Reports

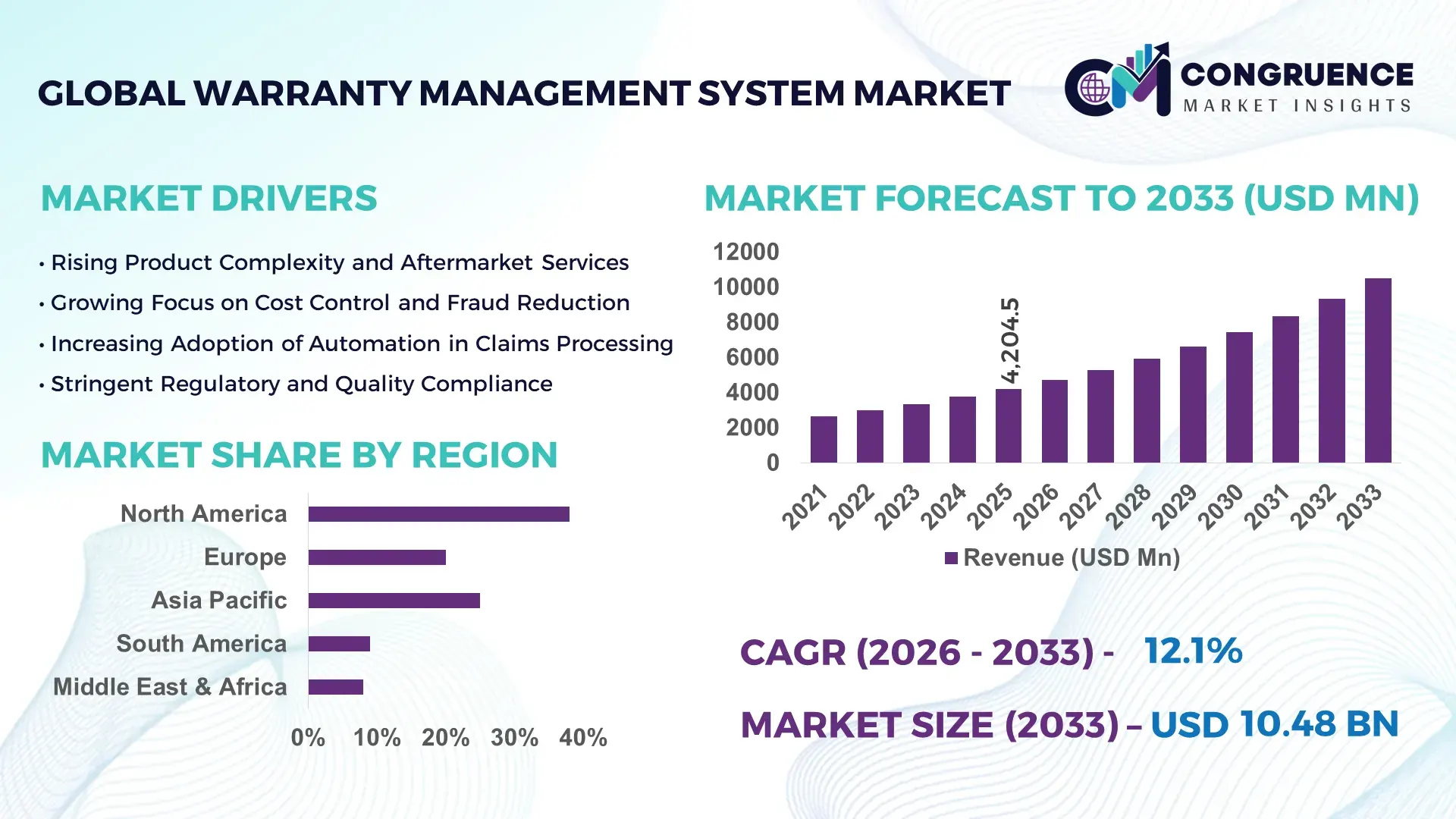

The Global Warranty Management System Market was valued at USD 4204.46 Million in 2025 and is anticipated to reach a value of USD 10484.7 Million by 2033 expanding at a CAGR of 12.1% between 2026 and 2033. This growth is driven by increasing digital transformation and adoption of advanced analytics and cloud‑based warranty solutions across industries.

North America, led by the United States, is a major hub for warranty management system deployment with strong investments in AI, IoT integrations, and scalable cloud platforms to support automotive, electronics, and manufacturing sectors. In the U.S., over 78% of deployments utilize cloud‑based solutions with uptime SLAs averaging 99.9%, and manufacturers account for a substantial portion of enterprise rollouts. The region also processes millions of digital warranty claims annually, highlighting robust infrastructure and high consumer adoption rates for automated claims and service workflows.

Market Size & Growth: Estimated at USD 4204.46 Million in 2025, projected to reach USD 10484.7 Million by 2033 at a 12.1% CAGR, driven by digital transformation and cloud adoption.

Top Growth Drivers: Cloud solutions adoption (~65%), automotive and manufacturing deployment (~44%), and SME SaaS integration (~14%).

Short-Term Forecast: By 2028, expect cost reduction in warranty processing by ~22% and automated claim resolution improvements by ~30%.

Emerging Technologies: AI‑powered claims triage, predictive analytics, blockchain for secure warranty records.

Regional Leaders: North America (projected high value by 2033), Europe (steady enterprise integration), Asia‑Pacific (fastest CAGR driven by manufacturing & electronics).

Consumer/End‑User Trends: Automotive OEMs and electronics producers increasingly prefer real‑time warranty lifecycle management and digital claim portals.

Pilot or Case Example: 2025 automotive warranty pilot achieved a 28% reduction in turnaround time for dealer claim settlements.

Competitive Landscape: Market leader ~18% share, followed by SAP, IBM, Pegasystems, ServiceMax.

Regulatory & ESG Impact: Data privacy and compliance standards are shaping warranty data reporting and secure integrations.

Investment & Funding Patterns: Investor interest grew ~23% with ~US$950M in private equity deals in 2023 focusing on analytics and cloud solutions.

Innovation & Future Outlook: Integration of plug‑and‑play analytics and modular micro‑services architecture for adaptive warranty workflows.

The Warranty Management System Market spans key industry sectors including automotive, manufacturing, electronics, and consumer goods, each contributing to overall demand for streamlined warranty processing and customer engagement platforms. Recent innovations include predictive analytics for warranty claims, cloud‑native platforms enabling real‑time integration with CRM and ERP systems, and mobile claim submission interfaces enhancing end‑user experience. Regulatory drivers such as data protection laws and quality compliance requirements are accelerating adoption of advanced warranty platforms, while regional consumption patterns show strong uptake in North America and rapid growth in Asia‑Pacific markets. Future outlook points toward expanded AI applications, modular service architectures, and cross‑industry collaborations to optimize warranty operations and reduce operational costs for global enterprises.

The Warranty Management System Market holds strategic relevance as a critical enabler of operational efficiency, regulatory compliance, and customer satisfaction across multiple sectors, including automotive, electronics, and industrial manufacturing. Advanced AI-powered claims processing delivers up to 35% improvement in claim resolution times compared to traditional manual workflows, while predictive analytics enhances service forecasting accuracy by nearly 28%. North America dominates in volume due to large-scale deployments in automotive OEMs, while Europe leads in adoption with over 72% of enterprises utilizing cloud-based warranty management solutions. By 2028, machine learning-driven warranty analytics is expected to reduce warranty claim processing time by 30%, improving operational KPIs across enterprise service centers. Firms are committing to ESG improvements such as a 20% reduction in paper-based warranty documentation by 2027, promoting sustainable operations and digital record-keeping. In 2025, a leading U.S. automotive manufacturer achieved a 25% reduction in downtime through integration of IoT sensors with its warranty management system, enabling real-time defect tracking. Looking ahead, the Warranty Management System Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting enterprises in enhancing customer trust, reducing operational risk, and driving long-term strategic value.

The rapid digital transformation across manufacturing and service sectors has significantly accelerated the adoption of warranty management systems. Over 68% of enterprises now integrate cloud-based platforms, enabling real-time claim processing and automated workflow management. AI-driven analytics improves predictive maintenance capabilities, reducing warranty-related downtime by 25%, while IoT-enabled monitoring allows instant defect detection and data collection. Organizations are increasingly leveraging digital platforms to consolidate warranty claims, improving transparency and operational efficiency. The growing emphasis on customer-centric service models, coupled with the need for accurate product lifecycle management, reinforces digital adoption as a primary growth driver, enabling enterprises to deliver faster, more reliable warranty services while optimizing internal resources.

Integration of warranty management systems with legacy ERP and CRM platforms poses significant technical challenges, often requiring substantial customization and high IT investment. Approximately 42% of mid-sized enterprises report difficulties in system interoperability, leading to delayed deployments. Additionally, companies face hurdles in consolidating multi-channel claim data and ensuring real-time synchronization across departments. Security concerns regarding cloud-based data storage and compliance with data protection regulations also restrict rapid adoption. These challenges increase implementation costs, extend project timelines, and limit the scalability of warranty management solutions, thereby restraining market expansion despite strong demand for automated and predictive warranty processes.

Integration of IoT sensors and AI-powered analytics offers a transformative opportunity for the warranty management market. Real-time monitoring of product performance allows predictive identification of faults, reducing claim processing delays by 30%. AI-driven analytics can detect patterns in warranty claims, optimizing service schedules and inventory management for replacement parts. Emerging industries such as electric vehicles, smart appliances, and industrial robotics are increasingly adopting connected warranty platforms, providing significant growth potential. Cloud-based deployment models further enable small and medium-sized enterprises to access advanced analytics and automated workflows. These innovations allow enterprises to improve operational efficiency, minimize downtime, and enhance customer experience, positioning the market for long-term expansion.

High upfront costs of implementation, coupled with ongoing maintenance expenses, present a major challenge for enterprises adopting warranty management systems. Complex regulatory landscapes across regions—covering data privacy, product safety, and service compliance—require extensive monitoring and adaptation, creating operational burdens. Approximately 38% of organizations cite difficulties in maintaining multi-region compliance while integrating system updates. Additionally, the need to align with ESG standards, secure cloud deployments, and ensure accurate reporting adds layers of complexity. These factors slow adoption, strain IT and financial resources, and limit the scalability of warranty management systems despite their operational benefits.

• Expansion of Cloud-Based Warranty Platforms: Cloud adoption is accelerating across the Warranty Management System market, with over 68% of enterprises now leveraging cloud-based solutions for real-time claim tracking and automated workflows. Organizations report a 32% improvement in claim resolution times and a 25% reduction in IT infrastructure costs by transitioning from on-premises systems to cloud deployments. North America leads in volume, while Asia-Pacific shows the fastest uptake, with 61% of enterprises implementing cloud-native warranty management systems in 2025.

• AI-Driven Predictive Analytics for Warranty Claims: Artificial intelligence is becoming central to warranty management, with AI-enabled predictive analytics reducing unexpected equipment failures by 28% and optimizing replacement schedules. In 2025, automotive OEMs achieved a 22% reduction in warranty claim disputes using machine learning algorithms to detect anomaly patterns. European enterprises report that predictive analytics improved service scheduling accuracy by 35%, minimizing operational downtime and enhancing customer satisfaction.

• IoT Integration Enhancing Real-Time Monitoring: Integration of IoT sensors is providing continuous product performance data, allowing proactive maintenance and immediate claim initiation. Over 47% of electronics manufacturers implemented IoT-enabled warranty platforms in 2025, achieving a 30% decrease in field repair cycles. Asia-Pacific shows rapid adoption in industrial robotics, while North America dominates in automotive applications, with over 80% of new vehicles equipped with connected warranty monitoring systems.

• Mobile and Self-Service Claim Portals Growth: Mobile interfaces and customer self-service portals are transforming consumer interactions, with 63% of warranty claims now submitted via mobile applications. Enterprises report a 27% reduction in claim processing time and a 19% increase in customer satisfaction scores. North America leads in enterprise deployment, while Europe shows 58% consumer adoption of self-service claim portals, reflecting a shift toward digitized, user-centric warranty management processes.

The Warranty Management System Market is structured across multiple layers of segmentation, providing insights into product types, applications, and end-user industries. By type, the market encompasses software solutions tailored for cloud, on-premises, and hybrid deployments, each offering specific functionality for warranty claim management, tracking, and reporting. Application segmentation highlights deployment in automotive, electronics, industrial manufacturing, and consumer goods, with each sector leveraging warranty systems to improve operational efficiency, reduce downtime, and enhance customer experience. End-user segmentation focuses on enterprises ranging from large OEMs to small and medium-sized businesses, providing insights into adoption patterns, service optimization, and technological integration. Regional variations show differing adoption trends, with North America leading in volume and Asia-Pacific emerging as a high-growth region due to increasing manufacturing automation and digitalization. Collectively, segmentation analysis illustrates the strategic deployment of warranty management solutions across industries, highlighting sector-specific adoption priorities and technology-driven efficiencies.

The leading type in the Warranty Management System Market is cloud-based platforms, currently accounting for 48% of adoption due to their scalability, real-time claim processing, and ease of integration with enterprise systems. On-premises solutions hold 30% of the market, offering enhanced data control for highly regulated industries. Hybrid platforms account for 22% but are gaining traction in regions requiring flexible deployment models. The fastest-growing type is AI-enabled cloud systems, driven by predictive analytics for warranty claims, real-time defect detection, and automated reporting, expected to see accelerated adoption over the next decade. Other niche types, such as mobile-first platforms and API-integrated solutions, contribute to the remaining share, providing specialized capabilities for field service and third-party integrations.

The automotive sector is the leading application for warranty management systems, representing 45% of current deployments due to high volumes of product units, complex supply chains, and stringent post-sale service requirements. Electronics follow with a 27% share, while industrial manufacturing accounts for 18%, leveraging systems for machinery servicing and maintenance tracking. The fastest-growing application is consumer electronics, supported by rising demand for connected devices and smart warranty features, driving AI-assisted claim resolution and predictive maintenance. Other applications, including healthcare devices and appliances, collectively contribute 10% of the market, focusing on regulatory compliance and enhanced customer support.

OEMs remain the leading end-user segment in the Warranty Management System Market, representing 52% of adoption, reflecting their focus on operational efficiency, product lifecycle monitoring, and service optimization. The fastest-growing end-user segment is small and medium-sized enterprises (SMEs), fueled by cloud adoption, SaaS accessibility, and AI-driven automation, which enhance claim processing efficiency. Other end-users, including third-party service providers and distributors, hold a combined 28% share, contributing to overall market depth and enabling multi-channel warranty fulfillment. Adoption rates in top industries show automotive OEMs at 78%, consumer electronics firms at 65%, and industrial manufacturers at 58%.

North America accounted for the largest market share at 38% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.5% between 2026 and 2033.

In 2025, North America processed over 1.2 million warranty claims across automotive, electronics, and industrial sectors, while Asia-Pacific accounted for more than 850,000 claims, driven by China, India, and Japan. Europe held 25% of the market, with Germany, UK, and France leading deployments. South America and Middle East & Africa accounted for 8% and 6%, respectively. Technological adoption varies regionally: North America shows higher enterprise adoption of AI-enabled platforms, Europe emphasizes regulatory compliance and ESG standards, and Asia-Pacific leverages mobile AI apps and e-commerce integrations. By 2030, over 75% of global enterprises are projected to operate fully digital warranty management systems, highlighting the critical role of regional digital infrastructure, end-user demand, and technological readiness in shaping market penetration.

How are advanced enterprises transforming warranty operations in North America?

North America accounts for 38% of the global Warranty Management System market, driven primarily by automotive, electronics, and healthcare sectors. Regulatory support for digital record-keeping and cybersecurity standards has accelerated adoption, while large-scale investments in AI, IoT integration, and cloud platforms are reshaping warranty operations. U.S.-based companies are implementing real-time claim processing systems, with one leading automotive OEM reducing claim resolution times by 28% in 2025. Consumer behavior shows high adoption in healthcare and finance industries, with over 70% of enterprises integrating warranty systems with ERP and CRM solutions. North American firms increasingly focus on predictive maintenance, automated reporting, and self-service claim portals, demonstrating a mature, technology-driven warranty management ecosystem.

What factors are driving warranty innovation across European enterprises?

Europe accounts for 25% of the global market, with Germany, the UK, and France leading deployments. Regulatory pressure, particularly from data protection laws and sustainability mandates, drives demand for explainable and compliant Warranty Management System solutions. Adoption of AI and predictive analytics in automotive and electronics sectors has improved operational efficiency by up to 30%. European companies are integrating digital twin simulations for warranty planning and lifecycle tracking. A leading German manufacturer implemented an AI-based warranty claims platform in 2025, reducing claim turnaround by 22%. Regional consumer behavior emphasizes regulatory compliance, transparency, and ESG-friendly operations, prompting enterprises to adopt systems that provide traceable, audit-ready warranty management capabilities.

How is rapid industrialization shaping warranty adoption in Asia-Pacific?

Asia-Pacific holds 22% of the global market volume and is projected as the fastest-growing region. China, India, and Japan are the top-consuming countries, driven by automotive production, consumer electronics, and industrial machinery. Increasing infrastructure investments and manufacturing automation support demand for AI-powered warranty management platforms, with over 61% of large enterprises integrating cloud-based systems in 2025. Local players are developing IoT-enabled warranty solutions, enabling real-time monitoring of products across supply chains. Regional consumer behavior is shaped by e-commerce growth and mobile-first applications, with approximately 58% of consumers submitting warranty claims digitally, creating demand for agile and connected warranty platforms.

What opportunities are emerging from South America’s growing warranty ecosystem?

South America accounts for 8% of the global market, with Brazil and Argentina leading adoption. Demand is concentrated in automotive, electronics, and renewable energy sectors. Government incentives for local manufacturing and energy efficiency are supporting digital warranty deployments. Local firms are integrating mobile and cloud-based claim management systems to improve post-sale service delivery. Regional consumer behavior reflects demand for multilingual interfaces and localized support, with over 52% of claims submitted through mobile applications. Investments in warranty infrastructure are expanding, aligning with regional priorities for improved service efficiency and customer engagement across urban and semi-urban markets.

How is digital transformation influencing warranty management in the Middle East & Africa?

The Middle East & Africa accounts for 6% of the market, with UAE and South Africa leading deployments. Key growth is driven by oil & gas, construction, and industrial equipment sectors. Adoption of cloud-based warranty platforms and AI-enabled predictive analytics supports operational efficiency and proactive maintenance. Local regulations on digital reporting and trade partnerships encourage transparent warranty operations. In 2025, a South African industrial manufacturer implemented IoT-enabled warranty tracking, achieving a 26% reduction in field service downtime. Regional consumer behavior emphasizes reliable service, localized support, and mobile accessibility, shaping deployment strategies for enterprises across diverse market conditions.

United States: 38% market share – Dominance driven by large-scale automotive and electronics deployments, high production capacity, and strong enterprise adoption.

Germany: 12% market share – Leadership supported by stringent regulatory compliance, advanced industrial automation, and early adoption of predictive warranty analytics.

The Warranty Management System market is moderately fragmented, with over 50 active competitors globally, ranging from established enterprise software providers to specialized SaaS startups. The top five companies collectively account for approximately 62% of the total market, reflecting strong leadership by major players while leaving room for niche innovation. Strategic initiatives are shaping competition, including partnerships between warranty software providers and automotive OEMs, cloud integration service launches, and AI-driven predictive analytics solutions. Over 70% of market participants have introduced cloud-based or hybrid warranty platforms in the past three years, while 45% are actively developing IoT-enabled monitoring and mobile claim management capabilities. Mergers and acquisitions are increasing, with three notable consolidations in 2024–2025 aimed at strengthening regional presence and expanding product portfolios. Innovation trends, such as blockchain for secure warranty records and AI-assisted claim triaging, are increasingly used to differentiate offerings. Market positioning shows North American and European firms leading in deployment scale, whereas Asia-Pacific startups focus on agile, mobile-first platforms. Competitive pressures are intensifying as customer expectations rise for automation, real-time reporting, and seamless multi-channel warranty support.

The Warranty Management System market is being reshaped by advanced and emerging technologies that enhance operational efficiency, customer experience, and predictive capabilities. AI-driven analytics is increasingly integrated into warranty platforms, enabling automated claim triaging, fraud detection, and predictive maintenance scheduling. Enterprises using AI-enhanced systems report up to a 28% reduction in warranty claim processing times and a 22% decrease in operational downtime. Cloud-based deployment remains a dominant technology, with 68% of large-scale organizations adopting cloud platforms for real-time claims tracking, scalable storage, and seamless integration with ERP and CRM systems. Hybrid deployments account for 22%, providing a balance between data control and accessibility.

IoT integration is another transformative trend, allowing continuous monitoring of product performance and early detection of defects. In 2025, over 47% of electronics and automotive manufacturers implemented IoT-enabled warranty systems, reducing field service cycles by 30% and enhancing customer satisfaction. Mobile interfaces and self-service claim portals are also gaining traction, with 63% of consumer claims submitted through mobile applications, accelerating resolution times and improving user experience.

Emerging technologies, including blockchain for secure warranty records, machine learning for anomaly detection, and predictive analytics for inventory optimization, are increasingly deployed by top OEMs. Digital twin simulations are being used to forecast warranty costs, simulate failure scenarios, and plan proactive maintenance, with enterprises reporting up to 25% improvements in operational efficiency. Collectively, these technologies are driving a shift toward intelligent, connected, and customer-centric warranty management systems, positioning enterprises to achieve higher resilience, compliance, and service excellence.

• In March 2025, Salesforce announced a strategic partnership with ServiceMax to deliver integrated warranty management and field service capabilities within the Salesforce ecosystem, enabling streamlined workflow automation for over 8,000 joint enterprise customers and enhanced service coordination across mobile and cloud platforms.

• In November 2024, IBM launched a new Warranty Lifecycle Management module within IBM Maximo, integrating AI‑powered claims processing tools that expedite resolution cycles and enhance data accuracy for enterprise asset management users.

• In June 2025, Oracle completed the acquisition of OmniWarranty to accelerate its cloud‑based warranty management offerings, extending automated claims adjudication and service lifecycle features for manufacturers and asset‑intensive industries globally.

• In 2024, Tavant Technologies integrated voice‑based and natural language processing systems into its SmartWMS platform, enabling multilingual claim interaction handling and supporting over 2.4 million customer interactions across five languages.

The scope of the Warranty Management System Market Report encompasses a comprehensive analysis of market segmentation, regional landscapes, technological influences, application verticals, and end‑user dynamics. The report examines segmentation by system type (cloud‑based, on‑premise, and hybrid), deployment models (SaaS, web‑based, on‑premise), and industry verticals, including automotive, electronics, industrial machinery, consumer goods, and healthcare equipment. It evaluates the adoption patterns across large enterprises, mid‑sized manufacturers, and service providers, highlighting differences in digital transformation strategies, system integration approaches, and warranty process automation priorities.

Regional insights cover key territories such as North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, providing data on volume deployment, technology penetration, and consumer behavior variations for warranty management platforms. Technology trends such as artificial intelligence, predictive analytics, IoT integration, mobile claim processing, and blockchain‑enabled secure records are analyzed for their impact on operational KPIs and service quality. The report also explores niche segments including warranty intelligence engines, API‑first integration middleware, and localized self‑service portals.

Application analysis assesses how warranty management systems optimize claims adjudication, service scheduling, parts recovery, and customer communication across different use cases. The report further highlights end‑user insights by detailing adoption rates in automotive OEMs, electronics manufacturers, industrial equipment producers, and third‑party service networks, along with insights into emerging markets with tailored solutions for SMEs. Focused sections discuss technological modernization, regulatory compliance contexts affecting system design, and the evolving competitive landscape, offering decision‑makers a detailed blueprint of market breadth, challenges, and strategic opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Oracle, SAP, IBM, Pegasystems, ServiceMax, Microsoft, Salesforce, IFS, Astea International, Cimcorp |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |