Reports

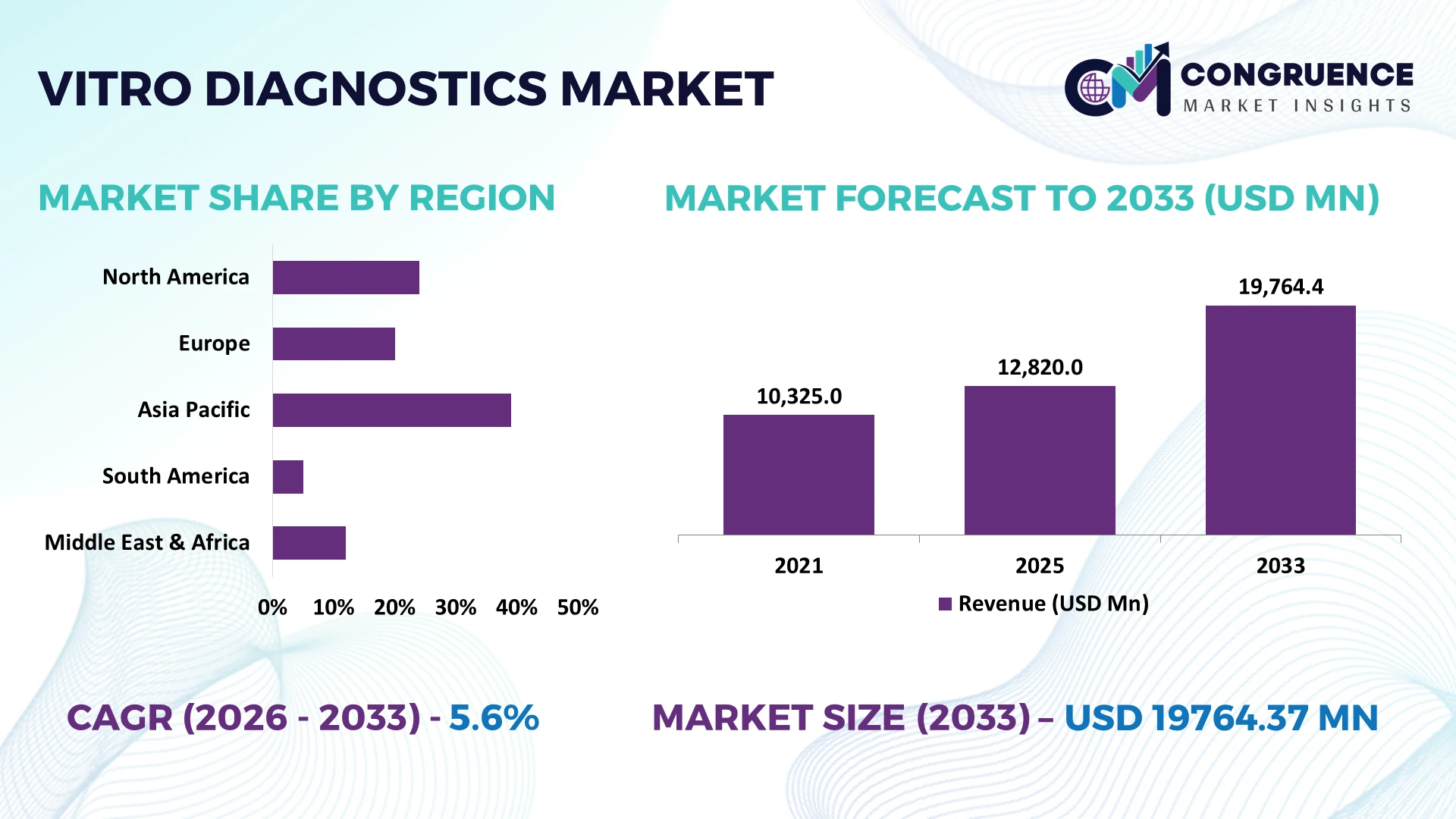

The Global Vitro Diagnostics Market was valued at USD 12820 Million in 2025 and is anticipated to reach a value of USD 19764.37 Million by 2033 expanding at a CAGR of 5.56% between 2026 and 2033. Growth is being accelerated by wider deployment of molecular diagnostics, AI-assisted laboratory workflows, and decentralized testing platforms that improve diagnostic accuracy and clinical turnaround times.

