Reports

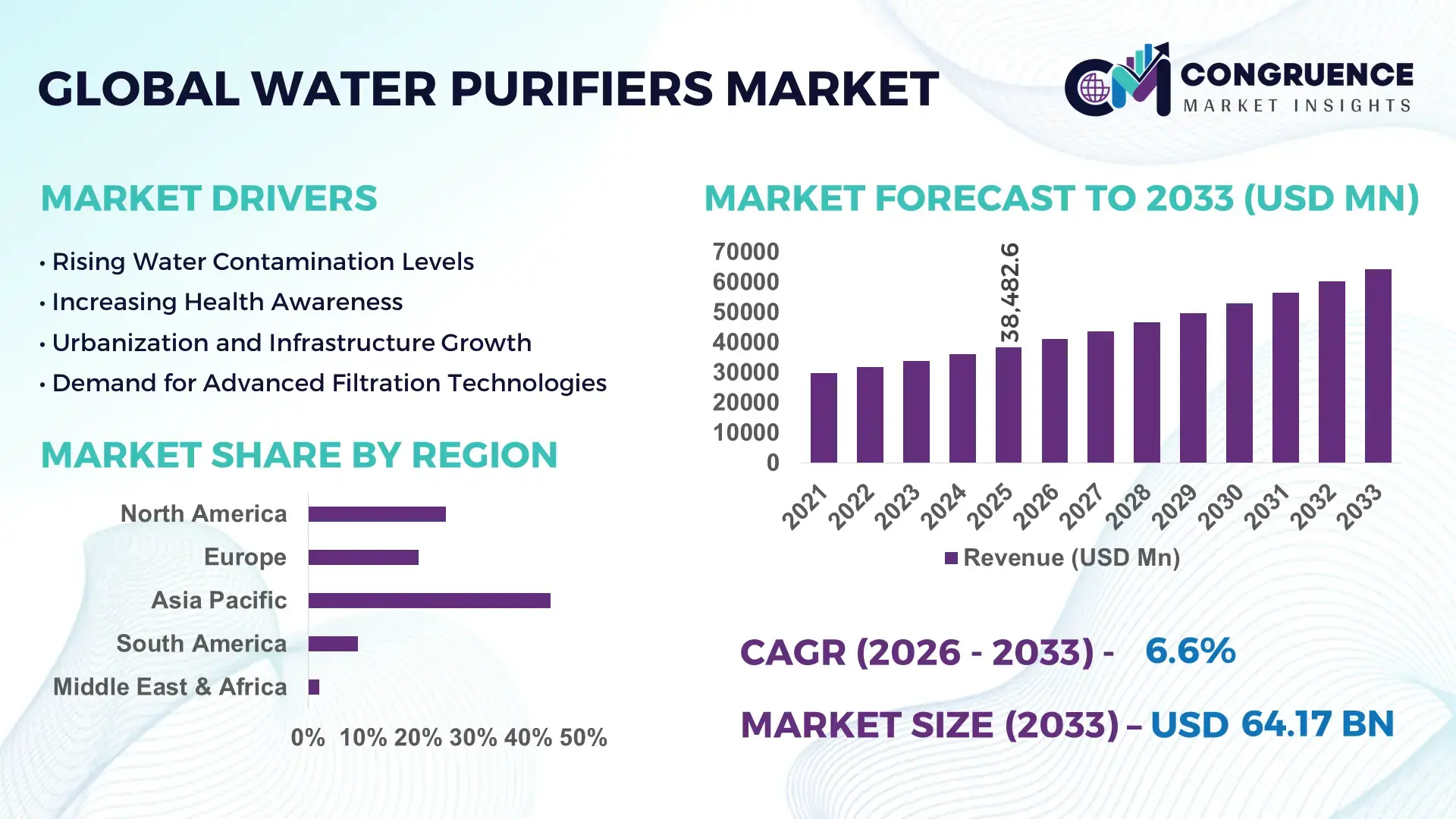

The Global Water Purifiers Market was valued at USD 38482.6 Million in 2025 and is anticipated to reach a value of USD 64168.52 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033. The growth is primarily driven by increasing concerns over water contamination and rising demand for safe drinking water solutions across urban and rural populations.

China continues to dominate the water purifiers market with extensive manufacturing capacity and large-scale investments in water treatment infrastructure. The country produces over 40% of global household purification units annually, supported by more than 3,000 active manufacturers and component suppliers. Urban adoption of advanced purification technologies such as reverse osmosis and ultrafiltration exceeds 65% in Tier-1 cities, while rural penetration is expanding through government-backed clean water initiatives covering over 300 million residents. Industrial applications, particularly in food processing and electronics manufacturing, account for nearly 30% of domestic purifier demand. Continuous innovation in smart filtration systems and IoT-enabled monitoring devices has led to a 20% increase in product efficiency and lifecycle performance, strengthening China's leadership in production scale and technological advancement.

Market Size & Growth: USD 38482.6 Million in 2025, projected to reach USD 64168.52 Million by 2033, growing at 6.6%, driven by rising demand for advanced water filtration systems in residential and industrial sectors.

Top Growth Drivers: Urban adoption increase by 48%, industrial water reuse efficiency improvement by 35%, and smart purifier integration growth by 42%.

Short-Term Forecast: By 2028, smart water purifier systems are expected to improve filtration monitoring accuracy by 30% and reduce maintenance costs by 25%.

Emerging Technologies: AI-based water quality sensors, IoT-enabled purification devices, and nanotechnology filtration membranes are transforming system performance.

Regional Leaders: Asia-Pacific projected to exceed USD 28000 Million by 2033 with strong urban demand; North America to reach USD 15000 Million driven by smart home adoption; Europe expected to surpass USD 12000 Million with sustainability-focused solutions.

Consumer/End-User Trends: Residential users account for over 60% adoption, while commercial sectors such as healthcare and hospitality are increasing usage by 20% annually.

Pilot or Case Example: In 2024, India implemented smart water purification units in urban clusters, achieving 35% reduction in waterborne contamination incidents.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players including multinational filtration technology firms and regional manufacturers.

Regulatory & ESG Impact: Governments are enforcing water quality standards, with over 50 countries implementing stricter purification compliance and sustainability benchmarks.

Investment & Funding Patterns: Recent investments exceed USD 5 billion globally, with strong growth in smart water infrastructure and decentralized purification systems.

Innovation & Future Outlook: Integration of AI diagnostics, energy-efficient purification technologies, and modular filtration units is shaping future market expansion.

The water purifiers market is influenced by a combination of residential demand, industrial water treatment requirements, and government-led infrastructure programs. Residential applications contribute approximately 60% of total demand, while industrial sectors such as pharmaceuticals, food processing, and electronics account for nearly 25%. Innovations in membrane technology, including graphene-based filters, have improved contaminant removal efficiency by up to 40%. Regulatory frameworks focused on safe drinking water and wastewater reuse are accelerating adoption, especially in Asia-Pacific and the Middle East. Increasing urbanization, coupled with rising health awareness, is driving consistent consumption growth. Future trends indicate a shift toward smart, energy-efficient purification systems integrated with real-time monitoring and predictive maintenance capabilities.

The water purifiers market holds strategic importance as governments and industries prioritize water security, public health, and sustainable resource management. Advanced purification technologies such as AI-enabled filtration systems deliver up to 35% improvement in contaminant detection accuracy compared to conventional reverse osmosis systems. Asia-Pacific dominates in volume due to high population density and infrastructure expansion, while North America leads in adoption with over 55% of households using advanced purification systems integrated with smart home ecosystems.

In the short term, by 2028, AI-driven water quality monitoring is expected to reduce operational inefficiencies by 30% while improving system reliability by 25%. Companies are increasingly investing in modular purification systems that enable decentralized water treatment, particularly in remote and underserved areas. ESG commitments are also shaping strategic decisions, with firms targeting up to 40% reduction in wastewater discharge and 25% improvement in water recycling rates by 2030.

A notable micro-scenario occurred in 2024, where India deployed IoT-enabled purification systems across municipal networks, achieving a 32% reduction in waterborne disease incidents through real-time contamination alerts. Regulatory bodies are enforcing stringent water quality standards, compelling manufacturers to innovate in energy-efficient and low-waste filtration technologies. Looking ahead, the water purifiers market is positioned as a critical pillar for resilience, regulatory compliance, and sustainable growth, driven by technological advancements, increasing investments, and rising global awareness of water quality challenges.

The increasing level of water contamination due to industrial discharge, agricultural runoff, and urban waste is a major driver for the water purifiers market. According to global environmental data, nearly 80% of wastewater is discharged untreated into natural water bodies, significantly impacting drinking water sources. This has led to a surge in demand for advanced purification systems capable of removing heavy metals, bacteria, and chemical pollutants. Urban households are increasingly adopting multi-stage purification systems, with penetration rates exceeding 70% in several metropolitan regions. Additionally, industries are investing in high-capacity filtration systems to comply with strict water quality regulations. Public awareness campaigns and health concerns related to waterborne diseases have further accelerated adoption, making purification systems an essential household and commercial utility.

The high initial cost of advanced water purification systems, particularly those using reverse osmosis and smart monitoring technologies, remains a key restraint in the market. Installation costs can account for up to 25% of the total system price, while annual maintenance expenses, including filter replacement and servicing, can add another 15–20%. These cost barriers limit adoption in price-sensitive regions, especially in rural and low-income populations. Additionally, the requirement for regular maintenance and skilled servicing creates operational challenges. In developing economies, limited access to service networks further complicates system upkeep. As a result, consumers often opt for low-cost alternatives with limited filtration capabilities, impacting the overall penetration of advanced purification technologies.

The integration of smart technologies presents significant opportunities in the water purifiers market. IoT-enabled purification systems allow real-time monitoring of water quality, filter life, and system performance, improving efficiency by up to 30%. These systems are increasingly being adopted in urban households and commercial facilities, driven by the growing trend of connected devices. Emerging markets are also witnessing increased deployment of decentralized purification units powered by solar energy, expanding access to clean water in remote areas. Furthermore, advancements in nanotechnology-based filtration are enabling the removal of microscopic contaminants with higher precision. Governments and private organizations are investing in smart water infrastructure, creating a favorable environment for innovation and market expansion.

Stringent regulatory requirements related to water quality and environmental sustainability pose challenges for manufacturers in the water purifiers market. Compliance with multiple regional standards requires continuous investment in research and development, increasing operational costs. Additionally, traditional purification systems, particularly reverse osmosis, generate significant wastewater, with rejection rates ranging from 30% to 50%, raising environmental concerns. Disposal of used filters and cartridges also contributes to waste management issues. Manufacturers must innovate to develop eco-friendly solutions that minimize water wastage and reduce environmental impact. Balancing regulatory compliance with cost efficiency remains a critical challenge, especially for small and medium-sized enterprises operating in competitive markets.

• Rapid Expansion of Smart and IoT-Enabled Water Purifiers: The adoption of smart water purifiers integrated with IoT technology has increased by over 42% in urban households, enabling real-time monitoring of water quality, filter status, and usage patterns. Approximately 55% of premium purifier models launched in 2025 included app-based connectivity features, while sensor-driven filtration systems improved detection accuracy of contaminants by nearly 30%. This trend is particularly strong in developed regions, where over 60% of new installations are connected devices, supporting predictive maintenance and reducing servicing frequency by 25%.

• Growing Demand for Energy-Efficient and Low-Waste Filtration Systems: Energy-efficient water purifiers have gained traction, with systems reducing power consumption by up to 35% compared to conventional models. Additionally, innovations in reverse osmosis technology have decreased water wastage ratios from 50% to nearly 25%, addressing environmental concerns. Over 48% of newly deployed purification systems in 2025 were designed with water-saving mechanisms, reflecting increasing regulatory pressure and consumer preference for sustainable solutions across residential and commercial sectors.

• Surge in Point-of-Use and Portable Purification Devices: The demand for compact, point-of-use water purifiers has increased by approximately 38%, driven by urban mobility trends and space constraints in modern housing. Portable purification units, including UV and gravity-based systems, now account for nearly 28% of total unit sales in emerging economies. These devices offer up to 99% bacterial removal efficiency and are widely adopted in regions with inconsistent water supply, particularly in Asia-Pacific and Africa, where decentralized solutions are critical for ensuring safe drinking water access.

• Integration of Advanced Filtration Materials and Nanotechnology: The use of nanotechnology-based membranes and graphene filters has improved contaminant removal efficiency by over 40%, particularly for heavy metals and microplastics. Around 33% of newly developed filtration systems incorporate advanced materials that extend filter life by up to 50%, reducing replacement frequency and operational costs. This trend is supported by increasing R&D investments, with over 20% of manufacturers focusing on next-generation filtration materials to enhance performance and durability in high-demand industrial and residential applications.

The water purifiers market is segmented across product types, applications, and end-user categories, each contributing uniquely to overall demand patterns. Reverse osmosis, ultrafiltration, and UV purification systems dominate the product landscape, with increasing integration of hybrid technologies to enhance efficiency. Residential applications lead in volume, driven by urbanization and health awareness, while commercial and industrial segments are expanding due to regulatory compliance requirements. End-user insights reveal strong adoption across households, healthcare institutions, and manufacturing sectors. Approximately 60% of total installations are concentrated in residential use, while industrial applications contribute nearly 25%, particularly in food processing and pharmaceuticals. Regional consumption patterns vary, with Asia-Pacific leading in unit demand and North America focusing on technologically advanced systems. The market is witnessing a transition toward smart, sustainable, and compact purification solutions, supported by evolving consumer preferences and stricter water quality regulations.

The water purifiers market by type includes reverse osmosis (RO), ultraviolet (UV), ultrafiltration (UF), gravity-based purifiers, and hybrid systems. Reverse osmosis systems currently dominate the segment, accounting for approximately 48% of total adoption due to their ability to remove dissolved solids, heavy metals, and chemical contaminants with high efficiency. UV purification systems hold around 22% share, primarily used for microbial disinfection, while ultrafiltration systems contribute nearly 15% due to their low energy consumption and effectiveness in removing suspended particles.

Hybrid systems are the fastest-growing segment, expanding at an estimated CAGR of 8.2%, driven by their ability to combine RO, UV, and UF technologies for multi-stage purification. These systems are increasingly preferred in urban households and commercial establishments where water quality varies significantly. Gravity-based purifiers and other niche technologies collectively account for approximately 15% of the market, particularly in rural and off-grid areas due to their low cost and ease of use.

The application segment of the water purifiers market includes residential, commercial, and industrial uses. Residential applications lead the segment, accounting for nearly 62% of total adoption, driven by increasing health awareness, urban population growth, and rising concerns over waterborne diseases. Commercial applications, including hospitality, healthcare, and educational institutions, represent around 23% of the market, where consistent water quality is essential for operations and compliance.

Industrial applications, although currently accounting for approximately 15%, are the fastest-growing segment with an estimated CAGR of 7.5%. This growth is driven by stringent regulatory requirements in sectors such as pharmaceuticals, food and beverage processing, and electronics manufacturing, where water purity is critical for production processes. Advanced purification systems in these industries can reduce contaminants by over 95%, ensuring compliance with strict quality standards.

The end-user segment of the water purifiers market includes households, commercial establishments, industrial facilities, and institutional users. Households remain the leading end-user category, accounting for approximately 60% of total installations, driven by increasing urbanization and rising consumer awareness regarding water quality. Commercial establishments, including hotels, restaurants, and offices, contribute around 20%, where purified water is essential for daily operations and customer satisfaction.

Industrial users represent the fastest-growing segment, with an estimated CAGR of 7.8%, fueled by increasing demand for high-purity water in manufacturing processes. Industries such as pharmaceuticals and food processing report adoption rates exceeding 70% for advanced purification systems to meet regulatory standards. Institutional users, including schools and government facilities, account for the remaining 20%, benefiting from public health initiatives and infrastructure investments.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Asia-Pacific leads with over 220 million units installed, driven by rapid urbanization and increasing water contamination concerns across China and India, where household penetration exceeds 58% in urban areas. North America holds approximately 24% share, supported by strong adoption of smart purification systems, with over 65% of households using advanced filtration technologies. Europe accounts for nearly 18% of the market, with sustainability regulations pushing demand for energy-efficient purifiers. South America and the Middle East & Africa collectively contribute around 12%, with infrastructure development projects increasing access to clean water. Globally, over 70% of demand is concentrated in residential use, while industrial and commercial applications account for 30%, reflecting a diversified consumption pattern across regions.

North America accounts for approximately 24% of the global water purifiers market, with strong demand driven by residential, healthcare, and food service industries. Over 65% of households utilize advanced purification systems, including reverse osmosis and UV technologies, reflecting high consumer awareness regarding water quality. Regulatory frameworks such as strict drinking water standards have led to increased adoption of certified purification systems, with compliance rates exceeding 80% across major states. Technological advancements include the integration of IoT-enabled devices, where nearly 58% of new installations feature smart monitoring capabilities. A notable regional player has introduced AI-based filtration systems that improve contaminant detection accuracy by 30%, enhancing system efficiency. Consumer behavior shows a preference for premium, multi-stage purification systems, particularly in urban areas, where health-conscious buyers prioritize advanced features and long-term reliability.

Europe holds around 18% of the global water purifiers market, with key markets including Germany, the United Kingdom, and France contributing significantly to regional demand. Stringent environmental regulations and sustainability initiatives have led to a 40% increase in adoption of energy-efficient purification systems. Regulatory bodies enforce strict water quality standards, prompting manufacturers to innovate in eco-friendly filtration technologies. Approximately 52% of new systems incorporate low-waste or recyclable components, aligning with circular economy goals. Advanced technologies such as nanofiltration and smart sensors are being widely adopted, improving filtration efficiency by over 35%. A regional manufacturer has developed compact purification units designed for urban households, reducing water wastage by 28%. Consumer behavior in this region reflects a strong preference for sustainable and transparent purification processes, with over 60% of buyers prioritizing environmentally compliant products.

Asia-Pacific leads the water purifiers market in volume, accounting for over 220 million installed units and ranking as the largest consumption hub globally. China, India, and Japan are the top consuming countries, collectively contributing more than 70% of regional demand. Rapid urbanization has resulted in urban adoption rates exceeding 58%, while rural penetration continues to expand through government-backed clean water programs covering over 300 million individuals. The region is also a major manufacturing hub, producing over 40% of global purification systems annually. Technological innovation is accelerating, with over 45% of new products integrating smart features such as real-time water quality monitoring. A leading regional manufacturer has launched affordable IoT-enabled purifiers, increasing adoption by 25% in mid-income households. Consumer behavior varies, with strong growth driven by e-commerce platforms and mobile-based purchasing, enabling wider accessibility across diverse income groups.

South America accounts for approximately 7% of the global water purifiers market, with Brazil and Argentina serving as key markets. Infrastructure development and increasing awareness of waterborne diseases have driven adoption rates, particularly in urban centers where penetration has reached nearly 42%. Government initiatives aimed at improving water quality have led to a 30% increase in installation of purification systems in public facilities. The region is witnessing growth in energy-efficient purification technologies, with nearly 35% of new systems designed to reduce power consumption. Trade policies supporting import of advanced filtration components have enhanced product availability. A regional player has introduced cost-effective purification systems tailored for low-income households, improving access to clean water for over 2 million users. Consumer behavior indicates demand is closely tied to affordability and reliability, with a growing preference for durable, low-maintenance systems.

The Middle East & Africa region contributes approximately 5% of the global water purifiers market, with demand driven by water scarcity and rapid industrialization in countries such as the UAE and South Africa. Over 40% of water purification demand in this region is linked to industrial applications, particularly in oil & gas and construction sectors. Technological modernization is evident, with 38% of new installations featuring advanced desalination-compatible purification systems. Government initiatives promoting water conservation have led to increased adoption of efficient filtration technologies, with regulations targeting a 25% reduction in water wastage. Trade partnerships and infrastructure investments are supporting market expansion. A regional manufacturer has developed solar-powered purification units, increasing accessibility in off-grid areas by 20%. Consumer behavior reflects a strong reliance on durable and high-capacity systems due to extreme environmental conditions and limited water availability.

China Water Purifiers Market – 32% share: Dominance driven by high production capacity, strong domestic demand, and extensive manufacturing ecosystem.

India Water Purifiers Market – 21% share: Growth supported by large population base, government clean water initiatives, and rising urban adoption of purification systems.

The water purifiers market is moderately fragmented, with over 150 active global and regional players competing across residential, commercial, and industrial segments. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet diversified landscape. Leading companies are focusing on product innovation, with more than 45% of new product launches incorporating smart technologies such as IoT-enabled monitoring and AI-based filtration diagnostics. Strategic partnerships and collaborations have increased by 28% over the past two years, particularly in emerging markets where distribution networks are expanding rapidly.

Mergers and acquisitions are also shaping the competitive environment, with over 20 notable deals recorded in 2024 and 2025 aimed at strengthening technological capabilities and market reach. Companies are investing heavily in research and development, allocating nearly 12% of their operational budgets to develop advanced filtration materials and energy-efficient systems. Competitive differentiation is increasingly based on product performance, sustainability features, and digital integration. Additionally, regional players are gaining traction by offering cost-effective solutions tailored to local market needs, intensifying competition and driving innovation across the industry.

A.O. Smith Corporation

Kent RO Systems Ltd.

Eureka Forbes Ltd.

Panasonic Corporation

LG Electronics Inc.

Unilever PLC

Coway Co., Ltd.

Amway Corporation

Culligan International Company

3M Company

Brita GmbH

Tata Chemicals Limited

The water purifiers market is undergoing rapid technological transformation driven by advancements in filtration science, digital monitoring, and material engineering. Reverse osmosis (RO) technology continues to evolve, with modern systems achieving up to 99% removal efficiency for dissolved salts, heavy metals, and microbial contaminants. Ultrafiltration (UF) membranes with pore sizes as small as 0.01 microns are increasingly used in low-pressure systems, improving water flow rates by nearly 30% compared to conventional designs. UV purification technology has also advanced, with dual-lamp systems improving microbial inactivation efficiency by over 95%, particularly in municipal and residential applications.

A major technological shift is the integration of IoT-enabled smart purifiers, where over 45% of newly launched systems now feature real-time water quality tracking, filter life alerts, and automated maintenance notifications. AI-based diagnostic systems are also being adopted, enabling predictive maintenance that reduces operational downtime by approximately 25%. In addition, nanotechnology-based filtration membranes are gaining traction, improving contaminant removal efficiency by up to 40% while extending filter lifespan by nearly 50%.

Energy-efficient purification systems are another key innovation, with modern RO units reducing water wastage ratios from traditional 50% levels to nearly 25%. Hybrid systems combining RO, UV, and UF technologies are increasingly preferred, accounting for over 35% of premium installations. Material innovation is also reshaping the market, with graphene-based filters and anti-bacterial coatings improving durability and reducing microbial growth by more than 60%.

Smart connectivity is further enhancing user experience, with mobile-integrated platforms enabling remote monitoring adoption in over 60% of urban installations. These technological advancements collectively support higher efficiency, sustainability, and user convenience, making next-generation water purifiers a critical component of modern water management systems.

• In March 2025, A.O. Smith Corporation expanded its smart water purifier portfolio with upgraded IoT-enabled residential systems designed for real-time water quality monitoring and filter replacement alerts. The new models are integrated with advanced multi-stage filtration technology to enhance contaminant removal efficiency and improve user maintenance experience.

• In September 2024, Kent RO Systems Ltd. introduced an enhanced range of reverse osmosis purifiers featuring advanced mineral retention technology aimed at improving drinking water taste and nutritional balance. The company also strengthened its service network across urban and semi-urban regions to improve product accessibility and maintenance efficiency.

• In July 2025, Eureka Forbes Limited launched a new generation of Aquaguard smart purifiers with UV-LED sterilization and connected mobile app functionality. The system enables real-time monitoring of water quality parameters and enhances energy efficiency through automated operational control features designed for residential users.

• In November 2024, LG Electronics expanded its premium water purifier lineup featuring ThinQ-enabled smart diagnostics and multi-layer filtration systems. The product line focuses on improving water safety consistency and integrates digital controls that allow remote monitoring, reflecting increasing demand for connected home water solutions.

The water purifiers market report covers a comprehensive analysis of multiple dimensions influencing global demand, technological evolution, and application expansion. The scope includes segmentation by product types such as reverse osmosis (RO), ultraviolet (UV), ultrafiltration (UF), gravity-based systems, and hybrid purification technologies. Each segment is evaluated based on adoption trends, performance efficiency, and technological advancements across residential, commercial, and industrial applications. Geographically, the report spans major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, collectively accounting for 100% of global market distribution. Asia-Pacific dominates volume consumption with over 45% share of installations, while North America and Europe collectively represent more than 40% of demand driven by technological adoption and regulatory compliance. Emerging regions are witnessing increasing penetration due to infrastructure development and water quality improvement initiatives.

The application scope includes household drinking water systems, healthcare facilities, food and beverage processing, pharmaceuticals, hospitality, and institutional usage. Residential applications account for nearly 60% of total demand, while industrial and commercial segments contribute the remaining 40%, reflecting diversified usage patterns across sectors. Technological coverage includes IoT-enabled purification systems, AI-based monitoring platforms, nanotechnology filtration, energy-efficient RO systems, and hybrid multi-stage purification units. The report also evaluates material innovations such as graphene membranes and anti-microbial coatings that enhance system durability and efficiency.

Additionally, the scope incorporates analysis of regulatory frameworks, sustainability initiatives, and ESG compliance requirements influencing product development and adoption. It also examines emerging niche markets such as portable purifiers, solar-powered systems, and decentralized water treatment units, highlighting evolving consumer preferences and long-term industry transformation trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

A.O. Smith Corporation, Kent RO Systems Ltd., Eureka Forbes Ltd., Panasonic Corporation, LG Electronics Inc., Unilever PLC, Coway Co., Ltd., Amway Corporation, Culligan International Company, 3M Company, Brita GmbH, Tata Chemicals Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |