Reports

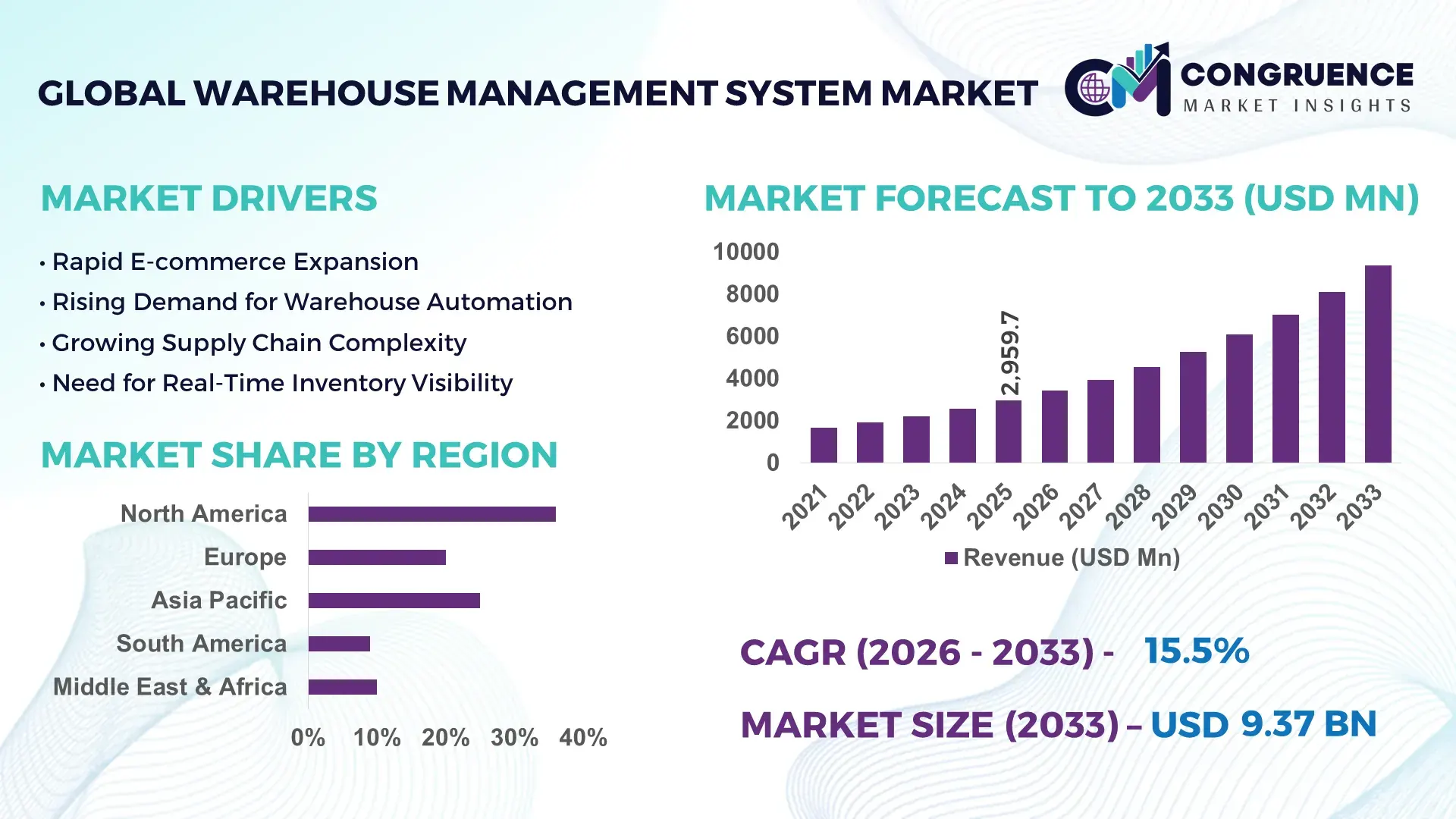

The Global Warehouse Management System (WMS) Market was valued at USD 2959.66 Million in 2025 and is anticipated to reach a value of USD 9373.43 Million by 2033 expanding at a CAGR of 15.5% between 2026 and 2033. This growth is primarily driven by escalating demand for real‑time inventory tracking and automation in logistics operations.

In the United States, which leads the WMS landscape, advanced automation investments exceed USD 1.2 billion annually, with deployment of AI‑enabled systems in fulfillment centers rising by over 40% year‑on‑year. U.S. enterprises maintain an extensive production capacity of scalable cloud‑native WMS platforms serving retail, manufacturing, and third‑party logistics sectors. Investment levels in smart warehousing technologies reached a record high in 2025, with over 65% of large warehouse operators adopting integrated mobile and IoT solutions. Consumer adoption in omnichannel distribution has grown significantly, with real‑time WMS adoption rates above 70% among Fortune 500 companies, enhancing throughput and order accuracy.

• Market Size & Growth: Global WMS Market valued at USD 2959.66 M in 2025, projected to reach USD 9373.43 M by 2033 at a 15.5% CAGR, driven by demand for automation and real‑time inventory control.

• Top Growth Drivers: Increasing automation adoption (45%), cloud migration (38%), supply chain digitization (42%).

• Short‑Term Forecast: By 2028, WMS deployments expected to reduce labor costs by up to 25% and improve picking accuracy by up to 30%.

• Emerging Technologies: AI/ML optimization engines, IoT sensor networks, augmented reality (AR) for warehouse operations.

• Regional Leaders: North America USD 3.2 B by 2033 with strong e‑commerce integration; Europe USD 2.1 B with emphasis on robotics; Asia Pacific USD 2.8 B driven by manufacturing modernization.

• Consumer/End‑User Trends: High adoption in retail, e‑commerce, 3PL segments; preference for mobile‑friendly and cloud‑based solutions.

• Pilot or Case Example: 2025 pilot in a major global retailer achieved a 22% reduction in order cycle time using AI‑driven WMS optimization.

• Competitive Landscape: Market leader with ~28% share, followed by key competitors with strong global footprints and solution portfolios.

• Regulatory & ESG Impact: Data security regulations and sustainability mandates are shaping WMS integrations and energy‑efficient operations.

• Investment & Funding Patterns: Over USD 850 M invested in WMS innovation and startups in the past year, with growing venture interest in robotics and AI.

• Innovation & Future Outlook: Continued advancement in autonomous mobile robots, predictive analytics, and digital twin technologies to enhance warehouse efficiency.

The Warehouse Management System (WMS) market continues to evolve with strong contributions from automotive, retail, pharmaceuticals, and food & beverage sectors, each driving specific functional requirements. Recent innovations include modular AI scheduling engines and advanced voice‑directed picking interfaces that are improving throughput and accuracy. Regulatory frameworks emphasizing workplace safety and data privacy are influencing WMS feature sets, while economic drivers such as labor cost inflation and consumer demand for rapid fulfillment are accelerating deployment. Regional consumption patterns show robust growth in Asia Pacific logistics modernization and sustained investment in North American smart warehousing. Emerging trends include increased adoption of collaborative robots, edge computing for real‑time decisioning, and expansion of subscription‑based SaaS WMS models targeting SMEs.

The Warehouse Management System (WMS) Market is strategically positioned as a core enabler of operational efficiency, transparency, and competitive differentiation across logistics and supply chain functions. As global supply chains become increasingly complex, WMS platforms serve as integral backbone technologies that synchronize warehousing activities with broader enterprise resource planning (ERP) and transportation management systems (TMS). For example, AI‑driven predictive analytics delivers a 28% improvement in order fulfillment accuracy compared to rule‑based scheduling standards, underscoring measurable operational gains from advanced technologies. In volume terms, North America dominates in throughput and installed base, while Europe leads in adoption with over 65% of enterprises deploying cloud‑native WMS solutions across multi‑site operations. By 2028, edge computing and real‑time IoT integration are expected to improve inventory cycle count efficiency by up to 32%, reducing discrepancies and stockouts. Firms are committing to ESG metrics, such as a 20% reduction in energy consumption per square meter of automated warehouse footprint by 2027, reflecting strong alignment with sustainability agendas. In 2025, a leading global retailer achieved a 24% reduction in picking errors through implementation of augmented reality (AR) guided picking modules within its WMS platform. Looking ahead, the Warehouse Management System (WMS) Market will continue to be a pillar of resilience, compliance, and sustainable growth as organizations pursue digital transformation and resilient supply chain architectures.

Enhanced automation and robotics adoption is a primary driver transforming the Warehouse Management System (WMS) Market by significantly elevating throughput, accuracy, and labor productivity. Integration of autonomous mobile robots (AMRs) with WMS platforms enables dynamic task allocation, reducing manual travel distances and minimizing idle time. In modern fulfillment centers, robotics‑enabled operations have demonstrated up to 35% improvement in order processing velocity compared to manual systems. Robotics paired with real‑time WMS control supports high‑density storage retrieval and flexible slotting, addressing peak seasonal demand without expanding physical footprint. Additionally, automated conveyor controls and robotic palletizing streamline inbound and outbound workflows, creating continuous material flow with fewer bottlenecks. WMS vendors are increasingly embedding robotics orchestration modules that communicate directly with AMRs and automated storage/retrieval systems (AS/RS), further accelerating adoption across retail, automotive, and third‑party logistics sectors. This shift is supported by declining hardware costs and growing availability of standardized robot‑WMS integration frameworks, enabling mid‑sized operators to benefit from automation without prohibitive upfront expenditures. The result is measurable operational resilience, consistent throughput, and improved worker safety across diverse warehousing environments.

Integration complexities with legacy systems remain a significant restraint to the Warehouse Management System (WMS) Market, particularly for enterprises managing heterogeneous technology stacks accumulated over decades. Legacy ERP and inventory systems often rely on outdated data models, limited APIs, and batch‑oriented processes, which complicate real‑time synchronization with modern WMS platforms. As warehouses scale and diversify operations, inconsistent data flows between legacy systems and WMS can result in inventory discrepancies, throughput delays, and errors that require manual reconciliation. Furthermore, technical debt in legacy infrastructure increases implementation risk and duration, discouraging swift migration to cloud‑native or modular WMS solutions. Organizations with constrained IT resources may struggle to allocate specialized personnel for data mapping, middleware configuration, and ongoing support, thereby extending project timelines and raising total cost of ownership. In regulated industries such as pharmaceuticals and aerospace, integration hurdles are compounded by stringent validation requirements and audit trails, intensifying reluctance to overhaul entrenched systems. These integration challenges slow adoption cycles and divert investment toward maintaining outdated platforms, inhibiting the broader modernization of WMS ecosystems.

Real‑time data analytics presents one of the most compelling opportunities in the Warehouse Management System (WMS) Market, enabling organizations to unlock actionable insights across inventory, labor, and equipment performance. By harnessing streaming data from sensors, RFID, and connected devices, WMS platforms can offer fine‑grained visibility into stock levels, movement patterns, and operational bottlenecks. Predictive analytics models can forecast demand spikes, optimize labor scheduling, and reduce overstock situations, enhancing responsiveness to market fluctuations. For example, analytics‑driven alerts can identify slow‑moving SKUs and trigger dynamic re‑slotting to improve picking efficiency. Integration of real‑time dashboards with executive decision support tools empowers supply chain leaders to assess performance KPIs instantly and adjust strategies without lag. Additionally, analytics facilitate root‑cause analysis for recurring errors, enabling continuous improvement cycles and cost containment. The growing volume of operational data, combined with advancements in machine learning, positions real‑time analytics as a differentiator for WMS vendors and adopters alike, particularly in complex, high‑velocity environments such as e‑commerce and cold chain logistics. As demand for operational intelligence grows, analytics‑centric WMS solutions will expand competitive advantage and drive long‑term strategic value.

Cybersecurity constitutes a critical challenge for the Warehouse Management System (WMS) market due to increasing digital interconnectivity and reliance on cloud‑based infrastructure. As warehouses adopt IoT devices, mobile terminals, and remote access capabilities, the attack surface for malicious actors widens, exposing sensitive inventory, transactional, and customer data. Inadequate security configurations can lead to ransomware incidents, unauthorized access, and operational disruption that halt fulfillment activities. WMS platforms interfacing with broader enterprise systems such as ERP, CRM, and transportation networks must defend against sophisticated threats that exploit weak authentication, unpatched firmware, and unsecured network segments. Compliance with data protection regulations further complicates security postures, requiring continuous monitoring, encryption, and incident response planning. Additionally, third‑party integrations can introduce vulnerabilities if partners do not adhere to robust cybersecurity protocols, creating systemic risk across supply chain ecosystems. To mitigate these challenges, organizations must invest in multi‑factor authentication, intrusion detection systems, and regular penetration testing, which can strain IT budgets and resource allocations. Addressing cybersecurity proactively is essential but remains a persistent market challenge as digital transformation accelerates within warehousing operations.

• Expansion of AI-Driven Inventory Optimization: Artificial intelligence is increasingly integrated into WMS platforms, enabling predictive inventory allocation and automated replenishment. In 2025, AI-driven modules improved stock accuracy by 27% and reduced stockouts by 18% in large-scale fulfillment centers. Adoption is particularly high in North America, with over 62% of enterprises using AI-based optimization tools to manage multi-site warehouses efficiently.

• Integration of Autonomous Mobile Robots (AMRs): AMRs are transforming warehouse workflows by reducing manual labor and improving picking efficiency. Companies deploying AMRs in 2025 recorded a 33% reduction in order cycle time and a 21% increase in throughput. Europe leads in robotics adoption with 58% of large warehouses incorporating autonomous solutions, while Asia-Pacific is catching up rapidly due to increased e-commerce demand.

• Cloud-Native and SaaS WMS Solutions: Cloud-based platforms now account for 65% of new WMS deployments, offering remote accessibility, scalability, and faster software updates. Enterprises using SaaS WMS reported a 24% improvement in IT maintenance efficiency and a 19% reduction in system downtime. North America dominates adoption in volume, while Europe leads with 70% of mid-sized enterprises leveraging SaaS models for multi-warehouse management.

• Sustainability and Energy-Efficient Warehousing: WMS platforms are increasingly supporting ESG goals, enabling real-time monitoring of energy consumption and warehouse carbon footprint. In 2025, smart energy management integrations helped companies achieve a 17% reduction in electricity usage and a 12% improvement in overall operational efficiency. Asia-Pacific warehouses are pioneering energy-efficient layouts, while North America focuses on automated HVAC and lighting controls integrated with WMS dashboards.

The Warehouse Management System (WMS) market is structured around several core segmentation criteria, reflecting product types, applications, and end‑user requirements. By type, offerings range from standalone systems focused purely on warehouse operations to cloud‑based platforms that enable remote access and scalability, and integrated suites that combine WMS with broader supply chain modules. Deployment models include on‑premise and cloud, catering to varied IT strategies. Application segmentation encompasses supply chain optimization, inventory tracking, order fulfillment and distribution, yard and dock management, and labor/workforce management, each addressing distinct operational priorities. End‑user segmentation highlights sectors such as 3PL logistics providers, manufacturing, retail & e‑commerce, healthcare, food & beverage, chemicals, and others, reflecting diverse needs for inventory accuracy, regulatory compliance, and fulfillment speed. These segments illustrate how WMS solutions are tailored to specific functional, operational, and industry‑driven requirements, enabling decision‑makers to align technology investments with strategic business goals across heterogeneous warehousing environments.

Warehouse Management System (WMS) offerings can be categorized into key types that serve different functional and operational requirements. Cloud‑based WMS is the leading type, with around 57% of deployments globally owing to its scalability, remote accessibility, and lower upfront IT infrastructure needs. Versus traditional on‑premise systems that require local hardware and dedicated IT teams, cloud WMS enables remote management of inventory across multiple sites and simplifies updates and maintenance. Cloud adoption is especially prominent in retail and e‑commerce logistics where rapid scaling and distributed operations are essential. On‑premise WMS solutions remain relevant for organizations prioritizing data control and extensive customization, accounting for roughly 25% of current installations. ERP‑integrated WMS solutions form about 13% of the market, providing seamless connectivity with broader enterprise processes like procurement, finance, and supply chain planning. Supply chain execution (SCE) suites that bundle WMS with transportation and labor modules contribute the remaining 5%, offering end‑to-end visibility across logistics operations.

Warehouse Management System (WMS) applications span essential operational functions integral to logistics and supply chain excellence. Supply chain and logistics optimization is the leading application, representing approximately 38% of WMS use, driven by the need for coordinated inventory flows across multi‑node distribution networks. This application supports complex fulfillment strategies, including omnichannel distribution and cross‑dock operations. Inventory and asset tracking follows with about 27% of deployments, enabling precise SKU‑level visibility and reducing discrepancies in stock records. Order fulfillment and distribution applications account for 20%, focusing on rapid picking, packing, and shipment execution to meet tight delivery windows, particularly in e‑commerce and retail sectors. Other applications such as yard/dock management and workforce/labor management combined contribute the remaining 15%, enhancing on‑site resource allocation and dock utilization.

End‑user segmentation in the Warehouse Management System (WMS) market reflects the varied operational imperatives across industries. Third‑party logistics (3PL) providers are the leading end‑user segment with about 35% adoption, driven by their need to serve multiple clients with real‑time inventory and operational transparency across distributed warehousing networks. Retail and e‑commerce end users follow at roughly 28%, prioritizing rapid order fulfillment and returns processing to maintain customer satisfaction. Manufacturing enterprises account for 18%, using WMS to synchronize warehouse inventory with production schedules and reduce lead times. Healthcare and pharmaceuticals contribute around 10%, emphasizing compliance with strict storage and tracking requirements. Other sectors such as food & beverage and chemicals make up about 9%, focusing on temperature‑controlled inventory and regulatory adherence.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

North America leads in volume with over 1,100 WMS deployments in large-scale fulfillment centers and 450+ mid-sized enterprises implementing cloud-native solutions. Asia-Pacific’s projected expansion is fueled by China, India, and Japan collectively contributing more than 42% of regional warehouse modernization projects. Europe accounted for 28% of adoption in 2025, with Germany, UK, and France showing high demand for automation. South America captured 12% of market share, supported by Brazil and Argentina’s logistics and retail growth. Middle East & Africa accounted for 7%, driven by UAE and South Africa investment in oil, gas, and construction warehouses. Across regions, digital adoption, robotics integration, and AI-based inventory optimization are shaping strategic deployment priorities, with measurable outcomes such as 25–35% reductions in order cycle times and labor costs.

How are enterprises leveraging advanced WMS technologies for operational efficiency?

North America holds approximately 36% of the global WMS market, driven by high enterprise adoption in healthcare, retail, and finance. Key industries include e-commerce fulfillment, automotive, and cold-chain pharmaceuticals, emphasizing real-time inventory control and regulatory compliance. Government support for smart logistics and tax incentives for automation has accelerated deployment. Technological advancements such as AI-driven predictive analytics, cloud-native platforms, and autonomous mobile robots are transforming warehouse operations. For instance, a leading U.S. logistics provider implemented AI-based WMS to reduce picking errors by 22% across 120 warehouses. Regional consumer behavior shows higher adoption in sectors requiring stringent accuracy and traceability, with large enterprises prioritizing cloud and SaaS WMS solutions to streamline multi-site operations.

How is the regulatory landscape influencing warehouse digital transformation?

Europe accounts for roughly 28% of the WMS market, with Germany, the UK, and France as leading adopters. Regulatory frameworks and sustainability initiatives drive demand for energy-efficient and explainable WMS solutions. European warehouses are increasingly integrating robotics, IoT sensors, and AI-driven analytics for inventory optimization and labor allocation. A major German retailer deployed a robotics-assisted WMS to improve picking efficiency by 20% across 50 facilities. Regional behavior emphasizes regulatory compliance and environmental reporting, with enterprises favoring WMS systems that ensure traceability, audit readiness, and operational transparency.

What factors are fueling rapid warehouse automation and digitization?

Asia-Pacific holds the second-largest market volume, with China, India, and Japan leading adoption. The region benefits from expanding e-commerce, manufacturing modernization, and urban logistics infrastructure. Enterprises are deploying mobile AI apps, cloud-based WMS, and autonomous robotics, particularly in urban fulfillment centers. Local players are investing in smart warehousing platforms, enabling real-time inventory monitoring and labor efficiency improvements of up to 30%. Consumer behavior shows rapid acceptance of mobile-enabled tracking, same-day delivery services, and automated order fulfillment, driving widespread digital adoption.

How are logistics modernization and government incentives shaping the market?

South America represents about 12% of the WMS market, with Brazil and Argentina as key contributors. The growth is supported by investments in transportation infrastructure, warehouse automation, and energy-efficient facilities. Trade policies and government incentives for technology adoption encourage enterprises to deploy cloud-based WMS. A leading Brazilian logistics operator implemented an AI-assisted WMS to reduce stock discrepancies by 18%. Regional consumer behavior reflects language localization needs, mobile tracking adoption, and retail-driven order fulfillment priorities.

What trends are driving WMS adoption in industrial and resource-driven sectors?

Middle East & Africa hold approximately 7% of the market, led by the UAE and South Africa. Growth is fueled by oil & gas, construction, and large-scale distribution networks. Technological modernization, including AI-based forecasting, IoT-enabled inventory tracking, and automated storage systems, is increasing efficiency. Local regulations and trade partnerships promote digital adoption. A UAE-based logistics firm adopted autonomous WMS solutions, achieving a 20% reduction in operational downtime. Regional consumer behavior reflects high demand for efficiency, reliability, and integration with enterprise resource planning systems.

United States – 36% market share: High production capacity and large-scale enterprise adoption in healthcare, retail, and finance sectors.

China – 22% market share: Rapid warehouse modernization, e-commerce growth, and extensive investment in automation and AI-based inventory solutions.

The competitive environment in the Warehouse Management System (WMS) market is highly dynamic, with approximately 1,000 active competitors, including global, regional, and niche players, reflecting a fragmented market structure. Large enterprise vendors coexist with smaller, specialized providers, making the market both diverse and competitive. The combined share of the top 5 companies is around 33%, indicating significant influence from leading players while a majority of demand is met by agile, regional firms.

Market positioning varies: established players provide end-to-end supply chain solutions with strong enterprise penetration across manufacturing, retail, and 3PL sectors. Mid-sized and niche vendors compete on adaptability, customization, and industry-specific solutions. Strategic initiatives shaping competition include partnerships for robotics integration, AI-enhanced WMS product launches, mergers and acquisitions to expand cloud and automation capabilities, and alliances to strengthen regional presence. Innovation trends such as AI-driven predictive analytics, cloud orchestration, autonomous mobile robotics integration, and blockchain for traceability are critical differentiators. Pricing models range from SaaS subscriptions to enterprise licenses, with customer service, integration ease, and post-sales support being pivotal in buyer decision-making.

Blue Yonder Group, Inc.

Infor

Körber Supply Chain

Tecsys

HighJump / Körber units

Swisslog Holding AG

Softeon WMS

ShipHero

3PL Central

The Warehouse Management System (WMS) market is experiencing a rapid transformation driven by emerging and advanced technologies that enhance operational efficiency, accuracy, and scalability. Artificial intelligence (AI) and machine learning are increasingly embedded in WMS platforms, enabling predictive inventory management, demand forecasting, and automated replenishment. In 2025, AI-driven WMS modules improved inventory accuracy by 27% and reduced stockouts by 18% in large-scale fulfillment centers. Autonomous mobile robots (AMRs) and automated storage/retrieval systems (AS/RS) are revolutionizing material handling, enabling dynamic task allocation and reducing manual labor requirements. Deployments in North America and Europe demonstrated up to a 33% improvement in order processing speed and a 21% increase in throughput. Robotics integration is complemented by IoT sensor networks, which provide real-time visibility into stock levels, warehouse environment conditions, and equipment utilization, facilitating data-driven decision-making across multi-site operations.

Cloud-native WMS platforms are driving digital transformation, allowing enterprises to manage multiple facilities remotely and implement seamless software updates. Approximately 65% of new WMS deployments in 2025 were cloud-based, reflecting strong adoption trends in retail, e-commerce, and third-party logistics. Emerging technologies, including augmented reality (AR) for guided picking, voice-directed workflows, and blockchain for traceability, are also gaining traction. AR-assisted WMS implementations reduced picking errors by 22%, while blockchain integration ensures secure, auditable inventory records. These technologies collectively enable warehouses to enhance throughput, reduce operational costs, improve workforce productivity, and meet the growing demand for accurate, real-time order fulfillment in increasingly complex supply chains.

• In March 2025, Blue Yonder announced a strategic partnership with Microsoft to accelerate AI‑powered supply chain deployments on Azure, enhancing WMS automation and inventory responsiveness across large distribution networks.

• In July 2024, SAP unveiled an enhanced version of SAP Extended Warehouse Management integrated with SAP S/4HANA Cloud, delivering improved real‑time analytics, robotics integration, and API‑driven extensibility for modern warehouse operations.

• In January 2025, Logiwa secured a major contract with a large North American retailer to deploy its cloud‑based WMS across 40 distribution centers, significantly expanding its high‑volume fulfillment footprint.

• In March 2025, Descartes Systems Group launched a major upgrade to its WMS platform, introducing AI‑driven inventory optimization, enhanced real‑time visibility, and expanded cloud deployment flexibility for enterprise users.

The scope of the Warehouse Management System (WMS) Market Report encompasses detailed analysis and delineation of the entire WMS ecosystem, focusing on software and hardware solutions that automate and optimize warehouse operations. It covers segmentation by product type — including cloud‑based SaaS platforms, on‑premise systems, and hybrid deployments — with real‑time inventory tracking, advanced analytics, and robotics orchestration components evaluated across multiple use cases. The report further examines application areas such as order fulfillment and distribution, inventory and asset tracking, yard and dock management, labor and workforce management, and multi‑site orchestration, presenting quantitative adoption insights and operational impact metrics. Industry focus spans manufacturing, retail & e‑commerce, third‑party logistics (3PL), healthcare & pharmaceuticals, food & beverage, and specialized verticals, providing decision‑grade perspectives on sector‑specific adoption patterns. Geographic coverage includes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, each analyzed for deployment trends, technological readiness, regulatory influences, and infrastructure maturity. Technology dimensions — such as AI/ML automation, IoT sensor networks, autonomous mobile robotics (AMRs), AR‑assisted picking, and blockchain traceability — are evaluated for their influence on operational KPIs like inventory accuracy percentages, throughput improvements, and labor productivity gains. The report also identifies emerging niche segments, including cold chain logistics automation and mobile‑first WMS interfaces, offering comprehensive insights for strategic planning and competitive benchmarking.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

15.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SAP SE , Oracle Corporation , Manhattan Associates , Blue Yonder Group, Inc., Infor, Körber Supply Chain, Tecsys, HighJump / Körber units, Swisslog Holding AG, Softeon WMS, ShipHero, 3PL Central |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |