Reports

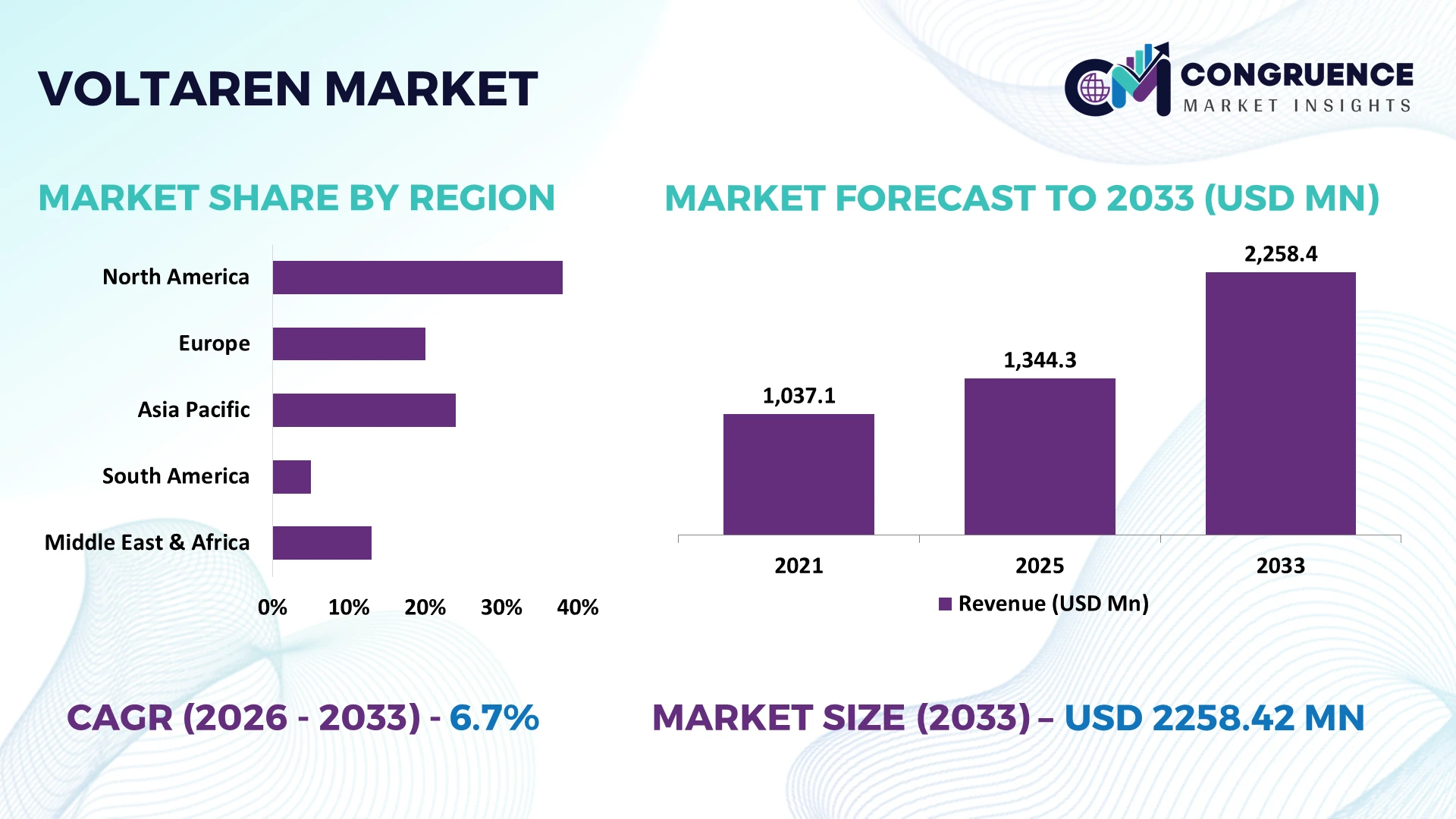

The Global Voltaren Market was valued at USD 1344.28 Million in 2025 and is anticipated to reach a value of USD 2258.42 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. Growth is supported by rising musculoskeletal disorder incidence, wider over-the-counter topical pain relief adoption, digital pharmacy expansion, and continued innovation in fast-absorbing diclofenac gel formulations.

The United States accounts for approximately 34% of global Voltaren consumption, supported by extensive retail pharmacy networks, high arthritis prevalence, and advanced self-care adoption, while Germany maintains strong prescription and OTC penetration across Europe. North America outpaces several Asia-Pacific markets in premium topical analgesic usage, whereas China is expanding manufacturing capacity and healthcare investment, strengthening regional supply resilience amid evolving global trade policies in 2026.

Strategic focus on resilient distribution networks, premium topical formulations, and high-growth self-medication channels will determine long-term competitive positioning.

Market Size & Growth: USD 1344.28 Million in 2025 to USD 2258.42 Million by 2033 at 6.7% CAGR, supported by expanding OTC pain-management adoption and advanced topical drug formulations.

Top Growth Drivers: Osteoarthritis cases +12%, OTC analgesic purchases +9%, e-pharmacy sales +18%, strengthening sustained global demand.

Short-Term Forecast: By 2027, digital pharmacy fulfillment improves distribution efficiency by 15% while inventory lead times decline by 10%.

Emerging Technologies: AI-enabled demand forecasting, automated pharmaceutical packaging, and enhanced transdermal formulation technologies improve supply accuracy and product performance.

Regional Leaders: North America approaches USD 790 Million, Europe exceeds USD 640 Million, Asia-Pacific surpasses USD 520 Million, driven by retail pharmacy expansion and self-care adoption.

Consumer/End-User Trends: More than 58% of repeat topical pain-relief buyers prefer non-invasive treatment options before oral therapies.

Pilot/Case Example: In 2025, automated pharmaceutical distribution programs reduced retail stock shortages by approximately 20%, improving product availability.

Competitive Landscape: Leading manufacturer holds nearly 32% market share alongside established multinational pharmaceutical companies competing through brand expansion and formulation improvements.

Regulatory & ESG Impact: Sustainable packaging initiatives lower plastic usage by nearly 18%, while stricter pharmaceutical compliance strengthens product quality across international markets.

Investment & Funding: More than USD 500 Million supports manufacturing upgrades, regional expansion, and digital healthcare partnerships as supply chains diversify globally.

Innovation & Future Outlook: Faster-absorbing topical gels, smart packaging, and digital consumer engagement accelerate premium product differentiation across high-growth healthcare markets.

The Voltaren market continues to benefit from increasing preference for localized pain management, particularly in osteoarthritis, sports injuries, and chronic musculoskeletal conditions. Advanced gel formulations with improved skin absorption and patient convenience are strengthening product differentiation, while OTC channel expansion supports wider accessibility. Approximately 18% growth in online pharmacy transactions is reshaping distribution, with manufacturers reinforcing regional supply networks amid evolving pharmaceutical compliance requirements, setting the stage for broader strategic market evaluation.

The Voltaren market is becoming strategically important as pharmaceutical companies compete through stronger over-the-counter portfolios, digital retail expansion, and localized manufacturing strategies. Supply-chain restructuring since recent geopolitical disruptions has accelerated investment in regional production and inventory optimization, reducing procurement risks while improving product availability. Companies are increasingly aligning commercialization strategies with consumer self-care trends and evolving non-prescription medicine regulations to strengthen market access and brand resilience.

Advanced transdermal formulation technologies provide approximately 20% faster dermal absorption than conventional topical gel platforms while automated packaging systems reduce manufacturing waste by nearly 15%, improving production efficiency and operational consistency. The United States leads in premium branded topical analgesic deployment through mature pharmacy networks, whereas India is expanding cost-efficient pharmaceutical manufacturing and export capabilities supported by modern production infrastructure. Over the next two to three years, digital pharmacy transactions are expected to exceed 25% of total OTC pain-relief distribution in several developed healthcare markets, reshaping channel strategies.

Manufacturers are expanding partnerships with retail pharmacy chains while integrating AI-based demand forecasting to improve inventory planning and reduce stock imbalances. Companies are simultaneously investing in sustainable packaging and regional distribution hubs to strengthen operational resilience. Organizations that combine formulation innovation, diversified manufacturing, and digitally enabled commercial execution will secure stronger competitive positioning and long-term market relevance.

Growing consumer preference for self-managed musculoskeletal treatment is accelerating Voltaren adoption across retail and digital healthcare channels. More than 60% of mild-to-moderate joint pain cases are initially managed through non-prescription therapies, while online pharmacy purchases have increased by nearly 18% over recent years. Regulatory expansion of OTC access in several developed countries has further improved product availability. Pharmaceutical companies are responding through faster-absorbing gel formulations, broader pharmacy partnerships, and localized packaging investments. Switzerland and the United States remain important innovation and commercialization hubs, enabling companies to improve supply continuity while differentiating products through formulation performance rather than price competition alone.

Manufacturers continue facing structural pressure from varying national regulations governing diclofenac labeling, dosage limits, and OTC distribution requirements. Compliance costs have increased by approximately 12%, while pharmaceutical ingredient procurement expenses fluctuate by nearly 10% due to global sourcing concentration and logistics volatility. These conditions affect production planning, launch timelines, and inventory management, particularly for multinational suppliers. Companies are reducing operational exposure through supplier diversification, regional manufacturing expansion, and long-term procurement contracts. Germany's emphasis on pharmaceutical quality compliance illustrates how regulatory consistency improves market confidence but simultaneously raises operating requirements for international manufacturers.

Digital health platforms and next-generation topical drug delivery technologies are creating differentiated commercial opportunities beyond traditional pharmacy sales. AI-supported demand planning has improved inventory accuracy by nearly 20%, while advanced transdermal formulation research enhances therapeutic consistency by approximately 15%. Japan continues investing in pharmaceutical innovation focused on patient convenience and formulation efficiency, supporting premium product positioning. Companies are expanding R&D collaborations, digital patient engagement programs, and smart retail partnerships to capture higher-value consumer segments. An emerging opportunity lies in integrating personalized digital healthcare guidance with OTC pain management, strengthening customer retention while improving treatment adherence.

Sustaining operational consistency across multiple healthcare systems remains a major execution challenge despite expanding demand. Cross-border compliance management increases administrative workloads by approximately 14%, while inventory synchronization across omnichannel distribution networks requires up to 25% greater planning accuracy than conventional retail models. Workforce capability gaps in digital supply-chain management further complicate large-scale deployment. Companies must strengthen enterprise analytics, automated quality monitoring, and integrated planning platforms to maintain reliable product availability. The United States demonstrates how sophisticated retail infrastructure supports scale, but manufacturers still require continuous investment in digital operations and cross-functional coordination to preserve long-term competitiveness.

Digital Pharmacy Channel Expansion Digital pharmacy fulfillment is reshaping Voltaren distribution, with online OTC analgesic transactions increasing by approximately 18% and automated prescription validation reducing processing time by nearly 25%. Retail chains are integrating omnichannel inventory systems following stricter pharmaceutical traceability requirements, enabling faster replenishment while manufacturers strengthen partnerships with e-commerce platforms and regional distributors.

Advanced Formulation Optimization Pharmaceutical developers are prioritizing improved topical delivery technologies, achieving nearly 20% higher dermal absorption efficiency and reducing residue by approximately 15% compared with earlier formulations. Companies are scaling formulation upgrades and manufacturing automation to enhance patient convenience, improve treatment adherence, and maintain differentiation as premium topical therapies become increasingly competitive.

Regional Manufacturing Diversification Supply-chain restructuring continues as manufacturers reduce dependence on single-country sourcing. Localized production capacity has expanded by roughly 16%, while inventory safety levels have increased by approximately 12% across major pharmaceutical hubs. Companies are expanding contract manufacturing partnerships and regional packaging operations to strengthen resilience against geopolitical uncertainty and logistics disruptions affecting active pharmaceutical ingredients.

Data-Driven Commercial Operations AI-enabled demand forecasting and pharmacy analytics are improving inventory accuracy by nearly 21% while reducing stock-out frequency by approximately 17%. Enterprise sales teams increasingly rely on predictive replenishment models to optimize retail allocation. A notable operational shift is the integration of consumer purchasing behavior into production planning, enabling manufacturers to synchronize supply with seasonal pain-management demand more effectively.

Topical Gel remains the dominant product type, accounting for approximately 48% of total market demand due to rapid application, localized pain relief, established consumer confidence, and broad over-the-counter availability. Manufacturers continue prioritizing gel-based formulations because they integrate efficiently into retail pharmacy networks while requiring limited patient training. Emulgel represents the fastest-growing segment, supported by improved skin penetration and enhanced cosmetic acceptability, with adoption increasing by nearly 14% across premium healthcare markets. Companies are expanding formulation research and upgrading production lines to strengthen differentiation.

Tablets and Capsules continue serving patients requiring systemic pain management, particularly where multiple inflammatory conditions coexist, although healthcare providers increasingly recommend topical therapies to minimize unnecessary systemic exposure. Topical Patch products are steadily expanding, supported by extended-release delivery and greater patient convenience, recording approximately 11% adoption growth in selected developed markets. Investment priorities increasingly emphasize advanced topical technologies, premium formulations, and diversified product portfolios to strengthen long-term competitive positioning.

Osteoarthritis represents the leading application, contributing approximately 43% of overall Voltaren utilization due to the growing elderly population and sustained need for localized pain management. Clinical preference for topical therapy before systemic treatment has strengthened prescribing and OTC purchasing patterns. Sports Injuries constitute the fastest-growing application, with utilization expanding by nearly 15% as recreational fitness participation rises and recovery-focused treatment protocols gain wider acceptance. Manufacturers are expanding sports medicine partnerships and targeted consumer campaigns to strengthen brand visibility.

Joint Pain and Muscle Pain continue generating stable demand across working-age adults seeking non-invasive treatment, while Back Pain remains an important application supported by increasing sedentary lifestyles and occupational strain. Companies are refining product positioning, improving patient education initiatives, and optimizing retail placement to address condition-specific demand. Investment increasingly favors differentiated formulations tailored to specific pain indications rather than a uniform therapeutic approach.

Retail Pharmacies account for approximately 52% of total Voltaren sales, benefiting from extensive store networks, immediate product availability, and strong consumer trust in pharmacist guidance. Online Pharmacies represent the fastest-growing end-user segment, expanding by nearly 19% as digital prescription services, home delivery, and mobile healthcare platforms improve accessibility. Pharmaceutical companies are strengthening omnichannel distribution strategies through retail alliances, digital marketing, and synchronized inventory management to maximize product availability.

Hospitals continue purchasing Voltaren for post-treatment and orthopedic pain management, while Specialty Clinics support targeted musculoskeletal care requiring clinician oversight. Ambulatory Care Centers are steadily increasing procurement as outpatient treatment volumes expand and same-day care models become more prevalent. Manufacturers are introducing customized packaging formats, pricing strategies, and digital ordering systems to meet varying procurement requirements across institutional and consumer-focused healthcare settings, improving distribution efficiency and competitive differentiation.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 7.8% CAGR between 2026 and 2033.

Strong OTC Ecosystem and Digital Distribution Leadership

North America maintains the largest share of the Voltaren market through advanced retail pharmacy infrastructure, high consumer awareness of self-managed pain relief, and established over-the-counter medicine regulations. The region contributes nearly 38% of global demand, supported by extensive pharmacy chains and integrated digital healthcare services. More than 70% of community pharmacies now operate omnichannel fulfillment systems, improving product availability and reducing replenishment delays. Manufacturers continue strengthening partnerships with national pharmacy retailers while expanding automated distribution centers to improve inventory efficiency. Growing adoption of predictive demand planning and digital inventory management is enhancing operational resilience across pharmaceutical supply networks while supporting premium topical analgesic positioning.

United States Market Outlook: The United States remains the regional leader due to its extensive pharmacy infrastructure, advanced pharmaceutical commercialization capabilities, and strong consumer preference for topical pain management. More than 60% of OTC pain-relief purchases occur through organized retail pharmacy networks, while digital pharmacy utilization continues expanding. Companies are investing in AI-enabled demand forecasting, localized warehousing, and retail partnerships to strengthen nationwide distribution efficiency and maintain competitive product availability.

Regulatory Excellence Driving Premium Product Positioning

Europe represents a mature pharmaceutical landscape characterized by rigorous regulatory standards, advanced manufacturing capabilities, and widespread adoption of topical anti-inflammatory therapies. The region accounts for approximately 30% of global market demand, supported by well-established healthcare infrastructure and strong pharmacist-led OTC recommendations. Pharmaceutical manufacturers continue modernizing production facilities, with automated packaging adoption increasing by nearly 18% across major manufacturing sites. Sustainability initiatives, improved quality management systems, and standardized compliance processes are reinforcing supply reliability while supporting premium product differentiation throughout established healthcare markets.

Germany Market Outlook: Germany serves as Europe's operational center for pharmaceutical manufacturing excellence, supported by advanced production technology, stringent quality standards, and highly integrated distribution networks. More than 65% of pharmaceutical production facilities utilize digital quality monitoring systems, strengthening manufacturing consistency. Companies continue investing in process automation, sustainable packaging solutions, and high-efficiency production technologies to maintain operational leadership and regulatory compliance.

Manufacturing Scale and Healthcare Expansion

Asia-Pacific is strengthening its position through expanding pharmaceutical manufacturing capacity, growing healthcare accessibility, and increasing consumer awareness of topical pain management. The region contributes approximately 26% of global market demand while recording the highest deployment momentum. Pharmaceutical production capacity has expanded by nearly 20% across major manufacturing hubs, supported by investments in automated production lines and export-oriented facilities. Companies are establishing regional supply centers, expanding contract manufacturing partnerships, and improving logistics infrastructure to serve both domestic and international markets more efficiently.

China Market Outlook: China plays a pivotal role through its large-scale pharmaceutical manufacturing ecosystem, integrated supply chain, and expanding domestic healthcare consumption. Automated production systems now support over 55% of modern pharmaceutical manufacturing operations in leading facilities. Companies continue investing in advanced formulation technologies, production modernization, and export-oriented manufacturing capabilities, strengthening competitiveness across international pharmaceutical supply networks.

Expanding Retail Healthcare Access

South America continues advancing through broader retail pharmacy penetration, improving healthcare accessibility, and increasing availability of non-prescription pain management products. The region represents approximately 5% of global market demand, supported by modernization of pharmaceutical distribution and stronger retail partnerships. Organized pharmacy networks have expanded by nearly 12% in major urban markets, improving consumer access despite logistical challenges across remote areas. Manufacturers are strengthening local distribution agreements and optimizing inventory planning to reduce supply interruptions while supporting stable product availability across expanding healthcare networks.

Brazil Market Outlook: Brazil leads regional demand through its extensive pharmacy network, expanding healthcare coverage, and established pharmaceutical manufacturing base. More than half of OTC pharmaceutical purchases are concentrated within organized retail pharmacy chains serving major metropolitan areas. Companies are enhancing local packaging operations, strengthening wholesaler relationships, and investing in digital inventory management to improve nationwide product availability and distribution efficiency.

Healthcare Modernization Supporting Market Expansion

The Middle East & Africa market is progressing through healthcare infrastructure modernization, pharmaceutical distribution improvements, and expanding private healthcare investment. The region contributes approximately 4% of global demand while demonstrating increasing adoption of branded topical therapies. Modern pharmaceutical warehousing capacity has expanded by nearly 15% in major healthcare markets, improving storage standards and product availability. Companies are strengthening regional partnerships, expanding local distribution capabilities, and investing in temperature-controlled logistics to enhance operational consistency across diverse healthcare environments.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most strategically significant market due to sustained healthcare modernization, advanced pharmaceutical procurement systems, and increasing investment in localized healthcare infrastructure. More than 70% of pharmaceutical procurement within major public healthcare institutions utilizes centralized digital purchasing platforms. Manufacturers continue expanding regional partnerships, strengthening distribution capabilities, and supporting national healthcare transformation initiatives through improved supply-chain integration and operational efficiency.

Global pharmaceutical leaders including Haleon, Viatris, Teva Pharmaceutical Industries, Perrigo, and Dr. Reddy's Laboratories compete directly against regional OTC analgesic manufacturers through formulation quality, retail distribution strength, pricing efficiency, and pharmacy relationships. The top five participants collectively control approximately 68% of market activity, creating a highly brand-driven competitive environment. Competition increasingly centers on premium topical formulations, where improved absorption delivers nearly 20% better patient satisfaction, while automated manufacturing lowers production costs by about 12% and AI-enabled demand forecasting improves inventory accuracy by 18%. Companies are expanding regional production, securing long-term ingredient contracts, strengthening pharmacy partnerships, and investing in differentiated topical delivery technologies rather than competing solely on price. The competitive landscape is shifting toward supply-chain resilience and digital commercial execution as localized manufacturing reduces logistics exposure. Regulatory compliance, established consumer trust, and pharmacy access remain significant entry barriers. Winning requires superior formulation performance, resilient supply networks, omnichannel distribution capability, and continuous innovation supported by strong brand credibility.

Haleon plc

Viatris Inc.

Teva Pharmaceutical Industries Ltd.

Perrigo Company plc

Dr. Reddy's Laboratories Ltd.

Sun Pharmaceutical Industries Ltd.

Cipla Ltd.

Alkem Laboratories Ltd.

Glenmark Pharmaceuticals Ltd.

Viatris Healthcare

Sandoz AG

STADA Arzneimittel AG

Advanced topical drug delivery technologies are transforming the Voltaren market through enhanced diclofenac absorption, optimized excipient systems, and precision formulation engineering. Modern transdermal delivery platforms improve skin penetration by approximately 20% compared with conventional gel technologies while reducing residue by nearly 15%, supporting greater patient adherence. Around 55% of premium topical product development programs now incorporate advanced permeation enhancement techniques, enabling manufacturers to strengthen therapeutic consistency and product differentiation in competitive OTC markets.

Manufacturing technology is advancing through AI-enabled demand forecasting, automated filling systems, and digital quality monitoring. Automated production lines reduce packaging defects by approximately 18% while predictive maintenance lowers equipment downtime by nearly 14% compared with legacy manual operations. Companies operating integrated digital manufacturing platforms gain stronger supply reliability, faster batch release, and improved regulatory compliance, creating measurable operational advantages over producers relying on conventional production workflows.

Between 2026 and 2028, smart packaging, connected inventory platforms, and AI-assisted consumer analytics will reshape commercial execution. Digital serialization deployment is expected to exceed 60% across major pharmaceutical supply networks, strengthening traceability and counterfeit prevention. Manufacturers investing early in intelligent manufacturing, formulation innovation, and digitally integrated distribution will improve operational responsiveness, accelerate product availability, and reinforce competitive positioning as pharmacy channels become increasingly data-driven and patient-centric.

September 2024 Haleon agreed to increase its ownership in the Tianjin TSKF joint venture in China from 55% to 88%, strengthening local manufacturing and distribution for Voltaren and other OTC brands. The venture generated about 40% of Haleon's China revenue, improving long-term operational control. Source: Reuters

May 2025 Haleon expanded the Voltaren portfolio by introducing new Liquid Gel Caps and extending its patented patch range, with Voltaren systemics growing at nearly double the overall market rate and medicated patches growing almost three times faster than the category. This reinforced premium pain-relief positioning.

June 2025 Haleon completed the acquisition of the remaining 12% stake in Tianjin TSKF, making the Chinese OTC venture wholly owned. The business represented approximately 40% of Haleon's China operations, increasing strategic flexibility for Voltaren manufacturing, innovation, and market expansion. Source: Haleon News

July 2025 Haleon reported continued improvement in Voltaren consumption following the rollout of new-format patches and systemic Voltadexibu in Germany and Italy, leveraging a new active ingredient requiring a smaller therapeutic dose. The innovation strengthened product differentiation and operational portfolio expansion. Source: Haleon Investor Relations

The report delivers a comprehensive assessment of the Voltaren market across product types, applications, end-users, and major geographic markets. It evaluates Topical Gel, Emulgel, Tablets, Capsules, and Topical Patch products while examining demand across osteoarthritis, muscle pain, joint pain, back pain, and sports injuries. Analysis extends to hospitals, retail pharmacies, online pharmacies, specialty clinics, and ambulatory care centers. More than 60% of market activity is concentrated within topical formulations, reflecting the ongoing shift toward localized pain management and consumer self-care.

The study provides strategic evaluation of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating competitive positioning, technology adoption, manufacturing trends, regulatory developments, and distribution transformation. It also examines digital pharmacy expansion, advanced transdermal technologies, supply-chain optimization, and enterprise investment priorities. The insights support portfolio planning, regional expansion strategies, partnership decisions, operational benchmarking, and competitive positioning while identifying emerging opportunities expected to shape market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1344.28 Million |

Market Revenue in 2033 | USD 2258.42 Million |

CAGR (2026 - 2033) | 6.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Haleon plc, Viatris Inc., Teva Pharmaceutical Industries Ltd., Perrigo Company plc, Dr. Reddy's Laboratories Ltd., Sun Pharmaceutical Industries Ltd., Cipla Ltd., Alkem Laboratories Ltd., Glenmark Pharmaceuticals Ltd., Viatris Healthcare, Sandoz AG, STADA Arzneimittel AG |

Customization & Pricing | Available on Request (10% Customization is Free) |