Reports

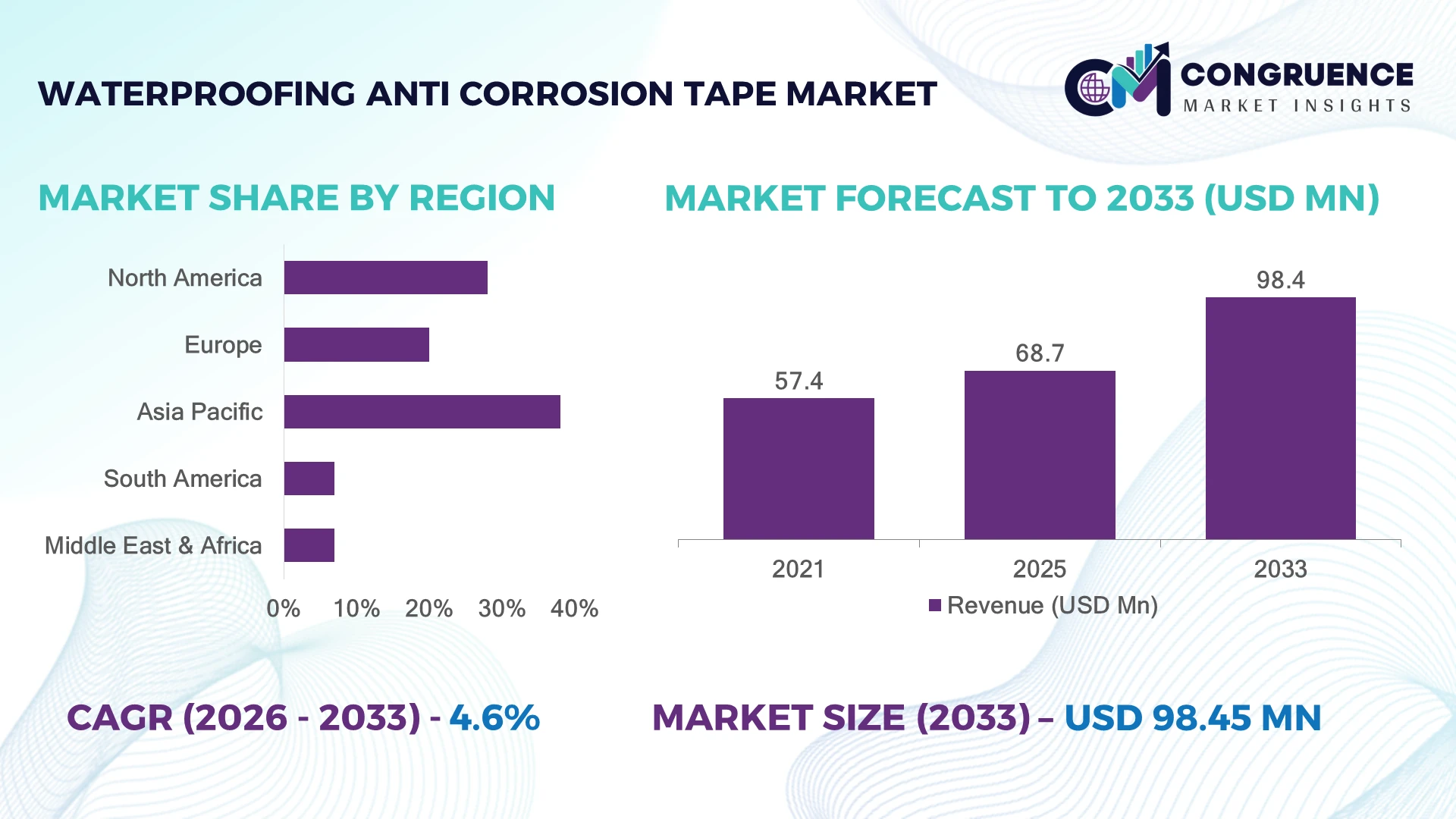

The Global Waterproofing Anti-Corrosion Tape Market was valued at USD 68.7 Million in 2025 and is anticipated to reach a value of USD 98.4 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Growth is driven by rising pipeline rehabilitation activities, increased use of advanced self-amalgamating tapes, and stricter corrosion protection requirements across oil & gas, marine, and infrastructure assets.

China dominates the global market with nearly 38% share supported by extensive pipeline networks, infrastructure modernization, and large-scale industrial investments under energy security initiatives. The country operates more than 100,000 km of oil and gas pipelines, creating strong demand for corrosion-resistant solutions. In comparison, North America accounts for approximately 28% share, driven by aging pipeline replacement programs and industrial maintenance spending, with adoption of advanced waterproofing tapes increasing by over 15% in critical infrastructure applications.

Strategic expansion into high-risk industrial zones and durable asset protection will define competitive positioning.

Market Size & Growth: Global market reaches USD 68.7 Million in 2025 and USD 98.4 Million by 2033 at 4.6% CAGR, supported by pipeline maintenance and advanced corrosion prevention materials.

Top Growth Drivers: Pipeline infrastructure renewal (35%), industrial corrosion protection demand (30%), and marine/offshore asset maintenance (25%) lead market expansion.

Short-Term Forecast: By 2028, automated wrapping systems and improved adhesive formulations reduce installation time by 20% and improve coating consistency.

Emerging Technologies: Advanced polymer tapes, AI-based corrosion monitoring integration, and automated application equipment are reshaping waterproofing protection.

Regional Leaders: Asia Pacific reaches approximately USD 40 Million by 2033 with infrastructure expansion; North America exceeds USD 27 Million with pipeline modernization; Europe approaches USD 22 Million through industrial compliance adoption.

Consumer/End-User Trends: Over 60% of industrial users prioritize long-life corrosion protection solutions to reduce maintenance cycles and downtime.

Pilot/Case Example: 2024 pipeline refurbishment projects using advanced anti-corrosion tapes achieved nearly 30% reduction in maintenance intervention frequency.

Competitive Landscape: Leading companies include 3M, Nitto Denko Corporation, Shurtape Technologies, Scapa Group, and Polyken, with established players controlling a significant portion of premium-grade applications.

Regulatory & ESG Impact: Infrastructure operators adopting corrosion-resistant solutions achieve up to 20% lower material waste through longer asset life cycles and reduced replacements.

Investment & Funding: More than USD 500 Million is being directed globally toward pipeline upgrades, industrial asset protection, and corrosion management technologies.

Innovation & Future Outlook: Next-generation tapes with higher temperature resistance, recyclable materials, and smart monitoring compatibility are driving the shift toward intelligent infrastructure protection.

Waterproofing Anti-Corrosion Tape solutions are gaining importance across oil pipelines, underground utilities, marine structures, and industrial facilities due to their ability to provide long-term moisture barriers and corrosion resistance. Demand is increasing for high-performance polymer-based tapes with stronger adhesion and environmental durability, with more than 40% of new infrastructure projects emphasizing extended asset protection cycles. Supply-chain diversification across Asia and increased infrastructure resilience programs are accelerating adoption of advanced corrosion-control materials, creating new opportunities for manufacturers.

The Waterproofing Anti-Corrosion Tape Market is becoming strategically important as industries prioritize asset longevity, operational reliability, and reduced maintenance exposure across critical infrastructure. Aging pipelines, offshore facilities, and industrial networks are driving a shift from traditional coating methods toward flexible corrosion protection systems that enable faster installation and lower operational disruption.

Infrastructure modernization programs and supply-chain restructuring are increasing demand for locally available advanced materials. Compared with conventional liquid coatings, modern polymer-based anti-corrosion tapes provide faster application cycles, reduce surface preparation requirements by approximately 25%, and improve repair efficiency in difficult environments.

Asia Pacific remains the largest deployment region due to rapid industrial expansion and pipeline investments, while North America leads in technology adoption through advanced inspection systems and rehabilitation projects. Europe emphasizes environmentally compliant materials aligned with industrial sustainability goals.

Companies are expanding production capacity, forming industrial partnerships, and investing in improved adhesive technologies to address demanding environments. For example, pipeline operators are increasingly combining corrosion tapes with digital inspection methods to improve maintenance planning. Competitive advantage will depend on delivering durable, efficient, and adaptable corrosion protection solutions for evolving infrastructure needs.

Aging pipeline networks and industrial asset protection programs are accelerating adoption of waterproofing anti-corrosion tapes, particularly across oil & gas, marine, and utility sectors. More than 35% of demand is linked to pipeline rehabilitation activities, while advanced polymer-based tapes improve installation efficiency by nearly 20% compared with traditional protection methods. China’s expansion of energy infrastructure and India’s pipeline modernization initiatives are strengthening procurement activity. Companies are responding by increasing production capacity, developing high-temperature resistant materials, and forming partnerships with infrastructure operators to deliver durable corrosion-control solutions for critical assets.

Fluctuating prices of polymer resins, adhesives, and specialty compounds create cost pressures for waterproofing anti-corrosion tape manufacturers. Raw material expenses represent approximately 45%–55% of production costs, while dependence on specialized chemical suppliers affects pricing stability and delivery timelines. Manufacturers in countries such as Japan and South Korea face supply-chain constraints for advanced adhesive technologies due to limited supplier concentration. Companies are reducing exposure through localized sourcing strategies, multi-year supplier agreements, and investments in alternative material formulations to improve operational stability and protect margins.

Growing adoption of advanced materials and digital asset monitoring systems is creating new opportunities for waterproofing anti-corrosion tape manufacturers. Smart infrastructure projects are increasing demand for tapes compatible with sensor-based inspection systems, while more than 40% of new industrial maintenance programs emphasize extended asset lifecycle management. Countries including Saudi Arabia and India are expanding pipeline and industrial infrastructure investments, opening opportunities for specialized corrosion protection solutions. Companies are focusing on R&D, strategic collaborations, and customized product development to address high-temperature, underwater, and chemically aggressive environments.

Maintaining consistent performance across diverse operating environments remains a major challenge for waterproofing anti-corrosion tape deployment. Approximately 30% of application failures are associated with improper surface preparation, installation conditions, or environmental exposure. Offshore facilities, underground pipelines, and extreme-weather locations require specialized solutions with higher durability standards. Regulatory changes related to industrial safety and environmental compliance are increasing testing requirements for manufacturers. Companies must invest in installer training, quality-control systems, and advanced product validation technologies to ensure reliable performance and maintain competitiveness in demanding infrastructure markets.

Advanced Polymer Formulations Manufacturers are shifting toward polyethylene, butyl rubber, and composite adhesive technologies, with advanced tapes improving moisture resistance by 20%–30% and extending protection cycles by over 15%. Industrial operators are replacing conventional coatings in harsh environments where faster application and lower downtime are priorities. Companies are expanding R&D programs and forming material partnerships to develop lightweight, high-durability solutions.

Automated Installation Processes Pipeline operators are increasing adoption of semi-automated wrapping equipment, reducing installation labor requirements by nearly 25% and improving application consistency by 15%–20%. The labor shortage in maintenance-intensive industries is accelerating workflow automation, particularly in China and North America. Manufacturers are responding through equipment integration, installer training programs, and bundled product-service offerings.

Sustainable Material Transition Environmental compliance initiatives are encouraging manufacturers to introduce recyclable backings and lower-emission adhesive systems. Nearly 30% of industrial buyers now prioritize sustainable corrosion protection materials during procurement evaluations. Companies are restructuring supply chains, investing in eco-friendly formulations, and developing products aligned with evolving industrial sustainability requirements.

Digital Asset Monitoring Integration Infrastructure owners are combining corrosion tapes with digital inspection technologies, enabling predictive maintenance programs that improve asset monitoring efficiency by approximately 20%. Energy companies are adopting sensor-enabled maintenance strategies to reduce unexpected failures. Tape manufacturers are collaborating with technology providers to create integrated protection systems for pipelines and industrial facilities.

Polyethylene-based anti-corrosion tapes represent the leading type due to high durability, chemical resistance, and suitability across underground pipelines and industrial assets. This segment accounts for nearly 40% of overall adoption as operators prefer lightweight solutions with easier installation compared with traditional protective materials. Petrolatum tapes maintain strong demand in maintenance applications because of their flexibility and compatibility with irregular surfaces, while PVC-based tapes continue serving cost-sensitive industrial users. Composite and advanced adhesive tapes are emerging as the fastest-growing type, supported by demand for higher temperature resistance and longer service intervals. Adoption of next-generation materials is increasing by approximately 15% annually among infrastructure operators seeking reduced maintenance frequency. Companies are prioritizing product innovation, customized formulations, and expanded manufacturing capacity to capture demand from energy, utility, and industrial sectors.

Oil and gas pipeline protection is the leading application segment, driven by extensive transmission networks, underground infrastructure maintenance, and corrosion prevention requirements. This application contributes nearly 45% of demand as operators prioritize solutions that reduce leakage risks and extend asset life. Water pipelines and utility infrastructure represent stable adoption areas, while chemical and industrial pipeline applications are gaining importance due to exposure to aggressive environments. Marine and offshore applications are emerging as the fastest-growing segment, supported by increasing investment in coastal infrastructure and offshore energy assets. Adoption in these environments is rising by approximately 20% as operators require waterproof solutions capable of handling humidity, salt exposure, and temperature fluctuations. Companies are expanding specialized product portfolios and developing application-specific tapes for complex operating conditions.

Oil and gas companies represent the dominant end-user group due to extensive pipeline networks, high corrosion exposure, and continuous maintenance requirements. This segment accounts for nearly 50% of industrial demand as operators invest in protective technologies to improve asset lifespan and operational safety. Utility providers and water infrastructure companies are also increasing adoption as aging networks require cost-efficient rehabilitation solutions. Construction and marine industries are emerging as faster-growing users, with demand increasing by approximately 18% as infrastructure modernization and offshore projects expand. These buyers increasingly prefer flexible, easy-to-install solutions that reduce project timelines and workforce requirements. Companies are targeting these segments through customized product specifications, distributor partnerships, and application support services.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America accounted for approximately 28% of the global Waterproofing Anti-Corrosion Tape Market in 2025, supported by extensive oil & gas pipeline networks, utility modernization, and industrial maintenance programs. The United States represents the primary demand center due to aging infrastructure requiring protective upgrades and corrosion management solutions. More than 30% of regional demand originates from pipeline and energy applications, while manufacturers are expanding distribution networks and developing advanced adhesive technologies for harsh operating conditions. Increasing adoption of preventive maintenance practices is encouraging operators to replace traditional repair methods with durable tape-based protection systems.

United States Market Outlook: The United States leads North American adoption due to its large pipeline infrastructure and industrial asset base. Over 70% of new corrosion management programs focus on extending existing infrastructure life rather than full replacement. Domestic manufacturers and suppliers are investing in high-performance polymer tapes and customized solutions for energy, water, and transportation infrastructure.

Europe captured nearly 20% of the global market in 2025, driven by strict industrial safety requirements, aging utility infrastructure, and sustainability-focused maintenance strategies. Countries such as Germany, the United Kingdom, and France are increasing adoption of advanced corrosion protection solutions for energy networks and industrial facilities. Nearly 25% of regional demand is linked to infrastructure refurbishment projects, where durable materials help reduce replacement frequency and maintenance interruptions. European manufacturers are emphasizing low-emission materials, recyclable components, and improved adhesive performance to align with environmental standards and industrial efficiency goals.

Germany Market Outlook: Germany remains the leading European market due to its advanced manufacturing ecosystem and strong industrial infrastructure. The country’s chemical, automotive, and energy sectors account for significant consumption of corrosion protection materials. More than 40% of industrial operators prioritize long-life protection systems to improve asset reliability and reduce maintenance costs.

Asia-Pacific dominated the global market with approximately 38% share in 2025, supported by large-scale pipeline construction, industrial expansion, and manufacturing capabilities. China, India, Japan, and South Korea are major contributors due to growing energy infrastructure and utility development. China’s extensive pipeline network and manufacturing capacity strengthen regional supply leadership, while India’s infrastructure expansion is increasing demand for protective materials. Over 45% of regional applications are concentrated in energy, water, and industrial sectors. Companies are increasing production capacity, improving polymer formulations, and expanding local partnerships to meet rising infrastructure protection requirements.

China Market Outlook: China holds the strongest position in Asia-Pacific due to its manufacturing advantage and extensive industrial infrastructure. The country operates more than 100,000 km of oil and gas pipelines, creating sustained demand for corrosion prevention technologies. Domestic producers are scaling advanced tape manufacturing to support energy security and infrastructure modernization programs.

South America represented around 7% of the global market in 2025, with demand concentrated in Brazil, Argentina, and Chile. Oil pipelines, mining operations, and water infrastructure projects are key application areas driving adoption. Brazil contributes the largest share due to its energy industry scale and offshore development activities. Approximately 20% of regional demand comes from pipeline maintenance applications, while infrastructure limitations and import dependency influence deployment timelines. Companies are strengthening local distributor networks, improving inventory availability, and introducing application-specific solutions for mining and energy environments.

Brazil Market Outlook: Brazil is the leading South American market due to its extensive energy infrastructure and industrial activity. Offshore oil operations and pipeline networks create strong demand for waterproof corrosion protection solutions. More than 30% of regional industrial infrastructure investment is associated with energy and resource-related projects, supporting continued adoption.

Middle East & Africa accounted for approximately 7% of the global market in 2025 and is emerging as a high-potential market due to oil infrastructure expansion, industrial modernization, and pipeline protection requirements. Saudi Arabia, the United Arab Emirates, and South Africa are key demand centers. More than 35% of regional applications are linked to oil & gas assets where corrosion resistance is critical for operational continuity. Companies are increasing partnerships with energy operators, expanding regional service capabilities, and introducing high-temperature resistant products for desert and offshore environments.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically important market in the region due to its extensive oil infrastructure and industrial diversification initiatives. The country’s large pipeline network and energy modernization projects are increasing demand for advanced corrosion protection materials. Over 50% of industrial maintenance investments prioritize improving asset reliability and extending infrastructure lifespan.

The Waterproofing Anti-Corrosion Tape Market features global material leaders competing with specialized industrial tape manufacturers and regional suppliers. Key players include 3M, Nitto Denko Corporation, Shurtape Technologies, Scapa Group, and specialized corrosion-control suppliers. The top five players collectively account for approximately 45% of market activity, with competition centered on adhesive technology, product durability, customization, and supply reliability. Premium manufacturers compete through advanced polymer formulations, while regional suppliers focus on cost efficiency and faster delivery, influencing nearly 30% of procurement decisions. Companies are expanding production, forming infrastructure partnerships, and integrating application services. The competitive shift is moving toward high-performance materials and localized supply chains. Winning requires superior material innovation, dependable availability, and application expertise.

Nitto Denko Corporation

Shurtape Technologies

Scapa Group

Polyken

Saint-Gobain

Tesa SE

Berry Global

Lintec Corporation

Advance Tapes International

Lohmann GmbH & Co. KG

Waterproofing anti-corrosion tape technology is shifting from conventional single-layer protection toward advanced polymer composites, butyl rubber systems, and high-performance adhesive structures. Modern formulations improve moisture resistance by 20%–30% compared with traditional materials and enable longer service intervals. Adoption is increasing among pipeline operators and industrial maintenance teams seeking faster installation and reduced downtime.

Digital integration is becoming an emerging technology trend as corrosion tapes are combined with inspection sensors and predictive maintenance platforms. These systems improve asset monitoring efficiency by approximately 20% and help operators prioritize maintenance activities. Companies benefiting most are infrastructure owners and technology-enabled suppliers developing integrated protection solutions rather than standalone materials.

Between 2026 and 2028, automated application systems and sustainable material development will influence competitive positioning. Compared with manual legacy wrapping processes, automated systems reduce installation labor requirements by nearly 25%. Manufacturers are investing in recyclable backing materials, smart inspection compatibility, and customized industrial solutions to improve operational performance and strengthen market differentiation.

March 2025 Nitto Denko Corporation expanded focus on advanced industrial adhesive technologies, including anti-corrosion tape solutions such as NITOHULLMAC XG Series designed for outdoor corrosion protection. The technology emphasizes weather resistance and simplified installation for industrial assets. Source: www.nitto.com

January 2025 Shurtape Technologies strengthened industrial tape offerings for steel pipe coating applications with high-performance solutions designed for demanding temperature and adhesion requirements. The company highlights products supporting industrial workflows and corrosion protection processes. Source: www.shurtape.com

October 2025 Nitoms introduced a new anti-mold waterproof tape product line for moisture-prone environments, reflecting expansion of adhesive technologies into protective surface applications. The product uses integrated anti-fungal materials in both backing and adhesive layers. Source: www.prtimes.jp

July 2025 Nitto Denko Corporation continued industrial tape technology development through research and business initiatives across advanced adhesive applications. The company maintained investment focus on high-performance tape technologies supporting industrial reliability and specialized applications.

The Waterproofing Anti-Corrosion Tape Market Report covers comprehensive analysis across product types including polyethylene, petrolatum, PVC, and advanced composite tapes. The study evaluates applications across pipelines, industrial facilities, marine structures, utilities, and infrastructure projects, along with end-users such as oil & gas operators, construction companies, utilities, and industrial manufacturers. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report provides strategic insights into material innovation, adhesive technology advancements, supply-chain developments, and competitive positioning. It evaluates adoption patterns, deployment trends, company strategies, and emerging opportunities supporting investment planning and expansion decisions. The analysis helps stakeholders understand technology shifts, regional demand concentration, and future positioning requirements from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 68.7 Million |

| Market Revenue (2033) | USD 98.4 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | 3M; Nitto Denko Corporation; Shurtape Technologies; Scapa Group; Polyken; Saint-Gobain; Tesa SE; Berry Global; Lintec Corporation; Advance Tapes International; Lohmann GmbH & Co. KG |

| Customization & Pricing | Available on Request (10% Customization Free) |