The United States leads the global vitro diagnostics market with approximately 39% of worldwide demand, supported by advanced hospital laboratory networks, strong biotechnology investment, and rapid adoption of automated diagnostic systems. China continues expanding manufacturing capacity and domestic innovation, with local production exceeding 60% of several routine diagnostic consumables, while European laboratories increasingly prioritize digital pathology integration following regional healthcare resilience initiatives influenced by evolving global supply-chain realignment during 2026.

Organizations expanding localized manufacturing, digital laboratory infrastructure, and advanced diagnostic portfolios are positioned to strengthen competitive advantage while improving long-term healthcare delivery resilience.

Market Size & Growth: USD 12820 Million in 2025 reaching USD 19764.37 Million by 2033 at 5.56% CAGR, supported by AI-enabled laboratory automation and expanding precision diagnostics.

Top Growth Drivers: Molecular diagnostics adoption exceeds 18%, laboratory automation improves workflow by 30%, and point-of-care testing expands over 20% across healthcare systems.

Short-Term Forecast: By 2028, laboratory processing efficiency increases nearly 25% while average diagnostic turnaround time declines around 20%.

Emerging Technologies: AI diagnostics, digital pathology, and next-generation sequencing accelerate high-throughput testing with automation improving laboratory productivity by approximately 35%.

Regional Leaders: North America exceeds USD 7.4 billion, Europe approaches USD 5.8 billion, and Asia-Pacific surpasses USD 5.2 billion through expanding localized manufacturing and digital healthcare adoption.

Consumer/End-User Trends: More than 55% of hospitals prioritize integrated diagnostic platforms supporting faster clinical decision-making and connected laboratory ecosystems.

Pilot/Case Example: In 2025, automated laboratory deployment reduced manual processing errors by approximately 28% while increasing testing throughput by 32%.

Competitive Landscape: Leading supplier holds about 15% market share, with major competition from Roche, Abbott, Siemens Healthineers, Danaher, and Sysmex amid regional manufacturing expansion.

Regulatory & ESG Impact: Digital compliance initiatives reduce documentation time by nearly 22%, while sustainable laboratory operations lower packaging waste by approximately 18%.

Investment & Funding: Global investment exceeds USD 4 billion, driven by strategic partnerships, manufacturing expansion, and advanced diagnostic platform commercialization amid supply-chain diversification.

Innovation & Future Outlook: Multiplex testing, AI-assisted clinical interpretation, and decentralized diagnostics strengthen next-generation healthcare delivery through faster, connected, and data-driven testing.

The vitro diagnostics market continues expanding across infectious disease detection, oncology screening, genetic testing, and chronic disease monitoring, with AI-assisted interpretation improving laboratory productivity by nearly 30%. Multiplex assay platforms and portable diagnostic systems are reshaping testing environments, while regulatory alignment and regional supply-chain diversification in 2026 support faster commercialization, creating a strong foundation for the following strategic market assessment.

The vitro diagnostics market has become strategically significant as healthcare providers prioritize faster clinical decisions, resilient laboratory operations, and data-driven disease management. Competitive advantage increasingly depends on integrated diagnostic ecosystems that combine automation, molecular testing, and digital connectivity. A major industry shift is ongoing supply-chain restructuring, with manufacturers expanding localized production and dual-sourcing strategies to reduce procurement disruptions while strengthening regulatory compliance and delivery reliability.

Modern AI-assisted laboratory analyzers process sample workflows up to 35% faster than conventional manual systems while reducing repeat testing by approximately 20%, lowering operational costs and improving diagnostic consistency. The United States continues leading high-value innovation through precision diagnostics and digital laboratory infrastructure, whereas China is expanding large-scale reagent manufacturing and automated instrument production to improve domestic supply resilience. Over the next two to three years, automated laboratory deployment is expected to exceed 60% across leading hospital networks, supported by increasing interoperability between diagnostic platforms and electronic health records.

A practical example is the deployment of fully automated molecular diagnostic laboratories capable of integrating sample preparation, analysis, and reporting within unified digital workflows, reducing manual intervention while increasing throughput. Companies are responding through manufacturing expansion, strategic technology partnerships, and AI software integration to strengthen laboratory performance, enhance regulatory readiness, and secure long-term competitive positioning in an increasingly technology-driven diagnostics landscape.

Precision diagnostics and laboratory automation are reshaping healthcare delivery by improving testing speed, accuracy, and operational efficiency. More than 65% of tertiary hospitals are increasing investments in automated laboratory systems, while molecular diagnostic testing volumes continue expanding by approximately 18% annually across major healthcare networks. In the United States, modernization initiatives encourage broader adoption of AI-assisted diagnostic platforms that reduce manual workflow requirements by nearly 30%. This operational shift enables laboratories to process higher testing volumes with greater consistency. Companies are expanding manufacturing capacity, strengthening software partnerships, and introducing integrated diagnostic platforms that combine automation, analytics, and connectivity, creating stronger competitive differentiation and improving long-term laboratory productivity.

High capital expenditure and uneven laboratory infrastructure remain significant barriers to wider deployment of advanced vitro diagnostics technologies. Automated diagnostic platforms typically require 25–35% higher initial investment than conventional laboratory equipment, while reagent import dependence exceeds 40% in several developing healthcare systems. Ongoing supply-chain volatility also affects component availability for specialized instruments, extending procurement timelines and increasing operational costs. These structural constraints limit deployment in secondary hospitals and independent laboratories while compressing profitability for suppliers. Companies are responding by localizing reagent production, negotiating long-term procurement contracts, and expanding regional manufacturing partnerships to improve supply stability, reduce import exposure, and strengthen deployment economics.

Next-generation decentralized diagnostics integrated with artificial intelligence present substantial opportunities beyond traditional laboratory environments. AI-assisted clinical interpretation improves diagnostic workflow efficiency by approximately 30%, while connected point-of-care testing reduces reporting time by nearly 40%. Japan and South Korea are accelerating digital healthcare policies supporting interoperable diagnostic infrastructure and remote patient monitoring. Companies are investing in cloud-enabled diagnostic platforms, multiplex molecular assays, and strategic collaborations with digital health providers to expand ecosystem capabilities. An emerging opportunity lies in integrating diagnostic data with predictive healthcare analytics, enabling earlier disease intervention, optimized resource allocation, and stronger clinical decision support across both hospital and community healthcare settings.

Long-term market expansion depends on successful integration of advanced diagnostic technologies across diverse healthcare infrastructures. More than 45% of laboratories continue operating mixed legacy and digital systems, while cybersecurity incidents affecting healthcare organizations have increased by over 20%, placing greater emphasis on secure diagnostic data management. In Germany and the United States, interoperability between laboratory information systems and hospital platforms remains a significant operational challenge despite ongoing digital modernization. Companies must invest in standardized software architecture, workforce training, secure cloud infrastructure, and cross-platform integration capabilities. Organizations that solve deployment complexity while maintaining regulatory compliance will achieve stronger operational resilience and sustainable competitive advantage.

AI-Enabled Laboratory Automation AI-assisted diagnostic platforms are reducing sample processing time by nearly 35% while improving result consistency by approximately 20%. Large hospital networks in the United States are integrating predictive workflow software to address laboratory staffing shortages. Companies are expanding AI partnerships and embedding analytics into core diagnostic platforms to increase throughput, optimize instrument utilization, and strengthen enterprise-wide laboratory standardization.

Localized Manufacturing Expansion Supply-chain diversification continues reshaping procurement strategies as manufacturers increase regional production, with localized reagent output rising by approximately 25% and average delivery times improving by nearly 18%. China and India are expanding domestic manufacturing to reduce import dependence following recent supply disruptions. Companies are restructuring supplier networks, investing in multi-site production, and strengthening inventory resilience to ensure uninterrupted diagnostic operations.

Integrated Molecular Testing Platforms Multiplex molecular diagnostic systems now reduce laboratory workflow steps by around 30% while increasing testing capacity by approximately 28%. Regulatory emphasis on faster infectious disease preparedness has accelerated deployment of integrated sample-to-answer platforms across reference laboratories. Companies are scaling automated testing portfolios, expanding software compatibility, and forming technology collaborations to simplify deployment while supporting higher testing accuracy and operational flexibility.

Connected Point-of-Care Ecosystems Digital connectivity between point-of-care devices and hospital information systems has increased by nearly 40%, reducing manual reporting errors by approximately 22%. Enterprise healthcare providers are standardizing cloud-enabled diagnostic workflows to improve decentralized testing oversight. Companies are investing in interoperable software architectures, remote device management, and secure data integration, enabling faster clinical decisions while creating new recurring service opportunities beyond instrument sales.

Reagents & Kits remain the largest segment, accounting for approximately 46% of the vitro diagnostics market because of their recurring purchasing cycle, compatibility with multiple testing platforms, and indispensable role in routine and specialized diagnostics. Continuous utilization across infectious disease screening, oncology, and chronic disease management sustains stable procurement volumes. Consumables support uninterrupted laboratory operations through high-frequency replacement, while Instruments continue benefiting from automation upgrades and laboratory modernization initiatives. Manufacturers are strengthening production capacity, introducing higher-performance assay portfolios, and expanding distribution partnerships to improve product availability and customer retention.

Software & Services represent the fastest-growing segment as healthcare providers prioritize digital laboratory management and AI-assisted workflow optimization. Adoption of laboratory informatics platforms has increased by nearly 32%, while cloud-enabled workflow management reduces reporting delays by approximately 20%. Companies are integrating software with diagnostic instruments, expanding subscription-based service models, and strengthening digital ecosystems that improve interoperability, compliance, and operational efficiency. Investment priorities increasingly favor connected laboratory platforms capable of supporting scalable diagnostics across complex healthcare environments.

Infectious Disease Testing remains the leading application, representing approximately 34% of the vitro diagnostics market due to sustained surveillance programs, rapid pathogen detection requirements, and routine hospital screening protocols. Molecular Diagnostics is the fastest-growing application, with deployment increasing by roughly 24% as precision medicine and genomic testing become increasingly integrated into clinical practice. Clinical Chemistry continues supporting high-volume routine diagnostics, while Immunodiagnostics strengthens demand across oncology and autoimmune disease management. Blood Testing remains essential for emergency medicine, preventive healthcare, and transfusion support across healthcare systems.

Companies are expanding multiplex testing capabilities, integrating automated sample preparation, and deploying connected diagnostic platforms that improve laboratory efficiency. AI-assisted interpretation has reduced laboratory turnaround time by approximately 18%, enabling faster clinical decision-making and increased testing throughput. Strategic investment increasingly focuses on scalable diagnostic systems capable of supporting multiple clinical applications while improving workflow consistency and laboratory resource utilization.

Diagnostic Laboratories account for approximately 42% of total market demand, supported by centralized testing infrastructure, high daily sample volumes, and extensive deployment of automated analytical systems. Hospitals remain the second-largest purchasing group through continuous inpatient, outpatient, and emergency diagnostic requirements. Pharmaceutical Companies represent the fastest-growing end-user segment as biomarker development, companion diagnostics, and clinical trial testing activities expand by nearly 22%. Research Institutes and Academic Institutions continue advancing assay validation, translational research, and diagnostic innovation supporting future product development.

Manufacturers are introducing customized reagent packages, integrated software solutions, and long-term service agreements designed for large laboratory networks and hospital systems. Laboratory automation has improved operational throughput by approximately 30%, encouraging buyers to prioritize scalable platforms with digital connectivity and lifecycle support. Strategic collaborations with pharmaceutical companies and research organizations are strengthening product innovation while expanding specialized diagnostic capabilities across precision medicine and clinical research applications.

North America accounted for the largest market share at 39.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.9% CAGR between 2026 and 2033.

Advanced Laboratory Automation Driving Market Leadership

North America remains the leading regional market due to its mature healthcare infrastructure, strong diagnostic manufacturing base, and rapid deployment of automated laboratory technologies. The region contributes nearly 39% of global demand, supported by widespread adoption of molecular diagnostics, AI-enabled laboratory information systems, and high-throughput testing platforms. More than 70% of large hospital laboratories have integrated automated sample handling systems, improving workflow efficiency and reducing manual intervention. Enterprise partnerships between healthcare providers and diagnostic technology companies continue accelerating digital laboratory modernization, while expanding decentralized testing capabilities improve access across community healthcare networks. Continuous investment in precision diagnostics and advanced clinical laboratory infrastructure reinforces the region's competitive advantage and supports sustained technology deployment across public and private healthcare systems.

United States Market Outlook: The United States serves as the region's innovation center through extensive biotechnology capabilities, advanced hospital infrastructure, and strong deployment of precision diagnostics. More than 75% of large clinical laboratories operate automated diagnostic workflows, while increasing investment in AI-supported diagnostic interpretation continues improving testing efficiency. Domestic manufacturers are expanding production capacity, strengthening digital diagnostic ecosystems, and forming strategic partnerships with healthcare providers to accelerate commercialization and support long-term laboratory modernization.

Regulatory Harmonization Accelerating Digital Diagnostics

Europe maintains a strong position through advanced healthcare systems, standardized regulatory frameworks, and widespread adoption of laboratory automation. The region represents approximately 27% of global market activity, supported by growing implementation of digital pathology, molecular diagnostics, and connected laboratory information systems. More than 60% of reference laboratories have upgraded automated workflow infrastructure to improve testing consistency and regulatory compliance. Healthcare organizations continue modernizing diagnostic facilities while manufacturers expand regional production and software integration capabilities to strengthen operational resilience. Sustainability initiatives encouraging resource-efficient laboratory operations are also influencing procurement decisions across public healthcare institutions.

Germany Market Outlook: Germany leads the European market through its strong medical technology industry, advanced manufacturing capabilities, and highly standardized laboratory infrastructure. Large diagnostic laboratories continue investing in integrated automation platforms and digital quality management systems, with automated laboratory deployment exceeding 65% across leading clinical networks. Domestic innovation, engineering expertise, and close collaboration between healthcare providers and technology developers strengthen Germany's leadership in advanced diagnostic solutions.

Manufacturing Scale and Healthcare Expansion Fuel Adoption

Asia-Pacific is emerging as the fastest-expanding regional market, supported by expanding healthcare infrastructure, large-scale diagnostic manufacturing, and increasing investment in laboratory modernization. The region accounts for approximately 25% of global demand while maintaining the highest production growth across diagnostic consumables and reagents. Local manufacturing output has increased by nearly 28% as companies diversify supply chains and strengthen regional production hubs. Governments continue investing in hospital infrastructure, digital healthcare systems, and disease surveillance programs, encouraging broader deployment of automated diagnostic technologies. Enterprise partnerships and localized production strategies are improving product availability while reducing procurement dependence on imported diagnostic components.

China Market Outlook: China has established itself as the region's largest manufacturing and deployment center through extensive production capacity, government-backed healthcare modernization, and expanding domestic innovation. Local manufacturers now supply more than 60% of routine diagnostic consumables used within the country, while investments in automated laboratory equipment and molecular diagnostics continue increasing. Strong industrial capabilities and integrated supply chains position China as a key global production and export hub for vitro diagnostics technologies.

Healthcare Modernization Supporting Diagnostic Expansion

South America continues strengthening its diagnostic capabilities through healthcare infrastructure upgrades, expanded laboratory networks, and increasing adoption of automated testing platforms. The region contributes approximately 5% of global market activity, with public healthcare investments supporting broader access to infectious disease diagnostics and clinical laboratory services. Laboratory automation has improved testing capacity by nearly 18% across major urban healthcare facilities. Despite continued dependence on imported diagnostic technologies, manufacturers are expanding regional partnerships, local distribution networks, and technical support capabilities to improve operational efficiency and supply continuity while addressing infrastructure disparities between metropolitan and rural healthcare systems.

Brazil Market Outlook: Brazil remains the region's largest market due to its extensive healthcare network, expanding diagnostic laboratory sector, and growing investment in molecular testing capabilities. Large private laboratory groups continue modernizing testing infrastructure while increasing deployment of automated analyzers. National healthcare programs supporting disease surveillance and preventive diagnostics encourage sustained procurement of advanced diagnostic solutions and strengthen long-term market opportunities.

Healthcare Infrastructure Investment Reshaping Diagnostics

The Middle East & Africa market is advancing through significant healthcare infrastructure investment, laboratory modernization, and expansion of specialized diagnostic services. The region contributes approximately 4% of global demand while increasing deployment of automated laboratory technologies within tertiary healthcare facilities. Hospital modernization initiatives have increased installation of advanced diagnostic platforms by nearly 20% across major healthcare projects. Governments continue prioritizing localized healthcare capabilities, digital health integration, and strategic partnerships with international diagnostic manufacturers to strengthen testing capacity and improve operational resilience. These investments are gradually reducing dependence on overseas laboratory services while enhancing regional diagnostic preparedness.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through large-scale healthcare transformation programs, expanding hospital infrastructure, and sustained investment in advanced diagnostic technologies. Public and private healthcare providers are increasing deployment of automated laboratory systems and digital pathology solutions, while national healthcare initiatives continue strengthening local diagnostic capacity. Strategic partnerships with global technology companies and continued investment in specialized medical infrastructure position the country as the regional leader in advanced vitro diagnostics adoption.

The competitive landscape is led by Roche, Abbott, Siemens Healthineers, Danaher, and Sysmex, which compete directly on integrated diagnostic ecosystems, while regional manufacturers challenge them through lower-cost reagents, localized production, and faster customer support. Global technology leaders increasingly compete against agile domestic suppliers in China and India, whereas OEMs compete with specialized software and automation providers to secure laboratory digitalization projects. The top five companies collectively control approximately 58% of the global market, supported by broad product portfolios and established distribution networks. Competition centers on automation, diagnostic accuracy, supply reliability, and workflow integration, with AI-enabled platforms improving laboratory productivity by nearly 30% and localized manufacturing reducing delivery times by approximately 20%. Companies are expanding manufacturing capacity, pursuing technology partnerships, strengthening reagent portfolios, and vertically integrating software with instruments. The market is shifting toward connected diagnostics and platform-based solutions, while regulatory compliance and validation remain significant entry barriers. Winning requires scalable innovation, resilient supply chains, digital integration, and strong clinical support capabilities.

Roche

Abbott

Siemens Healthineers

Danaher Corporation

Sysmex Corporation

bioMérieux

Thermo Fisher Scientific

Becton, Dickinson and Company (BD)

Qiagen

Hologic

Agilent Technologies

Bio-Rad Laboratories

QuidelOrtho Corporation

Mindray

Advanced automation, artificial intelligence, and molecular diagnostics are redefining the vitro diagnostics market by improving testing speed, precision, and laboratory scalability. AI-assisted image interpretation reduces diagnostic review time by approximately 35%, while automated sample handling lowers manual processing errors by nearly 25%. More than 60% of large clinical laboratories are deploying integrated laboratory information systems that connect analyzers, quality management, and reporting workflows. These technologies improve operational consistency while enabling healthcare providers to process growing testing volumes without proportional workforce expansion.

Next-generation sequencing, multiplex molecular assays, and digital pathology are replacing conventional single-analyte testing across specialized clinical applications. Compared with legacy manual workflows, integrated molecular platforms improve laboratory throughput by approximately 40% while reducing repeat testing by nearly 20%. Large hospital networks, reference laboratories, and precision medicine providers gain the greatest competitive advantage because integrated diagnostic platforms support faster clinical decisions, standardized workflows, and better utilization of laboratory infrastructure. Companies continue integrating cloud connectivity, AI analytics, and remote instrument monitoring into enterprise diagnostic ecosystems.

Between 2026 and 2028, decentralized diagnostics, predictive analytics, and interoperable digital laboratory platforms will become primary investment priorities. Connected point-of-care systems, cybersecurity-enabled data management, and automated quality assurance are expected to exceed 50% deployment across advanced healthcare networks. Organizations adopting integrated diagnostic technologies early will strengthen operational resilience, accelerate regulatory compliance, optimize laboratory capacity, and establish sustainable competitive differentiation as digital healthcare ecosystems continue expanding globally.

January 2025 Roche received U.S. FDA clearance with CLIA waiver for its cobas liat multiplex STI molecular tests, delivering PCR-quality results in 20 minutes and expanding decentralized testing access. The approval strengthened Roche's point-of-care diagnostics portfolio and accelerated adoption in urgent care settings.

December 2025 Roche launched the next-generation cobas 6800/8800 systems in the United States, increasing laboratory throughput flexibility and enabling broader test consolidation through upgraded software. The platform enhanced operational efficiency for high-volume laboratories facing staffing and workflow pressures.

November 2025 Abbott announced its acquisition of Exact Sciences in a transaction valued at up to USD 23 billion, significantly expanding its cancer diagnostics portfolio. The strategic move strengthened Abbott's position in precision oncology screening and diversified long-term diagnostics capabilities.

March 2026 Roche received FDA 510(k) clearance for the cobas c 703 and cobas ISE neo analytical units, delivering up to 2,000 tests per hour with enhanced laboratory automation. The approval improved high-throughput clinical chemistry workflows while helping laboratories address staffing shortages.

The report delivers comprehensive analysis of the vitro diagnostics market across Reagents & Kits, Instruments, Consumables, and Software & Services, while evaluating key applications including Infectious Disease Testing, Clinical Chemistry, Immunodiagnostics, Molecular Diagnostics, and Blood Testing. It further examines demand across Hospitals, Diagnostic Laboratories, Research Institutes, Pharmaceutical Companies, and Academic Institutions. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic evaluation of country-level deployment patterns, manufacturing capabilities, and technology adoption.

The study assesses competitive positioning of leading manufacturers, emerging innovators, and regional suppliers while examining automation, artificial intelligence, molecular diagnostics, digital pathology, and connected laboratory ecosystems. It incorporates operational indicators including laboratory automation adoption exceeding 60% in advanced healthcare networks and increasing digital workflow integration across major diagnostic facilities. The report supports investment planning, product expansion, partnership strategies, supply-chain optimization, competitive benchmarking, and long-term business decisions by identifying technology priorities, evolving customer demand, and strategic opportunities expected to shape the market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 12820 Million |

Market Revenue in 2033 | USD 19764.37 Million |

CAGR (2026 - 2033) | 5.56% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Roche, Abbott, Siemens Healthineers, Danaher Corporation, Sysmex Corporation, bioMérieux, Thermo Fisher Scientific, Becton, Dickinson and Company (BD), Qiagen, Hologic, Agilent Technologies, Bio-Rad Laboratories, QuidelOrtho Corporation, Mindray |

Customization & Pricing | Available on Request (10% Customization is Free) |