Reports

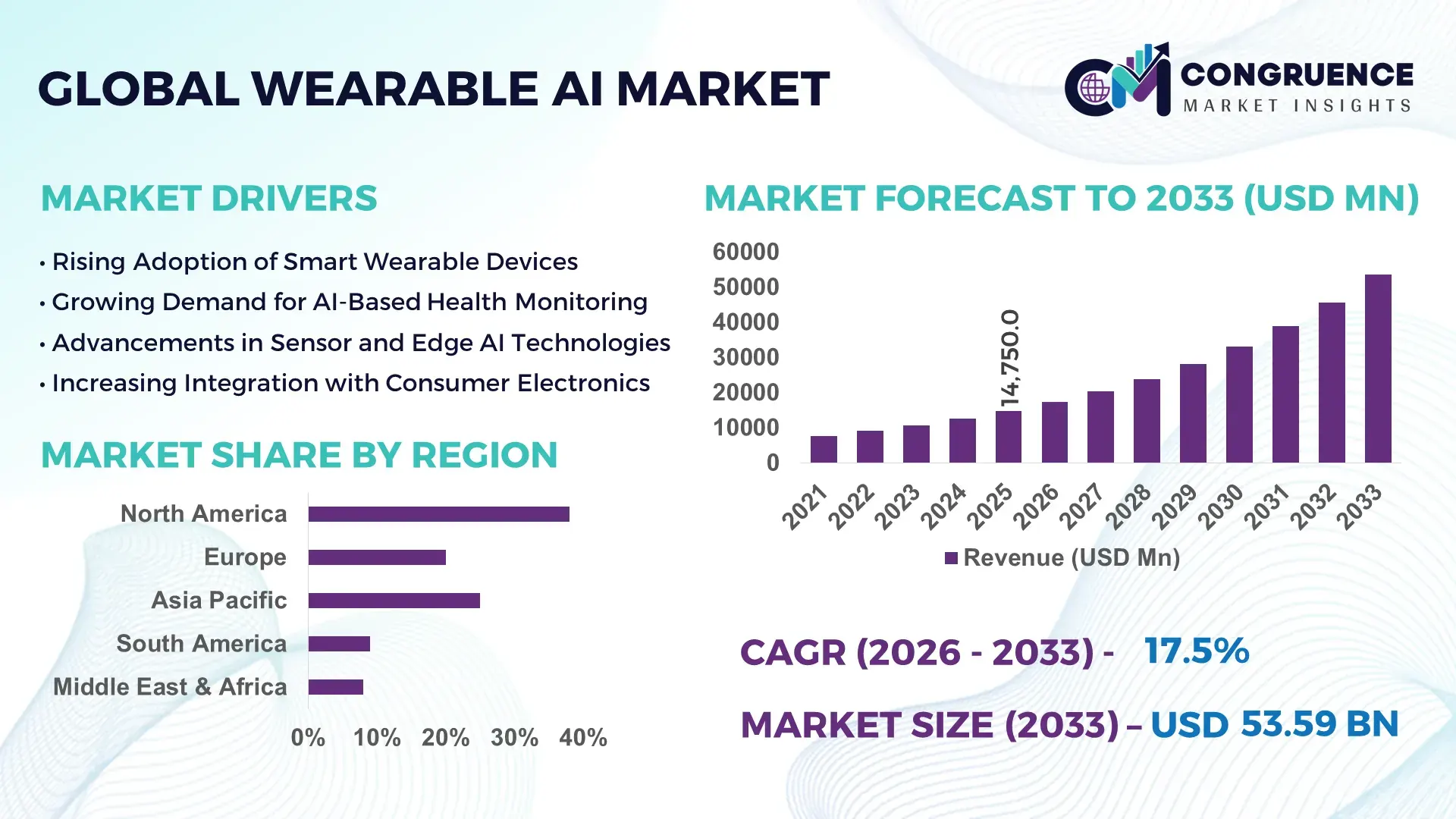

The Global Wearable AI Market was valued at USD 14750 Million in 2025 and is anticipated to reach a value of USD 53591.38 Million by 2033 expanding at a CAGR of 17.5% between 2026 and 2033. The growth is largely driven by increasing adoption of AI-enabled wearable devices across healthcare, fitness monitoring, industrial safety, and consumer electronics applications.

The United States remains a central hub for wearable AI development and deployment, supported by strong semiconductor capabilities, advanced healthcare infrastructure, and continuous technology investments. In 2024, the country recorded shipments exceeding 95 million wearable devices, including AI-powered smartwatches, augmented reality glasses, and intelligent health trackers. Over 40% of hospitals in the U.S. are piloting AI-enabled wearable patient monitoring systems that analyze biometric data such as heart rate variability, sleep patterns, and glucose levels in real time. Technology companies and startups collectively invested more than USD 4 billion in wearable AI hardware and software platforms between 2023 and 2025, accelerating innovation in edge AI chips and low-power neural processing units. Industrial sectors are also deploying AI wearables for worker safety monitoring, with over 25% of large manufacturing plants implementing smart helmets and biometric safety bands.

• Market Size & Growth: The wearable AI market reached USD 14750 million in 2025 and is projected to reach USD 53591.38 million by 2033 with a CAGR of 17.5%, supported by rapid integration of artificial intelligence into health monitoring, enterprise mobility, and smart consumer devices.

• Top Growth Drivers: AI-powered health tracking adoption (48%), enterprise worker productivity improvement (35%), and smart fitness device penetration (42%).

• Short-Term Forecast: By 2028, AI-driven wearable analytics platforms are expected to improve real-time health monitoring accuracy by nearly 30% while reducing device energy consumption by 18%.

• Emerging Technologies: Edge AI processors, biometric sensor fusion technology, and AI-enabled augmented reality wearables are reshaping real-time data analytics capabilities in wearable devices.

• Regional Leaders: North America projected to exceed USD 18 billion by 2033 with strong healthcare integration; Asia-Pacific expected to approach USD 16 billion driven by consumer electronics manufacturing; Europe anticipated to reach USD 12 billion with rising enterprise wearable adoption.

• Consumer/End-User Trends: Healthcare providers, fitness enthusiasts, logistics workers, and industrial safety teams represent major end-users, with health monitoring wearables accounting for nearly 38% of device usage globally.

• Pilot or Case Example: In 2024, a manufacturing safety pilot in Japan deployed AI-powered smart helmets, reducing workplace accidents by 22% and improving worker productivity by 15%.

• Competitive Landscape: Apple holds roughly 28% of the wearable AI ecosystem, followed by Samsung, Huawei, Fitbit, and Garmin with strong device innovation and AI health analytics platforms.

• Regulatory & ESG Impact: Governments are implementing digital health regulations and data privacy standards, while manufacturers aim for 20% recyclable materials in wearable electronics by 2030.

• Investment & Funding Patterns: Venture capital and corporate investments in wearable AI startups surpassed USD 7 billion between 2023 and 2025, focusing on AI chipsets, digital health analytics, and smart sensor technology.

• Innovation & Future Outlook: Integration of generative AI assistants, predictive health algorithms, and AI-powered gesture recognition is expected to transform wearable devices into autonomous personal health and productivity platforms.

Wearable AI solutions are rapidly expanding across multiple industry sectors, with healthcare contributing nearly 35% of device applications through continuous patient monitoring and remote diagnostics. Consumer fitness and lifestyle devices account for approximately 30% of global demand, while enterprise applications in logistics, manufacturing, and field services represent close to 20% of deployments. Recent product innovations include AI-enabled smart rings capable of tracking over 20 biometric parameters and smart glasses equipped with real-time object recognition. Regulatory emphasis on digital health data protection and medical device compliance is encouraging companies to develop secure AI analytics platforms. Regional consumption patterns indicate strong growth in Asia-Pacific due to high smartphone penetration and electronics manufacturing capacity, while Europe shows rising demand for occupational safety wearables in industrial environments.

The wearable AI market is becoming strategically significant as organizations increasingly rely on real-time biometric analytics, predictive health insights, and intelligent workforce monitoring systems. Enterprises are integrating wearable AI technologies into operational workflows to enhance productivity, employee safety, and healthcare outcomes. AI-powered sensor fusion platforms combine data from heart rate monitors, accelerometers, oxygen sensors, and motion tracking systems to deliver continuous analytics across healthcare and industrial environments. Advanced edge computing chips embedded in wearable devices now process large volumes of data locally, reducing latency and enabling faster decision-making in medical monitoring and workplace safety scenarios.

Comparatively, edge-based AI wearable processors deliver nearly 45% faster data analysis compared to traditional cloud-dependent wearable platforms. This improvement significantly reduces connectivity dependence and improves response times for health alerts and industrial risk detection. North America dominates in device shipment volume due to strong consumer electronics demand, while Asia-Pacific leads in adoption with nearly 52% of electronics manufacturers integrating AI capabilities into wearable devices.

Practical applications illustrate the measurable value of wearable AI adoption. In 2024, a South Korean healthcare network deployed AI-enabled patient monitoring wearables across intensive care units, improving early anomaly detection rates by 32% and reducing emergency response time by 18%. As digital healthcare ecosystems and smart enterprise operations continue to expand, the wearable AI market is positioned to serve as a foundational technology supporting resilience, regulatory compliance, and sustainable innovation across multiple global industries.

The rapid growth of digital health monitoring technologies is a major driver of the wearable AI market. Healthcare providers and consumers are increasingly adopting AI-enabled wearable devices that track vital health indicators continuously and provide predictive analytics. Studies indicate that more than 65% of healthcare institutions globally are exploring wearable technologies for remote patient monitoring, particularly for chronic disease management such as cardiovascular disorders and diabetes. AI-powered wearable sensors can analyze heart rhythm irregularities, sleep disorders, and metabolic patterns with accuracy improvements of nearly 25% compared to earlier wearable health trackers. Remote patient monitoring programs using AI wearables have demonstrated the ability to reduce hospital readmissions by up to 20% in pilot healthcare programs. The growing integration of wearable AI devices with telemedicine platforms and digital health records is further strengthening their role in preventive healthcare and personalized treatment strategies.

Despite its strong growth potential, the wearable AI market faces significant restraints related to data privacy, cybersecurity, and regulatory compliance. Wearable AI devices collect large volumes of sensitive personal data, including health metrics, location tracking, and behavioral patterns. Industry surveys indicate that nearly 58% of consumers express concerns about how wearable devices store and process personal health data. Regulatory frameworks such as health data protection rules and digital privacy laws require manufacturers to implement advanced encryption, secure cloud integration, and strict data governance practices. However, implementing these cybersecurity safeguards increases development complexity and operational costs. Additionally, the interconnected nature of wearable devices and mobile ecosystems exposes them to potential cyber threats and unauthorized access. These challenges often slow enterprise adoption and require continuous investment in secure AI infrastructure to maintain user trust and regulatory compliance.

The integration of artificial intelligence into enterprise wearable devices presents significant opportunities across industrial and workforce management sectors. Companies are increasingly deploying AI-powered smart helmets, biometric safety bands, and augmented reality glasses to enhance worker safety and operational efficiency. These devices use machine learning algorithms to detect hazardous conditions, monitor fatigue levels, and provide real-time guidance to employees performing complex tasks. In logistics operations, AI-enabled wearable scanners have improved order fulfillment accuracy by approximately 30% while reducing manual errors. Industrial safety wearables equipped with environmental sensors can detect toxic gas exposure or unsafe working conditions and immediately alert supervisors. As industrial automation and smart manufacturing initiatives expand globally, enterprises are expected to invest heavily in wearable AI platforms that integrate seamlessly with factory monitoring systems, predictive maintenance tools, and workforce management software.

Hardware limitations and battery performance constraints remain critical challenges affecting the wearable AI market. Wearable devices must balance processing power, sensor integration, connectivity, and battery life within compact and lightweight designs. AI algorithms require significant computational resources to analyze biometric and environmental data in real time, which can increase power consumption. Many wearable devices currently operate with battery durations ranging from 24 to 72 hours depending on usage intensity, creating challenges for continuous monitoring applications. Furthermore, integrating advanced sensors such as electrocardiogram modules, temperature sensors, and motion detectors increases hardware complexity and manufacturing costs. Engineers are working to address these issues through low-power AI chipsets and improved battery technologies, but limitations in miniaturized energy storage remain a technical barrier. Overcoming these challenges will be essential for scaling next-generation wearable AI devices across healthcare, enterprise, and consumer applications.

• Rapid Expansion of AI-Enabled Health Monitoring Devices: Healthcare-focused wearable AI devices are witnessing strong global uptake as consumers and medical institutions prioritize continuous health tracking. More than 62% of newly launched wearable devices in 2024 included AI-powered biometric analytics capable of monitoring heart rhythm, oxygen saturation, sleep quality, and stress levels. Hospitals integrating AI wearables into remote patient monitoring programs have reported improvements of nearly 28% in early anomaly detection rates. In addition, over 70 million wearable health monitoring devices were shipped globally during the same period, reflecting strong demand from both clinical and consumer health segments.

• Growth of Edge AI Processing in Wearable Devices: The integration of edge-based artificial intelligence chips is transforming wearable device capabilities by enabling real-time data analysis without relying heavily on cloud connectivity. Approximately 48% of new wearable AI products released in 2025 incorporate on-device neural processing units capable of performing predictive analytics locally. These processors have reduced response latency by nearly 35% while improving data processing efficiency by approximately 30%. Device manufacturers are increasingly embedding low-power AI chipsets that allow smartwatches and smart glasses to run multiple machine learning models simultaneously.

• Increasing Enterprise Adoption of Industrial Safety Wearables: Industrial sectors are rapidly deploying AI-powered wearable technologies to enhance worker safety and productivity. Around 41% of large manufacturing and logistics facilities have implemented wearable AI solutions such as smart helmets, biometric wristbands, and AI-enabled safety glasses. These systems analyze worker movements, fatigue patterns, and environmental conditions in real time. Companies using AI-powered safety wearables have reported reductions of nearly 24% in workplace accidents and improvements of around 18% in operational efficiency due to proactive risk detection and automated safety alerts.

• Surge in AI-Integrated Smart Glasses and Augmented Reality Wearables: AI-powered augmented reality wearables are emerging as a transformative trend across field service, healthcare, and logistics operations. More than 32% of enterprise organizations experimenting with augmented reality technologies are testing AI-enabled smart glasses capable of object recognition, visual instructions, and remote collaboration support. These systems can reduce training time for complex technical tasks by nearly 26%. Additionally, logistics companies deploying AI smart glasses for warehouse operations have reported picking accuracy improvements of approximately 30%, demonstrating the operational value of wearable AI-enabled visual computing.

The wearable AI market demonstrates a diverse segmentation structure driven by technological innovation and cross-industry adoption. Product segmentation includes smartwatches, smart glasses, smart clothing, and fitness trackers, each supporting different AI-enabled capabilities such as biometric monitoring, gesture recognition, and real-time analytics. Among applications, healthcare monitoring, fitness and lifestyle management, and enterprise productivity solutions represent the most prominent use cases. Healthcare adoption has expanded rapidly due to the ability of wearable AI devices to analyze physiological indicators such as heart rhythm, sleep patterns, and activity levels in real time. Application diversification is also occurring in industrial sectors where AI wearables are deployed for worker safety and environmental monitoring. End-user segmentation highlights strong participation from healthcare providers, consumer electronics users, manufacturing organizations, and logistics enterprises. These segments collectively contribute to a rapidly evolving ecosystem where artificial intelligence, sensor technologies, and connected device platforms converge to create intelligent wearable solutions supporting both personal and enterprise-level decision-making.

The wearable AI market includes several major product types such as smartwatches, smart glasses, fitness trackers, and AI-enabled smart clothing. Among these categories, smartwatches currently represent the leading product type, accounting for nearly 46% of global wearable AI device adoption. Their dominance is driven by multi-functional capabilities including biometric monitoring, AI-driven fitness analytics, mobile connectivity, and integration with digital health ecosystems. Fitness trackers follow with approximately 27% of device adoption, widely used for activity tracking, calorie monitoring, and personal wellness insights. Smart glasses represent a rapidly emerging category used for augmented reality visualization, object recognition, and hands-free enterprise collaboration.

Smart clothing and biometric sensor wearables are currently niche segments but continue gaining traction in specialized healthcare and sports analytics applications. Collectively, these emerging device categories account for roughly 27% of the wearable AI product ecosystem. However, AI-powered smart glasses represent the fastest-growing segment, expanding at an estimated CAGR of nearly 19% due to increasing enterprise use in logistics, remote assistance, and technical training environments.

The wearable AI market spans multiple application segments including healthcare monitoring, fitness and lifestyle management, enterprise productivity solutions, and industrial safety monitoring. Healthcare monitoring remains the dominant application area, accounting for approximately 39% of wearable AI usage. Hospitals and healthcare providers increasingly deploy wearable AI sensors to monitor heart rhythm irregularities, respiratory patterns, sleep cycles, and chronic disease indicators in real time. Fitness and lifestyle management represents the second-largest segment with roughly 28% adoption, driven by growing consumer awareness of health metrics and personal wellness optimization.

Enterprise productivity applications including warehouse operations, field service support, and workforce monitoring contribute around 19% of current wearable AI usage. Industrial safety monitoring, involving hazard detection and worker fatigue tracking, also continues to expand across manufacturing and mining environments. Among all applications, enterprise productivity solutions represent the fastest-growing category with an estimated CAGR of nearly 18%, driven by digital transformation initiatives and the adoption of AI-powered augmented reality wearables.

End-user segmentation in the wearable AI market includes healthcare institutions, consumer electronics users, industrial enterprises, and logistics and transportation companies. Consumer electronics users represent the largest end-user group, accounting for approximately 44% of wearable AI device adoption globally. This segment includes individuals using AI-powered smartwatches, fitness trackers, and smart rings to monitor health metrics, physical activity, sleep quality, and stress levels through mobile-connected platforms. Healthcare institutions account for nearly 29% of adoption as hospitals increasingly implement AI wearables for remote patient monitoring and digital health analytics. Industrial enterprises including manufacturing and construction organizations represent around 16% of the wearable AI user base. These organizations deploy AI-enabled safety wearables to monitor worker conditions, detect hazardous environments, and track physical movement patterns in real time. Logistics and transportation companies contribute the remaining 11% through the use of AI smart glasses and wearable scanning devices for warehouse automation and delivery operations. Healthcare institutions are currently the fastest-growing end-user segment with an estimated CAGR of approximately 20%, fueled by rising investments in digital health infrastructure and remote patient care platforms.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.2% between 2026 and 2033.

North America’s leadership is supported by high adoption of AI-powered consumer wearables, enterprise safety devices, and advanced healthcare monitoring platforms. The region recorded shipments exceeding 110 million wearable AI devices in 2025, with more than 52% of hospitals experimenting with remote patient monitoring technologies. Europe represented approximately 27% of global demand, driven by digital healthcare programs and increasing enterprise adoption of augmented reality wearables. Asia-Pacific accounted for roughly 25% of global wearable AI consumption, supported by large-scale electronics manufacturing capacity and rapidly expanding smartphone ecosystems across China, Japan, and India. Meanwhile, South America and the Middle East & Africa collectively contributed close to 10% of the market, with adoption growing across logistics, oil & gas safety monitoring, and fitness applications. Across all regions, over 420 million wearable AI devices are currently in active use globally, with approximately 64% connected to mobile AI analytics platforms.

How are advanced digital health ecosystems accelerating intelligent wearable technology adoption?

North America accounts for nearly 38% of global wearable AI adoption, supported by strong demand from healthcare, consumer electronics, and enterprise workforce management sectors. The United States dominates the regional landscape with more than 85 million active AI-powered wearable devices in use across healthcare monitoring, fitness tracking, and occupational safety programs. Digital health integration is particularly strong, with approximately 48% of healthcare institutions implementing wearable-based patient monitoring solutions. Government health initiatives promoting telemedicine and remote monitoring have also accelerated adoption. Technological advancements in low-power AI processors and biometric sensor fusion are driving next-generation wearable capabilities in the region. Enterprise adoption is also expanding rapidly in logistics and manufacturing industries where wearable safety devices track worker fatigue and environmental exposure. A prominent regional player has expanded its wearable AI ecosystem by integrating predictive health algorithms into its smartwatch platform, enabling real-time cardiovascular anomaly detection for millions of users. Consumer behavior trends indicate higher enterprise and healthcare adoption, with over 60% of corporate wellness programs incorporating wearable AI devices for employee health tracking.

How are strict data governance policies shaping intelligent wearable technology deployment?

Europe represents approximately 27% of the global wearable AI market, with major adoption occurring across Germany, the United Kingdom, and France. The region has witnessed increasing demand for AI-powered wearable devices across healthcare monitoring, workplace safety, and sports performance analytics. Germany leads regional adoption with more than 18 million wearable AI devices currently in use, followed by the UK with around 15 million connected wearables integrated into mobile health platforms. Regulatory oversight plays a significant role in shaping the European market environment. Data protection regulations and medical device standards have encouraged companies to develop secure AI analytics systems and explainable health monitoring algorithms. Sustainability initiatives across the region are also influencing product development, with manufacturers targeting over 25% recyclable materials in wearable hardware components. European technology firms are investing in augmented reality wearable solutions for industrial maintenance and training environments. Consumer behavior in the region reflects cautious but steady adoption patterns, where regulatory compliance and data transparency strongly influence purchasing decisions.

What factors are driving rapid expansion of intelligent wearable technologies in digital-first economies?

Asia-Pacific ranks among the fastest expanding regions in the wearable AI ecosystem, accounting for roughly 25% of global device consumption and representing the largest manufacturing hub for wearable electronics. China, Japan, and India collectively account for more than 70% of regional wearable device shipments, supported by strong consumer electronics production capacity and rapidly expanding mobile AI application ecosystems. China alone manufactures more than 40% of the world’s wearable AI hardware components, including smart sensors and edge AI processors. Innovation hubs across Shenzhen, Tokyo, and Bangalore are driving research in AI-enabled biometric analytics, gesture recognition systems, and smart eyewear technologies. Manufacturing investments in miniaturized semiconductor chips have enabled companies to produce compact wearable AI devices capable of processing large data volumes locally. A leading regional electronics manufacturer recently launched a smartwatch equipped with AI-powered health diagnostics capable of tracking over 20 physiological indicators simultaneously. Consumer behavior trends indicate strong growth driven by e-commerce adoption and mobile AI apps, with wearable device usage among urban consumers exceeding 35%.

How are digital transformation initiatives encouraging adoption of intelligent wearable solutions?

South America currently accounts for approximately 6% of global wearable AI demand, with Brazil and Argentina representing the largest national markets in the region. Brazil alone hosts more than 14 million active wearable devices used primarily for fitness monitoring and personal health tracking. The regional market is gradually expanding as digital transformation initiatives and mobile internet penetration continue to rise. More than 72% of urban consumers in Brazil now use smartphones capable of connecting with wearable AI applications. Enterprise adoption is also increasing across logistics and industrial safety sectors. Oil, mining, and construction companies are exploring wearable AI solutions such as smart helmets and biometric safety trackers to improve worker monitoring and reduce workplace incidents. Government policies supporting digital health innovation have encouraged healthcare providers to integrate wearable monitoring systems into patient care programs. Consumer behavior patterns across the region show strong interest in fitness and lifestyle wearables, with nearly 46% of wearable device purchases linked to health and exercise tracking applications.

How are smart infrastructure investments accelerating intelligent wearable technology deployment?

The Middle East & Africa region represents roughly 4% of global wearable AI adoption but is showing steady growth as industries adopt digital monitoring technologies. Countries such as the United Arab Emirates and South Africa are leading adoption, particularly in sectors including oil & gas, construction, and healthcare services. In the UAE, more than 1.8 million wearable AI devices are actively used for health tracking, enterprise productivity monitoring, and sports performance analysis. Technological modernization initiatives across smart city programs are encouraging the use of wearable AI devices integrated with IoT-based urban infrastructure systems. Oil and gas companies are increasingly deploying AI-enabled smart helmets and biometric monitoring devices to track worker fatigue and hazardous exposure levels. Regional governments are also promoting digital healthcare initiatives that incorporate wearable monitoring tools for chronic disease management. Consumer adoption in the region reflects strong interest in health-focused devices, with approximately 35% of wearable purchases linked to fitness and lifestyle tracking applications.

• United States – 34% Wearable AI Market Share: The United States leads the wearable AI market due to strong consumer electronics demand, extensive healthcare digitalization programs, and high investment in AI-enabled wearable technologies.

• China – 21% Wearable AI Market Share: China maintains a leading position through large-scale manufacturing capacity, strong domestic consumer adoption, and extensive development of AI-integrated wearable electronics.

The wearable AI market is characterized by a moderately fragmented competitive landscape with more than 70 active global and regional technology companies developing intelligent wearable devices, AI software platforms, and sensor technologies. The top five companies collectively account for approximately 55% of total industry activity, supported by strong brand recognition, advanced semiconductor capabilities, and large-scale product ecosystems. Competition in the market is largely driven by continuous innovation in biometric sensors, AI-enabled analytics platforms, and low-power edge computing processors.

Major technology firms are investing heavily in research and development to expand the capabilities of wearable AI devices. Over 300 new wearable AI product models were introduced globally between 2023 and 2025, many incorporating advanced health diagnostics, gesture recognition systems, and AI-powered personal assistants. Strategic partnerships between semiconductor manufacturers, healthcare organizations, and consumer electronics companies are accelerating product innovation cycles.

Mergers, acquisitions, and ecosystem partnerships are also reshaping competitive dynamics. Several companies are forming alliances with healthcare technology providers to integrate wearable AI data with telemedicine platforms and hospital analytics systems. At the same time, enterprise-focused wearable solutions for industrial safety and logistics automation are gaining traction, encouraging companies to develop specialized wearable AI hardware. As competition intensifies, companies are differentiating themselves through advanced AI algorithms, improved battery efficiency, and integrated digital health services that transform wearable devices into intelligent personal data platforms.

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Garmin Ltd.

Sony Corporation

Xiaomi Corporation

Google LLC

Meta Platforms, Inc.

Fitbit Inc.

Realme TechLife

Amazfit (Zepp Health Corporation)

Lenovo Group Limited

Technological innovation is the primary force shaping the wearable AI market, with advancements in edge computing, biometric sensors, and artificial intelligence algorithms transforming device capabilities. Modern wearable AI devices increasingly integrate multi-sensor architectures capable of monitoring more than 15 to 25 physiological indicators simultaneously, including heart rate variability, oxygen saturation, body temperature, and electrodermal activity. Sensor fusion technology enables these devices to combine data from accelerometers, gyroscopes, GPS modules, and optical sensors, allowing real-time contextual analysis of user activity and health conditions.

Edge AI processing is another major technological advancement driving the wearable AI ecosystem. Many next-generation wearable devices now include low-power neural processing units capable of executing machine learning models locally on the device. These processors can analyze biometric data in milliseconds while reducing cloud dependency and improving user privacy. Advanced wearable chipsets now operate at power consumption levels below 1 watt while supporting real-time anomaly detection, predictive health analytics, and motion recognition.

Artificial intelligence algorithms embedded in wearable devices are becoming more sophisticated, with predictive health models capable of identifying early indicators of cardiovascular irregularities and sleep disorders with accuracy improvements exceeding 25%. Gesture recognition technologies are also expanding rapidly, enabling smart glasses and smart rings to interpret over 30 unique hand movements for device control and augmented reality interaction.

Battery innovation is another crucial technology trend, as manufacturers develop compact lithium-polymer batteries capable of sustaining wearable devices for 48 to 72 hours of continuous monitoring. In parallel, flexible electronics and conductive textile technologies are enabling the development of AI-powered smart clothing embedded with micro-sensors and washable circuits. As these technologies mature, wearable AI devices are expected to become more autonomous, energy-efficient, and capable of delivering advanced predictive analytics for healthcare, industrial safety, and personal productivity applications.

• In January 2025, Samsung Electronics launched the Galaxy Ring, an AI-powered smart wearable designed to track sleep patterns, heart rate variability, and physical activity through advanced biometric sensors. The device integrates Samsung Health AI analytics to deliver personalized health insights and predictive wellness recommendations.

• In February 2024, Apple introduced the Apple Vision Pro, an advanced spatial computing wearable that combines artificial intelligence with augmented reality and gesture recognition technology. The device integrates eye-tracking sensors, voice commands, and real-time object recognition to enhance immersive computing and professional collaboration. Source: www.apple.com

• In September 2024, Meta Platforms expanded its Ray-Ban Meta smart glasses lineup with AI-powered visual recognition capabilities and hands-free voice interaction, allowing users to capture photos, stream live video, and receive contextual AI assistance directly through wearable smart eyewear. Source: www.meta.com

• In March 2025, Garmin introduced new AI-enhanced health monitoring features in its smartwatch ecosystem, enabling continuous tracking of stress levels, heart rate variability, and sleep quality using machine learning algorithms designed to provide predictive health insights and improved athlete performance analytics. Source: www.garmin.com

The Wearable AI Market Report provides a comprehensive evaluation of the global ecosystem of artificial intelligence-enabled wearable technologies across consumer, healthcare, and enterprise sectors. The report examines more than 10 major device categories including smartwatches, smart glasses, smart rings, fitness trackers, and AI-enabled smart clothing, each offering advanced capabilities such as biometric monitoring, gesture recognition, and contextual data analytics. It analyzes how wearable AI devices integrate with mobile applications, cloud computing platforms, and enterprise analytics systems to deliver real-time insights and predictive intelligence.

From a technology perspective, the report covers critical innovations including edge AI processors, multi-sensor biometric platforms, augmented reality visualization systems, and low-power machine learning models. The analysis evaluates how these technologies support applications such as remote patient monitoring, workplace safety monitoring, fitness and wellness tracking, and industrial productivity enhancement. More than 25 biometric parameters are now commonly monitored by advanced wearable devices, providing organizations and individuals with continuous streams of real-time health and activity data.

The report also provides extensive geographic coverage, examining adoption trends across five major regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Regional analysis includes evaluation of manufacturing capacity, device shipment volumes, enterprise adoption rates, and consumer usage patterns across more than 20 key countries. Industry-specific insights highlight the role of wearable AI in sectors such as healthcare, logistics, sports performance analytics, construction safety, and digital workforce management.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple Inc., Samsung Electronics Co., Ltd., Huawei Technologies Co., Ltd., Garmin Ltd., Sony Corporation, Xiaomi Corporation, Google LLC, Meta Platforms, Inc., Fitbit Inc., Realme TechLife, Amazfit (Zepp Health Corporation), Lenovo Group Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |