Reports

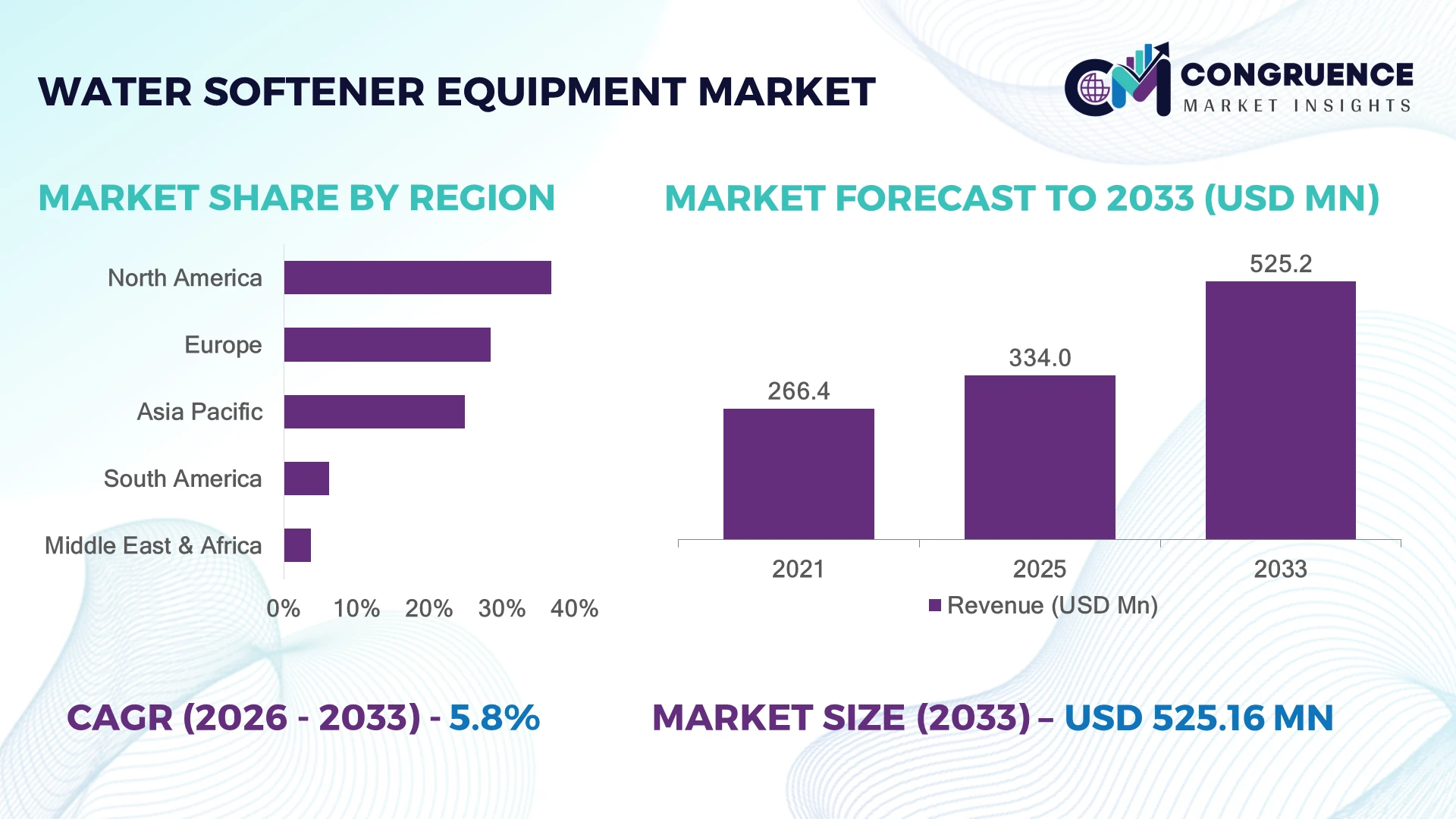

The Global Water Softener Equipment Market was valued at USD 334.0 Million in 2025 and is anticipated to reach a value of USD 525.2 Million by 2033 expanding at a CAGR of 5.82% between 2026 and 2033. Growth is driven by stricter industrial water quality standards, expanding municipal water treatment upgrades, and rising adoption of ion-exchange systems across manufacturing, commercial facilities, and residential infrastructure.

The United States leads the global market with an estimated 31% share, supported by extensive hard water prevalence, advanced municipal infrastructure, and strong demand from food processing, healthcare, and power generation industries. More than 85 million households experience hard water conditions, while industrial modernization and water reuse initiatives continue to accelerate equipment deployment. Compared with Germany, the U.S. maintains broader large-scale commercial adoption backed by higher infrastructure investment and replacement activity.

The market favors manufacturers investing in high-efficiency systems, digital monitoring capabilities, and region-specific distribution strategies to strengthen long-term competitive positioning.

Market Size & Growth: USD 334.0 Million in 2025 is projected to reach USD 525.2 Million by 2033 at a CAGR of 5.82%, supported by expanding industrial water treatment modernization and infrastructure upgrades.

Top Growth Drivers: Industrial water treatment demand contributes over 40%, municipal infrastructure upgrades exceed 30%, and residential replacement demand accounts for nearly 25% of market expansion.

Short-Term Forecast: By 2028, smart monitoring integration is expected to improve maintenance efficiency by approximately 20% while reducing servicing requirements by nearly 15%.

Emerging Technologies: AI-enabled diagnostics, connected IoT controllers, and advanced high-capacity resin technologies are improving operational performance and predictive maintenance.

Regional Leaders: North America approaches USD 160 Million, Europe exceeds USD 115 Million, and Asia-Pacific nears USD 135 Million, supported by infrastructure expansion and industrial water reuse initiatives.

Consumer/End-User Trends: More than 55% of commercial buyers prioritize intelligent monitoring, lower salt consumption, and automated regeneration capabilities during procurement.

Pilot/Case Example: In 2024, smart commercial softening installations reduced maintenance visits by nearly 18% while improving operational uptime across large facilities.

Competitive Landscape: The leading supplier holds approximately 16% market share, while EcoWater Systems, Culligan International, Pentair, A. O. Smith, and Kinetico continue expanding product portfolios.

Regulatory & ESG Impact: Water efficiency regulations and discharge management initiatives reduce salt consumption by nearly 20%, supporting sustainable water treatment operations.

Investment & Funding: More than USD 500 Million has been directed toward manufacturing expansion, automation, and strategic partnerships as global supply chains continue regional diversification.

Innovation & Future Outlook: Connected softening platforms, intelligent regeneration software, and modular industrial systems are accelerating operational efficiency and long-term product differentiation.

Water Softener Equipment Market demand continues to expand across municipal utilities, food processing, pharmaceuticals, hospitality, and residential applications where consistent water quality improves operational reliability and equipment lifespan. Smart controllers, low-salt regeneration technologies, and connected monitoring solutions are becoming standard features, while over 45% of newly introduced commercial systems emphasize water efficiency. Ongoing infrastructure modernization and tightening water quality regulations continue to shape procurement strategies, setting the stage for broader strategic market developments.

Water softener equipment has become a strategic investment area as industries seek greater operational reliability, lower maintenance costs, and improved water efficiency. Infrastructure modernization, stricter water quality regulations, and industrial process optimization are encouraging manufacturers to expand production capacity while strengthening regional supply networks. Competitive differentiation increasingly depends on system intelligence, lifecycle performance, and service capabilities rather than equipment alone.

Modern smart water softeners equipped with automated regeneration and remote monitoring reduce salt consumption by nearly 20% and lower maintenance interventions by approximately 15% compared with conventional manually controlled systems. North America continues to lead in large-scale commercial deployments, while Asia-Pacific records faster installation activity through manufacturing expansion and urban infrastructure projects. During the next two to three years, connected monitoring capabilities are expected to be integrated into more than 35% of newly installed commercial systems.

Industrial facilities, hospitals, and hospitality operators are increasingly deploying centralized water softening systems to improve equipment protection and reduce operational downtime. Leading manufacturers are expanding regional production, strengthening distributor partnerships, and investing in digital service platforms to improve customer support and lifecycle management. Organizations that combine efficient system design with intelligent monitoring and localized supply capabilities will establish stronger competitive positions and sustain long-term operational advantage.

Industrial compliance requirements and infrastructure modernization are strengthening demand for advanced water softener equipment across manufacturing, healthcare, food processing, and commercial facilities. More than 60% of industrial boilers operate more efficiently with treated water, while optimized softening systems reduce scale formation by nearly 35% and lower maintenance frequency by approximately 20%. In the United States, tightening wastewater discharge standards and water reuse initiatives are encouraging facilities to replace aging treatment assets with intelligent softening solutions. This operational shift improves equipment longevity and process reliability. Leading manufacturers are expanding smart product portfolios, investing in connected monitoring platforms, and partnering with industrial service providers to deliver predictive maintenance capabilities. Companies combining digital diagnostics with efficient resin technologies are securing stronger long-term positions in high-value industrial applications.

The market continues to face structural pressure from fluctuating prices of ion-exchange resins, engineering plastics, and electronic control components, with procurement costs varying by nearly 15% during recent supply disruptions. More than 40% of specialized resin production remains concentrated among a limited number of global suppliers, increasing sourcing dependency for equipment manufacturers. In Germany, higher energy and manufacturing costs have also influenced production efficiency and replacement timelines. These constraints affect pricing consistency, project planning, and operating margins, particularly for mid-sized manufacturers. Companies are reducing exposure through supplier diversification, localized component sourcing, long-term procurement agreements, and standardized product platforms. Strengthening regional manufacturing networks has become a strategic priority to improve supply resilience and delivery performance.

Digital water management platforms are opening new opportunities beyond conventional residential installations. More than 45% of newly specified commercial treatment projects now include remote monitoring capabilities, while automated regeneration technologies reduce salt consumption by nearly 20% and improve service efficiency by approximately 18%. Japan continues to expand intelligent building infrastructure where connected water treatment systems support facility automation and preventive maintenance. Equipment manufacturers are increasing investment in IoT-enabled controllers, AI-assisted diagnostics, and cloud-based service platforms to deliver subscription-based monitoring solutions. A growing strategic opportunity lies in integrating water softening systems with broader building management ecosystems, allowing customers to optimize operational efficiency while reducing lifecycle maintenance costs through continuous performance analytics.

Expanding advanced water softener deployments across aging and mixed infrastructure remains a significant execution challenge. Nearly 30% of commercial buildings require additional plumbing modifications before intelligent systems can be fully integrated, while installation complexity increases project timelines by approximately 15%. In India, inconsistent water quality characteristics across municipalities require customized system configuration and resin optimization, limiting standardized deployment strategies. Workforce shortages in specialized installation and digital commissioning further affect implementation quality and long-term system performance. Manufacturers are addressing these challenges through installer certification programs, modular equipment architectures, digital commissioning software, and expanded technical support partnerships. Organizations capable of simplifying deployment while maintaining consistent operational performance will strengthen competitiveness in increasingly technology-driven water treatment markets.

Smart Connected System Expansion: Intelligent water softeners are becoming standard across commercial and industrial facilities as remote monitoring adoption exceeds 42% of new installations and predictive maintenance lowers unplanned servicing by nearly 18%. Digital controllers optimize regeneration cycles, reducing salt usage by approximately 20%. Manufacturers are expanding cloud-enabled product portfolios and integrating automated diagnostics to improve asset uptime while addressing skilled labor shortages.

Low-Salt Regeneration Technologies: High-efficiency regeneration systems continue replacing conventional designs as advanced resin optimization reduces water consumption by almost 25% while lowering operating costs by nearly 15%. Regulatory attention on wastewater discharge is accelerating deployment in the United States and Germany. Equipment suppliers are redesigning valve assemblies and investing in compact system architectures that simplify installation and improve long-term operating performance.

Industrial Retrofit Momentum: Manufacturing facilities increasingly replace aging water treatment assets instead of constructing entirely new systems, with retrofit projects representing nearly 45% of commercial deployments. Food processing, pharmaceuticals, and electronics manufacturers prioritize modular equipment that minimizes production interruptions. Companies are expanding regional engineering capabilities, strengthening installer networks, and standardizing modular product platforms to shorten project execution and improve lifecycle support.

Localized Manufacturing Strategies: Supply-chain resilience has become an operational priority as over 35% of equipment producers increase localized component sourcing to reduce delivery variability and inventory risk. Digital procurement platforms improve supplier visibility while automation accelerates production scheduling by approximately 16%. Manufacturers are restructuring supplier partnerships, expanding regional assembly capacity, and increasing inventory flexibility to strengthen customer responsiveness across industrial and commercial markets.

Ion Exchange Water Softeners remain the dominant segment, accounting for approximately 62% of global demand because of their proven hardness removal efficiency, mature supply ecosystem, and compatibility with residential, commercial, and industrial water treatment systems. Their reliable performance, scalable configurations, and relatively low maintenance requirements continue to support widespread deployment. Salt-Free Water Softeners represent the fastest-growing segment as organizations seek lower-maintenance alternatives and reduced environmental impact, with adoption increasing by nearly 17% across commercial buildings. Dual-Tank Water Softeners continue gaining traction where uninterrupted water availability is operationally essential, while Magnetic and Electronic Water Conditioners serve niche applications where installation simplicity is prioritized over complete hardness removal. Manufacturers are strengthening product differentiation through intelligent regeneration controls, compact modular designs, and digital monitoring capabilities. More than 48% of newly introduced premium systems incorporate smart diagnostics, reflecting increasing customer preference for connected equipment. Investment priorities continue shifting toward efficient resin technology, automated control valves, and reduced salt consumption to improve lifecycle performance and customer retention.

Industrial Water Treatment remains the largest application segment, representing approximately 39% of total equipment deployment due to stringent water quality requirements across power generation, food processing, pharmaceuticals, and manufacturing operations. Continuous process reliability and equipment protection sustain investment in centralized softening systems. Municipal Water Treatment is emerging as the fastest-growing application as infrastructure modernization and treated water distribution projects expand across developing economies. Commercial Buildings continue increasing adoption through hospitality, healthcare, and office infrastructure upgrades, while Residential Water Treatment maintains stable replacement demand. Boiler Feed Water Treatment remains strategically important where scale prevention directly influences energy efficiency and equipment lifespan. Equipment suppliers are expanding integrated solutions combining intelligent monitoring with automated regeneration to support higher operational efficiency. Nearly 44% of new commercial installations now include digital control platforms that simplify maintenance planning and improve system reliability. Modular deployment models and standardized engineering packages continue reducing installation complexity across large-scale projects.

Manufacturing Industries remain the leading end-user segment, contributing nearly 36% of total equipment demand because production processes require consistent water quality for operational efficiency and asset protection. Water Utilities represent the fastest-growing end-user group as governments modernize treatment infrastructure and improve distribution efficiency. Healthcare Facilities continue expanding installations to protect sterilization equipment and laboratory operations, while Hospitality strengthens demand through guest service quality and appliance protection. Residential Consumers remain an important volume segment, particularly in areas with persistent hard water conditions. Manufacturers are increasingly developing sector-specific product configurations and service packages tailored to industrial facilities, utilities, and institutional customers. Approximately 41% of enterprise procurement contracts now include predictive maintenance services and remote performance monitoring. Companies are strengthening distributor partnerships, expanding localized service capabilities, and offering customized lifecycle support programs to improve customer retention and operational reliability across diverse end-user environments.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

North America maintains the largest position in the Water Softener Equipment Market, supported by widespread hard water conditions, advanced industrial infrastructure, and continuous investment in commercial water treatment systems. Manufacturing, healthcare, food processing, hospitality, and power generation remain the primary deployment sectors, while digital water management platforms continue improving operational efficiency. The region contributes nearly 37% of global installations, with commercial and industrial applications accounting for more than 58% of equipment demand. Connected monitoring, automated regeneration controls, and predictive maintenance technologies are increasingly integrated into new installations. Equipment manufacturers continue expanding regional assembly operations, strengthening distributor partnerships, and enhancing aftermarket service capabilities to shorten project delivery cycles and improve customer retention across large enterprise accounts.

United States Market Outlook: The United States represents the largest national market due to extensive industrial activity, mature municipal infrastructure, and widespread hard water conditions affecting more than 85 million households. Industrial users continue replacing aging treatment equipment with intelligent water softening systems that improve equipment reliability and reduce maintenance requirements. Large manufacturers are expanding localized production, while digital monitoring platforms are becoming standard across commercial facilities to improve operational visibility and lifecycle asset management.

Europe remains a technologically advanced market where regulatory compliance, water efficiency initiatives, and industrial modernization continue shaping procurement decisions. The region accounts for approximately 28.4% of global demand, supported by strong adoption across pharmaceuticals, food processing, healthcare, and commercial infrastructure. Nearly 46% of newly installed commercial systems incorporate advanced control technologies that optimize regeneration cycles and reduce resource consumption. Industrial users increasingly prioritize compact, low-maintenance equipment that aligns with sustainability objectives. Manufacturers are investing in automated production, expanding regional service networks, and developing environmentally efficient resin technologies to strengthen competitive differentiation while meeting evolving environmental performance standards.

Germany Market Outlook: Germany leads the European market through its advanced manufacturing ecosystem, engineering expertise, and strong industrial water quality standards. Chemical processing, automotive manufacturing, and pharmaceutical production continue driving equipment deployment. More than 40% of industrial replacement projects prioritize digitally controlled water treatment systems, encouraging suppliers to expand intelligent product portfolios and strengthen long-term maintenance partnerships with enterprise customers.

Asia-Pacific is emerging as the fastest-expanding market due to accelerating industrialization, urban infrastructure development, and growing investment in municipal water treatment. The region represents approximately 24.9% of global market activity, while manufacturing facilities account for nearly half of new commercial installations. Industrial parks, electronics manufacturing, food processing, and healthcare infrastructure continue increasing demand for high-capacity softening systems. Equipment suppliers are expanding production facilities, improving localized supply chains, and introducing modular product platforms to meet diverse operational requirements. Ongoing investments in industrial water reuse and infrastructure modernization continue strengthening long-term deployment opportunities across both public and private sectors.

China Market Outlook: China dominates the regional market through its extensive manufacturing base, expanding municipal infrastructure, and continuous investment in industrial water management. Electronics, chemicals, pharmaceuticals, and power generation remain major end users. More than 45% of new industrial facilities now integrate advanced water treatment systems during initial project development, encouraging manufacturers to expand domestic production capacity and accelerate product innovation.

South America continues strengthening its market position through increasing industrial investment, commercial construction activity, and modernization of municipal water infrastructure. The region contributes approximately 6.2% of global demand, with mining, food processing, hospitality, and manufacturing sectors driving equipment deployment. Nearly 32% of recent commercial water treatment projects include high-efficiency softening systems to improve equipment durability and reduce operating costs. Manufacturers are expanding regional distribution partnerships and strengthening technical support capabilities to improve project execution despite infrastructure variability and logistics challenges across several countries.

Brazil Market Outlook: Brazil represents the region's largest market because of its diversified industrial economy, expanding food and beverage sector, and continuous investment in commercial infrastructure. Industrial operators increasingly deploy automated water treatment systems to improve production reliability and reduce maintenance downtime. Equipment suppliers continue strengthening local distribution networks while expanding engineering support services for large industrial customers.

The Middle East & Africa market is expanding through major investments in water infrastructure, industrial diversification, and commercial real estate development. The region accounts for approximately 3.7% of global demand, with desalination support systems, hospitality, healthcare, and oil and gas facilities driving equipment adoption. More than 38% of newly developed commercial properties incorporate centralized water treatment solutions to improve operational efficiency and equipment protection. Manufacturers are increasing regional partnerships, enhancing local service capabilities, and supplying customized systems designed for high-mineral water conditions and demanding operating environments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional deployment through large-scale infrastructure projects, industrial diversification initiatives, and significant investment in water management facilities. Energy, hospitality, healthcare, and municipal utilities remain major equipment users. Industrial operators increasingly specify intelligent water softening systems for integrated treatment networks, while international manufacturers continue expanding regional partnerships and technical support operations to strengthen long-term project delivery and lifecycle services.

The competitive landscape is led by A. O. Smith, Pentair, Culligan International, EcoWater Systems, and Kinetico, which primarily compete against regional manufacturers and value-focused OEMs through technology, service capability, and distribution reach rather than price alone. The top five companies collectively account for approximately 46% of the global market, leaving substantial opportunities for specialized local suppliers. Premium brands differentiate through intelligent controls, connected monitoring, and lifecycle service contracts, while regional competitors compete with pricing that is typically 15–20% lower and faster customization. More than 55% of enterprise buyers prioritize operational efficiency and digital monitoring over initial acquisition cost, strengthening the position of technology-focused suppliers. Companies continue expanding manufacturing capacity, strengthening dealer networks, pursuing strategic partnerships, and increasing vertical integration for critical components to improve supply resilience. Competition is shifting toward digitally enabled water management platforms and recurring service models. Strong distribution networks, technical support, regulatory compliance, and continuous product innovation remain the essential requirements for outperforming established market leaders.

Pentair plc

Culligan International

EcoWater Systems LLC

Kinetico Incorporated

BWT Holding GmbH

Canature Health Technology Group Co., Ltd.

Harvey Water Softeners

US Water Systems

Water-Right, Inc.

Atlas Filtri S.r.l.

Marlo Incorporated

Smart automation is becoming the defining technology across the Water Softener Equipment Market. IoT-enabled controllers, cloud-connected monitoring, and predictive maintenance platforms now support approximately 42% of newly deployed commercial systems. Automated regeneration algorithms reduce salt consumption by nearly 20% while lowering maintenance interventions by around 15%, providing measurable operational savings for industrial and commercial users. Manufacturers integrating digital diagnostics gain stronger aftermarket engagement and improved equipment lifecycle management.

Advanced ion-exchange resin engineering, high-efficiency control valves, and compact modular system architecture are replacing conventional timer-based equipment. Modern demand-based regeneration improves water efficiency by approximately 25% compared with legacy fixed-cycle systems while extending resin service life by nearly 18%. Smart valve technology also enables remote performance optimization, reducing field service requirements. Premium manufacturers benefit most from these innovations because enterprise customers increasingly prioritize operating efficiency and predictive asset management over conventional standalone equipment.

Between 2026 and 2028, AI-assisted diagnostics, digital twins for water treatment assets, and integrated building management connectivity are expected to reshape commercial deployments. More than 35% of enterprise installations are projected to include centralized monitoring platforms supporting multiple treatment assets. Companies investing early in intelligent software ecosystems, modular upgrades, and connected service platforms will strengthen competitive positioning through higher customer retention, lower operating costs, faster maintenance response, and improved long-term equipment performance.

May 2025 – Culligan International introduced Culligan with ZeroWater Technology featuring a five-stage filtration platform and an integrated TDS meter capable of removing 99.9% of total dissolved solids, strengthening its premium residential water treatment portfolio. Source: www.culliganinternational.com

January 2026 – A. O. Smith completed the acquisition of Leonard Valve, expanding its commercial water management portfolio and strengthening integrated building water solutions while supporting broader technology integration across institutional applications. Source: www.aosmith.gcs-web.com

June 2026 – Kinetico launched the HYDRO ECO tankless reverse osmosis system delivering certified on-demand purification in a compact platform. A consumer survey associated with the launch found 58% of U.S. households expressed concerns about tap water quality. Source: www.prnewswire.com

April 2026 – Pentair released its 2025 Sustainability Report highlighting continued progress in water stewardship and product sustainability initiatives while advancing digital water management capabilities across residential and commercial product lines.

The report provides comprehensive analysis of the global Water Softener Equipment Market across major product types, applications, end-user industries, and key geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates technology evolution, deployment trends, competitive positioning, industrial adoption, distribution strategies, and emerging opportunities across residential, commercial, municipal, and industrial water treatment environments. More than 60% of market demand is concentrated within industrial and commercial applications, while intelligent monitoring solutions continue expanding across new installations.

The study delivers strategic intelligence covering product innovation, digital water management technologies, regulatory developments, supply-chain evolution, and enterprise purchasing behavior between 2026 and 2033. It assesses competitive benchmarking, regional deployment patterns, technology adoption rates, and company strategies to support investment evaluation, market entry planning, portfolio optimization, expansion prioritization, partnership development, and long-term competitive positioning across established and emerging application segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 334.0 Million |

| Market Revenue (2033) | USD 525.2 Million |

| CAGR (2026–2033) | 5.82% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | A. O. Smith Corporation; Pentair plc; Culligan International; EcoWater Systems LLC; Kinetico Incorporated; BWT Holding GmbH; Canature Health Technology Group Co., Ltd.; Harvey Water Softeners; US Water Systems; Water-Right, Inc.; Atlas Filtri S.r.l.; Marlo Incorporated |

| Customization & Pricing | Available on Request (10% Customization Free) |