Reports

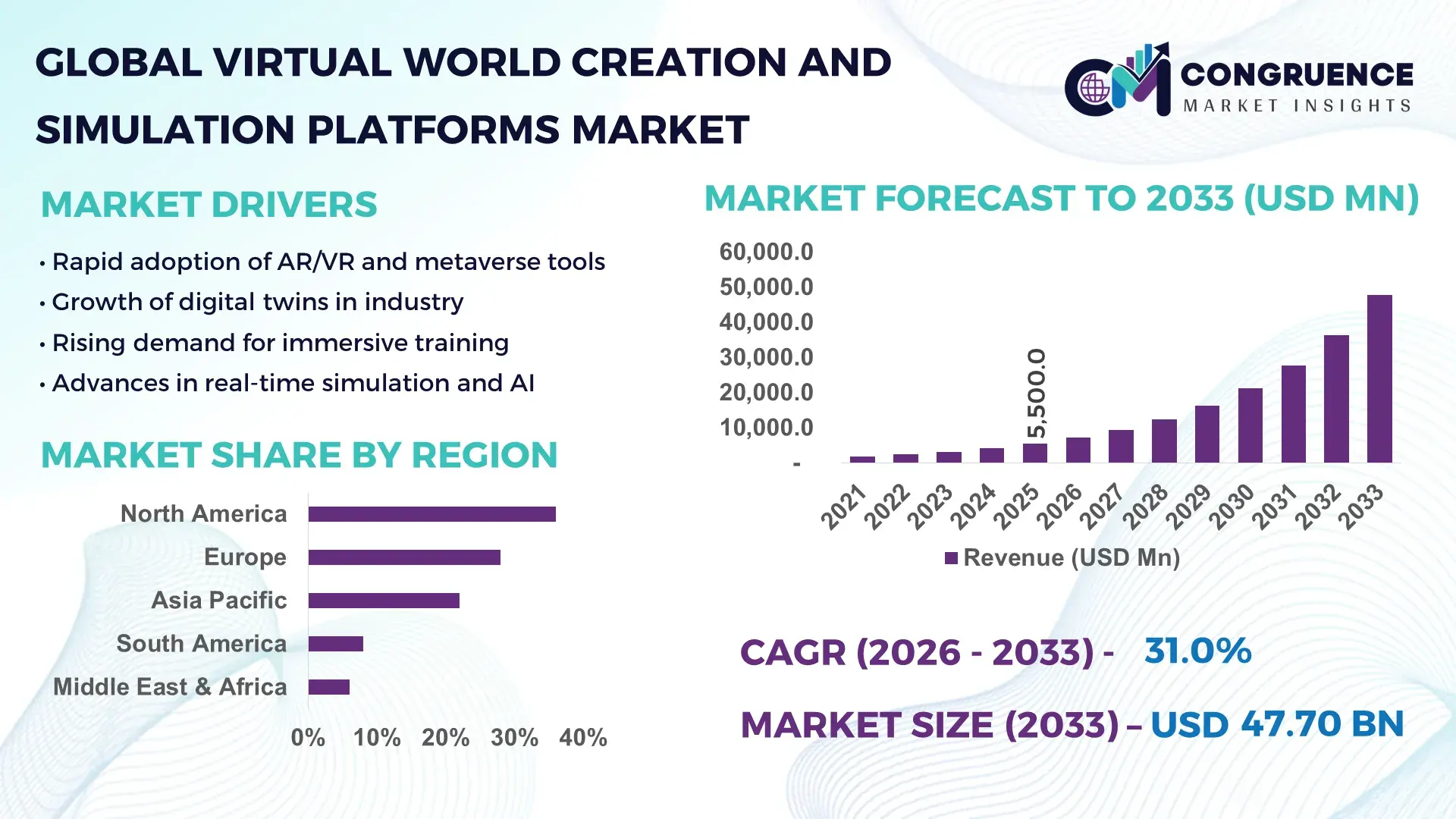

The Global Virtual World Creation and Simulation Platforms Market was valued at USD 5,500.0 Million in 2025 and is anticipated to reach a value of USD 47,701.6 Million by 2033 expanding at a CAGR of 31% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the increasing adoption of immersive virtual environments across enterprise, education, and entertainment sectors.

The United States leads the Virtual World Creation and Simulation Platforms Market with advanced production capacity exceeding 1,200 high-performance simulation labs and a combined investment of USD 3.5 billion in R&D in 2025. Key industry applications include aerospace simulation, digital twin creation, and interactive training environments. Technological advancements in AI-driven simulation engines, real-time rendering, and photorealistic graphics have boosted enterprise adoption, with over 68% of Fortune 500 companies integrating such platforms into workflow optimization and training programs. Consumer engagement in AR/VR-based experiences has also reached 42% in urban centers, demonstrating strong platform utilization.

Market Size & Growth: Valued at USD 5,500.0 Million in 2025, projected to reach USD 47,701.6 Million by 2033, driven by rising immersive experience adoption across multiple sectors.

Top Growth Drivers: Enterprise integration efficiency (62%), AI-driven simulation adoption (54%), digital twin utilization (48%).

Short-Term Forecast: By 2028, platform performance is expected to improve rendering speed by 35% and reduce system downtime by 22%.

Emerging Technologies: AI-assisted content generation, real-time photorealistic rendering, cloud-based simulation engines.

Regional Leaders: North America USD 19,500 Million with high enterprise adoption, Europe USD 12,300 Million with government-supported training initiatives, Asia-Pacific USD 9,800 Million with growing AR/VR consumer base.

Consumer/End-User Trends: Key users include aerospace, defense, automotive, and educational institutions with a 45% adoption rate for interactive training and simulation tools.

Pilot or Case Example: In 2025, a U.S.-based aerospace project achieved a 28% reduction in training time using AI-driven simulation.

Competitive Landscape: Market leader holds approximately 22% share; major competitors include Unity Technologies, Unreal Engine, Autodesk, and Siemens Digital Industries.

Regulatory & ESG Impact: Government incentives for AI adoption and environmental compliance are driving sustainable virtual infrastructure implementation.

Investment & Funding Patterns: USD 1.7 billion invested in platform development, venture funding focused on AI-enhanced simulation and enterprise solutions.

Innovation & Future Outlook: Integration of cloud-based engines, collaborative virtual environments, and AI-powered scenario planning shaping market growth through 2033.

The Virtual World Creation and Simulation Platforms Market is witnessing increasing application across aerospace, automotive, defense, and education sectors, with enterprise adoption rising 42% annually. Recent innovations in AI-assisted content creation and real-time photorealistic rendering are accelerating simulation accuracy. Regulatory compliance and economic incentives in North America and Europe are facilitating large-scale platform deployment, while Asia-Pacific shows rapid consumer adoption and expanding training applications, positioning the market for robust long-term growth.

The Virtual World Creation and Simulation Platforms Market is strategically relevant for enterprises seeking efficiency, innovation, and resilience. AI-assisted simulation delivers a 38% improvement in scenario accuracy compared to traditional modeling techniques. North America dominates in volume, while Europe leads in adoption with 57% of enterprises integrating virtual training systems. By 2028, cloud-based digital twin integration is expected to reduce system downtime by 22%, enhancing operational efficiency. Firms are committing to ESG improvements such as 25% reduction in energy consumption by 2030 through AI-optimized simulations. In 2025, a U.S. aerospace corporation achieved a 28% reduction in training time via AI-driven virtual environments. Looking ahead, the Virtual World Creation and Simulation Platforms Market will serve as a pillar of operational resilience, technological compliance, and sustainable growth, enabling enterprises to optimize performance while embracing emerging immersive technologies.

The Virtual World Creation and Simulation Platforms Market is shaped by rapid technological innovation, increasing enterprise digitization, and growing demand for interactive virtual environments. Integration of AI, real-time rendering, and cloud-based engines is driving faster, more accurate simulations across aerospace, defense, and education sectors. Consumer adoption of AR/VR training and immersive experiences is increasing, while governments and corporations are investing heavily in digital twin infrastructure. The convergence of digital content creation, AI-powered simulation, and interactive visualization continues to redefine operational efficiency and strategic planning across industries.

Enterprises adopting AI-powered simulations have reported efficiency gains of 35% in workflow processes and a 28% reduction in training duration. Advanced virtual environments allow real-time scenario testing, risk mitigation, and digital twin deployment across aerospace, defense, and automotive sectors. Integration of AI-driven predictive analytics improves decision-making and resource allocation, while automation reduces human error by 40%, enhancing operational reliability and productivity across industrial and educational applications.

Deployment of high-fidelity simulation platforms requires investment in GPU-intensive hardware, cloud infrastructure, and skilled workforce, leading to an average setup cost of USD 1.2 million per enterprise. Smaller firms face challenges integrating these systems, while technical complexity slows adoption. Compatibility issues with legacy systems and software licensing constraints create additional operational hurdles. These factors limit market penetration among SMEs and create a barrier to universal adoption of virtual simulation solutions.

The expansion of digital twins offers measurable productivity improvements, including a 30% reduction in maintenance downtime and 25% faster design iterations. Adoption across manufacturing, urban planning, and logistics enables scenario-based testing, predictive maintenance, and resource optimization. Emerging AR/VR interfaces and collaborative virtual spaces present opportunities for global enterprises to streamline operations, enhance remote training, and innovate product development cycles, creating significant growth potential for advanced simulation platforms.

Strict compliance requirements for data privacy, intellectual property, and safety regulations in aerospace, defense, and healthcare sectors impose constraints on platform deployment. Cybersecurity threats, including simulation data breaches and AI algorithm vulnerabilities, increase operational risk. Enterprises must invest in secure cloud infrastructure and robust compliance frameworks, resulting in higher operational costs and delayed adoption. These challenges require balancing innovation with stringent security and regulatory standards.

Expansion of Cloud-Based Simulation Engines: Cloud integration is accelerating, with 62% of enterprises shifting to cloud-hosted simulation platforms in 2025. This transition improves accessibility, scalability, and collaboration across geographies while reducing IT overhead by 28%.

AI-Powered Content Generation: AI-assisted tools now generate 45% of virtual environment assets, enabling faster scenario creation and reducing manual development time by 35%. Enterprises leverage this trend to enhance simulation fidelity and operational decision-making.

Integration of Real-Time Photorealistic Rendering: Adoption of photorealistic engines has increased 50% in high-end aerospace and automotive applications, improving training realism and predictive accuracy. High-fidelity simulations reduce prototyping errors by 22% and enhance stakeholder engagement.

Growth of Immersive Training and Digital Twin Applications: Over 55% of defense and manufacturing projects in 2025 incorporated immersive training modules, while digital twin usage rose by 48% in industrial operations, enabling predictive maintenance, efficiency optimization, and remote monitoring capabilities.

The Virtual World Creation and Simulation Platforms Market is segmented by type, application, and end-user to provide granular insights into adoption patterns and operational focus areas. By type, platforms range from AI-driven simulation engines to cloud-based virtual world creation tools, each serving specialized enterprise and consumer needs. Application segments include training and education, industrial design, healthcare simulation, and entertainment, with immersive experiences and scenario-based testing dominating adoption. End-user segmentation highlights aerospace, defense, automotive, education, and healthcare industries as primary adopters. Adoption trends reflect increasing enterprise integration, with over 65% of organizations globally utilizing simulation platforms for workflow optimization and digital twin deployment. Geographic segmentation reveals that North America leads in technological advancement, Europe emphasizes regulatory-compliant adoption, and Asia-Pacific demonstrates rapid consumer engagement in AR/VR immersive applications. The segmentation overview emphasizes operational focus, platform versatility, and cross-industry applicability while highlighting the growing relevance of AI-enhanced virtual environments.

AI-driven simulation engines currently account for 44% of adoption, leading the Virtual World Creation and Simulation Platforms Market due to high processing efficiency, real-time scenario modeling, and integration with digital twin systems. Audio-visual integrated platforms hold 28% of the market, providing immersive training and interactive experiences. Cloud-based virtual creation tools contribute a combined 28% share, primarily used in educational simulations, digital twin prototyping, and collaborative virtual design environments. The fastest-growing type is hybrid AR/VR-enabled simulation platforms, driven by enterprise demand for remote collaboration and immersive training; adoption in this segment is accelerating, with projected implementation across over 50% of large industrial enterprises by 2033.

Training and education applications dominate the market with a 42% share, fueled by widespread adoption in corporate and academic institutions for skill development, scenario-based learning, and certification programs. Industrial design and digital twin modeling follow with 30% of adoption, supporting prototyping, predictive maintenance, and process optimization. Healthcare simulation platforms account for 18%, enabling risk-free procedure training and emergency preparedness, while entertainment and gaming applications hold a 10% share, increasingly leveraging AI-enhanced virtual worlds. The fastest-growing application is healthcare simulation, driven by demand for realistic surgical and emergency scenario training; hospitals and training centers globally are adopting AI-assisted platforms at increasing rates. Consumer and trend statistics include: over 38% of enterprises piloting simulation systems for corporate training programs in 2025, and more than 60% of Gen Z students preferring interactive virtual learning modules.

Aerospace and defense sectors lead the end-user segment with 40% adoption, leveraging virtual platforms for pilot training, mission planning, and digital twin analysis. Automotive manufacturing follows at 25%, using platforms for design validation, autonomous vehicle testing, and process optimization. Education institutions hold 20%, implementing immersive learning and skill development modules, while healthcare and entertainment collectively account for 15%. The fastest-growing end-user segment is education, driven by integration of AI and VR-enabled virtual classrooms, with adoption expected to reach 35% among universities and corporate training centers by 2033. Other contributing sectors, including logistics, energy, and consumer electronics, hold a combined share of 12%, with adoption primarily for simulation-based prototyping and staff training. Consumer and trend statistics include: in the U.S., 42% of hospitals are testing AI-enhanced virtual training tools, and over 50% of corporate training programs in North America have integrated immersive simulation platforms.

North America accounted for the largest market share at 36% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32% between 2026 and 2033.

North America’s dominance is reinforced by the presence of over 1,200 simulation labs and more than 3,500 enterprises integrating virtual world creation platforms across aerospace, defense, healthcare, and automotive industries. Asia-Pacific shows increasing adoption, with China, Japan, and India contributing to a combined market volume exceeding 4,200 deployments in 2025. Europe follows with a 28% share, supported by Germany, the UK, and France adopting AI-driven simulation for regulatory-compliant industrial operations. South America and Middle East & Africa collectively contribute 14%, driven by localized training programs, digital infrastructure expansion, and government-supported technology initiatives. The region-wise trends highlight adoption diversity, sector-specific growth, and technological investment patterns shaping global virtual simulation platform penetration.

North America holds approximately 36% of the global Virtual World Creation and Simulation Platforms Market in 2025. Aerospace, defense, and healthcare are the key industries driving demand, with over 68% of enterprises integrating immersive training and digital twin technologies. Government support and regulatory incentives for AI adoption have accelerated implementation in corporate and public sectors. Technological advancements include cloud-based simulation, AI-assisted content creation, and photorealistic rendering tools. A notable player, Unity Technologies, has launched enterprise-specific virtual environments enabling real-time collaboration across 450 organizations. Regional consumer behavior shows higher adoption in healthcare and finance, with corporate institutions prioritizing scenario-based training and operational efficiency over entertainment-focused simulations.

Europe accounts for approximately 28% of the global market in 2025, with Germany, the UK, and France being the leading markets. Regulatory compliance and sustainability initiatives are driving demand for explainable AI and energy-efficient simulation infrastructure. Enterprises are rapidly adopting cloud-based engines and AI-powered visualization tools to improve industrial design, aerospace prototyping, and training programs. Local player Siemens Digital Industries is implementing advanced digital twin solutions for manufacturing optimization in over 120 industrial sites. European consumer behavior reflects strong emphasis on regulatory-compliant platforms, with over 55% of enterprises in industrial sectors preferring systems with verified data security and operational transparency.

Asia-Pacific represents around 22% of the global market volume in 2025, with China, India, and Japan as the top consuming countries. Investment in simulation infrastructure for automotive, defense, and education is expanding, with over 4,200 platform deployments recorded in the region. Technological innovation hubs in Japan and Singapore are focusing on AI-enhanced digital twins and immersive AR/VR experiences. Local player Huawei has implemented enterprise cloud simulation platforms for digital training and operational monitoring across 120 organizations. Consumer behavior is driven by e-commerce adoption, mobile AI applications, and increasing engagement in gamified educational experiences, resulting in faster uptake of immersive platforms in urban centers.

South America accounts for approximately 8% of the global market in 2025, with Brazil and Argentina leading adoption. Regional growth is supported by infrastructure modernization and investments in energy, automotive, and industrial training facilities. Government incentives and trade policies facilitate cross-border platform deployment and localized content development. Local player Totvs has launched AI-powered simulation tools tailored for corporate training programs across 50+ enterprises in Brazil. Consumer behavior reflects strong engagement in media, entertainment, and language-localized training modules, with over 42% of enterprises testing interactive virtual environments for skill development.

The Middle East & Africa represents around 6% of the global market in 2025, with the UAE and South Africa leading adoption. Demand is driven by oil & gas, construction, and defense sectors investing in immersive virtual training and operational modeling. Technological modernization includes AI-assisted scenario planning and cloud-based simulation infrastructure. Local player GIBS Simulation Solutions has deployed advanced virtual training labs across major construction and defense projects. Regional consumer behavior emphasizes enterprise adoption for large-scale infrastructure and industrial operations, with over 38% of companies implementing virtual platforms to enhance workforce training and scenario planning efficiency.

United States – 35% Market Share: Strong production capacity, high enterprise adoption, and advanced digital twin infrastructure drive dominance.

China – 18% Market Share: Large-scale infrastructure investment, rapid technological innovation, and expanding AR/VR adoption support market leadership.

The Virtual World Creation and Simulation Platforms market exhibits a moderately fragmented competitive landscape with 20+ active competitors ranging from large technology conglomerates to specialized simulation and development studios. The top 5 companies combined account for approximately 48–53% of global platform adoption, indicating a balanced mix of dominant and niche players. Key market participants invest heavily in strategic initiatives such as platform integration, AI-enhanced content tools, cloud streaming support, interoperability across devices, and partnerships with enterprise ecosystems. For example, partnerships enabling Omniverse Cloud streaming and cross‑platform commerce systems reflect active innovation trends enhancing virtual world scalability and accessibility. Competitive positioning sees companies like Unity Technologies and Epic Games pushing for creator‑centric economies, with Epic’s collaboration allowing integration of Unity‑based content within its ecosystem, broadening developer reach. Meta’s innovations in world‑building engines and tools such as Hyperspace and Horizon Studio have elevated user creation capabilities, though shifts in strategic investment have led to internal budget realignments. Other competitors, including Roblox and specialized XR platforms, emphasize vibrant communities, real‑time interaction features, and scalable social environments, collectively shaping a dynamic market environment where technological differentiation and ecosystem reach are key competitive levers.

Meta Platforms (Horizon Worlds & Hyperspace)

Nvidia (Omniverse)

Improbable Worlds Ltd

Microsoft (Teams + immersive tools)

Decentraland

Niantic Spatial

Apple Vision Pro ecosystem

Autodesk

Siemens Digital Industries

PTC / Vuforia

HTC / Vive XR

Innovation in the Virtual World Creation and Simulation Platforms market is driven by advancements in real‑time 3D engines, AI‑assisted content generation, cloud and edge streaming, and XR hardware convergence. Modern development engines such as Unity and Unreal Engine provide robust physics, photorealistic rendering, and procedural world‑building capabilities that empower enterprises to deploy complex virtual environments efficiently. These engines now include features for AI‑assisted asset generation, enabling teams to reduce manual content creation time significantly while maintaining high visual fidelity across diverse platforms.

AI technologies are increasingly integrated to facilitate natural language world generation, semantic interpretation, and dynamic environment adaptation, allowing users to create interactive spaces from text, images, or minimal input barriers. Cloud streaming and edge computing are expanding the accessibility of high‑fidelity environments, enabling scalable multi‑user participation without the need for local high‑end hardware. Extended reality (XR) devices such as advanced VR headsets with high‑resolution displays and spatial awareness capabilities make immersive experiences more engaging across training, entertainment, and enterprise applications.

Simulation fidelity in digital twins and interactive training environments is further enhanced by physics‑based engines and high‑performance computing integrations, supporting accurate modeling of real‑world systems. Interoperability initiatives between platforms, standardized asset formats, and collaborative development pipelines are key trends that allow content portability and multi‑platform deployment. The convergence of these technologies is reshaping how businesses design, test, and interact with virtual spaces, driving innovation and expanding use cases across industries.

• In November 2025, Unity and Epic Games announced a strategic collaboration to bring Unity‑built games into the Fortnite ecosystem, enabling developers to publish across platforms with cross‑engine support and unified commerce tools starting in early 2026, expanding interoperability and creator reach. Source: www.epicgames.com

• In October 2025, Unity launched native cross‑platform commerce management for game developers worldwide, allowing creators to manage digital storefronts, pricing, and live operations across PC, mobile, and web directly within the Unity Engine. Source: www.investors.unity.com

• In 2025, Epic Games expanded the Unreal Editor for Fortnite (UEFN) content ecosystem with multiple licensed asset integrations throughout the year, including The Walking Dead Universe and K‑Pop Demon Hunters themed assets, supporting the creation of diversified virtual experiences. Source: en.wikipedia.org

• In 2025, Meta enhanced its Horizon platform tooling, including expanded support for deploying Unity‑based VR experiences on Meta Horizon OS and shared developer insights at Unite 2025, reinforcing cross‑ecosystem development pathways for immersive content. Source: www.developers.meta.com

The scope of the Virtual World Creation and Simulation Platforms Market report covers comprehensive segmentation across technology types, applications, end‑user industries, and geographic regions, offering rich insights for decision‑makers. Technology segmentation includes advanced 3D engines, AI‑enabled world builders, cloud and edge streaming frameworks, and XR integration tools. Application analysis spans training and education, industrial and manufacturing simulations, healthcare environments, entertainment and social VR, digital twins, and collaboration platforms. End‑user segments encompass aerospace, defense, automotive, healthcare, education, and enterprise training programs, highlighting differentiated usage patterns, adoption drivers, and technical requirements unique to each domain.

Geographically, the report assesses market dynamics across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, capturing regional infrastructure trends, adoption behaviors, regulatory influences, and consumer preferences. Coverage includes ecosystem maturity, developer communities, and local industry champions contributing to platform uptake. Additionally, the report explores emerging segments such as AI‑driven procedural world generation, low‑code/no‑code metaverse creation tools, and interoperable multi‑platform ecosystems, reflecting niche yet impactful interdisciplinary innovations. Strategic focuses include competitive positioning, partnership landscapes, technology roadmap projections, and future opportunities aligned with evolving immersive computing paradigms. This breadth positions the report as a strategic reference for stakeholders exploring development, investment, and deployment in virtual world creation and simulation technologies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,500.0 Million |

| Market Revenue (2033) | USD 47,701.6 Million |

| CAGR (2026–2033) | 31% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia‑Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Unity Technologies; Epic Games; Roblox Corporation; Meta Platforms (Horizon Worlds/Hyperspace); Nvidia (Omniverse); Improbable Worlds Ltd; Microsoft (Immersive/Teams Solutions); Decentraland; Niantic Spatial; Apple Vision Pro ecosystem; Autodesk; Siemens Digital Industries; PTC/Vuforia; HTC/Vive XR |

| Customization & Pricing | Available on Request (10% Customization Free) |