Reports

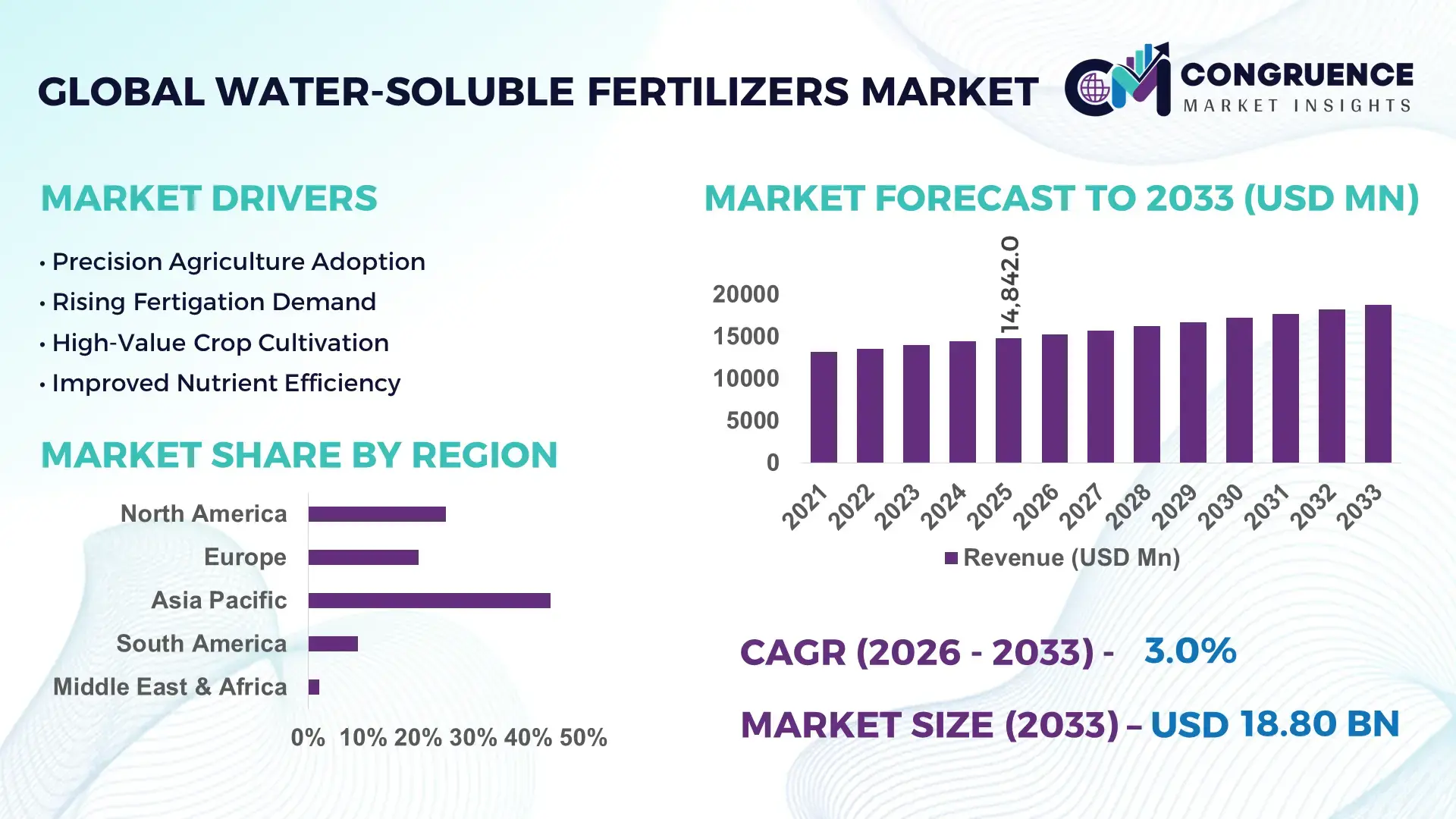

The Global Water-Soluble Fertilizers Market was valued at USD 14841.99 Million in 2025 and is anticipated to reach a value of USD 18801.39 Million by 2033 expanding at a CAGR of 3% between 2026 and 2033.

Precision agriculture adoption and fertigation systems are accelerating nutrient-use efficiency by over 20%, directly reducing input waste and improving yield consistency across high-value crops. Between 2024 and 2026, tightening environmental regulations on nitrogen runoff and increased pressure on water efficiency have reshaped fertilizer formulations toward low-salt index and high-purity soluble grades.

China remains the dominant country, accounting for approximately 32% of global production capacity, supported by large-scale manufacturing clusters and export-driven supply chains. Over USD 1.5 billion has been directed toward upgrading controlled-release and specialty soluble fertilizer facilities, while adoption of drip irrigation exceeds 45% in intensive horticulture zones, reinforcing demand for water-soluble inputs. In comparison, India contributes nearly 14% of demand, driven by expanding greenhouse cultivation and government-backed micro-irrigation programs covering over 12 million hectares. This creates a clear regional production-consumption imbalance, with Asia-Pacific outperforming Europe in volume by nearly 1.8x.

The market’s structural shift toward high-efficiency nutrient delivery systems positions manufacturers to prioritize formulation innovation and localized production strategies to mitigate logistics volatility and regulatory risk.

Market Size & Growth: USD 14.8B (2025) to USD 18.8B (2033) at 3% CAGR, driven by precision fertigation adoption improving nutrient efficiency by 20%.

Top Growth Drivers: Drip irrigation expansion (↑18%), greenhouse farming growth (↑22%), specialty crop demand (↑15%).

Short-Term Forecast: By 2027, input cost efficiency improves by 12% through optimized nutrient dosing systems.

Emerging Technologies: AI-based nutrient monitoring, automated fertigation, and advanced chelated micronutrients increase uptake efficiency by 25%.

Regional Leaders: Asia-Pacific (~USD 7B) leads via intensive farming; Europe (~USD 4.2B) driven by sustainability mandates; North America (~USD 3.8B) adopts precision ag at 40% farm penetration.

Consumer/End-User Trends: Over 55% of commercial growers prefer water-soluble fertilizers for high-value crops due to faster nutrient absorption.

Pilot/Case Example: 2025 fertigation project in Israel improved crop yield by 28% while reducing fertilizer usage by 15%.

Competitive Landscape: Top players hold ~38% share, with key companies focusing on specialty blends and controlled nutrient release.

Regulatory & ESG Impact: Nitrogen emission reduction policies cut fertilizer overuse by 10–12% across regulated regions.

Investment & Funding: Over USD 2.3B invested in advanced fertilizer production and supply chain localization since 2024.

Innovation & Future Outlook: Next-gen bio-enhanced soluble fertilizers and nano-nutrient delivery systems improve absorption rates by 30%, shaping high-efficiency agriculture.

High-value horticulture accounts for nearly 46% of total demand, followed by greenhouse cultivation at 28% and open-field specialty crops at 18%, reflecting a strong shift toward precision-driven agriculture. Recent innovations include nano-chelated micronutrients and sensor-integrated fertigation systems, improving nutrient uptake efficiency by up to 25%. Asia-Pacific leads demand with over 52% share, while Europe’s regulatory-driven adoption exceeds 35% in controlled farming systems. Supply chain localization trends and stricter environmental compliance are accelerating regional production strategies, positioning advanced formulations as a core competitive lever in the evolving market landscape.

Water-soluble fertilizers are rapidly becoming a critical lever for agricultural productivity, cost optimization, and resource efficiency, positioning the market at the center of global food security strategies and high-value crop economics. The shift toward precision agriculture is accelerating demand for targeted nutrient delivery systems that enhance yield while minimizing input waste, making this segment strategically essential for both agribusiness investors and input manufacturers. Regulatory pressure on nutrient runoff and water usage is transforming formulation standards and forcing producers to innovate toward cleaner, high-efficiency inputs.

Advanced fertigation systems improve nutrient-use efficiency by 25% while reducing application costs by 18% compared to traditional broadcasting methods, creating a measurable competitive advantage for early adopters. Asia-Pacific leads in production volume, while Europe leads in adoption and innovation with over 38% of farms integrating precision nutrient systems. Over the next 2–3 years, fertilizer application efficiency is expected to increase by 15%, driven by sensor-based irrigation and AI-integrated crop monitoring. ESG alignment is emerging as a direct competitive differentiator, with compliant producers reducing regulatory penalties and achieving up to 10% cost savings through optimized nutrient cycles. A 2025 greenhouse project in Spain demonstrated a 30% yield increase with 20% lower fertilizer consumption using fully automated fertigation. Major companies are shifting capital allocation toward specialty soluble blends and regional production hubs, signaling a clear move toward localized, high-efficiency supply chains. The competitive edge will belong to players that can integrate advanced formulations with precision delivery systems at scale, redefining operational efficiency and market leadership.

The accelerating adoption of precision agriculture is fundamentally reshaping demand for water-soluble fertilizers, driven by the need for higher nutrient efficiency and reduced environmental impact. Drip irrigation adoption has increased by over 18% globally, directly boosting demand for fully soluble fertilizers that integrate seamlessly with fertigation systems. This shift is further reinforced by a 22% rise in greenhouse farming, where controlled environments demand precise nutrient delivery for consistent yield output. A significant global trigger has been the tightening of nitrogen emission regulations across Europe and parts of Asia, forcing farmers to transition toward low-loss nutrient solutions. This cause-effect dynamic is pushing agribusinesses to expand production of high-purity soluble fertilizers and invest in R&D for advanced formulations. Companies are responding through capacity expansion in specialty fertilizers, forming partnerships with irrigation technology providers, and accelerating digital integration to offer bundled nutrient-delivery solutions that optimize both yield and cost efficiency.

Despite strong demand momentum, the market faces critical constraints due to raw material dependency and cost volatility. Key inputs such as potassium nitrate and phosphates have experienced price fluctuations exceeding 20%, directly impacting production costs and margin stability. Supply concentration in a few exporting countries creates additional vulnerability, with over 60% of certain raw materials sourced from limited regions, exposing manufacturers to geopolitical and trade disruptions. Infrastructure gaps in emerging markets further constrain large-scale adoption, particularly where fertigation systems penetration remains below 25%. These factors increase operational costs and delay project scalability for producers and distributors. In response, companies are actively diversifying sourcing strategies, entering long-term supply agreements, and investing in alternative nutrient technologies such as bio-based soluble fertilizers. Strategic stockpiling and regional production expansion are also being implemented to mitigate supply chain risks and stabilize pricing structures.

The next wave of growth is emerging from advanced nutrient technologies and expanding high-value agriculture in emerging markets. Nano-enhanced fertilizers are improving nutrient absorption efficiency by up to 30%, offering a clear performance advantage over conventional soluble products. Simultaneously, emerging economies in Asia and Latin America are witnessing a 20% increase in adoption of micro-irrigation systems, unlocking new demand pockets for water-soluble inputs. A key future signal is the integration of AI-driven crop analytics with fertigation systems, enabling real-time nutrient optimization and reducing waste by over 15%. Beyond traditional applications, vertical farming and hydroponics are creating non-obvious opportunities, where water-soluble fertilizers are essential for closed-loop nutrient systems. Companies are positioning aggressively by investing in R&D for next-generation formulations, expanding into underserved regional markets, and building integrated ecosystems that combine fertilizers, sensors, and digital advisory platforms to secure long-term competitive dominance.

Execution complexity and infrastructure limitations remain significant barriers to sustained growth and scalability. While demand is rising, nearly 35% of potential users lack access to efficient irrigation infrastructure, limiting the full benefits of water-soluble fertilizers. Additionally, inconsistent product performance due to water quality variations can reduce nutrient efficiency by up to 12%, affecting farmer confidence and repeat adoption. Regulatory compliance is also becoming more stringent, with environmental standards tightening across major agricultural economies, increasing compliance costs by approximately 8–10%. A real-world pressure point is the uneven adoption of precision agriculture technologies, particularly in developing regions where upfront investment costs remain a constraint. These challenges directly impact long-term market consistency and scalability. To remain competitive, companies must invest in farmer education, develop adaptable formulations for varied water conditions, and form strategic partnerships with irrigation and agri-tech providers to ensure integrated, scalable solutions that address both performance and accessibility gaps.

Precision fertigation adoption rises by 25%, reshaping nutrient delivery execution. Across commercial farming systems, over 48% of high-value crop producers are now integrating automated fertigation, compared to nearly 35% two years earlier. This shift is driven by real-time dosing systems that reduce nutrient losses by 18% and improve application accuracy by 22%. Companies are responding by bundling fertilizers with irrigation technologies and scaling partnerships with agri-tech providers, directly optimizing input efficiency while lowering labor dependency.

Micronutrient-enriched formulations expand by 30%, redefining product mix. Demand for chelated and fortified water-soluble fertilizers has increased sharply, with micronutrient blends now accounting for nearly 27% of specialty product lines. This transition is happening through reformulation strategies that address soil depletion and crop-specific deficiencies. The business impact is evident in yield improvements of up to 15% and reduced corrective treatments. Manufacturers are restructuring portfolios toward high-margin specialty blends, supported by targeted R&D and localized customization.

Regional production localization increases by 20%, forcing supply chain restructuring. In response to recent trade disruptions and input cost volatility, nearly 40% of producers are shifting toward regional manufacturing hubs. Asia-Pacific continues to dominate volume output, while Europe is accelerating localized production to meet regulatory compliance and reduce import dependency by 12%. This shift reduces lead times by 15% and stabilizes supply consistency. Companies are investing in decentralized facilities and forming joint ventures to secure raw material access and mitigate geopolitical risks.

Subscription-based supply models grow by 18%, transforming procurement dynamics. Agribusinesses are increasingly adopting contract-based fertilizer supply linked to crop cycles, with over 32% of large-scale growers shifting to recurring procurement models. This operational change ensures predictable demand flows and reduces procurement costs by 10%. A non-obvious shift is the integration of advisory services within these models, where companies combine product delivery with nutrient planning. This approach strengthens customer retention and enables producers to optimize inventory and demand forecasting simultaneously.

The water-soluble fertilizers market is segmented across types, applications, and end-users, reflecting a highly specialized and demand-driven structure. NPK blends and nitrogen-based fertilizers dominate product demand due to their versatility and compatibility with fertigation systems, collectively accounting for over 55% of total usage. Application-wise, fertigation leads with more than 42% share, supported by expanding micro-irrigation infrastructure, while hydroponics is emerging rapidly due to controlled environment agriculture growth. From an end-user perspective, the agriculture sector remains the largest consumer, contributing nearly 50% of demand, driven by large-scale crop production and efficiency needs. However, demand is steadily shifting toward greenhouse operators and horticulture growers, where precision nutrient delivery offers measurable yield improvements and cost control. This segmentation highlights a clear transition toward high-efficiency, crop-specific solutions, forcing companies to align product development, distribution strategies, and customer targeting with evolving usage patterns.

Nitrogen-based fertilizers dominate the market with approximately 34% share, driven by their critical role in plant growth and compatibility with most irrigation systems, making them highly scalable and cost-efficient. However, NPK blends are the fastest-growing segment, expanding at over 8% in adoption terms, as they offer balanced nutrient delivery and reduce the need for multiple applications. This creates a direct comparison where nitrogen-based products lead in volume, while NPK blends are capturing value through efficiency and integrated performance. Phosphatic and potassic fertilizers, along with micronutrient fertilizers, collectively account for nearly 38% of demand, serving niche but essential roles in crop-specific nutrition and soil correction. Companies are increasingly shifting focus toward customized NPK and micronutrient blends, investing in formulation innovation and expanding specialty product lines to capture high-margin segments. The business implication is clear: growth is moving from bulk nutrient supply toward precision-engineered formulations, requiring strategic investment in R&D and targeted production capabilities.

“According to a 2025 report by International Fertilizer Association, NPK blends were adopted by over 46% of intensive farming operations, resulting in a 20% improvement in nutrient-use efficiency, reinforcing its growing strategic importance.”

Fertigation leads the market with over 42% share, as it enables direct nutrient delivery through irrigation systems, significantly improving efficiency and reducing waste. Hydroponics is the fastest-growing application, expanding by more than 10% in adoption, driven by the rapid rise of controlled environment agriculture and urban farming systems. This creates a strong contrast where fertigation dominates large-scale operations, while hydroponics is redefining high-precision, space-efficient farming. Foliar application, greenhouse cultivation, and open-field farming together represent around 48% of usage, each serving specific operational needs based on crop type and environmental conditions. Companies are adapting by developing application-specific formulations and integrating digital advisory tools to optimize usage patterns. The shift toward precision applications is forcing manufacturers to align product design with delivery systems, creating opportunities for integrated solutions that combine fertilizers with technology platforms, ultimately enhancing performance and customer retention.

“According to a 2025 report by Food and Agriculture Organization, fertigation was deployed across over 18 million hectares globally, improving water-use efficiency by 25%, highlighting its rapid operational adoption.”

The agriculture sector dominates with nearly 50% share, driven by large-scale cultivation and consistent demand for yield optimization across staple and cash crops. However, greenhouse operators are the fastest-growing segment, with adoption increasing by over 12%, fueled by the expansion of controlled environment farming and demand for high-quality produce. This creates a clear contrast where traditional agriculture maintains volume dominance, while greenhouse operators drive innovation and premium product demand. Horticulture growers, turf and landscape managers, and agricultural cooperatives together account for approximately 40% of demand, with increasing adoption of precision nutrient solutions to enhance output quality and reduce input costs. Companies are targeting these segments through customized pricing models, crop-specific formulations, and strategic partnerships with cooperatives to expand distribution reach. The business implication highlights a shift toward value-driven demand, where specialized end-users are influencing product innovation and shaping future growth trajectories.

“According to a 2025 report by International Fertilizer Development Center, adoption among greenhouse operators increased by 12%, with over 250,000 facilities implementing precision fertigation systems, leading to a 28% productivity improvement, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

Asia-Pacific dominates due to high-volume agricultural output and cost-efficient production, contributing over 50% of global fertilizer consumption. Europe, with nearly 24% share, is accelerating adoption through sustainability mandates and precision farming penetration exceeding 38%. North America holds around 18%, leading in advanced fertigation integration and digital agriculture adoption above 40%. A key structural shift is the global push toward localized production to reduce import dependency by 12%, reshaping supply chains. Companies are prioritizing Asia-Pacific for scale, Europe for innovation compliance, and North America for technology-led optimization strategies.

How are precision agriculture and cost optimization reshaping fertilizer deployment?

North America accounts for approximately 18% of global demand, driven by large-scale commercial farming and high adoption of precision agriculture technologies. Over 42% of farms utilize advanced fertigation and nutrient monitoring systems, directly increasing fertilizer efficiency by 20%. Regulatory pressure around nutrient runoff is forcing adoption of high-efficiency formulations, while supply chain restructuring is reducing dependency on imports by nearly 10%. Companies are scaling localized blending facilities and investing in digital nutrient management platforms. Growers prioritize performance-driven solutions with measurable yield improvements, favoring customized blends over bulk products. This region is attracting investment due to its strong technology integration and consistent demand for efficiency-focused agricultural inputs.

What is driving the shift toward compliance-led nutrient optimization?

Europe holds nearly 24% of the market, led by countries such as Germany, France, and the Netherlands, where sustainability regulations are redefining fertilizer usage. Over 38% of farms have adopted precision nutrient systems to comply with strict nitrogen emission standards, reducing excess application by 12%. The market is structurally shaped by environmental policies that enforce low-impact farming practices, pushing demand for high-purity soluble fertilizers. Companies are investing in eco-friendly formulations and expanding regional production to meet compliance needs. Buyers exhibit a strong preference for certified, performance-verified products. This region compels innovation, making regulatory alignment a prerequisite for market participation and long-term competitiveness.

Why is large-scale adoption accelerating demand at unmatched speed?

Asia-Pacific leads with over 46% market share, supported by high agricultural output in China and India and strong manufacturing capacity. The region produces more than 55% of global supply, benefiting from cost-efficient production and expanding irrigation infrastructure. Drip irrigation adoption has crossed 35%, accelerating demand for water-soluble fertilizers in intensive farming systems. Companies are expanding localized production hubs and increasing export capacity by 15% to meet global demand. Buyers prioritize cost-effective, scalable solutions with rapid deployment capability. This region remains critical for volume expansion and supply chain dominance, making it a focal point for global market scaling strategies.

How are agricultural expansion and infrastructure gaps shaping adoption?

South America contributes around 7% of global demand, with Brazil and Argentina leading due to strong agribusiness sectors. Demand is driven by large-scale cultivation of cash crops, where fertilizer efficiency improvements of up to 18% are critical for profitability. However, infrastructure limitations and uneven irrigation access restrict adoption, with less than 28% of farms using advanced fertigation systems. Companies are responding by expanding distribution networks and introducing cost-optimized formulations. Farmers demonstrate high price sensitivity, favoring products that balance performance with affordability. This region presents a high-growth opportunity, but requires strategic investment to overcome infrastructure and accessibility constraints.

How is resource optimization transforming agricultural input strategies?

The Middle East & Africa region accounts for approximately 5% of global demand, driven by water scarcity and the need for efficient agricultural practices. Countries such as Israel and South Africa are leading adoption, with over 30% of irrigated farms using fertigation systems. Investment in modern irrigation infrastructure has increased by 20%, supporting demand for water-soluble fertilizers. Companies are forming partnerships to deploy advanced nutrient delivery solutions and improve agricultural productivity. Buyers prioritize water-efficient and high-performance inputs due to resource constraints. This region is emerging as a strategic market where innovation and infrastructure investment are unlocking long-term growth potential.

China – 32% share: Water-Soluble Fertilizers Market in China leads due to massive production capacity, export dominance, and extensive adoption in intensive agriculture.

India – 14% share: Water-Soluble Fertilizers Market in India is driven by expanding micro-irrigation coverage and strong demand from high-value crop cultivation.

The market is defined by competition between global specialty fertilizer leaders, regional cost-focused manufacturers, and agri-tech integrated solution providers. Key players such as Yara International, Nutrien Ltd., ICL Group, Haifa Group, and SQM collectively hold approximately 38% of market share, competing directly on formulation quality, distribution reach, and technology integration. Global leaders focus on advanced nutrient solutions and precision farming compatibility, while regional players compete aggressively on price, often offering 10–15% lower-cost alternatives.

Competition is increasingly shifting toward integrated solutions, where companies combine fertilizers with digital advisory and fertigation systems, improving efficiency by over 20%. Strategic moves include capacity expansion, joint ventures for localized production, and vertical integration to secure raw material supply. A notable shift is the rise of customized crop-specific blends, forcing traditional bulk producers to innovate or lose share. Entry barriers remain high due to formulation complexity and supply chain control. Winning in this market requires technological differentiation, supply reliability, and the ability to deliver measurable on-field performance improvements.

Yara International

Nutrien Ltd.

ICL Group

Haifa Group

SQM (Sociedad Química y Minera de Chile)

K+S Aktiengesellschaft

EuroChem Group

Coromandel International Limited

Gujarat State Fertilizers & Chemicals Limited

The Mosaic Company

CF Industries Holdings, Inc.

OCI N.V.

Precision fertigation systems integrated with sensor-based monitoring are redefining nutrient delivery efficiency, with real-time dosing improving nutrient-use efficiency by 25% and reducing input waste by 18%. Adoption has crossed 40% among commercial farms, particularly in high-value crop segments. This integration enables automated adjustments based on soil and crop conditions, delivering measurable operational gains and lowering labor dependency, giving early adopters a clear cost-performance advantage.

Advanced chelation and nano-nutrient technologies are emerging as critical enablers of targeted nutrient absorption, improving micronutrient uptake by up to 30% compared to conventional formulations. Deployment remains at approximately 22% but is accelerating due to soil degradation concerns and demand for crop-specific solutions. These technologies reduce leaching losses and enhance yield consistency, positioning specialty fertilizer manufacturers ahead of bulk producers in performance-driven markets.

AI-driven crop analytics combined with digital advisory platforms are transforming fertilizer application strategies, with adoption nearing 28% across technologically advanced regions. These systems improve decision accuracy by 20% and reduce over-application, directly impacting cost optimization. Compared to legacy blanket application methods, AI-integrated systems deliver over 15% higher efficiency while lowering operational costs by 12%, creating a decisive competitive edge for integrated solution providers.

Looking ahead to 2026–2028, bio-enhanced soluble fertilizers and closed-loop nutrient systems in hydroponics are expected to scale rapidly, with efficiency gains exceeding 20% and adoption projected to surpass 35% in controlled farming environments. Companies investing in integrated nutrient ecosystems combining formulation, delivery, and analytics will dominate, as the market shifts from product-centric competition to performance-driven, technology-enabled differentiation.

March 2026 – Yara International expanded its specialty fertilizer production capacity in Europe by 12%, focusing on low-emission water-soluble formulations aligned with tightening environmental standards. This strengthens regional supply resilience and improves compliance-driven product positioning. [Capacity Expansion] Source: https://www.yara.com

November 2025 – Nutrien Ltd. partnered with a digital agriculture platform to integrate AI-based nutrient management, improving fertilizer application efficiency by 18% across pilot farms. This accelerates precision agriculture deployment and enhances operational decision-making. [Digital Integration] Source: https://www.nutrien.com

July 2025 – ICL Group launched a new line of bio-enhanced water-soluble fertilizers, achieving 20% higher nutrient uptake efficiency in controlled trials. This innovation supports sustainable farming practices and strengthens its specialty solutions portfolio. [Product Innovation] Source: https://www.icl-group.com

February 2024 – Haifa Group expanded its global distribution network by 15%, targeting Asia and Latin America to improve product accessibility and reduce delivery lead times. This move enhances supply chain efficiency and regional market penetration. [Market Expansion] Source: https://www.haifa-group.com

The report delivers comprehensive coverage of the water-soluble fertilizers market across key segments, including types such as nitrogen-based, phosphatic, potassic, NPK blends, and micronutrient fertilizers, alongside applications like fertigation, foliar application, greenhouse cultivation, open-field farming, and hydroponics. It further analyzes end-user segments including agriculture, horticulture growers, greenhouse operators, turf and landscape managers, and agricultural cooperatives. Geographically, the study spans five major regions with detailed country-level insights, capturing over 90% of global demand distribution. Technology coverage includes precision fertigation systems, nano-nutrient formulations, and AI-integrated nutrient management platforms, with adoption levels ranging from 25% to 40% across advanced markets.

Analytically, the report evaluates more than 15 segment combinations and profiles over 10 key companies, incorporating measurable indicators such as nutrient-use efficiency improvements of up to 30% and regional adoption differentials exceeding 20%. It highlights emerging segments such as hydroponics and bio-enhanced fertilizers, where adoption is rising above 18%, signaling future demand concentration. The report provides strategic value by enabling stakeholders to identify high-growth pockets, optimize investment allocation, and strengthen competitive positioning through technology adoption and regional expansion strategies, offering forward-looking insights aligned with market evolution through 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14841.99 Million |

|

Market Revenue in 2033 |

USD 18801.39 Million |

|

CAGR (2026 - 2033) |

3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Yara International, Nutrien Ltd., ICL Group, Haifa Group, SQM (Sociedad Química y Minera de Chile), K+S Aktiengesellschaft, EuroChem Group, Coromandel International Limited, Gujarat State Fertilizers & Chemicals Limited, The Mosaic Company, CF Industries Holdings, Inc., OCI N.V. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |