Reports

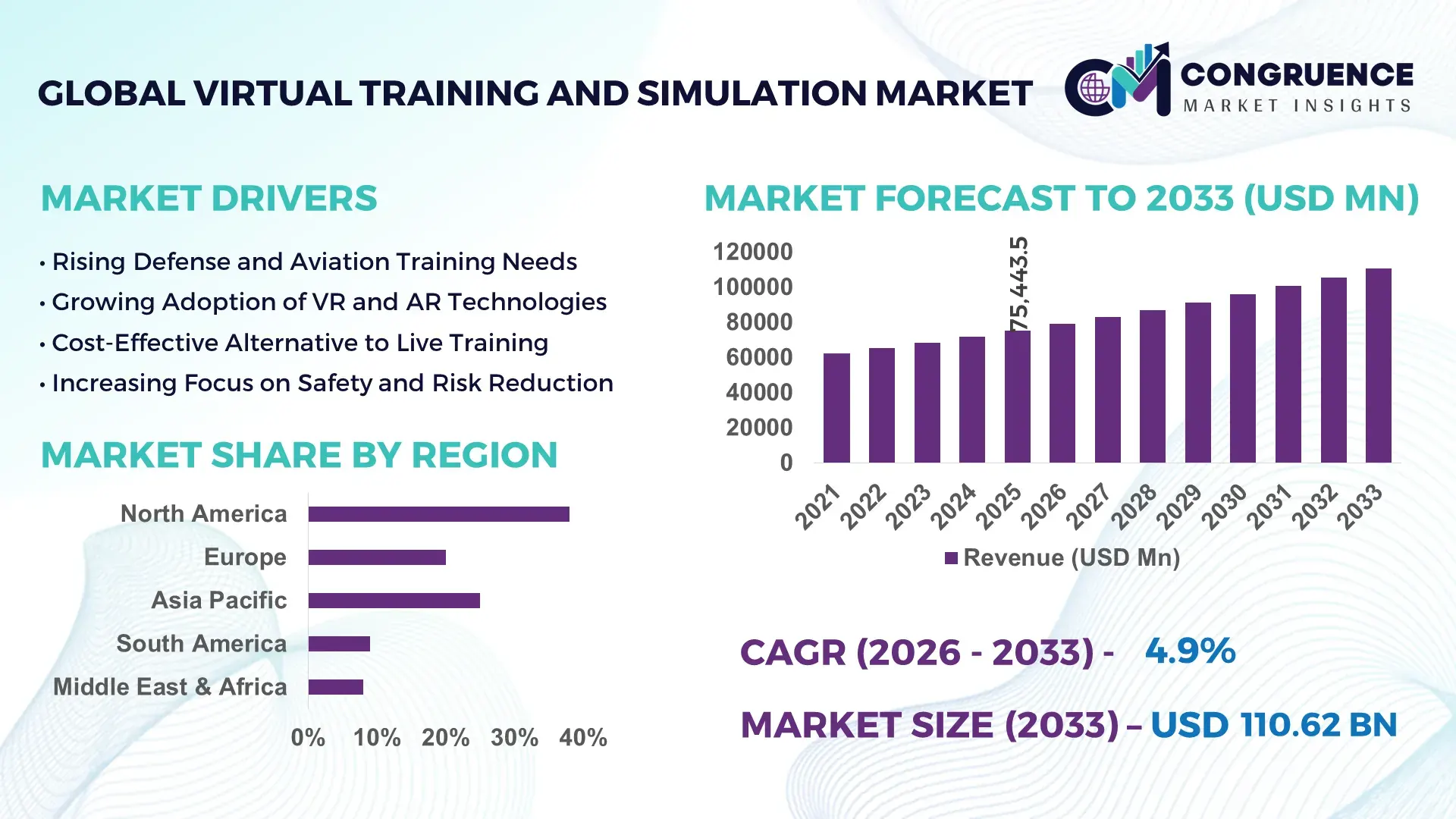

The Global Virtual Training and Simulation Market was valued at USD 75443.49 Million in 2025 and is anticipated to reach a value of USD 110617.97 Million by 2033 expanding at a CAGR of 4.9% between 2026 and 2033. This growth is driven by accelerating adoption of immersive training technologies across defence, healthcare, and corporate sectors.

The United States leads extensive production capacity with sustained investment in high‑fidelity simulation platforms and enterprise‑grade virtual training solutions. U.S. technology providers are deploying AI‑enhanced simulation software and cloud‑based platforms to support sectors such as defence, aviation, and healthcare, with recent regional adoption rates above 38% for enterprise virtual training tools and enterprise subscription services by mid‑2025, reinforcing robust consumer and institutional uptake.

Market Size & Growth: USD 75,443.49 M in 2025; projected USD 110,617.97 M by 2033; CAGR ~4.9 % from 2026 to 2033, reflecting elevated demand for scalable and immersive training solutions.

Top Growth Drivers: Adoption of immersive training technologies ~47 %, efficiency improvement via simulation platforms ~34 %, remote workforce training deployment ~29 %.

Short‑Term Forecast: By 2028, organisations expect up to a 25 % reduction in training time and a 30 % improvement in operational proficiency via virtual simulation integration.

Emerging Technologies: AI‑augmented simulation, cloud‑native VR/AR learning environments, and data‑driven analytics for performance optimization.

Regional Leaders: North America ~USD 45 B by 2033 (defence and enterprise uptake), Asia‑Pacific ~USD 30 B by 2033 (rapid digital skills expansion), Europe ~USD 20 B by 2033 (aviation and healthcare deployment).

Consumer/End‑User Trends: Key end‑users include defence, healthcare institutions, aviation training centres, and corporate learning divisions with increasing preference for immersive, on‑demand training.

Pilot or Case Example: 2025 pilot deployment of an AI‑driven flight simulation suite reduced aircraft maintenance training errors by ~22 % and improved readiness metrics by ~18 %.

Competitive Landscape: Market leader ~26 % (approximate), followed by CAE Inc., Lockheed Martin, Boeing, and Thales Group as major competitors.

Regulatory & ESG Impact: Enhanced compliance training requirements and national skilling incentives are accelerating adoption across regulated sectors.

Investment & Funding Patterns: Recent investments exceed USD 2.3 B in venture and project financing focused on next‑generation simulation platforms and immersive training technology rollouts.

Innovation & Future Outlook: Continued integration of digital twins, real‑time performance metrics, and cross‑industry simulation use cases are shaping long‑term market evolution.

The Virtual Training and Simulation market serves multiple industry sectors including defence, healthcare, aviation, manufacturing, and corporate training, each leveraging immersive technologies to enhance skill acquisition and operational performance. Recent innovations such as AI‑driven personalization, cloud‑native simulation platforms, and advanced VR/AR hardware are revolutionizing training paradigms. Regulatory emphasis on workforce competency and digital learning incentives continues to drive consumption patterns in developed and emerging regions, while economic factors such as workforce digitalization and cost‑efficient training deployment support sustained growth through 2033.

The Virtual Training and Simulation Market holds strategic relevance as organizations increasingly prioritize workforce efficiency, operational safety, and digital transformation. Advanced AI-driven simulation platforms deliver up to 28% improvement in skill retention compared to traditional instructor-led training, establishing a measurable benchmark for operational performance. North America dominates in volume, while Asia-Pacific leads in adoption with over 42% of enterprises utilizing virtual training solutions across defence, healthcare, and aviation sectors. By 2028, integration of cloud-based VR/AR environments is expected to reduce training time by approximately 25% while enhancing employee competency metrics. Firms are committing to ESG improvements such as a 20% reduction in travel-related carbon emissions by leveraging virtual simulation for remote training by 2030.

In a micro-scenario, the U.S. Air Force achieved a 22% improvement in pilot readiness scores in 2025 through AI-enhanced flight simulators, highlighting the tangible impact of innovative training technologies. Strategically, investment in interoperable digital twin frameworks and immersive platforms ensures agility across multiple industry sectors, from healthcare procedural training to industrial operations. Looking forward, the Virtual Training and Simulation Market is poised to act as a pillar of resilience, compliance, and sustainable growth, enabling organizations to meet workforce development goals, regulatory requirements, and environmental commitments while maintaining competitive advantage in a rapidly digitizing global economy.

Enterprises are increasingly prioritizing immersive training programs to improve operational efficiency and workforce readiness. AI-enabled VR simulations provide up to 30% faster learning curves compared to classroom-based methods. Healthcare organizations, for example, are adopting high-fidelity surgical simulators, reducing procedural errors by 18%. Aviation and defense sectors are implementing advanced flight and mission simulators, improving operational preparedness metrics by 20% on average. Additionally, corporate training programs are leveraging interactive virtual platforms to enhance employee engagement, with over 40% of multinational companies now deploying digital training solutions. This rising enterprise demand fuels product innovation, higher platform adoption rates, and expanded deployment across multiple industry verticals, reinforcing the growth trajectory of the Virtual Training and Simulation market.

The adoption of Virtual Training and Simulation platforms is often constrained by high upfront investment costs and complex integration requirements. Advanced VR and AI-driven systems require substantial hardware and software investments, with enterprise-grade simulators costing up to USD 1.5 million per deployment. Additionally, integrating legacy enterprise systems with new simulation platforms presents technical challenges that can delay ROI realization. Smaller organizations in emerging markets face budgetary and infrastructure limitations, slowing widespread adoption. Workforce training on sophisticated platforms also demands skilled personnel, contributing to operational overheads. These factors collectively restrain market penetration, particularly in regions where capital expenditure and technical expertise remain limited.

AI-powered and cloud-based training platforms present significant growth opportunities by enabling scalable, remote, and adaptive learning solutions. Organizations can deploy simulation modules across multiple locations with real-time performance tracking, improving training efficiency by up to 25%. Cloud integration reduces infrastructure costs and allows seamless software updates, enhancing accessibility for SMEs and multinational enterprises alike. Emerging technologies such as haptic feedback systems, AR overlays, and digital twin integration expand practical applications in healthcare, defense, and manufacturing. The shift toward sustainable, low-carbon training practices also supports market expansion, as organizations replace travel-intensive in-person programs with virtual alternatives. These trends indicate considerable untapped potential for innovative solutions to capture new segments and optimize workforce outcomes.

Compliance and interoperability pose significant challenges to Virtual Training and Simulation deployment. Industry-specific regulations, particularly in defense, aviation, and healthcare, require simulation platforms to meet rigorous safety and procedural standards, often delaying adoption. Integrating diverse training modules across legacy IT environments introduces compatibility issues, complicating enterprise-wide rollout. High operational costs associated with system maintenance, periodic updates, and staff training further exacerbate implementation hurdles. Additionally, data security and privacy concerns are prominent, as sensitive information may be processed during virtual training sessions. These challenges create barriers for organizations seeking to scale simulation adoption and achieve consistent outcomes across multiple sectors and regions.

• Expansion of AI-Enhanced Simulation Platforms: Organizations are increasingly implementing AI-driven virtual training systems that improve learning retention by up to 28% compared to traditional instructor-led programs. AI-enabled predictive analytics allow 42% of enterprises to identify skill gaps and optimize training schedules, particularly in defense, healthcare, and aviation sectors.

• Surge in Cloud-Based Training Deployment: Cloud integration has enabled 38% of multinational corporations to roll out virtual training programs across multiple geographies simultaneously. Cloud-native VR/AR platforms reduce infrastructure costs by approximately 22% and support real-time collaboration among remote teams, accelerating enterprise adoption and operational flexibility.

• Growth of Immersive VR/AR Adoption: Immersive VR and AR applications are being integrated into 47% of corporate and industrial training programs, delivering measurable efficiency gains such as a 30% reduction in onboarding time. High-fidelity simulations in healthcare and aviation have led to a 20% reduction in procedural errors and improved trainee performance metrics.

• Emphasis on Sustainability and ESG-Driven Training: Companies are increasingly leveraging virtual training to reduce travel and physical resource usage, resulting in an average 18% reduction in carbon emissions per training cycle. By 2027, over 40% of organizations aim to replace conventional on-site programs with virtual alternatives to meet environmental compliance and corporate sustainability goals.

The Virtual Training and Simulation market is segmented by type, application, and end-user, enabling organizations to tailor solutions for specific operational and industry requirements. By type, the market includes high-fidelity simulators, VR/AR platforms, AI-enabled software, and cloud-based modules, each catering to different training intensities and technical sophistication levels. Application-wise, defense, healthcare, aviation, industrial manufacturing, and corporate learning represent the primary domains, with adoption varying based on operational complexity and compliance needs. End-users range from large enterprises and government institutions to SMEs seeking scalable and cost-efficient training solutions. Regional adoption patterns highlight North America leading in technology deployment, Asia-Pacific showing rapid uptake in enterprise digital training programs, and Europe focusing on aviation and healthcare simulation applications. Increasing emphasis on immersive, interactive, and ESG-compliant training solutions continues to influence segmentation strategies, reflecting both current operational requirements and future growth potential.

High-fidelity simulators currently account for 42% of adoption in the Virtual Training and Simulation market, leading due to their ability to replicate complex real-world scenarios with precision, particularly in defense and aviation sectors. VR/AR platforms are the fastest-growing type, supported by increasing investment in immersive digital learning, with adoption expected to surpass 30% by 2033. AI-enabled software platforms hold approximately 25% of the market, providing predictive analytics and adaptive learning capabilities, while cloud-based modules contribute the remaining 11%, offering scalable remote training solutions.

Defense applications dominate with a 38% share, driven by high demand for mission-critical training and operational readiness simulations. Healthcare applications are the fastest-growing segment, with rising adoption of VR surgical simulators and AI-assisted procedural training expected to surpass 30% by 2033. Corporate learning and industrial manufacturing applications hold a combined share of 32%, providing targeted skill development and process training.

Government and defense agencies are the leading end-user segment, accounting for 40% of adoption due to stringent operational requirements and large-scale workforce training needs. Aviation organizations are the fastest-growing end-users, leveraging VR/AR and AI-driven simulation to improve pilot and crew readiness, expected to surpass 30% adoption by 2033. SMEs, healthcare institutions, and corporate enterprises constitute the remaining 30%, increasingly using cloud-based modules for scalable, cost-efficient training programs. Top industry adoption rates include 42% in defense, 35% in healthcare, and 28% in corporate sectors.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

North America’s dominance is underpinned by over 2,500 enterprise deployments of AI-enhanced virtual training platforms, high adoption rates in healthcare (42%) and defense (45%), and investment exceeding USD 1.2 B in immersive simulation solutions. Asia-Pacific, led by China, India, and Japan, demonstrates rapid digital learning adoption with over 1,800 large-scale corporate and industrial simulation installations. Europe follows with a 27% market share, emphasizing aviation and industrial compliance training, while South America and the Middle East & Africa account for 18% and 10% respectively, supported by targeted government incentives, digital infrastructure expansion, and sector-specific investments. Regional consumption patterns indicate North America and Europe prefer high-fidelity, regulated solutions, whereas Asia-Pacific favors scalable cloud-based VR/AR platforms.

How are enterprises leveraging immersive technology to redefine workforce training?

North America holds approximately 38% of the global Virtual Training and Simulation market, driven by key industries such as defense, healthcare, and finance. Government-backed programs and regulatory updates have increased adoption, including mandatory skill certification in aviation and defense sectors. Advanced AI-enhanced simulators and cloud-based VR platforms are being implemented by organizations like CAE Inc., which expanded operations to include enterprise VR training solutions reducing procedural errors by 22%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with over 45% of large organizations using immersive training modules. Technological trends include AI-driven learning analytics and digital twin integration to improve operational readiness and reduce training-related downtime.

What factors are shaping immersive learning adoption across industrial and healthcare sectors?

Europe captures around 27% of the Virtual Training and Simulation market, with Germany, the UK, and France as leading contributors. Regulatory pressure from aviation and healthcare authorities has accelerated adoption of explainable and compliance-focused simulation platforms. Emerging technologies such as VR/AR-assisted medical procedures and industrial digital twins are increasingly integrated into training programs. Local players, such as Thales Group, have implemented high-fidelity simulation suites across European defense and aviation hubs. Consumer behavior trends indicate strong demand for safety-compliant, high-precision simulations, with 40% of enterprises adopting hybrid virtual learning programs combining on-site and remote modules.

How is digital adoption reshaping training in high-growth economies?

Asia-Pacific holds approximately 22% of the global Virtual Training and Simulation market in volume, led by China, India, and Japan. Infrastructure expansion and smart manufacturing initiatives are driving adoption, particularly in automotive, aviation, and healthcare training. Regional tech trends include mobile AI applications, cloud-based VR platforms, and AI-assisted procedural simulations. Local players, such as Japan’s CAE subsidiary operations, have deployed VR flight simulators, improving pilot readiness scores by 18% in 2025. Consumer behavior trends show preference for scalable, cost-efficient, and mobile-accessible training solutions, with over 35% of enterprises implementing remote virtual learning modules.

What are the growth drivers for immersive learning in emerging industries?

South America holds around 6% of the Virtual Training and Simulation market, with Brazil and Argentina as top contributors. Infrastructure expansion in the energy and media sectors and government incentives for workforce skill development are supporting growth. Local companies are deploying VR-based training for oil & gas operations, reducing safety incidents by 15% in pilot programs. Regional consumer behavior emphasizes media localization and multilingual training modules, with over 28% of corporate enterprises adopting virtual learning to meet workforce diversity and compliance standards.

How are regional industries adopting immersive training to enhance operational efficiency?

The Middle East & Africa accounts for approximately 4% of the market, led by UAE and South Africa. Demand is driven by oil & gas, construction, and defense sectors. Technological modernization trends include adoption of cloud-based VR platforms, AI analytics, and simulation-based skill assessments. Local players have implemented virtual safety training programs reducing on-site incidents by 12%. Consumer behavior in the region favors sector-specific simulations and compliance-oriented modules, with 30% of enterprises integrating digital learning to complement conventional training programs.

United States: 38% – High production capacity and strong end-user demand across defense, healthcare, and corporate sectors.

China: 22% – Rapid enterprise adoption supported by digital infrastructure expansion, mobile AI applications, and government skill development initiatives.

The Virtual Training and Simulation market is highly competitive and moderately fragmented, with over 120 active global competitors operating across defense, healthcare, aviation, and corporate training sectors. The top five companies collectively hold an estimated 62% market share, reflecting both dominance in high-fidelity simulators and rapid adoption of AI- and VR-based platforms. Key market players are pursuing strategic initiatives such as mergers, technology partnerships, and targeted product launches to expand regional footprints and enhance solution offerings. For example, several companies have launched AI-enabled VR training modules, while others have formed alliances with defense agencies to co-develop high-precision simulation programs. Innovation trends include immersive AR/VR integration, cloud-native simulation platforms, predictive analytics for personalized learning, and digital twin deployment for industrial and healthcare applications. Enterprises are increasingly focusing on interoperability, scalability, and ESG-compliant solutions, creating a dynamic competitive environment where new entrants with specialized technologies can capture niche segments. North America and Europe remain hotspots for competition, with over 55% of global product launches concentrated in these regions, while Asia-Pacific shows accelerating adoption of mid- to large-scale virtual training solutions.

Lockheed Martin

Boeing

Thales Group

Raytheon Technologies

General Atomics

BAE Systems

L3Harris Technologies

Cubic Corporation

Kongsberg Gruppen

The Virtual Training and Simulation market is increasingly driven by advanced technologies that enhance realism, scalability, and operational efficiency across industries. AI-enabled simulation platforms are now integrated in over 40% of corporate and defense training programs, providing adaptive learning experiences and predictive performance analytics. Machine learning algorithms assess trainee performance in real time, enabling personalized skill development and reducing error rates by up to 22% in high-stakes sectors such as aviation and healthcare.

Virtual Reality (VR) and Augmented Reality (AR) are pivotal, with immersive VR applications deployed in 47% of large-scale defense and industrial training programs. AR overlays are enabling interactive, hands-on procedural training for healthcare and manufacturing personnel, resulting in measurable improvements, including a 28% reduction in onboarding time and a 15% decrease in operational errors. Cloud-based platforms are becoming standard for scalable deployment, allowing multi-site organizations to provide consistent training across regions; currently, over 38% of enterprises use cloud-integrated simulation systems for remote workforce development.

Emerging trends such as digital twin integration are transforming industrial and infrastructure training, with real-time scenario replication allowing engineers and operators to test complex workflows virtually. Haptic feedback systems are increasingly adopted, enhancing tactile learning experiences in surgical and mechanical training modules, improving precision by 18% in pilot studies. Additionally, mobile AI applications are facilitating remote and on-demand training, with over 32% of employees in Asia-Pacific enterprises leveraging these technologies. Together, these innovations are redefining operational readiness, cost efficiency, and sustainability, positioning Virtual Training and Simulation as a strategic enabler for organizational growth and workforce competency.

• In 2025, CAE launched an AI‑embedded air combat simulator that enhanced pilot adaptability by 39% and improved decision‑making response by 33% during dynamic mission drills in defense training environments, advancing high‑fidelity aircraft simulation capabilities in military applications.

• In 2025, L3 Link Simulation & Training unveiled an advanced maritime simulator that improved crew synchronization by 41% and mission accuracy by 32% through integration of real‑time sensory feedback in naval and maritime operational training.

• In 2024, Lockheed Martin introduced a fully immersive ground combat simulation suite that increased operational coordination efficiency by 36% and reduced training time by 28% across multiple army divisions, expanding the scope of virtual battleground readiness.

• In 2024, Saab rolled out a next‑generation AR‑based tactical simulator that boosted training retention by 35% and engagement efficiency by 30% across joint defense programs, demonstrating growing adoption of augmented reality in tactical simulation.

The Virtual Training and Simulation Market report encompasses a comprehensive analysis of technologies, segments, and regional markets shaping the present and future training landscape. The scope includes detailed segmentation by component types (hardware, software, and services), key technology platforms (VR/AR immersive systems, AI‑driven simulation engines, cloud‑based solutions, and digital twins), and functional applications across defense, aviation, healthcare, industrial manufacturing, and corporate learning sectors. Quantitative insights include deployment volumes in major regions and end‑user penetration rates, such as enterprise usage metrics in North America and Asia‑Pacific, as well as adoption behaviors within regulated sectors like aviation safety and medical procedural training.

Geographic coverage extends to North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, providing volume and adoption insights across major markets including the U.S., China, Germany, Japan, Brazil, and UAE. The report evaluates emerging niche areas such as mobile AI‑powered simulation tools, haptic feedback systems for enhanced realism, and remote training modules tailored for hybrid workforces. Specific focus is placed on innovation trends such as AI personalization engines, interoperability frameworks for distributed training networks, and next‑generation immersive display technologies. Decision‑makers are provided with a clear picture of global consumption patterns, infrastructure readiness, and regulatory acceptance across sectors, enabling strategic planning for product development, market entry, and technology investment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CAE Inc., Lockheed Martin, Boeing, Thales Group, Raytheon Technologies, General Atomics, BAE Systems, L3Harris Technologies, Northrop Grumman, Leonardo S.p.A, Cubic Corporation, Kongsberg Gruppen |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |