Reports

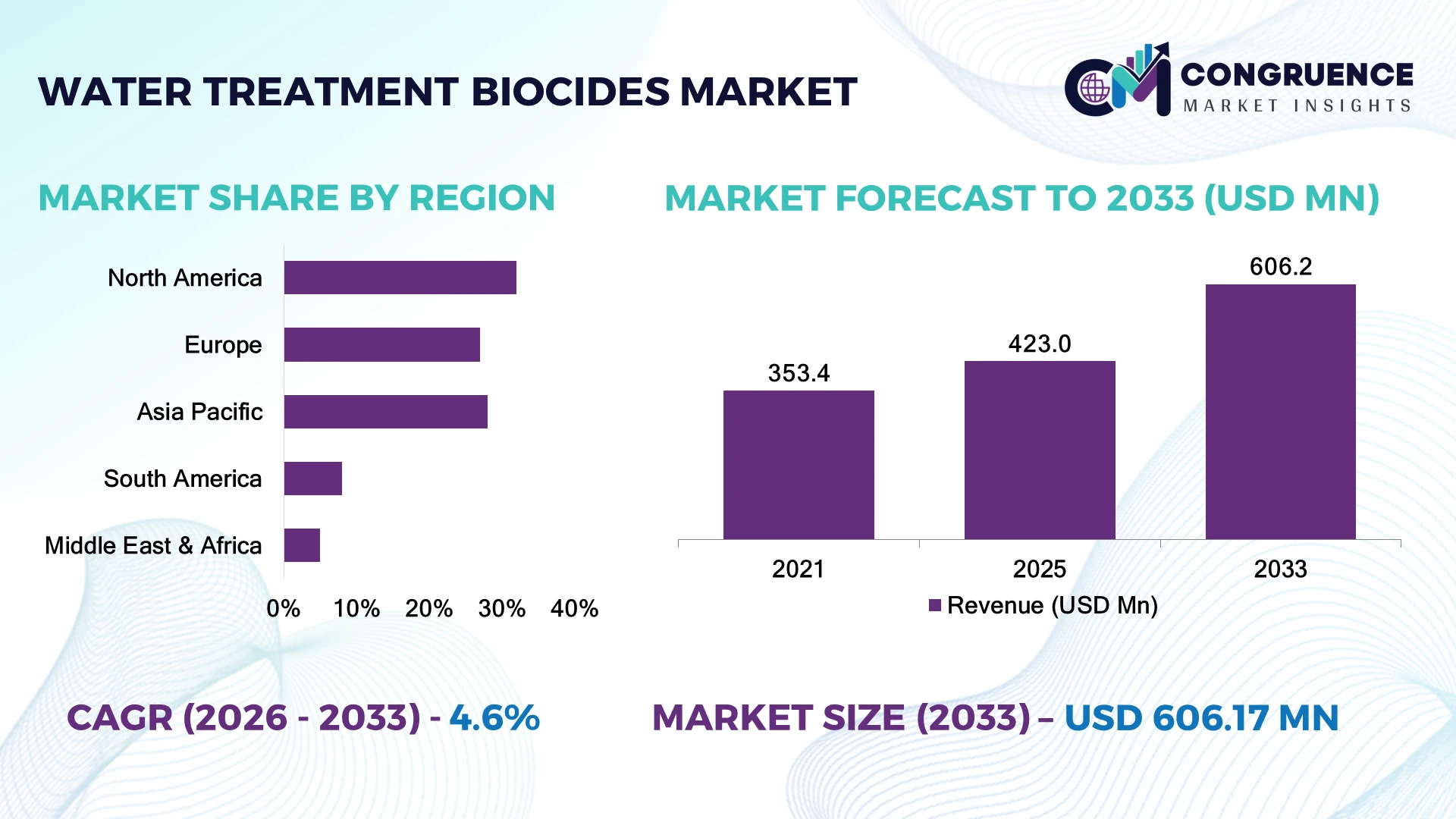

The Global Water Treatment Biocides Market was valued at USD 423.0 Million in 2025 and is anticipated to reach a value of USD 606.2 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Growth is driven by stricter microbial control regulations, rising adoption of advanced membrane treatment systems, and increasing use of low-toxicity biocide formulations in industrial water recycling.

The United States dominates the market with nearly 32% share, supported by large-scale investments in municipal water upgrades, oil & gas operations, and industrial wastewater management. The country operates over 16,000 wastewater treatment facilities, while China has expanded industrial water reuse capacity by more than 20% through infrastructure modernization initiatives. Compared with Europe’s stricter chemical compliance framework, North America focuses on high-performance treatment solutions for energy and manufacturing sectors.

Strategic decisions increasingly prioritize sustainable biocide technologies, regulatory compliance, and long-term operational reliability.

Market Size & Growth: USD 423.0 Million in 2025 to USD 606.2 Million by 2033 at 4.6% CAGR, driven by advanced wastewater recycling and microbial control technologies.

Top Growth Drivers: Industrial wastewater treatment (35%), water reuse adoption (28%), and regulatory compliance upgrades (22%) are major expansion factors.

Short-Term Forecast: By 2028, automated dosing systems improve chemical efficiency by 15% and reduce treatment wastage by 10%.

Emerging Technologies: AI-based monitoring, smart dosing automation, and biodegradable biocide formulations are reshaping advanced treatment operations.

Regional Leaders: North America reaches USD 190 Million with digital monitoring adoption; Asia Pacific approaches USD 210 Million through industrial expansion; Europe reaches USD 130 Million with sustainable chemistry adoption.

Consumer/End-User Trends: More than 45% of industrial operators are integrating optimized chemical management systems to reduce water treatment costs.

Pilot/Case Example: 2024 industrial wastewater projects using automated biocide control achieved around 18% reduction in chemical consumption.

Competitive Landscape: Leading suppliers including Ecolab, BASF, Solenis, Veolia, and DuPont compete through formulation innovation and service expansion, with leading players accounting for approximately 40% market presence.

Regulatory & ESG Impact: Sustainability regulations are accelerating adoption of low-impact formulations, with environmentally compliant products representing over 30% of new industrial applications.

Investment & Funding: More than USD 2 billion is being directed globally toward water infrastructure modernization, digital treatment platforms, and industrial water partnerships.

Innovation & Future Outlook:

Next-generation biocides, predictive analytics, and circular water management strategies are driving the shift toward smarter treatment ecosystems.Water Treatment Biocides are becoming increasingly important across cooling towers, municipal systems, oil & gas operations, and manufacturing facilities due to rising microbial contamination risks and stricter water quality standards. Advanced formulations such as non-oxidizing biocides and combination treatment programs are improving performance, with nearly 40% of industrial users prioritizing solutions that enhance operational efficiency. Growing emphasis on water reuse and compliance with evolving environmental standards, including industrial regulations in regions such as the European Union, is creating new opportunities for technology-driven treatment providers.

The Water Treatment Biocides Market is becoming strategically important as industries worldwide prioritize reliable water management, resource efficiency, and compliance-driven treatment solutions. Growing pressure from water scarcity, industrial discharge regulations, and infrastructure modernization is reshaping procurement strategies across manufacturing, energy, and municipal sectors. Supply-chain diversification is also accelerating as companies expand regional chemical production capabilities to reduce dependency risks.

Technology transformation is creating measurable operational advantages. Traditional manual chemical dosing systems are increasingly replaced by automated monitoring platforms that improve dosing accuracy by nearly 20% and reduce unnecessary chemical usage compared with legacy practices. North America maintains leadership through mature industrial water networks, while Asia Pacific is advancing rapidly through large-scale manufacturing investments and wastewater infrastructure development.

Industrial facilities are deploying integrated treatment systems combining sensors, analytics, and advanced biocide formulations to maintain water quality while lowering operational disruptions. Companies are increasing investments in partnerships, local production facilities, and sustainable chemistry development to meet evolving customer requirements. Over the next few years, competitive advantage will depend on combining treatment efficiency, regulatory readiness, and digital capabilities, positioning advanced water treatment providers for stronger long-term market relevance.

Rising industrial water reuse initiatives are strengthening demand for advanced biocide solutions, particularly in manufacturing, power generation, and oil processing facilities. The United States has increased investment in water infrastructure modernization, with industrial facilities targeting 20–30% reductions in freshwater dependency through recycling programs. Growing adoption of automated dosing technologies, used by over 35% of large treatment operators, is improving microbial control accuracy and reducing chemical waste. Companies are responding by expanding specialty formulation portfolios, forming technology partnerships, and investing in smart monitoring platforms. The key strategic shift is the move from conventional chemical supply toward integrated water management solutions.

Regulatory restrictions on certain active ingredients and fluctuating raw material availability are limiting operational flexibility for biocide manufacturers. In Europe, tighter chemical compliance frameworks have increased formulation evaluation requirements, raising development costs by approximately 15–20% for new products. Global supply disruptions affecting specialty chemical inputs have contributed to procurement volatility, with some industrial users reporting 10–15% increases in treatment chemical management costs. Companies are reducing exposure through localized production, multi-source procurement agreements, and alternative formulation development. A major operational challenge is maintaining treatment performance while adapting quickly to changing environmental standards and chemical approval processes.

Digital water management and environmentally optimized biocides are creating new opportunities for market expansion. Adoption of sensor-based water monitoring systems is increasing, with more than 40% of large industrial facilities exploring automated treatment controls to improve efficiency. Bio-based and low-toxicity formulations are gaining traction as sustainability requirements influence procurement decisions, particularly in Germany, Japan, and the United States. Companies are investing in R&D partnerships focused on biodegradable chemistry, predictive analytics, and integrated treatment platforms. A significant opportunity lies in emerging industrial hubs where wastewater recycling infrastructure is still developing, allowing technology providers to establish long-term service-based models.

Deployment complexity across diverse industrial environments remains a major challenge for water treatment biocide providers. Large facilities often operate multiple water systems requiring customized chemical programs, creating integration difficulties and increasing operational dependency on skilled technicians. Approximately 25–30% of industrial water operators continue to face limitations in real-time monitoring capabilities, affecting treatment consistency and resource optimization. Cybersecurity concerns are also emerging as connected water management platforms expand across critical infrastructure sites. Companies must address these barriers through advanced analytics, workforce training, cybersecurity investments, and stronger collaboration with industrial operators to ensure reliable long-term deployment and sustainable treatment performance.

Smart Dosing Integration Growth Industrial facilities are rapidly adopting automated dosing and monitoring platforms, with nearly 40% of large water treatment operators integrating digital controls to improve chemical accuracy and reduce over-treatment by 10–15%. Manufacturing hubs in the United States and Germany are deploying sensor-driven systems to optimize cooling water and wastewater processes. Companies are responding through automation partnerships, cloud-based monitoring solutions, and integrated service models that improve operational visibility and reduce maintenance interruptions.

Sustainable Chemistry Transition Low-toxicity and environmentally compliant biocide formulations are gaining momentum as regulatory pressure increases, with sustainable product adoption rising by approximately 25% among industrial buyers. European chemical compliance reforms and stricter discharge standards are accelerating formulation redesign. Companies are restructuring product portfolios toward biodegradable technologies, investing in R&D collaborations, and expanding alternatives that balance microbial control with environmental performance.

Localized Supply Networks Expansion Water treatment chemical suppliers are strengthening regional manufacturing networks as specialty chemical supply volatility impacts procurement strategies. Approximately 30% of major suppliers are increasing local production capabilities or establishing strategic partnerships to secure critical inputs. Companies in China, India, and the United States are prioritizing shorter supply chains, inventory optimization, and contract-based sourcing models to improve delivery reliability and reduce operational risks.

Predictive Water Management Adoption Predictive analytics is transforming industrial treatment workflows, with around 35% of advanced facilities evaluating AI-supported water quality forecasting tools. These platforms enable early microbial detection, improve response speed, and reduce unexpected system downtime. Companies are combining analytics with chemical expertise to create performance-based treatment services, reflecting a shift from product sales toward long-term operational solutions.

Non-oxidizing biocides represent the leading type segment, accounting for approximately 45% of market adoption, driven by their effectiveness in controlling microorganisms while minimizing corrosion risks in sensitive industrial systems. Their strong performance in cooling towers, oil & gas operations, and manufacturing applications supports wider integration. Oxidizing biocides maintain a significant position with nearly 35% share due to cost advantages and rapid microbial control capabilities, particularly in large-scale municipal and industrial facilities. Other specialty biocide categories contribute around 20% through targeted applications requiring customized treatment chemistry. The fastest-growing shift is toward advanced and environmentally optimized formulations, with adoption increasing by nearly 20% among industries seeking improved sustainability compliance. Companies are investing in hybrid treatment programs, formulation upgrades, and strategic partnerships to improve efficiency. The competitive focus is moving from basic chemical supply toward performance-driven solutions combining effectiveness, safety, and regulatory alignment.

Cooling water treatment remains the leading application segment with approximately 50% market share, supported by extensive use across power generation, manufacturing plants, and commercial infrastructure. High microbial control requirements in cooling towers make biocide application operationally critical, especially in energy-intensive industries. Wastewater treatment applications account for nearly 30% share and are expanding as industries increase recycling and discharge compliance efforts. Other applications, including process water treatment, represent around 20% of demand through specialized industrial requirements. Wastewater treatment is emerging as the fastest-growing application area, with adoption increasing by approximately 25% as companies invest in circular water management systems. Industrial operators in China, India, and the United States are expanding treatment capacity through automation and advanced monitoring integration. Companies are responding with customized treatment packages, digital service platforms, and application-specific formulations to address evolving operational needs.

Industrial facilities represent the dominant end-user segment, accounting for approximately 55% of demand due to intensive water consumption across manufacturing, energy, chemicals, and processing industries. These users require continuous microbial control to protect equipment reliability and maintain production efficiency. Municipal water operators contribute nearly 25% share, supported by infrastructure modernization programs and stricter water quality requirements. Commercial and other specialized users account for the remaining 20%, focusing on localized treatment needs. The fastest-growing end-user group is industrial manufacturing, where adoption is rising by nearly 22% as companies integrate water reuse strategies and automated treatment systems. Facilities in Japan, Germany, and the United States are increasing investments in customized chemical management solutions and long-term service partnerships. Suppliers are responding through sector-specific formulations, technical support programs, and integrated monitoring ecosystems.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America holds the leading position in the Water Treatment Biocides Market, supported by extensive industrial water infrastructure, strict environmental compliance requirements, and high adoption of automated treatment systems. The region contributes approximately 32% of global demand, with the United States representing the largest share due to strong utilization across power generation, oil & gas, chemical processing, and municipal facilities. More than 16,000 wastewater treatment facilities operate across the United States, creating consistent demand for microbial control solutions. Companies are increasing investments in smart dosing platforms, sustainable formulations, and integrated treatment services to improve efficiency and regulatory compliance.

United States Market Outlook: The United States remains the key country due to its large industrial base, advanced water infrastructure, and technology adoption capabilities. Over 40% of major industrial operators are integrating digital monitoring systems to optimize chemical usage. Strong demand from cooling water applications, manufacturing facilities, and energy operations continues to support supplier expansion and innovation strategies.

Europe maintains a strong position in the market through stringent chemical regulations, sustainability-focused water policies, and advanced industrial treatment practices. Countries including Germany, France, and the United Kingdom are accelerating adoption of environmentally optimized biocide formulations due to stricter discharge standards and industrial efficiency goals. The region contributes nearly 27% of global demand, with manufacturing and municipal applications accounting for a significant share of deployment. More than 35% of European industrial buyers are prioritizing low-impact chemical solutions to align with environmental compliance objectives. Companies are responding through green chemistry development, localized production, and partnerships focused on sustainable water management technologies.

Germany Market Outlook: Germany leads European adoption due to its advanced manufacturing ecosystem, chemical industry strength, and focus on industrial water efficiency. The country has over 2,000 large industrial wastewater treatment facilities supporting demand for specialized microbial control solutions. German companies are investing in automation, sustainable formulations, and resource-efficient treatment systems to maintain industrial competitiveness.

Asia-Pacific represents the fastest-transforming market, driven by manufacturing growth, infrastructure expansion, and increasing industrial wastewater treatment requirements. The region contributes around 28% of global demand, with China, India, Japan, and South Korea accounting for major consumption volumes. China’s large chemical, electronics, and manufacturing sectors are increasing adoption of advanced treatment systems, while India is expanding industrial water recycling capabilities. Industrial water reuse initiatives have increased by more than 20% in several manufacturing clusters. Companies are strengthening local production capacity, forming regional partnerships, and introducing cost-efficient formulations to serve diverse industrial requirements.

China Market Outlook: China remains the largest Asia-Pacific contributor due to its extensive manufacturing base and infrastructure modernization programs. The country operates thousands of industrial treatment facilities supporting demand from electronics, chemicals, textiles, and power industries. Growing emphasis on wastewater compliance and industrial recycling is encouraging companies to expand advanced treatment chemical production and technology partnerships.

South America is developing as an important market supported by mining operations, industrial processing facilities, and increasing focus on water quality management. Brazil, Chile, and Argentina represent major demand centers, particularly across mining, pulp & paper, and energy sectors. The region contributes approximately 8% of global demand, with mining operations accounting for a significant portion of specialized treatment requirements. Investment in industrial water infrastructure is increasing, with several operators adopting improved chemical dosing systems to enhance process reliability. Companies are expanding distribution networks and developing customized treatment programs to address diverse operational conditions.

Brazil Market Outlook: Brazil leads regional demand due to its large industrial base, mining activity, and expanding wastewater infrastructure. The country has more than 200 million people, creating significant municipal and industrial water management requirements. Companies are focusing on localized supply chains, technical service expansion, and application-specific biocide solutions for industrial operators.

The Middle East & Africa market is gaining momentum through desalination projects, industrial diversification, and water security investments. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are increasing deployment of advanced water treatment technologies across municipal and industrial facilities. The region accounts for nearly 5% of global demand, with desalination plants, oil & gas operations, and power facilities representing major application areas. More than 60% of Gulf Cooperation Council countries rely heavily on desalination infrastructure, creating strong demand for microbial control solutions. Companies are expanding partnerships, establishing regional service capabilities, and investing in treatment technologies designed for harsh operating environments.

Saudi Arabia Market Outlook: Saudi Arabia represents the region’s most strategically significant market due to large-scale desalination capacity and industrial expansion programs. The country operates some of the world’s largest desalination facilities, requiring continuous water treatment management. Investments under national infrastructure initiatives are supporting adoption of advanced biocide solutions, digital monitoring systems, and sustainable water technologies.

The Water Treatment Biocides Market features competition between global chemical leaders such as Ecolab, BASF, Solenis, and DuPont against regional suppliers specializing in cost efficiency and localized distribution. The top five players collectively account for approximately 40% of market presence, creating a moderately consolidated structure. Competition is shaped by formulation performance, supply reliability, customization, and regulatory compliance, with advanced solutions gaining preference among industrial users. Around 35% of large facilities prioritize digital dosing integration, while nearly 30% seek sustainable chemical alternatives. Leading companies compete through acquisitions, regional manufacturing expansion, technology partnerships, and integrated service platforms. The market is shifting toward environmentally compliant formulations and smart treatment ecosystems, increasing pressure on traditional chemical suppliers. High entry barriers include regulatory approvals, technical expertise, and established customer relationships. Winning requires combining innovation, supply resilience, and application-specific treatment capabilities.

BASF

Solenis

DuPont

Veolia

LANXESS

Clariant

Kemira

Kurita Water Industries

Arxada

Italmatch Chemicals

BWA Water Additives

Smart monitoring and automated dosing technologies are transforming industrial water treatment operations. IoT-enabled sensors and analytics platforms allow real-time microbial tracking, improving chemical-use efficiency by approximately 15% compared with manual systems. Adoption among large industrial facilities has reached nearly 40%, enabling predictive maintenance, reduced downtime, and better regulatory compliance.

Advanced formulation technologies are also reshaping product development. Low-toxicity and biodegradable biocides provide improved environmental performance while maintaining microbial control efficiency. Compared with conventional formulations, newer solutions deliver nearly 20% improvement in treatment optimization through targeted application. Chemical manufacturers benefit by developing customized solutions aligned with sustainability requirements and industrial compliance standards.

Artificial intelligence-based water management platforms represent the next disruptive phase between 2026 and 2028. AI-driven prediction models are expected to improve operational response speed by around 25% through early contamination detection. Global leaders with strong digital capabilities and chemical expertise are positioned to gain competitive advantages, while traditional suppliers face pressure to integrate technology-driven services into their offerings.

March 2025LANXESS presented advanced water treatment solutions at Aquatech 2025, including Aqucar DB 20, Kathon WTE, and Aqucar GA 50 non-oxidizing biocides for controlling biofouling in reverse osmosis and nanofiltration membrane systems. The solutions support improved membrane reliability and industrial water security. Source: www.lanxess.com

March 2025Solenis recognized Kenya Breweries Limited for a water recovery project using Solenis’ Biocidal Acid OSA-N technology within a Clean-In-Place system. The project improved operational efficiency by combining cleaning and disinfection steps while reducing chemical handling requirements in brewery operations. Source: www.solenis.com

May 2026BASF strengthened its North American water treatment portfolio by introducing NSF/ANSI/CAN 60-certified sodium metabisulfite and sodium sulfite grades for municipal, industrial, and formulated water treatment applications. The expansion improves regulatory compliance, product reliability, and supply availability for water treatment customers. Source: www.basf.com

November 2025Solenis completed the acquisition of NCH Corporation to expand its global water and hygiene solutions capabilities. The transaction increased Solenis’ operating footprint to more than 160 countries and strengthened its industrial water treatment service network.

The Water Treatment Biocides Market Report provides comprehensive coverage of product types, applications, end-user industries, regional performance, technology trends, and competitive strategies. The analysis evaluates major segments including oxidizing and non-oxidizing biocides, cooling water systems, wastewater treatment, industrial facilities, and municipal applications across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report examines emerging technologies such as automated dosing, digital monitoring, sustainable formulations, and predictive treatment systems. With analysis of more than 10 key industry participants and multiple application environments, the study supports investment planning, expansion strategies, supplier evaluation, and competitive positioning. It highlights evolving demand patterns and strategic opportunities shaping market direction from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 423.0 Million |

| Market Revenue (2033) | USD 606.2 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Ecolab; BASF SE; Solenis; DuPont; Veolia; LANXESS AG; Clariant AG; Kemira Oyj; Kurita Water Industries Ltd.; Arxada; Italmatch Chemicals S.p.A.; BWA Water Additives |

| Customization & Pricing | Available on Request (10% Customization Free) |