Reports

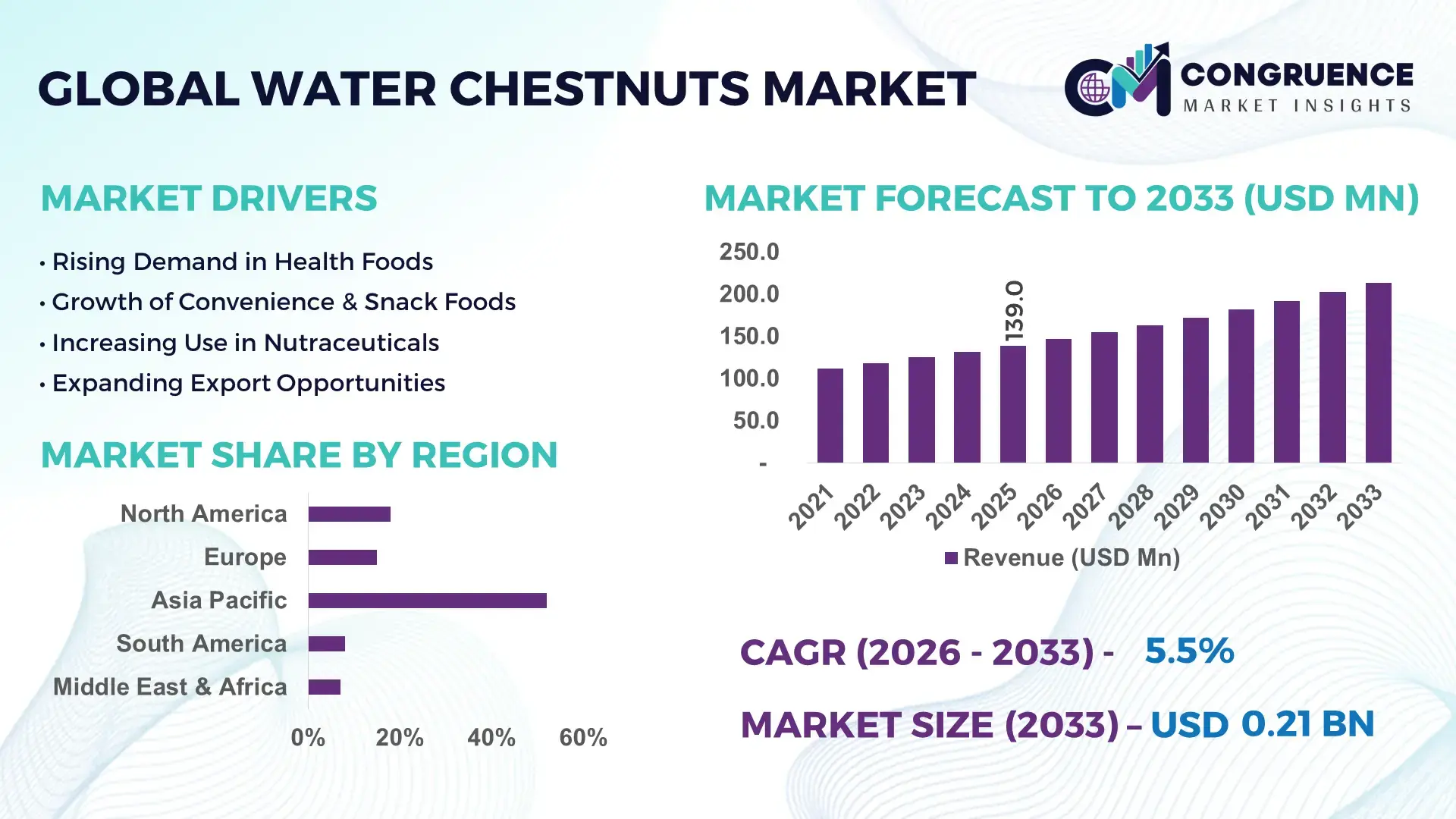

The Global Water Chestnuts Market was valued at USD 139.0 Million in 2025 and is anticipated to reach a value of USD 213.3 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Market expansion is driven by rising consumer preference for natural, gluten-free, and nutritious ingredients across food, beverage, cosmetic, and pharmaceutical applications.

China is the dominant producer of water chestnuts, with advanced cultivation systems and mechanized harvesting supporting global supply. The country produces over 35% of global output, with significant investments in irrigation infrastructure and processing facilities capable of handling both fresh and processed products. Consumer adoption is high, with approximately 60% of processed water chestnut products distributed through modern retail and e-commerce channels, and ongoing R&D focuses on product quality improvements and post-harvest technologies.

Market Size & Growth: 2025 market ~USD 139.0 Million; 2033 projected ~USD 213.3 Million; growth driven by rising health awareness and functional food demand.

Top Growth Drivers: Consumer health adoption ~42%, plant-based diet penetration ~33%, functional food applications ~28%.

Short-Term Forecast: By 2028, processing efficiency expected to improve supply chain lead time by ~18%.

Emerging Technologies: Advanced sorting automation, vacuum packaging systems, aseptic processing integration.

Regional Leaders: Asia Pacific ~USD 120 Million by 2033 (rapid urban consumption); North America ~USD 45 Million (ethnic food adoption); Europe ~USD 38 Million (healthy ingredient trend).

Consumer/End-User Trends: Growth in foodservice menus, increased home cooking usage, snack innovation.

Pilot or Case Example: 2025 pilot in East China reduced processing waste by ~22% through AI-based quality grading.

Competitive Landscape: Leading player ~21% presence, followed by 4–5 major firms focusing on product portfolios and export networks.

Regulatory & ESG Impact: Strengthened food safety standards and enhanced agricultural sustainability initiatives.

Investment & Funding Patterns: Rising private investments in processing technology and venture funding in product diversification.

Innovation & Future Outlook: Expansion of value-added product lines and digital traceability adoption.

Water Chestnuts Market activity spans food & beverages, pharmaceuticals, and personal care sectors. Innovations such as powdered and ready-to-eat formats are increasing traction, while sustainable sourcing, urban consumption patterns, and regulatory drivers are shaping future growth opportunities.

The Water Chestnuts Market is strategically relevant as both a traditional food ingredient and a functional commodity leveraged across multiple industry sectors. Its importance is evident in measurable consumer adoption, reflected in increasing incorporation into health-oriented food products, beverages, and nutraceuticals. For example, advanced cold-chain processing delivers 15% improvement in shelf life performance compared to conventional processing standards, enhancing market competitiveness.

Regionally, Asia Pacific dominates in production volume, while North America leads in adoption with ~48% of enterprises integrating water chestnut products into their portfolios. By 2028, automation and AI-assisted quality sorting are expected to reduce operational inefficiencies by ~20%, further strengthening market positioning. ESG commitments are central, with firms targeting a 25% reduction in water usage and waste by 2030, aligning with sustainability objectives.

Micro scenarios highlight the impact of technological adoption: in 2025, a processing facility in China achieved a 30% reduction in energy consumption through IoT-enabled drying and automated handling technologies. Forward-looking strategies emphasize resilience, compliance, and sustainable growth, positioning the Water Chestnuts Market as a key contributor to global functional food and ingredient ecosystems.

The Water Chestnuts Market is shaped by consumer health trends, technological advancements, and regulatory focus on sustainable agriculture. Rising health consciousness has boosted demand in food and beverage applications, while plant-based diet adoption continues to expand water chestnut usage. Innovations in automated processing enhance quality and reduce post-harvest losses, improving competitiveness in both fresh and processed segments. Evolving distribution channels, especially online retail, are increasing accessibility and broadening the consumer base. Regulatory emphasis on food safety and eco-friendly practices further encourages investment in cultivation infrastructure, cementing water chestnuts as a multifunctional and adaptable market with growth potential.

Rising global focus on nutrition and plant-based diets has significantly influenced water chestnuts demand. Recognized for high fiber and antioxidants, water chestnuts are increasingly used in salad mixes, gluten-free foods, and functional snacks. Urban consumers are adopting pre-sliced and ready-to-cook variants in supermarkets and online platforms, increasing measurable engagement. Food manufacturers are integrating water chestnuts into mainstream retail products, creating new opportunities for market penetration while responding to health and wellness trends.

Water chestnuts require flooded fields and controlled cultivation environments, making production sensitive to climatic variation. Labor-intensive harvesting increases operational costs, and inadequate cold chain infrastructure in some regions causes spoilage and distribution challenges. These factors limit scalability and affect supply predictability, constraining growth for processors and exporters. Addressing these restraints requires continued investment in irrigation systems, mechanization, and processing technologies to ensure consistent quality and timely delivery to markets.

Functional food market expansion opens new avenues for water chestnut applications beyond traditional culinary use. Derivatives like flour, extracts, and ready-to-eat snacks are increasingly incorporated into gluten-free and plant-based product lines, offering texture, fiber, and clean-label benefits. Personal care and nutraceutical brands are exploring water chestnut antioxidant properties, while cross-regional partnerships support global market expansion. These developments create untapped revenue streams and increase market visibility in emerging sectors.

Fresh water chestnuts have a limited shelf life, requiring advanced cold storage and transportation, which raises costs. Diverse regulatory requirements complicate international trade, and maintaining consistent quality for processed forms demands investment in modern processing and food safety systems. These factors challenge smaller producers and affect profitability, emphasizing the need for standardized quality protocols, improved logistics, and infrastructure to ensure market reliability and competitiveness.

Growing Functional Ingredient Integration: Water chestnut derivatives in gluten-free and plant-based products have risen by over 40% in new product launches, reflecting strong consumer preference for natural ingredients.

Accelerated E-Commerce Channels: Online sales for water chestnut products have surged by 28% year-on-year, driven by urban digital adoption and expanded product visibility.

Processing Technology Adoption: Automated sorting and packaging reduces post-harvest losses by 15–20%, enhancing shelf stability for both fresh and processed products, particularly in major production hubs.

Premium Snack Innovation: Ready-to-eat and snack formats have grown by ~35% in penetration within health snack segments, catering to consumers seeking alternatives to traditional high-calorie snacks and creating high-value market niches.

The Water Chestnuts Market is segmented comprehensively to reflect diverse product forms, practical uses, and a broad range of end‑user scenarios. For product type, offerings include fresh, dried, flour, powder, frozen, organic, conventional, packaged, and processed formats that support different supply chains and consumer preferences, from perishable fresh corms to long‑lasting processed formats for retail and foodservice distribution. In terms of applications, water chestnuts serve food processing, traditional dishes, snacks, flour products, nutraceuticals, exports, and retail products, illustrating their versatility from kitchen staples to functional ingredient uses. Distribution channels span supermarkets/hypermarkets, convenience stores, online retail, and specialty outlets, ensuring widespread market reach. Finally, end‑users include household consumers, food service establishments, and industrial processors, with households typically leading usage for culinary purposes and processors leveraging water chestnut derivatives for value‑added foods, cosmetics, and pharmaceutical products. These segments together reflect a dynamic market where versatile consumption patterns and expanding product innovations drive ongoing strategic planning.

The Water Chestnuts Market product type landscape comprises fresh water chestnuts, processed variants (canned, frozen, dried), flour, powder, organic, and conventional forms. Fresh water chestnuts currently account for approximately 38% of overall product adoption, while processed canned and frozen forms hold around 32%. Flour and powder variants together contribute about 20%, and organic plus specialty formats represent the remaining 10%. Fresh water chestnuts lead due to their superior texture, natural nutritional profile, and direct culinary use in salads, stir‑fries, and traditional dishes, appealing to both household and high‑end foodservice segments. Processed variants are valued for convenience and extended shelf life, particularly in retail and food service applications, where ready‑to‑use products are preferred. Flour and powder formats are essential in bakery, gluten‑free, and specialty food sectors due to their functional properties. Other niche types, such as organic and bulk packaged water chestnut products, cater to specific consumer segments focused on health and sustainability.

Water chestnuts are applied across food & beverages, pharmaceuticals, cosmetics & personal care, and other niche sectors. Food & beverages currently hold around 55% of usage, with food processing and traditional cuisines being central, while pharmaceuticals and personal care applications account for approximately 22% and 13%, and other applications make up about 10%. The food & beverage segment is dominant due to widespread culinary use of fresh and processed water chestnuts in salads, stir‑fries, soups, snacks, and functional drink formulations, driven by their crunchy texture and nutritional benefits. Pharmaceuticals use water chestnut extracts in supplements and health‑oriented products, aligning with consumer interest in natural health solutions. The cosmetics & personal care segment is adopting water chestnut‑derived antioxidants and hydrating compounds in skincare creams and masks.

Consumer adoption & trend statistics: In 2025, more than 42% of food service providers globally reported increasing integration of water chestnuts in menu offerings to meet health‑oriented customer preferences.

End‑user segmentation includes household, food service, and industrial categories. Household consumers represent approximately 47% of end‑user adoption, food service accounts for around 30%, and industrial processors contribute about 23%. Households lead due to routine culinary use of fresh and ready‑to‑cook water chestnuts in everyday meals and traditional dishes. Food service segments, including restaurants, hotels, and catering providers, are significant users of both fresh and processed forms, leveraging water chestnuts for menu differentiation and nutrition‑focused offerings. Industrial end‑users encompass food manufacturers, cosmetic formulators, and pharmaceutical producers who utilize water chestnut derivatives for product innovation and functionality.

Consumer adoption & trend statistics: In 2025, over 36% of urban households increased water chestnut purchasing driven by health and texture preferences in home cooking.

Asia-Pacific accounted for the largest market share at 52% in 2025, however, North America is expected to register the fastest growth, expanding at a CAGR of 6% between 2026 and 2033.

Asia-Pacific’s dominance stems from large-scale cultivation in China, India, and Japan, contributing over 500,000 metric tons annually, supported by modern irrigation systems and mechanized harvesting. North America, while holding 18% market share, benefits from increasing adoption in health-oriented food products, processed snacks, and functional beverages. Europe accounts for 15%, led by Germany, UK, and France, with strong regulatory focus on sustainability. South America holds 8%, driven by Brazil and Argentina, and the Middle East & Africa represent 7%, with UAE and South Africa expanding niche food ingredient applications. Regional infrastructure, e-commerce penetration, and technology adoption contribute to measurable consumer and industrial adoption trends across all markets.

North America accounts for approximately 18% of the global Water Chestnuts Market. Key industries driving demand include foodservice, health foods, and functional beverages, with increasing incorporation in gluten-free and plant-based products. Regulatory updates promoting food safety and organic labeling have boosted adoption in retail and online channels. Technological advancements such as automated sorting and AI-enabled quality assessment are improving processing efficiency. Local players like Sunrise Foods have launched pre-sliced and frozen water chestnut products, reducing preparation time by 20% for restaurant chains. Consumer behavior shows higher enterprise adoption in healthcare and foodservice, with growing preference for convenient, healthy ingredients and e-commerce-enabled product delivery.

Europe holds around 15% of the global Water Chestnuts Market, with Germany, the UK, and France as the top contributors. Regulatory initiatives promoting sustainable agriculture and food safety have strengthened compliance and increased market credibility. Emerging technologies such as automated sorting, vacuum packaging, and IoT-enabled supply chain monitoring are widely adopted. Local players like Delica AG focus on providing frozen and packaged water chestnut products for retail and industrial customers. Consumer behavior varies, with urban households preferring processed and ready-to-cook formats, while foodservice emphasizes premium and organic products.

Asia-Pacific dominates with 52% of global market volume, primarily driven by China, India, and Japan. Manufacturing infrastructure includes large-scale mechanized harvesting, automated processing plants, and cold storage facilities. Technology adoption, including AI-enabled grading and IoT monitoring, supports high-quality production standards. Local players such as Yangcheng Lake Produce Ltd. supply fresh and frozen products to domestic and international markets. Consumer behavior is influenced by rapid e-commerce adoption, urbanization, and increasing demand for ready-to-eat and functional food products, which further strengthens the region’s market leadership.

South America contributes 8% of the global Water Chestnuts Market, with Brazil and Argentina leading. Infrastructure improvements, such as enhanced cold storage and distribution networks, support broader market penetration. Government incentives and trade policies promoting agricultural exports facilitate growth. Local players like Amazon Fresh Foods provide frozen and packaged water chestnuts to retail and foodservice clients. Consumer behavior is influenced by media-driven awareness campaigns and cultural culinary trends, encouraging adoption of novel ingredients and processed formats in urban areas.

The Middle East & Africa account for 7% of the global Water Chestnuts Market, with UAE and South Africa as major growth hubs. Demand is driven by the foodservice, retail, and specialty food segments. Technological modernization, including automated processing lines and quality monitoring systems, improves supply reliability. Local players such as Desert Foods Ltd. provide imported and locally packaged water chestnut products to premium supermarkets. Regional consumer behavior reflects preference for health-oriented and convenient products, with growth further supported by trade partnerships and government programs promoting food diversification.

China – 35% Market Share: Dominant due to high production capacity and mechanized farming infrastructure.

India – 18% Market Share: Strong end-user demand in food processing and traditional culinary applications.

The competitive environment in the Water Chestnuts Market is moderately fragmented, with a mix of global exporters, regional processors, and niche innovators operating across fresh, processed, and value‑added formats. There are dozens of active competitors, but the combined share of the top 5 companies is estimated around 28–32%, indicating that no single player dominates outright and competition remains diversified. Key strategic initiatives include capacity expansion, acquisitions, and partnerships aimed at securing supply chains and broadening product portfolios. For example, acquisition activities have been used to consolidate production capabilities and absorb smaller processors, while strategic alliances are enabling joint commercialization of new water chestnut ingredients for innovative snack and beverage applications. Innovation trends show increased focus on advanced processing technologies such as automated cleaning, slicing, drying, and packaging systems that enhance product freshness and shelf life. Companies are also investing in clean‑label and organic product lines, responding to rising consumer preferences for natural, minimally processed food ingredients. Export diversification strategies further strengthen competitive positioning, with leading firms penetrating North American and European retail channels. Overall, the Water Chestnuts Market competitive landscape reflects dynamic positioning, investment in quality, and ongoing product development to capture emerging consumer and industrial demand.

Bharat Agro Overseas

Linyi City Kangfa Foodstuff Drinkable Co., Ltd.

Shanghai Xiangyi International Trade Co., Ltd.

Qingdao Hualitai Food Co., Ltd.

Guangxi Hengxian Xianggui Water Chestnut Food Co., Ltd.

Guangxi Yulin Oriental Food Co., Ltd.

Guangxi Nanning Taoyuan Preserved Fruit Co., Ltd.

Guangxi Yulin Hongjie Agricultural Development Co., Ltd.

Lakeside Food Sales, Inc.

Natureland Organics

Technology is playing an increasingly pivotal role in the Water Chestnuts Market, enhancing quality, processing efficiency, traceability, and product diversification. Current technologies focus heavily on automation in sorting, slicing, and packaging, which improves throughput and reduces manual labor dependency, particularly in large processing facilities. Cold chain and refrigeration systems ensure minimal quality degradation for fresh and canned formats, extending product availability throughout the year. Advanced IoT (Internet of Things) sensors and data analytics are being used to monitor environmental conditions during storage and transport, bolstering quality assurance and compliance with stringent food safety standards. In processing segments such as flour and powder, technologies like vacuum drying, freeze‑drying, and micronization are enabling producers to maintain nutritional integrity while creating new functional ingredient formats. Emerging digital solutions, including blockchain traceability platforms, are beginning to see adoption for end‑to‑end transparency—from source fields through distribution channels—addressing consumer demand for verified sourcing and sustainability credentials. Breeding and agritech innovations are also influencing upstream supply, with research into varieties that yield higher starch content and improved resilience to environmental stress. These technological advancements collectively support product consistency, extended shelf life, and alignment with evolving regulatory and consumer expectations, positioning the market for resilient growth.

• In December 2025, Amoytop Foods announced the official start of its new canned water chestnut production season, reporting the rollout of whole, sliced, and diced canned water chestnut products in multiple tin sizes designed for household and foodservice customers worldwide. Source: www.amoytopfoods.com

• In March 2025, Amoytop Foods reported ongoing rises in raw material costs for water chestnuts, citing price increases of up to 18% in regional procurement areas such as Lechang, Guangdong, and noting the impact on processing and sourcing strategies for canned products. Source: www.amoytopfoods.com

• Throughout 2025, Amoytop Foods maintained communications about increasing raw material availability and production season signals for canned water chestnuts, indicating gradual increases in fresh input supply as the growing season advanced, suggesting stronger production throughput in late 2025. Source: www.amoytopfoods.com

• In November 2024, Zhejiang Hengyi Agricultural Development Co formed a strategic partnership with Zhejiang Jiabao Food Co to jointly develop and commercialize water chestnut powder ingredients for ready‑to‑eat snacks, driving product innovation and market reach.

The Water Chestnuts Market Report offers a comprehensive assessment of market segments, technologies, regional landscapes, and industry focus areas to support strategic decision‑making. It encompasses detailed analysis of product types (fresh, processed, flour, powder, organic/conventional) and application areas including food & beverages, nutraceuticals, cosmetics, and other niche uses. Geographic coverage spans Asia‑Pacific, North America, Europe, South America, and Middle East & Africa, with insights into consumption patterns, infrastructure trends, and distribution channel dynamics. The report examines end‑user segments such as households, food service, and industrial processors, highlighting variations in adoption behaviors and regional consumer preferences. It also addresses technological influences, from processing automation and cold‑chain logistics to digital traceability and quality monitoring systems, offering professionals a nuanced view of competitive and operational environments. Emerging and niche segments, such as value‑added formulations (e.g., water chestnut powder for functional foods), are explored to demonstrate innovation pathways and investment opportunities. With its formal, business‑oriented structure and extensive numerical insights into segmentation and regional activities, the report serves analysts and executives seeking to navigate market complexities and identify growth levers across global and regional contexts.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 139.0 Million |

| Market Revenue (2033) | USD 213.3 Million |

| CAGR (2026–2033) | 5.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | Qingdao Dongsheng Foodstuffs Co., Ltd.,Fujian Lixing Foods Co., Ltd.,Amoytop Foods,Bharat Agro Overseas,Linyi City Kangfa Foodstuff Drinkable Co., Ltd.,Shanghai Xiangyi International Trade Co., Ltd.,Qingdao Hualitai Food Co., Ltd.,Guangxi Hengxian Xianggui Water Chestnut Food Co., Ltd.,Guangxi Yulin Oriental Food Co., Ltd.,Guangxi Nanning Taoyuan Preserved Fruit Co., Ltd.,Guangxi Yulin Hongjie Agricultural Development Co., Ltd.,Lakeside Food Sales, Inc.,The Raw Food World,Natureland Organics |

| Customization & Pricing | Available on Request (10% Customization Free) |