analytics is creating high-value opportunities across professional athletics, rehabilitation programs, and connected fitness ecosystems. In 2026, adoption of sensor-embedded apparel increased by 34% among elite endurance sports programs due to improved flexibility, lightweight materials, and non-invasive monitoring capabilities. AI-powered predictive injury modeling platforms are also reducing athlete downtime by nearly 22% through continuous biomechanical analysis and recovery optimization. Japan and Germany are accelerating investments in flexible electronics manufacturing and graphene-based biosensors to strengthen advanced wearable production capacity. Companies are positioning through partnerships with sports medicine institutions, semiconductor firms, and cloud analytics providers to develop integrated athlete intelligence ecosystems. A key strategic opportunity is emerging in subscription-based performance analytics services, where recurring software-driven revenue models improve long-term profitability beyond standalone hardware sales.

Long-term scalability in the wearable devices in sports market is increasingly challenged by cybersecurity exposure, fragmented athlete data infrastructure, and rising computational demands from real-time analytics systems. In 2026, over 37% of professional sports organizations identified data privacy compliance and encrypted transmission reliability as major operational concerns, particularly for cloud-connected monitoring platforms. High-frequency biometric streaming has increased edge-processing requirements by nearly 24%, forcing companies to upgrade infrastructure and reduce latency across distributed training environments. The United States and United Kingdom are tightening athlete data protection frameworks, increasing compliance costs for wearable technology providers operating across multiple leagues and jurisdictions. Companies must strengthen secure analytics architecture, interoperability standards, and low-power processing capabilities through sustained R&D investments and strategic cybersecurity partnerships. Firms unable to maintain trusted data governance and scalable infrastructure risk losing competitive relevance in performance-critical sports technology ecosystems.

• AI Coaching Systems Scaling AI-driven wearable coaching platforms are replacing traditional post-session analysis workflows across professional sports environments. In 2026, nearly 46% of elite football and basketball organizations integrated real-time biomechanical analytics into training operations, reducing manual performance review time by 32%. Companies are deploying edge-computing wearables to process athlete data locally, improving response speed and reducing cloud dependency costs. Rising restrictions around athlete data storage in Germany and the United States are also pushing vendors toward encrypted analytics ecosystems and regionalized data infrastructure partnerships.

• Smart Textile Deployment Expansion Sensor-embedded apparel adoption increased by 34% across endurance sports and rehabilitation programs as lightweight conductive fabrics improved flexibility and reduced device fatigue issues. Japanese manufacturers expanded graphene-based textile production capacity by approximately 21% to meet demand for non-invasive physiological monitoring. Sports brands are restructuring supplier agreements and increasing localized assembly operations to reduce production delays linked to semiconductor shortages. Integrated smart clothing systems are also improving continuous recovery monitoring accuracy by nearly 27% compared with wrist-based tracking devices.

• Hydration Analytics Integration Rising Sweat-monitoring and hydration analytics wearables are becoming operational priorities in high-temperature training environments and international tournament preparation programs. More than 38% of professional sports academies deployed electrolyte monitoring systems in 2026 to reduce heat-related performance decline and recovery delays. Companies are integrating hydration analytics with athlete management software to automate recovery scheduling and workload optimization. A non-obvious shift is emerging in women’s sports programs, where hormone-linked biometric monitoring is increasing demand for customized physiological tracking platforms.

• Subscription Ecosystems Strengthening Wearable device providers are transitioning from hardware-focused sales models toward subscription-based performance intelligence ecosystems. Approximately 43% of commercial fitness wearable platforms now bundle predictive analytics, injury risk scoring, and recovery recommendations within recurring software services. United Kingdom sports clinics and collegiate athletic programs are expanding multi-device interoperability requirements, forcing companies to prioritize open API architectures and scalable cloud synchronization tools. Vendors are responding through AI partnerships, sports science collaborations, and software acquisition strategies to secure long-term customer retention and improve recurring operational value.

Smartwatches remain the leading segment in the wearable devices in sports market, accounting for nearly 37% of total deployments due to their multifunctional capabilities, broad application compatibility, and scalable integration with athlete analytics platforms. Professional sports teams and fitness ecosystems increasingly prefer smartwatches because they combine biometric tracking, GPS functionality, recovery analytics, and cloud synchronization within a single device architecture. Smart clothing is emerging as the fastest-growing segment, with adoption rising by approximately 31% in 2026 as sports organizations seek non-invasive monitoring and continuous physiological tracking. Compared with mature fitness bands, smart clothing delivers nearly 24% higher motion accuracy during high-intensity training sessions. Heart rate monitors continue to retain strategic relevance in rehabilitation and endurance sports, while GPS tracking devices remain operationally critical for football, cycling, and marathon training environments. Companies are expanding investments in flexible biosensors, AI-enabled dashboards, and lightweight wearable ecosystems to strengthen product differentiation and long-term athlete engagement.

Performance monitoring represents the dominant application segment as professional sports organizations, collegiate programs, and fitness operators prioritize real-time athlete optimization and workload management. Nearly 42% of wearable deployments in 2026 were linked directly to performance analytics systems integrating biometric tracking, fatigue analysis, and motion assessment tools. Injury prevention is the fastest-growing application, expanding rapidly as AI-driven predictive analytics reduced soft tissue injury incidents by approximately 26% in controlled training environments. Compared with traditional fitness tracking, advanced sports analytics platforms now improve coaching response efficiency by nearly 29% through continuous data interpretation and automated alerts. Athlete training and health monitoring applications are also gaining operational importance across rehabilitation-focused sports programs and endurance training facilities. Companies are scaling cloud-connected analytics infrastructure, expanding machine-learning capabilities, and integrating wearable ecosystems with sports medicine platforms to strengthen enterprise adoption and long-term operational value.

Professional athletes remain the dominant end-user segment due to intensive performance monitoring requirements, continuous recovery management, and large-scale deployment across organized sports ecosystems. Nearly 39% of advanced wearable device utilization in 2026 originated from elite athlete training programs integrating AI-based fatigue analytics and biomechanical tracking systems. Fitness centers are emerging as the fastest-growing end-user segment, with connected wearable adoption increasing by approximately 33% as commercial gyms integrate personalized coaching dashboards and subscription-based recovery analytics. Sports teams continue investing heavily in centralized athlete intelligence platforms, while healthcare providers are expanding wearable integration within sports rehabilitation and post-injury recovery programs. Individual consumers increasingly prefer multifunctional sports wearables with hydration monitoring and stress analytics capabilities, particularly in the United States and South Korea. Companies are responding through tiered pricing strategies, sports league partnerships, and ecosystem-driven product customization to secure long-term engagement across both enterprise and consumer-driven segments.

North America accounted for the largest market share at 34.7% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

AI-Driven Athlete Monitoring Dominates Enterprise Deployment

North America maintains leadership in wearable devices in sports through high enterprise deployment density, advanced analytics infrastructure, and strong integration across professional leagues and collegiate athletics. Nearly 63% of elite sports organizations in the United States and Canada utilize real-time biometric tracking platforms integrated with cloud-based coaching systems. Demand is accelerating for AI-enabled recovery analytics, hydration monitoring, and motion intelligence solutions following stricter athlete safety protocols across contact sports. Semiconductor and sports technology partnerships expanded significantly in 2026, with several wearable manufacturers localizing assembly and software operations to reduce supply-chain delays by approximately 19%. The region also benefits from strong sports medicine infrastructure and enterprise spending capacity, enabling faster commercialization of premium wearable ecosystems and predictive performance analytics platforms.

United States Market Outlook: The United States remains the operational center of the regional market due to large-scale professional sports infrastructure, advanced sports science adoption, and strong investment activity across athlete analytics platforms. More than 70% of professional sports franchises now integrate wearable monitoring into centralized performance management systems. Universities and Olympic training centers are increasing deployment of AI-powered fatigue analysis and biomechanical tracking tools, while enterprise partnerships between semiconductor firms and sports analytics providers are strengthening domestic innovation capacity and accelerating premium wearable device development.

Regulatory Compliance Reshapes Wearable Infrastructure

Europe is strengthening its position through athlete data governance modernization, sustainable electronics adoption, and advanced football analytics deployment. Nearly 49% of professional football clubs across Germany, France, and the United Kingdom integrated wearable-based injury prediction systems into training operations during 2026. Demand for secure biometric data infrastructure increased following stricter digital privacy regulations, pushing companies toward encrypted cloud environments and regionalized data processing operations. Smart textile manufacturing capacity also expanded across Germany and Italy, improving supply-chain stability for premium sports wearables. Sports rehabilitation centers are increasingly adopting connected recovery monitoring systems, while enterprise collaborations between medical technology firms and sports organizations are accelerating commercialization of AI-enabled physiological analytics across elite and semi-professional sports ecosystems.

Germany Market Outlook: Germany leads the European market through advanced engineering capability, smart textile manufacturing strength, and structured sports science integration. More than 54% of Bundesliga-affiliated performance centers deployed wearable-assisted biomechanics systems in 2026 to optimize injury prevention and athlete recovery programs. The country’s industrial electronics ecosystem supports rapid sensor innovation, while collaboration between rehabilitation clinics, sports institutes, and wearable manufacturers is strengthening enterprise-grade analytics deployment across professional athletics and sports medicine applications.

Manufacturing Scale Accelerates Global Supply Position

Asia-Pacific is emerging as the fastest-expanding regional market due to large-scale electronics manufacturing, rapid fitness digitization, and growing professional sports investments. China, Japan, and South Korea collectively account for more than 46% of global sports wearable sensor production capacity, strengthening the region’s role in supply-chain integration and component scalability. Deployment of AI-enabled fitness tracking systems increased by approximately 37% across urban fitness centers and organized sports academies in 2026. Governments and private investors are expanding semiconductor fabrication and flexible electronics infrastructure to support smart textile and biosensor production. Regional manufacturers are also focusing on lightweight wearable designs, low-power chips, and localized assembly strategies to improve export competitiveness and reduce international procurement dependency.

China Market Outlook: China dominates regional production through vertically integrated electronics manufacturing, large-scale sensor assembly operations, and expanding connected fitness ecosystems. More than 61% of domestic commercial fitness chains integrated wearable-compatible coaching systems in 2026 to improve customer engagement and personalized training efficiency. The country’s semiconductor expansion initiatives and smart manufacturing investments continue strengthening supply-chain resilience, while domestic wearable brands are aggressively scaling AI-enabled sports analytics platforms for both professional athletics and mass-market fitness applications.

Football Analytics Drive Regional Adoption

South America is experiencing steady wearable device adoption driven by professional football infrastructure modernization and expanding fitness technology penetration. Brazil and Argentina remain the primary deployment hubs, accounting for nearly 58% of regional professional sports wearable utilization in 2026. Clubs are increasingly implementing GPS-based workload monitoring and injury prevention systems to improve player availability and training precision. Infrastructure limitations and imported component dependency continue affecting premium device affordability and deployment consistency across smaller sports institutions. However, regional distributors and fitness technology providers are strengthening partnerships with global sports analytics firms to improve software accessibility and reduce implementation complexity. Demand is also increasing among private sports academies seeking cloud-connected athlete monitoring platforms and automated recovery management systems.

Brazil Market Outlook: Brazil leads the regional market due to its extensive football ecosystem, expanding sports academy infrastructure, and increasing commercial fitness adoption. Nearly 47% of top-tier football clubs deployed AI-assisted wearable tracking systems during 2026 to improve tactical performance analysis and injury management. Domestic distributors are expanding partnerships with international wearable manufacturers, while private training facilities are investing in connected recovery analytics platforms to strengthen athlete development programs and improve long-term operational competitiveness.

Sports Infrastructure Modernization Expands Deployment

The Middle East & Africa market is advancing through sports infrastructure investments, international event preparation programs, and expanding connected fitness adoption. Gulf countries are driving most regional deployment activity, with nearly 44% of premium wearable device implementation linked to elite sports academies and national training centers. Governments are increasing investment in sports science facilities, digital athlete monitoring systems, and AI-enabled recovery platforms to strengthen international competitiveness. Wearable adoption is also expanding within private fitness chains and rehabilitation clinics, particularly in the United Arab Emirates and Saudi Arabia. Regional market growth remains partially constrained by limited localized manufacturing and dependence on imported high-performance sensor components, prompting companies to pursue strategic partnerships and distribution expansion initiatives.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s most strategically important market due to large-scale sports infrastructure modernization, rising investment in athlete development, and rapid expansion of connected fitness facilities. More than 40% of newly established elite training centers incorporated wearable-integrated performance monitoring systems in 2026. National sports transformation initiatives are encouraging partnerships between global wearable manufacturers, sports medicine providers, and technology integrators to accelerate advanced athlete analytics deployment and strengthen long-term regional sports technology capabilities.

Global technology leaders such as Apple, Garmin, Polar, Catapult Sports, and Fitbit compete aggressively against specialized sports analytics providers and lower-cost Asian device manufacturers. The top five players collectively control nearly 48% of market activity through ecosystem integration, sensor accuracy, software interoperability, and enterprise sports partnerships. Premium brands compete on AI-enabled analytics and battery efficiency, while regional manufacturers focus on cost optimization and faster production cycles, often delivering devices 18% cheaper than established competitors. Sports analytics firms are strengthening vertical integration by combining wearable hardware with cloud-based coaching and recovery platforms that improve athlete monitoring efficiency by approximately 27%. Competition is intensifying around smart textiles, edge-processing capability, and secure biometric data management as professional leagues tighten athlete data governance standards. High-performance sensor sourcing and proprietary analytics software remain major entry barriers. Companies that combine scalable manufacturing, predictive analytics precision, and enterprise-grade interoperability are securing stronger long-term competitive advantage.

Apple Inc.

Garmin Ltd.

Fitbit Inc.

Polar Electro Oy

Catapult Sports

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Suunto Oy

Whoop Inc.

Xiaomi Corporation

Zepp Health Corporation

Under Armour Inc.

Sony Group Corporation

COROS Wearables Inc.

AI-enabled biometric analytics, multi-band GPS tracking, and low-power edge computing remain the most commercially relevant technologies in the wearable devices in sports market. In 2026, nearly 64% of elite sports organizations integrated real-time physiological monitoring systems into centralized coaching workflows, improving athlete recovery assessment efficiency by approximately 29%. Compared with legacy GPS-only trackers, AI-assisted wearables now deliver nearly 31% faster fatigue interpretation and 24% higher motion accuracy during high-intensity training. Companies are prioritizing secure cloud synchronization, sensor miniaturization, and battery optimization to strengthen enterprise deployment scalability and athlete data reliability.

Emerging technologies such as smart textiles, graphene biosensors, and sweat-based hydration analytics are reshaping wearable integration across endurance sports and rehabilitation programs. Sensor-embedded apparel adoption increased by approximately 34% during 2026 as lightweight conductive fabrics improved continuous monitoring without restricting movement. Japanese and South Korean manufacturers are expanding flexible electronics production to reduce component dependency and accelerate deployment across commercial fitness ecosystems and professional sports academies.

Disruptive innovation between 2026 and 2028 will center on predictive injury intelligence, neural sensing wearables, and autonomous recovery analytics platforms. Companies controlling AI software ecosystems, semiconductor partnerships, and secure biometric infrastructure will gain stronger competitive advantage as sports organizations increasingly prioritize scalable athlete intelligence platforms over standalone hardware products.

September 2024 – Apple introduced Apple Watch Ultra 2 with advanced training load analytics, sleep apnea notifications, and dual-frequency GPS capabilities, extending battery performance up to 72 hours in low-power mode for endurance athletes. Business impact: strengthened premium sports wearable positioning.

May 2024 – WHOOP expanded wearable performance platform operations into 56 global markets while strengthening multilingual AI-driven recovery analytics capabilities across sports and fitness ecosystems. Business impact: accelerated international subscriber acquisition and enterprise deployment scale.

September 2025 – Garmin announced a strategic research collaboration with King’s College London covering up to 40,000 participants using smartwatch biometric monitoring for advanced digital health and physiological analytics research. Business impact: strengthened institutional wearable analytics credibility.

July 2025 – Garmin acquired sports timing company MYLAPS to integrate race timing, live tracking, and performance analytics technologies supporting millions of athletes across cycling, running, and motorsports environments. Business impact: expanded vertically integrated sports performance ecosystem capabilities.

The report provides detailed analysis of the wearable devices in sports market across major technology categories including smartwatches, fitness bands, smart clothing, heart rate monitors, and GPS tracking devices. It evaluates operational demand across performance monitoring, fitness tracking, injury prevention, athlete training, health monitoring, and sports analytics applications. The study covers adoption trends among professional athletes, sports teams, healthcare providers, sports academies, fitness centers, and individual consumers, while assessing deployment concentration across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report examines AI-enabled biometric analytics, smart textiles, predictive injury intelligence, edge computing integration, and cloud-connected athlete monitoring platforms shaping market evolution between 2026 and 2033. More than 60% of enterprise sports deployments now incorporate real-time physiological tracking systems, highlighting the operational shift toward connected performance ecosystems. Strategic insights focus on supply-chain restructuring, regional manufacturing expansion, enterprise partnerships, competitive positioning, commercialization strategies, and technology adoption patterns influencing long-term investment and expansion priorities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 41517.32 Million |

|

Market Revenue in 2033 |

USD 81639.27 Million |

|

CAGR (2026 - 2033) |

8.82% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple Inc., Garmin Ltd., Fitbit Inc., Polar Electro Oy, Catapult Sports, Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Suunto Oy, Whoop Inc., Xiaomi Corporation, Zepp Health Corporation, Under Armour Inc., Sony Group Corporation, COROS Wearables Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |