Reports

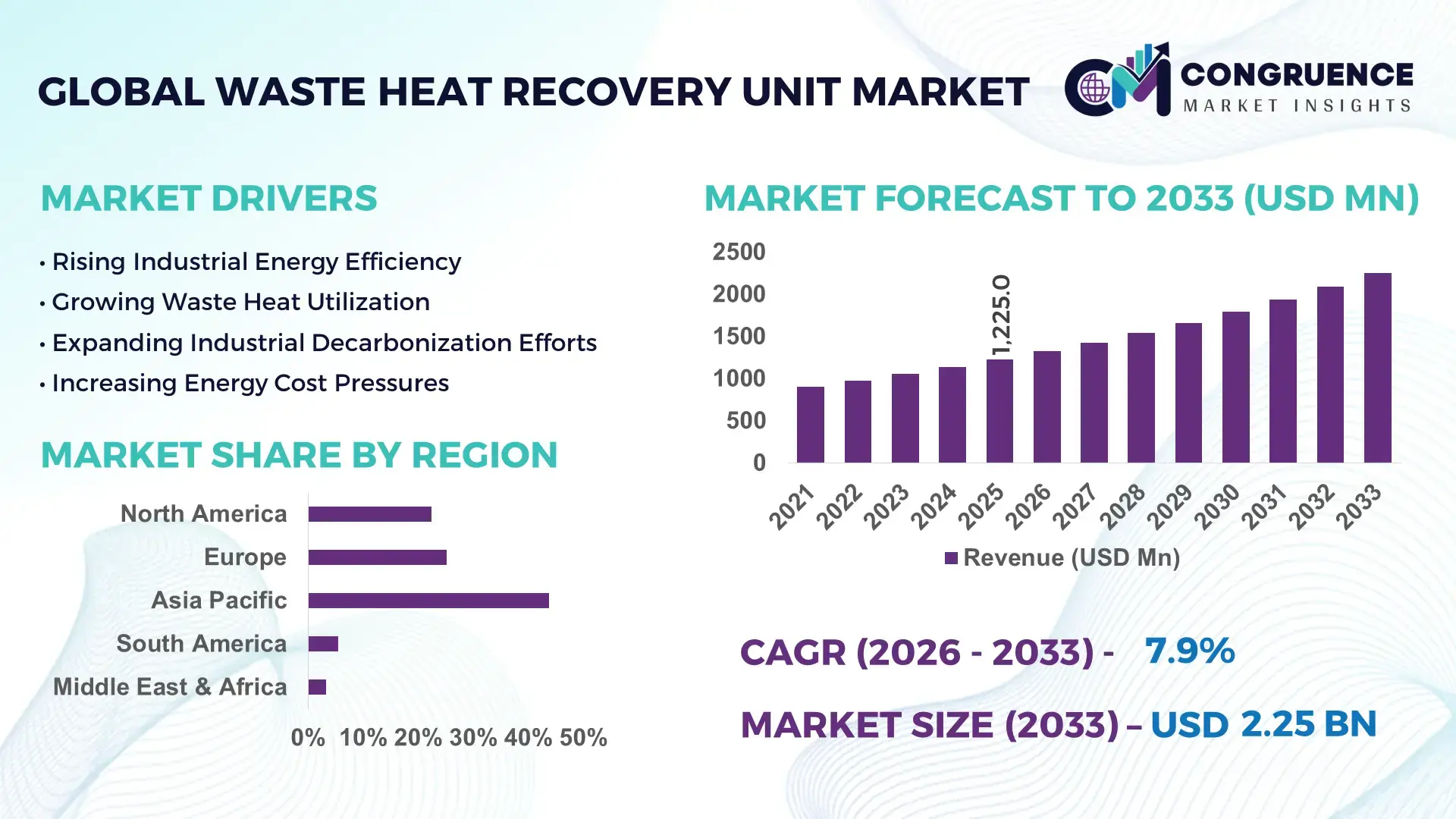

The Global Waste Heat Recovery Unit Market was valued at USD 1,225.0 Million in 2025 and is anticipated to reach a value of USD 2,250.6 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Rising industrial decarbonization mandates across cement and steel plants are accelerating deployment of high-efficiency WHRU systems, with energy recovery efficiency improvements reaching 18–24% in upgraded installations.

China dominates with ~34% share of installed WHRU capacity, driven by over 1,200 large-scale steel and cement facilities, while India’s adoption has surged by 22% YoY supported by National PAT cycle enforcement. Germany leads Europe with over €3.2 billion in industrial retrofit investments, outperforming France by nearly 9% in deployment intensity. The geopolitical shift toward energy security post-Russia–EU supply disruption has further strengthened EU retrofit demand.

Strategically, manufacturers prioritizing Asia–Europe supply chain localization and modular WHRU designs are capturing faster industrial retrofit contracts.

Market Size & Growth: USD 1,225.0M → USD 2,250.6M, 7.9%, driven by industrial energy efficiency mandates

Top Growth Drivers: Energy cost reduction 28%, emission compliance 41%, industrial expansion 19%

Short-Term Forecast: By 2028, fuel consumption efficiency improves 15% in retrofitted plants

Emerging Technologies: AI-based thermal optimization, organic Rankine cycle systems, advanced heat exchangers

Regional Leaders: Asia-Pacific USD 610M (rapid industrialization), Europe USD 320M (retrofit adoption), North America USD 260M (clean energy transition)

Consumer/End-User Trends: 52% of heavy industries integrating WHRU in new plant design cycles

Pilot/Case Example: 2024 India steel plant achieved 21% energy loss reduction via WHRU integration

Competitive Landscape: Leader holds ~12% share; key players include Siemens Energy, ABB, Mitsubishi Heavy Industries, General Electric, Thermax

Regulatory & ESG Impact: Emission compliance improved by 30% in regulated industries adopting WHRU systems

Investment & Funding: USD 3.8B global investments driven by EPC partnerships and industrial decarbonization programs

Innovation & Future Outlook: Shift toward hybrid WHRU–renewable systems enabling 25% operational efficiency gains

Waste heat recovery units are witnessing rising demand in steel, cement, and petrochemical sectors, where 60–70% of thermal energy is typically lost. Digital monitoring adoption has increased efficiency optimization by 14% across pilot plants. Europe’s retrofit push and India’s industrial electrification policies are creating parallel demand acceleration. A 19% increase in modular WHRU adoption highlights shift toward scalable deployment models, reinforcing long-term industrial energy circularity trends.

The market is becoming strategically critical as industries transition toward low-carbon production systems and energy self-sufficiency models. Regulatory tightening across the EU ETS framework and Asia’s industrial efficiency mandates is forcing manufacturers to integrate WHRU systems into core infrastructure planning, reshaping capital allocation strategies across heavy industries.

Technologically, modern WHRU systems deliver up to 22% higher thermal conversion efficiency compared to conventional recovery units, reducing operational energy costs significantly. Germany and Japan lead in high-precision deployment, while India and China scale volume-based installations across steel clusters and cement corridors. This regional divergence is shaping differentiated investment priorities between high-tech efficiency and mass industrial retrofitting.

In the next 2–3 years, over 35% of new industrial projects are expected to include WHRU integration at the design stage. A cement facility in Tamil Nadu demonstrated 18% reduction in grid dependency through WHRU coupling with captive power systems. Companies are increasingly forming EPC–technology partnerships to secure lifecycle efficiency advantages. Strategically, WHRU adoption is becoming a core competitive lever for energy-intensive industries aiming to stabilize margins amid volatile fuel markets.

Global decarbonization policies are accelerating WHRU deployment, with industrial energy efficiency mandates improving adoption rates by nearly 38% in regulated sectors. Steel and cement industries account for over 55% of total installations, driven by fuel cost optimization pressures. China’s industrial emission caps and India’s PAT compliance system are key regulatory triggers pushing adoption. Energy cost volatility, rising by 27% in key manufacturing hubs, is forcing firms to invest in recovery systems that improve thermal efficiency by 20–25%. Companies like Mitsubishi Heavy Industries and Siemens Energy are expanding modular WHRU portfolios to address retrofit demand across Asia and Europe. EPC collaborations are rising by 31%, reflecting rapid infrastructure modernization.A notable shift is the integration of WHRU systems into hybrid energy setups, enabling factories to reduce external energy dependency while improving operational resilience.

High upfront installation costs, accounting for nearly 30–35% of total project expenditure, remain a major barrier for small and mid-sized industries. In emerging economies, financing constraints reduce adoption feasibility by 18–22%, particularly in fragmented manufacturing clusters.Integration complexity with legacy industrial systems increases downtime risk by 15%, impacting production continuity. Supply chain disruptions in heat exchanger components have also caused procurement delays of up to 12 weeks in certain European retrofit projects. Companies in the US and Germany are addressing this through standardized modular WHRU designs and vendor financing models. To mitigate risks, industrial players are increasingly adopting phased implementation strategies and long-term EPC contracts to spread capital burden while ensuring operational continuity.

The integration of AI-based thermal analytics is improving energy recovery efficiency by 17–20%, unlocking new optimization opportunities across heavy industries. Emerging hybrid systems combining WHRU with solar thermal and waste-to-energy setups are gaining traction, particularly in Japan and South Korea. Over 40% of new industrial plants in China are evaluating digital WHRU integration models to enhance predictive maintenance and reduce downtime. Government-backed clean energy incentives in India are also accelerating deployment in industrial corridors. Companies are expanding R&D investment by 25% in advanced heat exchanger materials and smart control systems. Strategic partnerships between energy tech firms and EPC contractors are enabling scalable deployment models that reduce installation time by up to 15%, unlocking underserved mid-tier industrial markets.

Complex integration with aging industrial infrastructure remains a critical challenge, with compatibility issues affecting nearly 28% of retrofit projects globally. Variability in plant design standards across countries such as Brazil, India, and Eastern Europe increases engineering customization requirements by 20%. Cyber-physical system integration risks are rising, with digital WHRU systems introducing 14% higher operational complexity in monitoring and control layers. Workforce skill gaps in advanced thermal engineering further delay commissioning timelines by 10–12%. Companies are responding by investing in standardized digital twin platforms and workforce upskilling programs. EPC firms are increasingly adopting pre-engineered WHRU modules to reduce installation variability and ensure consistent performance across diverse industrial environments.

AI-Enabled Thermal Optimization Expansion Industrial operators are increasingly deploying AI-driven monitoring platforms that improve heat recovery efficiency by 12–18% while reducing unplanned downtime by nearly 20%. Steel and cement facilities in China and India are integrating predictive analytics directly into WHRU workflows, enabling faster thermal balancing and asset utilization. Companies are responding through automation partnerships and digital retrofit programs that shorten maintenance cycles and improve operational visibility across multi-site facilities.

Shift Toward Modular Deployment Models Modular WHRU systems now account for approximately 35% of new industrial installations, driven by faster commissioning timelines and lower site-engineering requirements. Deployment periods have declined by nearly 25%, while installation-related disruptions have fallen by 15%. Rising labor shortages in industrial engineering have accelerated demand for pre-engineered solutions. Manufacturers are expanding standardized product portfolios and regional assembly capabilities to improve delivery speed and reduce customization bottlenecks.

Industrial Retrofit Activity Accelerates More than 45% of large industrial energy-efficiency projects now prioritize retrofitting existing facilities rather than greenfield development. Cement and petrochemical operators are reporting thermal loss reductions exceeding 20% after modernization initiatives. Energy-security concerns and stricter emissions compliance requirements are driving investment decisions. Companies are restructuring service networks, expanding EPC partnerships, and introducing lifecycle support contracts to improve retrofit adoption rates.

Advanced Heat Exchanger Adoption Rising Next-generation heat exchangers utilizing enhanced surface materials have improved thermal transfer performance by 10–16% while reducing maintenance frequency by nearly 14%. Industrial users are increasingly prioritizing compact designs that optimize space utilization and process integration. Suppliers are investing in advanced manufacturing techniques and strategic material sourcing programs, creating a competitive advantage through higher durability, improved efficiency, and reduced operational interruption.

Organic Rankine Cycle (ORC) systems represent the leading segment, accounting for approximately 42% of global deployments due to their ability to recover low- and medium-temperature waste heat efficiently. Their scalability, flexible integration, and suitability across cement, glass, chemicals, and manufacturing facilities support widespread adoption. Industrial operators favor ORC technology because it can improve energy utilization by 15–25% without requiring major process redesign. Companies continue expanding ORC portfolios through efficiency-focused product enhancements and turnkey deployment models. Kalina Cycle systems are emerging as the fastest-growing segment, supported by superior performance in variable-temperature industrial environments and efficiency gains reaching 10–20% over conventional recovery technologies in selected applications. Steam Rankine Cycle systems maintain strong positions in large-scale steel and power facilities where high-temperature heat streams remain abundant. Direct heat exchange systems continue serving cost-sensitive industrial users seeking lower capital requirements and simplified installation. Investment priorities are gradually shifting toward advanced working-fluid technologies, digital controls, and hybrid thermal recovery platforms that maximize operational flexibility.

Power generation represents the largest application segment, contributing nearly 38% of market demand as industrial facilities increasingly convert waste heat into usable electricity. Energy-intensive industries are prioritizing onsite power generation to reduce grid dependency and improve energy resilience. Advanced WHRU installations are enabling electricity recovery improvements of 15–22%, strengthening adoption across steel, refining, and chemical processing operations. Companies continue scaling integrated energy-management strategies to maximize operational efficiency and stabilize production costs. The cement industry is the fastest-growing application segment due to high kiln exhaust temperatures and expanding decarbonization initiatives. Adoption rates within modern cement facilities have increased by more than 20% over recent years as operators seek reductions in fuel consumption and emissions intensity. The petroleum refining sector maintains substantial demand through process optimization initiatives, while metal production facilities increasingly deploy recovery systems to capture thermal losses from furnaces and smelting operations. Across applications, automation-enabled monitoring and thermal analytics are becoming critical deployment requirements.

The industrial manufacturing sector remains the largest end-user group, accounting for approximately 46% of total demand due to extensive thermal energy losses across steel, chemicals, cement, glass, and processing operations. High operating temperatures and continuous production cycles create favorable economics for heat recovery investments. Many large manufacturers are achieving energy savings of 15–25% through integrated recovery systems, strengthening adoption across both retrofit and new-build facilities. Suppliers are responding with industry-specific system designs and performance-guarantee service models. The energy and utilities sector is emerging as the fastest-growing end-user segment as operators modernize generation assets and improve overall thermal efficiency. Utilities are increasingly incorporating waste heat recovery into infrastructure upgrade programs, with deployment activity rising by nearly 18% in efficiency-focused projects. Commercial infrastructure users are gradually adopting smaller-scale systems for district energy applications, while mining and metals companies continue investing in high-capacity recovery solutions. Vendors are expanding strategic partnerships, customized engineering capabilities, and digital monitoring platforms to strengthen competitive positioning across diverse end-user requirements.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.8% between 2026 and 2033.

North America represented approximately 22.4% of global market activity in 2025, supported by strong deployment across steel, refining, chemicals, and power generation facilities. Industrial operators are prioritizing waste heat utilization to offset energy price volatility and strengthen operational efficiency. The region continues to lead in digitalized heat recovery integration, with more than 40% of newly deployed systems incorporating advanced monitoring and predictive maintenance capabilities. Infrastructure modernization programs and manufacturing reshoring initiatives are creating additional demand for thermal optimization technologies. Several large industrial facilities have reported energy consumption reductions exceeding 15% following WHRU implementation, reinforcing the business case for large-scale retrofits and efficiency-focused capital expenditure.

United States Market Outlook: The United States dominates regional demand due to its extensive industrial base, mature energy infrastructure, and strong adoption of efficiency-focused technologies. Steel manufacturing, petrochemicals, and refining facilities remain key deployment centers. More than 55% of regional industrial heat recovery projects are concentrated in the U.S., supported by growing investment in advanced manufacturing and emissions reduction initiatives. Companies are increasingly integrating digital energy management platforms with waste heat recovery systems to optimize plant-wide energy performance and improve operational resilience.

Europe accounted for nearly 25.1% of the global market in 2025, supported by stringent industrial efficiency regulations and widespread decarbonization initiatives. Heavy industries are increasingly retrofitting existing facilities with advanced thermal recovery systems to improve energy productivity and reduce operational waste. The region has become a major hub for high-efficiency heat exchanger technologies and advanced Organic Rankine Cycle deployments. More than 45% of large industrial energy-efficiency projects now evaluate waste heat recovery integration during modernization planning. Manufacturers are emphasizing low-carbon production strategies, while engineering firms continue expanding turnkey solutions that combine automation, monitoring, and thermal optimization capabilities.

Germany Market Outlook: Germany remains the strategic center of the European market due to its strong engineering ecosystem, advanced manufacturing sector, and industrial modernization agenda. The country hosts a significant concentration of steel, chemicals, and industrial processing facilities where thermal efficiency improvements remain a top priority. Industrial operators have increased investment in energy recovery technologies by more than 20% over recent years, while advanced automation integration is improving system performance and operational transparency across large-scale facilities.

Asia-Pacific led the global market with approximately 43.8% share in 2025, supported by rapid industrialization, extensive manufacturing activity, and expanding infrastructure development. The region hosts the world's largest concentration of cement, steel, chemicals, and power generation facilities, creating substantial thermal recovery opportunities. Industrial energy-efficiency programs continue driving deployment, while manufacturers increasingly integrate WHRU systems into both new-build and retrofit projects. More than 50% of newly commissioned heavy industrial facilities in key manufacturing economies evaluate heat recovery technologies during project planning. Growing demand for energy security and operational efficiency is strengthening adoption across industrial clusters.

China Market Outlook: China represents the largest country-level market globally, supported by its extensive steel, cement, petrochemical, and manufacturing sectors. The country accounts for roughly one-third of installed industrial waste heat recovery capacity worldwide. National efficiency initiatives and industrial modernization programs continue accelerating deployment across major production hubs. Enterprises are increasingly investing in high-capacity recovery systems, advanced controls, and integrated energy-management platforms to improve plant efficiency while reducing operational energy losses across large-scale manufacturing operations.

South America accounted for approximately 5.4% of global market activity in 2025, with demand concentrated in mining, cement, metals, and industrial processing sectors. Rising electricity costs and growing pressure to improve energy productivity are encouraging industrial operators to evaluate waste heat utilization strategies. Deployment activity remains strongest among large enterprises with established capital investment programs. Infrastructure limitations and uneven industrial modernization continue influencing adoption rates; however, several large-scale industrial facilities are integrating energy-efficiency technologies as part of broader operational improvement initiatives. Strategic partnerships between engineering firms and industrial operators are helping expand deployment opportunities across key industrial hubs.

Brazil Market Outlook: Brazil leads regional demand due to its extensive mining, cement, steel, and industrial processing industries. Large manufacturing facilities are increasingly focusing on thermal efficiency improvements to reduce operating costs and improve energy utilization. More than 40% of South America's industrial heat recovery installations are concentrated in Brazil. Companies are pursuing modernization projects that integrate automation, process optimization, and waste heat recovery technologies, creating a stronger foundation for long-term industrial competitiveness and energy resilience.

The Middle East & Africa represented approximately 3.3% of global market demand in 2025 but remains one of the most dynamic deployment environments. Industrial diversification programs, large-scale infrastructure development, and expanding downstream processing capacity are driving interest in thermal recovery technologies. Oil refining, petrochemicals, cement production, and industrial manufacturing remain the primary application sectors. Several major industrial projects have incorporated energy-efficiency requirements directly into facility design specifications, supporting broader adoption of waste heat recovery systems. Companies are increasing investments in integrated energy-management solutions to improve operational performance while reducing energy losses across large industrial complexes.

Saudi Arabia Market Outlook: Saudi Arabia is the region’s most strategically significant market due to its large industrial base, petrochemical leadership, and infrastructure modernization initiatives. Major industrial operators are integrating waste heat recovery technologies into refining and manufacturing projects as part of broader efficiency enhancement programs. Industrial energy optimization investments have increased significantly alongside large-scale economic diversification efforts. The country continues expanding advanced industrial zones where thermal recovery systems are increasingly deployed to improve process efficiency, reduce energy intensity, and strengthen long-term industrial productivity.

The Waste Heat Recovery Unit market is characterized by competition between global engineering leaders such as Siemens Energy, Mitsubishi Heavy Industries, ABB, Valmet, and Thermax and regional EPC-driven suppliers focused on cost-efficient deployment. The top five players collectively account for approximately 38–42% of market activity, creating a moderately consolidated structure. Competition centers on thermal efficiency, lifecycle cost, deployment speed, and customization. Advanced ORC and heat-exchanger technologies deliver 15–25% higher energy recovery performance, while modular solutions reduce installation timelines by nearly 20%. Leading vendors are expanding through technology partnerships, localized manufacturing, and vertically integrated service models. The competitive shift is moving toward digitalized energy optimization and turnkey decarbonization platforms rather than standalone equipment sales. High engineering complexity and project qualification requirements remain major entry barriers. Winning requires proven efficiency gains, strong EPC relationships, scalable technology platforms, and long-term operational support capabilities.

Mitsubishi Heavy Industries

ABB

Thermax Limited

Valmet Oyj

Ormat Technologies

Turboden S.p.A.

General Electric Vernova

Bosch Industriekessel

Exergy International

Climeon AB

Kawasaki Heavy Industries

John Wood Group

IHI Corporation

Waste heat recovery technology is rapidly evolving from conventional steam-based systems toward advanced Organic Rankine Cycle (ORC), Kalina Cycle, and intelligent thermal optimization platforms. ORC systems currently represent more than 40% of new industrial deployments due to their ability to recover low-temperature heat streams efficiently. Compared with traditional steam recovery systems, advanced ORC technologies improve usable energy conversion efficiency by 15–20% while reducing maintenance requirements. Industrial operators benefit through lower energy intensity and greater flexibility across diverse manufacturing environments.

Emerging technologies are centered on AI-enabled thermal management, digital twins, advanced heat exchangers, and predictive maintenance platforms. AI-assisted optimization improves recovery efficiency by 12–18%, while advanced heat transfer materials increase thermal capture performance by up to 16%. More than 35% of newly commissioned large-scale systems now incorporate digital monitoring capabilities. Technology leaders and industrial operators gain competitive advantages through reduced downtime, faster diagnostics, and enhanced energy utilization across complex process facilities.

Between 2026 and 2028, hybrid waste heat recovery architectures integrating renewable energy, thermal storage, and smart controls are expected to accelerate deployment. Modular platforms are reducing installation time by nearly 25%, while digital lifecycle management tools improve asset performance consistency. Companies investing early in intelligent recovery ecosystems, advanced automation, and scalable thermal technologies are expected to strengthen operational efficiency, improve energy resilience, and secure higher-value industrial contracts.

April 2026 – Turboden commissioned its fifth ORC waste-heat-to-power system for AGC Group in Thailand, adding 1.8 MWe of recovery capacity at a flat-glass facility. The project strengthens industrial energy efficiency and expands long-term deployment within the glass manufacturing sector. Source: www.turboden.com

March 2026 – Turboden and Tallgrass expanded their partnership through three additional waste-heat-to-power projects across Ohio and Indiana. The installations bring total planned capacity to 46.1 MW, demonstrating increasing utility-scale adoption of ORC technology for compressor station energy recovery.

February 2026 – Valmet secured a heat recovery project with Veolia in Poland, deploying technology capable of recovering more than 50 MW of thermal energy from flue gases. The development strengthens district heating efficiency and supports industrial decarbonization objectives.

April 2026 – Questor Technology received USD 1.9 million to accelerate commercialization of its 1500 kW ORC heat-to-power platform. The funding supports deployment of advanced waste heat conversion technology for industrial facilities seeking onsite power generation and emissions reduction.

The report provides comprehensive analysis of the Waste Heat Recovery Unit market across major technology types, applications, end-user industries, and regional markets. Coverage includes Organic Rankine Cycle systems, Steam Rankine Cycle systems, Kalina Cycle systems, and direct heat recovery technologies deployed across power generation, cement manufacturing, petroleum refining, metal processing, and industrial manufacturing operations. The assessment evaluates deployment trends, technology adoption patterns, operational efficiency improvements, and competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study analyzes demand distribution across heavy industries, utilities, commercial infrastructure, and emerging industrial applications. More than 40% of market activity is concentrated in advanced thermal recovery technologies, while digitalized energy-management integration continues expanding across new installations. The report examines technology innovation, industrial modernization initiatives, strategic partnerships, competitive dynamics, and deployment strategies. It supports investment planning, market entry assessment, expansion prioritization, supplier evaluation, and long-term business decision-making for the 2026–2033 period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,225.0 Million |

| Market Revenue (2033) | USD 2,250.6 Million |

| CAGR (2026–2033) | 7.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens Energy; Mitsubishi Heavy Industries; ABB; Thermax Limited; Valmet Oyj; Ormat Technologies; Turboden S.p.A.; GE Vernova; Bosch Industriekessel; Exergy International; Climeon AB; Kawasaki Heavy Industries; John Wood Group; IHI Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |