Reports

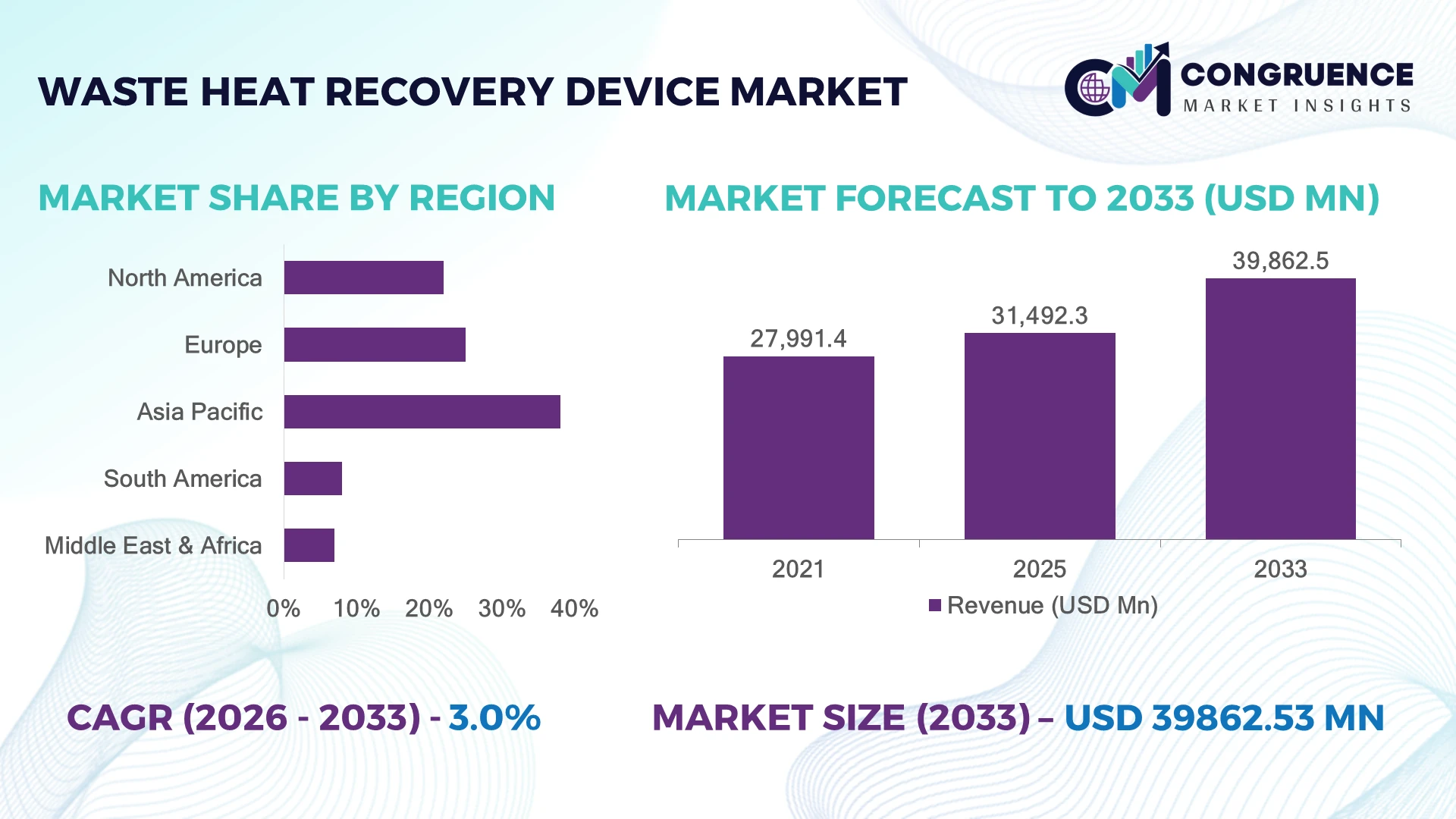

The Global Waste Heat Recovery Device Market was valued at USD 31,492.3 Million in 2025 and is anticipated to reach a value of USD 39,862.5 Million by 2033 expanding at a CAGR of 2.99% between 2026 and 2033. Growth is driven by industrial decarbonization initiatives, stricter energy-efficiency mandates, and rising adoption of advanced heat exchangers and organic Rankine cycle technologies across energy-intensive sectors.

China dominates the market with nearly 30% share, supported by large-scale steel, cement, and chemical industries, while investments under industrial energy transition programs accelerate deployment. The country operates more than 1,000 major industrial waste heat recovery installations. The United States follows with approximately 20% share, driven by refinery modernization and efficiency upgrades. Europe maintains over 25% adoption due to EU emissions regulations and industrial sustainability targets.

Strategic investments in high-efficiency recovery technologies will determine long-term competitive advantage.

Market Size & Growth: USD 31.49 Billion (2025) to USD 39.86 Billion (2033), 2.99% CAGR; industrial energy optimization and carbon reduction policies accelerate adoption.

Top Growth Drivers: Industrial energy efficiency (35%), decarbonization initiatives (30%), and rising manufacturing automation (25%) drive market expansion.

Short-Term Forecast: By 2028, advanced recovery systems reduce industrial energy losses by 10–15% and improve process efficiency by up to 20%.

Emerging Technologies: AI-based energy monitoring, smart heat exchangers, and advanced thermal materials reshape next-generation recovery solutions.

Regional Leaders: Asia-Pacific reaches USD 16 Billion+ with manufacturing adoption; Europe exceeds USD 10 Billion through ESG compliance; North America approaches USD 8 Billion through refinery upgrades.

Consumer/End-User Trends: Over 60% of large industrial facilities prioritize waste heat recovery as part of energy management strategies.

Pilot/Case Example: A 2023 European cement recovery project achieved approximately 15% fuel savings through upgraded heat recovery equipment.

Competitive Landscape: Leading suppliers including Siemens Energy, GE Vernova, Mitsubishi Heavy Industries, ABB, and Ormat Technologies compete through efficiency-focused solutions.

Regulatory & ESG Impact: Global industrial emission policies target 40%+ reductions in energy-related carbon intensity, strengthening recovery technology investments.

Investment & Funding: More than USD 10 Billion is directed toward industrial energy efficiency projects, with partnerships expanding across manufacturing hubs.

Innovation & Future Outlook: Next-generation systems integrate digital twins, modular designs, and AI-driven optimization for competitive industrial transformation.

Waste Heat Recovery Device Market adoption is accelerating across cement, steel, power generation, and chemical industries as companies prioritize energy reuse and operational efficiency. Recent innovations include compact heat exchangers, digital monitoring platforms, and hybrid recovery systems, with industrial facilities reporting up to 20% efficiency improvements. The global shift toward cleaner manufacturing following energy security concerns and regulatory tightening is creating new deployment opportunities across emerging economies.

The Waste Heat Recovery Device Market is becoming strategically important as industries seek energy independence, lower operating costs, and compliance with increasingly strict environmental standards. Manufacturers are restructuring energy strategies as global supply chains emphasize efficient production, particularly after energy price volatility in Europe and industrial modernization initiatives across Asia.

Advanced waste heat recovery technologies are outperforming conventional systems through improved thermal conversion and digital controls. Organic Rankine cycle systems and smart heat exchangers deliver approximately 15–25% higher efficiency compared with older recovery configurations while reducing maintenance requirements. Europe demonstrates strong technology-led adoption through emissions regulations, whereas Asia-Pacific leads in large-scale industrial deployment due to manufacturing capacity expansion.

Industries are increasingly integrating recovery devices into cement plants, steel mills, and power facilities. For example, large cement producers are deploying heat recovery units to convert kiln exhaust into usable electricity while reducing energy dependence. Companies are increasing partnerships with engineering firms and expanding investments in modular recovery solutions.

The next phase of market competition will depend on technological integration, lifecycle efficiency, and the ability to deliver measurable energy savings across industrial operations.

Rising industrial energy costs and carbon reduction mandates are accelerating waste heat recovery adoption across cement, steel, and chemical facilities. More than 40% of large industrial operators globally have introduced energy-efficiency programs, while advanced recovery systems can reduce process energy losses by 15–25%. In China, steel producers are expanding heat recovery installations to improve fuel utilization and meet emissions targets under industrial modernization initiatives. Companies are responding through technology partnerships, localized manufacturing, and investments in high-efficiency heat exchangers and organic Rankine cycle solutions. The strategic advantage is shifting toward manufacturers capable of delivering measurable energy savings with integrated digital monitoring.

High upfront investment, complex integration requirements, and uneven industrial infrastructure remain major barriers for waste heat recovery deployment. Installation costs can represent 20–30% of total project expenditure, while smaller industrial facilities often lack technical resources for system integration. In India and Southeast Asian manufacturing hubs, fragmented industrial operations limit large-scale adoption despite significant heat-loss potential. Supply-chain constraints for specialized components, including high-temperature materials and customized exchangers, affect project timelines and profitability. Companies are reducing exposure through modular system designs, supplier diversification, long-term component contracts, and regional manufacturing expansion. Operational flexibility has become a critical differentiator for improving deployment scalability.

The next opportunity phase is driven by smart energy management, artificial intelligence-based optimization, and expansion into previously underserved industrial segments. Digital monitoring platforms can improve recovery system performance by 10–20% through real-time heat-flow optimization and predictive maintenance. Japan and Germany are advancing industrial automation initiatives that integrate waste heat recovery with smart factory ecosystems. Growing demand from data centers, hydrogen facilities, and advanced manufacturing plants creates new application pathways. Companies are increasing R&D investments, forming technology partnerships, and developing compact modular recovery devices. The strongest opportunity lies in combining thermal recovery hardware with digital intelligence to create scalable energy-management solutions.

Long-term market advancement depends on overcoming integration challenges across diverse industrial environments and legacy production systems. Approximately 30% of industrial facilities operate with aging infrastructure that requires customized engineering before recovery technologies can be deployed effectively. Cybersecurity requirements are also increasing as connected monitoring systems become standard, with industrial networks facing rising protection demands. In the United States and Europe, evolving efficiency regulations require continuous technology upgrades and compliance adaptation. Companies must invest in workforce training, advanced engineering capabilities, and interoperable platforms to maintain reliable operations. The competitive landscape will favor providers that combine hardware expertise with digital infrastructure and lifecycle support.

Smart Heat Monitoring Growth Industrial operators are shifting toward digitally connected waste heat recovery devices, with AI-based monitoring and predictive analytics adoption rising by 20–30% in large manufacturing facilities. Companies are integrating IoT sensors, automated controls, and energy management platforms to improve heat capture visibility and reduce unplanned downtime. The transition is strongest in Germany and Japan, where smart factory investments are accelerating operational optimization. A non-obvious shift is that digital performance tracking is becoming a purchasing criterion alongside thermal efficiency.

Modular System Deployment Expansion Manufacturers are increasing demand for modular waste heat recovery units as industries seek faster installation and lower disruption periods. Modular designs reduce project implementation timelines by approximately 25% and improve deployment flexibility for mid-sized facilities. Companies are restructuring product portfolios toward compact systems that support phased industrial upgrades, particularly in India and Southeast Asia. Supply-chain pressure for customized engineering solutions is pushing suppliers toward standardized components and localized assembly models.

Industrial Electrification Integration Waste heat recovery systems are increasingly being integrated with electrification initiatives across steel, chemicals, and process industries. Facilities adopting combined heat recovery and electrification strategies report energy optimization improvements of 15–20%. Regulatory pressure from European industrial emissions frameworks is encouraging companies to redesign production workflows rather than only upgrade individual equipment. Technology providers are responding through partnerships that combine thermal recovery, automation, and energy management capabilities.

Advanced Material Adoption High-temperature alloys, corrosion-resistant materials, and improved heat exchanger designs are changing equipment performance standards. Advanced materials can extend operational life by 10–15% in demanding industrial environments while improving heat transfer reliability. Companies are increasing R&D collaboration with material suppliers to address challenges in chemical plants and metal processing facilities. This trend is creating a competitive advantage for manufacturers offering durable systems designed for extreme operating conditions.

Heat exchangers represent the leading type segment in the Waste Heat Recovery Device Market due to broad applicability across cement, steel, chemical, and power generation facilities. Their dominance is supported by scalability, proven integration capability, and compatibility with existing industrial processes. More than 50% of industrial recovery installations rely on advanced heat exchanger configurations because they offer efficient thermal transfer with relatively straightforward deployment. Companies are focusing on high-temperature exchanger designs, corrosion-resistant materials, and customized engineering solutions to improve performance. Organic Rankine Cycle (ORC) systems represent the fastest-growing type segment as industries seek electricity generation from low- and medium-temperature waste heat sources. ORC adoption is expanding by approximately 15–20% annually in niche industrial applications due to improved efficiency and modular designs. Traditional boilers and steam-based recovery systems remain important for heavy industries, while emerging technologies such as thermoelectric recovery gain attention for specialized applications. Companies are increasing investments in hybrid recovery platforms to capture diverse heat sources.

Power generation remains the leading application area as industries increasingly convert waste heat into usable electricity and reduce dependence on external energy sources. Cement plants, refineries, and steel facilities represent major demand centers, with large installations accounting for more than 60% of total industrial recovery capacity. Companies are expanding deployment of combined heat and power systems to improve energy resilience and control operating expenses. Process heating applications are emerging as the fastest-growing segment as manufacturers seek direct thermal reuse instead of electricity conversion. Adoption is increasing by around 20% in energy-intensive facilities where heat reuse improves production efficiency. Applications in chemical processing, food manufacturing, and data centers are expanding as operators prioritize continuous energy optimization. Remaining applications, including district heating and refrigeration support, are gaining strategic relevance through integrated energy networks.

Heavy industries represent the leading end-user segment due to high-temperature operations, continuous production cycles, and significant waste heat generation. Steel, cement, and chemical manufacturers account for a substantial portion of deployments, with large industrial facilities representing over 65% of installed recovery capacity. These companies are prioritizing customized solutions, long-term efficiency gains, and integration with existing production systems. Equipment suppliers are responding through strategic partnerships, lifecycle service models, and industry-specific engineering solutions. Power utilities and commercial facilities are emerging as the fastest-growing end-user groups as energy security and sustainability targets influence investment decisions. Adoption among these users is increasing by approximately 15–25% as organizations explore distributed energy optimization. Data centers, manufacturing clusters, and infrastructure operators are evaluating waste heat reuse for district heating and secondary applications. Companies are shifting toward flexible solutions that support multiple heat sources and changing operational requirements.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 3.8% between 2026 and 2033.

North America holds a significant position in the Waste Heat Recovery Device Market, supported by refinery modernization, power generation upgrades, and rising adoption across cement, chemical, and manufacturing industries. The region contributes approximately 22% of global market activity, with the United States accounting for the majority of deployments due to its large industrial base. More than 50% of new industrial energy-efficiency projects in major manufacturing sectors include digital monitoring or optimization technologies. Companies are expanding through technology partnerships and customized recovery solutions to improve operational efficiency and reduce energy losses.

United States Market Outlook: The United States remains the dominant country within North America due to its extensive refining, petrochemical, and industrial infrastructure. Over 30% of large industrial facilities are actively implementing energy management improvements, increasing demand for advanced heat recovery devices. Federal industrial efficiency programs and corporate sustainability commitments are encouraging investments in high-performance recovery systems and integrated energy platforms.

Europe maintains a strong market position due to strict emissions regulations, industrial decarbonization programs, and widespread adoption of energy-efficient manufacturing technologies. The region represents nearly 25% of global demand, supported by Germany, Italy, and France’s industrial sectors. More than 40% of European industrial companies have implemented structured energy-efficiency initiatives, increasing demand for advanced heat recovery equipment. Companies are investing in automated control systems, high-temperature materials, and integrated solutions to meet evolving sustainability requirements while improving production economics.

Germany Market Outlook: Germany leads Europe’s waste heat recovery adoption through its advanced manufacturing ecosystem, automotive supply chain, and chemical production capabilities. Nearly 60% of large manufacturing companies prioritize energy optimization projects, supporting deployment of efficient recovery systems. Industrial automation expertise and strong engineering capabilities position Germany as a key innovation hub for next-generation thermal recovery technologies.

Asia-Pacific represents the largest market for waste heat recovery devices, supported by extensive steel, cement, chemical, and power generation industries. The region contributes around 38% of global market activity, with China, Japan, and India driving adoption. China’s industrial sector accounts for a major share of installations, with more than 1,000 large industrial facilities utilizing waste heat recovery technologies. Companies are expanding manufacturing capacity, forming technology partnerships, and developing cost-efficient systems to support large-scale industrial deployment.

China Market Outlook: China dominates Asia-Pacific due to its massive industrial production base and continued investments in energy efficiency. The country’s steel, cement, and chemical industries represent major application areas, with industrial energy optimization programs supporting wider adoption. More than 30% of large industrial plants have incorporated advanced energy-saving technologies, strengthening demand for high-capacity recovery solutions.

South America is witnessing gradual adoption of waste heat recovery devices, driven by mining, metals, cement, and power generation industries. The region contributes approximately 8% of global market activity, with Brazil and Chile representing key deployment markets. Mining operations and mineral processing facilities are increasingly evaluating recovery solutions to improve energy utilization and reduce operational costs. Companies are focusing on localized partnerships and modular systems to overcome infrastructure limitations and improve project feasibility.

Brazil Market Outlook: Brazil remains the leading market in South America due to its large industrial base, steel production capacity, and mining operations. Around 25% of major industrial facilities are increasing investments in energy-efficiency measures, supporting demand for waste heat recovery technologies. Companies are prioritizing scalable solutions that integrate with existing production infrastructure and reduce energy dependency.

Middle East & Africa is emerging as a high-potential market due to refinery expansion, petrochemical investments, and industrial diversification programs. The region accounts for nearly 7% of global market activity, with demand concentrated in energy-intensive industries. Countries are investing in industrial modernization projects, with more than 20% of large energy-sector facilities exploring efficiency improvement technologies. Companies are expanding partnerships and deploying advanced recovery systems to improve resource utilization and support sustainability targets.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically important market in the region due to its large refining, petrochemical, and industrial infrastructure. Industrial transformation programs are increasing demand for energy optimization technologies, with major facilities integrating efficiency-focused upgrades. The country’s expanding manufacturing ecosystem and investment in advanced industrial systems are creating opportunities for waste heat recovery solution providers.

The Waste Heat Recovery Device Market features global technology leaders competing with regional engineering specialists and OEM suppliers. Key competitors include Siemens Energy, Mitsubishi Heavy Industries, GE Vernova, Ormat Technologies, and specialized ORC providers. The top five players collectively account for approximately 35–40% of market activity. Competition is based on technology efficiency, customization, supply reliability, and lifecycle service capabilities, with advanced systems improving recovery performance by 15–25%. Global leaders focus on integrated digital platforms and international expansion, while regional firms compete through cost advantages and faster customization. Partnerships, modular designs, and vertical integration are reshaping competitive positioning. High engineering expertise and industrial certification requirements create entry barriers. Winning requires combining thermal innovation, reliable supply chains, and application-specific solutions.

Mitsubishi Heavy Industries

GE Vernova

ABB

Alfa Laval

Ormat Technologies

Thermax Limited

Bosch Industriekessel

Turboden

Orcan Energy

Echogen Power Systems

BORSIG

Advanced heat exchangers, Organic Rankine Cycle (ORC) systems, and digital energy platforms are transforming waste heat recovery operations. Modern heat exchangers improve thermal transfer efficiency by 15–20% compared with conventional designs, while ORC technology enables electricity generation from lower-temperature heat sources. Adoption of automated monitoring systems is increasing across more than 30% of large industrial facilities as companies seek predictive maintenance advantages.

AI-enabled optimization and industrial IoT integration represent emerging technology shifts, allowing operators to track heat flows, adjust performance, and reduce energy losses by approximately 10–15%. Companies benefiting most are technology providers offering integrated hardware and software solutions rather than standalone equipment suppliers. Modular recovery units are also expanding deployment flexibility by reducing installation complexity and improving project timelines.

Between 2026 and 2028, competitive advantage will increasingly depend on smart recovery systems, advanced materials, and hybrid energy integration. New-generation solutions combining ORC modules, digital twins, and automated controls are positioned to outperform legacy systems through higher reliability, lower operating costs, and improved scalability. Companies investing now in intelligent thermal management platforms will strengthen industrial partnerships and capture emerging efficiency-driven demand.

May 2025 E.ON and ArcelorMittal launched a steel heat recovery project in Poland using flue-gas recovery technology operating at up to 250°C, improving energy reuse and reducing emissions in production operations. Source: www.news.eonenergy.com

February 2025 Alfa Laval deployed a textile heat recovery solution in India with Mangla Smart Energy Solutions, targeting 100,000 TPD hot effluent streams and improving fuel savings through advanced heat exchanger integration. Source: www.alfalaval.in

April 2025 Clean Energy Technologies announced $400,000 in ORC system sales and enhanced its 350 kW magnetic bearing system for larger industrial applications, expanding scalable waste heat recovery deployment. Source: www.cetyinc.com

May 2024 Orcan Energy commissioned an ORC waste heat recovery system at Dyckerhoff’s Geseke cement plant, using a 50-tonne heat exchanger to generate electricity from clinker cooling heat.

The Waste Heat Recovery Device Market Report covers comprehensive analysis across major technology types, applications, end-user industries, and geographic markets. The study evaluates heat exchangers, ORC systems, boilers, and advanced recovery technologies across industries including cement, steel, chemicals, power generation, and manufacturing. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level deployment insights.

The report provides strategic intelligence on market positioning, technology adoption patterns, competitive benchmarking, and investment priorities. It evaluates enterprise adoption trends, digital integration, modular system development, and emerging industrial applications. The analysis supports business planning through insights into expansion opportunities, partnership strategies, product innovation priorities, and competitive positioning through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 31,492.3 Million |

| Market Revenue (2033) | USD 39,862.5 Million |

| CAGR (2026–2033) | 2.99% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Siemens Energy; Mitsubishi Heavy Industries; GE Vernova; ABB; Alfa Laval; Ormat Technologies; Thermax Limited; Bosch Industriekessel; Turboden; Orcan Energy; Echogen Power Systems; BORSIG |

| Customization & Pricing | Available on Request (10% Customization Free) |