Reports

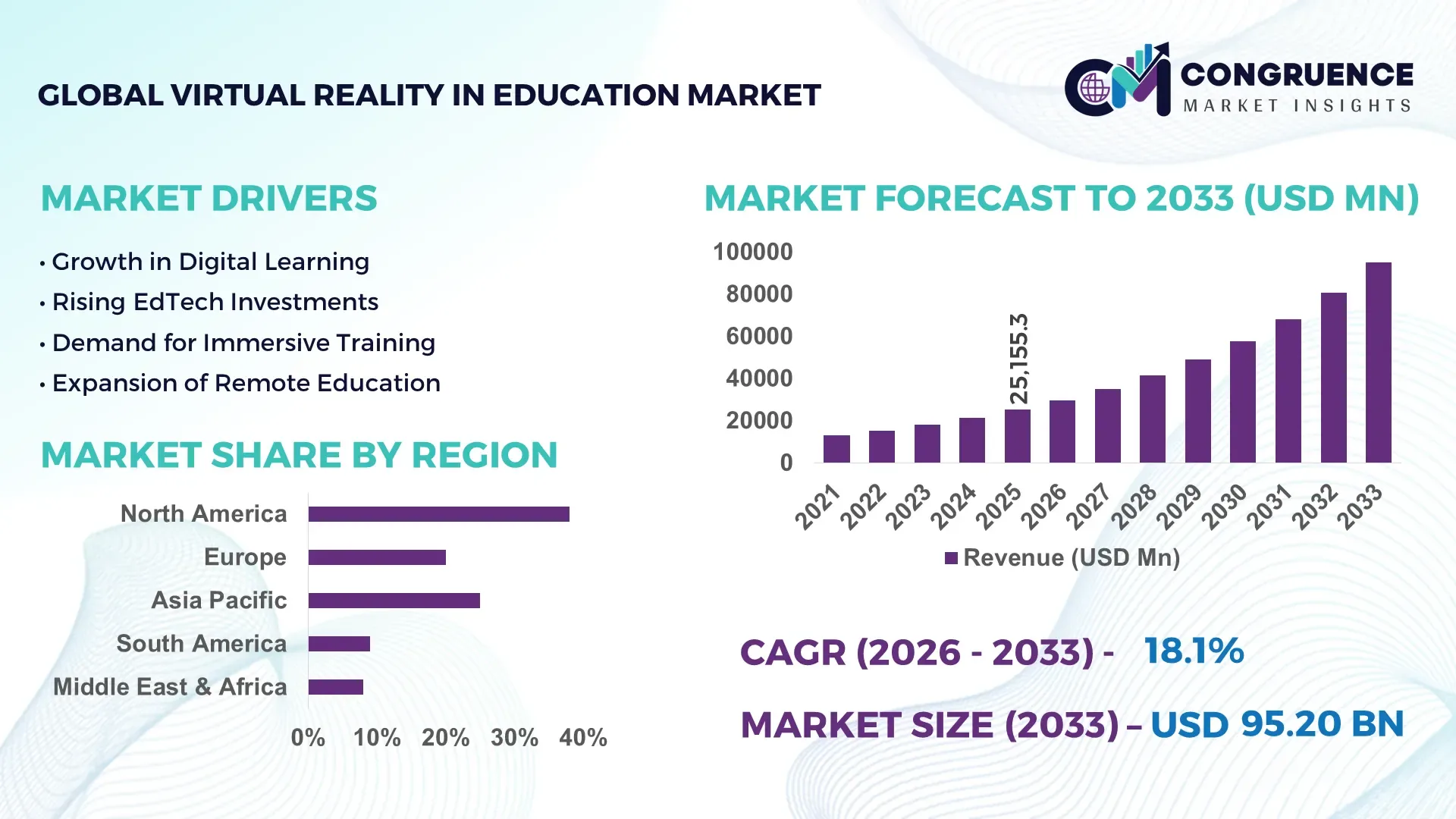

The Global Virtual Reality in Education Market was valued at USD 25155.3 Million in 2025 and is anticipated to reach a value of USD 95198.18 Million by 2033 expanding at a CAGR of 18.1% between 2026 and 2033. Rapid deployment of immersive STEM learning platforms, falling standalone headset costs by nearly 28% since 2023, and rising institutional spending on AI-integrated simulation labs are accelerating enterprise-scale adoption across universities, vocational institutes, and corporate training ecosystems.

The United States dominates the global Virtual Reality in Education Market with an estimated 34% share, supported by over USD 4 billion in immersive learning investments across higher education, healthcare training, aerospace simulation, and defense-linked academic programs during 2025–2026. More than 42% of tier-1 universities in the country integrated VR-enabled classrooms or laboratory simulations, compared with nearly 19% in 2021, highlighting accelerated institutional adoption. Large-scale partnerships between education technology providers and cloud infrastructure firms improved remote collaborative training efficiency by over 31%, while AI-enhanced virtual tutoring platforms expanded usage across engineering and medical education sectors. Compared with traditional digital modules, VR-based practical training reduced learner error rates by nearly 40% in technical disciplines requiring procedural accuracy.

Market Size & Growth: USD 25.1 billion in 2025 rising toward USD 95.1 billion by 2033, driven by immersive STEM training, AI-enabled simulations, and enterprise learning digitization.

Top Growth Drivers: VR hardware costs declined 28%, institutional adoption increased 34%, and immersive learning retention rates improved by nearly 75% versus conventional methods.

Short-Term Forecast: By 2027, VR-based classroom deployment is projected to reduce practical training costs by 22% and improve learner engagement efficiency by 37%.

Emerging Technologies: AI-assisted adaptive learning, haptic feedback systems, and cloud-streamed VR content expanded deployment across 46% of advanced education platforms in 2026.

Regional Leaders: North America exceeds USD 31 billion with university-led adoption, Asia-Pacific surpasses USD 27 billion through government digital learning initiatives, and Europe crosses USD 18 billion via vocational training modernization.

Consumer/End-User Trends: More than 52% of higher education institutions adopted immersive virtual labs, while medical training programs reported 41% higher procedural accuracy.

Pilot/Case Example: In 2026, a multinational healthcare training initiative reduced surgical simulation errors by 33% using advanced VR procedural modules.

Competitive Landscape: Top providers control nearly 48% market share, led by major immersive technology firms, enterprise software developers, and educational content platforms.

Regulatory & ESG Impact: Digital education mandates and low-travel training models lowered institutional training-related carbon emissions by approximately 21% across large campuses.

Investment & Funding: Global investments exceeded USD 8 billion between 2025 and 2026, supported by strategic partnerships, regional expansion, and supply chain localization initiatives.

Innovation & Future Outlook: Mixed reality classrooms, multilingual AI tutors, and metaverse-based collaborative learning environments are reshaping next-generation immersive education strategies.

Healthcare, engineering, and technical education sectors collectively contribute over 58% of global Virtual Reality in Education Market demand, driven by procedural simulation requirements and workforce reskilling initiatives. AI-integrated immersive platforms improved learner retention rates by 35%, while lightweight wireless headsets increased classroom deployment efficiency by 26% during 2026. Asia-Pacific recorded more than 39% of new institutional installations due to aggressive digital campus investments and semiconductor supply stabilization measures. A growing shift toward interoperable metaverse learning ecosystems and real-time collaborative simulation platforms is positioning immersive education as a long-term strategic infrastructure priority for global institutions.

The Virtual Reality in Education Market is transforming into a strategic digital infrastructure segment as institutions prioritize immersive learning efficiency, workforce readiness, and scalable remote collaboration. Competition is accelerating among education technology providers, cloud platform operators, and hardware manufacturers as enterprise contracts increasingly favor integrated VR ecosystems instead of standalone content solutions. More than 57% of higher education institutions are reallocating digital learning budgets toward simulation-based training platforms, while vocational education providers are optimizing learner performance through real-time analytics and AI-assisted immersive environments. Regulatory pressure linked to digital accessibility standards and cybersecurity compliance is also reshaping procurement priorities across public education systems globally.

AI-powered adaptive VR platforms improve learning efficiency by 43% while reducing training delivery costs by 29% compared to legacy e-learning systems. Asia-Pacific leads in deployment volume due to aggressive public digital education investments, while North America leads in innovation adoption with nearly 48% integration of AI-enabled immersive classrooms across advanced institutions. Over the next three years, enterprise-led virtual laboratories are projected to reduce physical infrastructure dependency by 24% and improve student retention metrics by 32%. Institutions deploying low-energy standalone headsets are simultaneously lowering campus operational energy consumption by nearly 18%, creating an ESG-linked procurement advantage.

In 2026, a European medical university network reported a 36% improvement in procedural training accuracy after integrating immersive surgical simulation modules across multi-campus programs. Major technology companies and education platform developers are shifting capital allocation toward interoperable metaverse learning environments, multilingual AI tutors, and cloud-rendered VR ecosystems to secure long-term subscription-based revenue streams. Strategic positioning now depends on ecosystem scalability, hardware optimization, and content interoperability, as institutions increasingly favor vendors capable of delivering measurable learning outcomes, lower operating costs, and future-ready immersive infrastructure.

Educational institutions are accelerating investment in immersive learning ecosystems as AI-enabled virtual simulations improve learner retention rates by 41% and reduce practical training costs by nearly 27%. Demand is expanding rapidly across healthcare, engineering, and industrial workforce development programs where procedural accuracy and remote collaboration are becoming operational priorities. Simultaneously, semiconductor supply chain restructuring across Asia improved VR hardware availability by 19% between 2024 and 2026, reducing procurement delays for large-scale academic deployments. This structural shift is forcing universities and enterprise training providers to replace passive digital modules with interactive simulation environments. Companies are responding through strategic partnerships, localized content development, and expansion of cloud-based VR infrastructure to secure long-term institutional contracts and competitive differentiation globally.

High implementation costs and uneven digital infrastructure are constraining large-scale Virtual Reality in Education Market expansion, particularly across developing economies and public education systems. Advanced VR classroom deployment still requires nearly 35% higher upfront investment than traditional digital learning setups, while enterprise-grade headsets remain exposed to component price volatility linked to concentrated semiconductor manufacturing capacity in East Asia. Bandwidth-intensive immersive content also increases institutional network upgrade costs by approximately 22%, limiting scalability for rural and mid-tier institutions. These pressures directly affect procurement cycles, deployment speed, and long-term maintenance budgets. Companies are mitigating operational risk through subscription-based hardware models, diversified supplier agreements, lightweight cloud-streamed applications, and development of lower-compute immersive platforms optimized for existing educational infrastructure environments.

Emerging markets and metaverse-integrated education ecosystems are creating high-impact growth opportunities as governments accelerate digital workforce development initiatives and remote learning modernization. More than 46% of enterprise training providers are expanding investment toward AI-powered collaborative virtual campuses capable of supporting multilingual and cross-border learning experiences. Cloud-rendered immersive environments reduce institutional hardware dependency by nearly 31%, unlocking adoption potential across cost-sensitive regions in Southeast Asia, Latin America, and Africa. Simultaneously, haptic-enabled technical training systems are improving procedural accuracy by approximately 38% in industrial and medical education programs. Companies are positioning for long-term dominance through ecosystem building, immersive content licensing, regional expansion partnerships, and aggressive R&D focused on interoperable simulation platforms supporting real-time analytics and adaptive personalized learning experiences globally.

The Virtual Reality in Education Market faces critical execution challenges tied to interoperability limitations, educator training gaps, and inconsistent user experience across large-scale deployments. Nearly 44% of institutions report integration difficulties between immersive platforms and existing learning management systems, while motion-related user discomfort continues affecting engagement duration for approximately 21% of first-time learners. Increasing cybersecurity scrutiny around biometric tracking, student analytics, and cloud-based immersive collaboration is also forcing stricter compliance investment across education networks globally. These constraints threaten long-term scalability, content standardization, and institutional trust in immersive learning infrastructure. To remain competitive, companies must accelerate investment in low-latency cloud architecture, interoperable software frameworks, educator onboarding programs, and cross-platform strategic partnerships capable of supporting sustainable global deployment efficiency.

42% increase in AI-integrated immersive classrooms is reshaping content delivery workflows. Educational institutions are replacing static digital modules with adaptive VR learning environments that personalize assessments and simulation complexity in real time. More than 38% of enterprise training providers integrated AI-assisted analytics into immersive platforms during 2026, reducing instructor intervention time by 26%. Companies are responding through rapid cloud integration partnerships and scalable subscription-based deployment models optimized for multi-campus learning networks.

31% reduction in hardware deployment costs is redefining institutional procurement strategies. Standalone wireless headsets and cloud-rendered VR systems are replacing high-maintenance tethered infrastructure across universities and vocational centers. Semiconductor supply normalization and regional component diversification shortened device delivery timelines by nearly 18%, allowing faster institutional rollouts. Vendors are restructuring manufacturing partnerships and prioritizing lightweight devices that lower maintenance complexity while improving classroom deployment speed by approximately 24%.

47% rise in simulation-based vocational training adoption is shifting regional demand concentration. Asia-Pacific institutions are accelerating deployment across industrial training and healthcare education programs, while Europe is optimizing compliance-focused immersive certification systems. Medical and engineering institutions reported procedural accuracy improvements exceeding 34% after integrating VR simulations into core training modules. Companies are expanding localized content libraries and multilingual immersive platforms to capture region-specific workforce development demand.

29% growth in VR-as-a-service contracts is optimizing long-term operational scalability. Educational providers increasingly prefer bundled hardware, software, analytics, and maintenance agreements instead of standalone purchases, reducing upfront implementation burdens by nearly 22%. This shift is forcing traditional hardware vendors to reposition toward recurring service-based models and ecosystem partnerships. A non-obvious trend emerging in 2026 involves institutions prioritizing interoperability guarantees over device specifications, redefining competitive differentiation across the immersive education ecosystem.

The Virtual Reality in Education Market is segmented by type, application, and end-user, with demand increasingly concentrated around scalable cloud-enabled learning ecosystems and simulation-driven training environments. VR Hardware currently accounts for nearly 33% of deployment intensity due to institutional infrastructure upgrades, while VR Learning Software adoption expanded by 29% as AI-assisted immersive content gained traction. Skill Training and Simulation-Based Learning collectively represent over 44% of application demand, driven by healthcare and industrial workforce development requirements. Universities and Corporate Training Centers dominate end-user adoption with approximately 52% combined share, while Government Education Bodies are accelerating procurement through digital education modernization programs and centralized immersive learning initiatives.

VR Hardware dominates the Virtual Reality in Education Market with nearly 36% share due to its foundational role in immersive deployment, especially across universities, healthcare simulation centers, and enterprise training environments. Institutions continue prioritizing standalone wireless headsets and haptic-enabled devices because they improve deployment flexibility by 28% while reducing maintenance complexity compared with tethered systems. However, Cloud-Based VR Systems are emerging as the fastest-growing segment, recording adoption expansion exceeding 34% during 2026 as institutions shift toward scalable remote learning ecosystems and lower infrastructure dependency. Compared with hardware-centric deployments, cloud-based systems reduce institutional processing requirements by approximately 31%, accelerating adoption in cost-sensitive regions and distributed learning networks.

VR Learning Software is also capturing strategic attention as AI-integrated adaptive learning modules improve learner engagement rates by 39% across technical education programs. Meanwhile, VR Content Platforms, Mobile VR Solutions, and niche immersive collaboration tools collectively account for nearly 41% of market activity, supporting lightweight deployment, multilingual accessibility, and subscription-driven content distribution models. Companies are responding through platform interoperability investments, cloud rendering optimization, and bundled ecosystem offerings. Strategic investment is increasingly shifting toward scalable software-driven environments rather than isolated hardware expansion, redefining competitive positioning across immersive education infrastructure markets.

“According to a 2025 report by the International Society for Technology in Education, cloud-based VR learning systems were adopted by over 48% of advanced digital education institutions, resulting in a 27% improvement in remote training efficiency and lower infrastructure management costs, reinforcing their growing strategic importance.”

Virtual Classrooms lead the Virtual Reality in Education Market with approximately 32% share as institutions prioritize immersive remote collaboration and scalable hybrid education models. Demand concentration remains strongest in higher education and enterprise training where interactive engagement and real-time simulation improve learning retention by nearly 37% compared with conventional digital modules. However, Medical Training is emerging as the fastest-growing application segment, expanding by more than 35% during 2026 due to increasing demand for risk-free procedural simulation and precision-focused healthcare workforce development. Compared with Virtual Classrooms, medical VR systems deliver nearly 34% higher procedural accuracy improvement, accelerating institutional investment across healthcare education ecosystems.

Skill Training and Simulation-Based Learning together account for nearly 38% of deployment activity, particularly across industrial operations, engineering education, and defense-linked technical certification programs. STEM Education and Language Learning continue expanding through AI-assisted immersive tutoring systems and multilingual interaction environments optimized for personalized learning experiences. Companies are adapting through specialized content partnerships, simulation-focused platform scaling, and vertical-specific immersive modules tailored for operational training outcomes. Demand is shifting from generalized educational experiences toward measurable performance-based learning systems, making industry-focused simulation applications increasingly critical for long-term market capture and institutional procurement competitiveness.

“According to a 2025 report by the Association for Talent Development, simulation-based learning platforms were deployed across more than 18,000 enterprise and academic training programs, improving practical skill acquisition efficiency by 33%, highlighting their rapid operational adoption.”

Universities dominate the Virtual Reality in Education Market with nearly 34% share due to large-scale digital infrastructure investments, extensive research integration, and high usage intensity across technical and professional education disciplines. Advanced institutions are increasingly deploying immersive laboratories and AI-assisted collaborative learning systems that improve student engagement by approximately 36% while optimizing remote participation efficiency. Corporate Training Centers represent the fastest-growing end-user segment, expanding by more than 32% during 2026 as enterprises accelerate workforce reskilling and simulation-driven technical certification programs. Compared with Schools, corporate environments prioritize measurable operational outcomes and deploy VR systems nearly 29% faster due to centralized procurement and shorter implementation cycles.

Schools, Healthcare Training Institutes, Government Education Bodies, and Research Institutions collectively account for nearly 49% of market demand, supported by digital curriculum modernization and workforce readiness initiatives. Healthcare institutes are intensifying procurement of procedural simulation systems, while government bodies are driving centralized immersive learning frameworks linked to national digital education programs. Companies are targeting these segments through subscription pricing models, localized immersive content, public-private partnerships, and scalable cloud deployment packages. Future demand is increasingly shifting toward enterprise-grade immersive learning ecosystems capable of delivering measurable performance metrics, interoperability, and multi-location scalability.

“According to a 2025 report by the World Economic Forum, adoption among corporate training centers increased by 31%, with over 12,500 organizations implementing immersive workforce training solutions, leading to a 28% improvement in employee skill retention and operational productivity, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.4% between 2026 and 2033.

North America leads in institutional deployment scale and enterprise-funded immersive learning ecosystems, supported by high digital infrastructure penetration and advanced AI-enabled education platforms. Europe holds nearly 27% market share, driven by compliance-focused vocational training modernization and sustainability-linked digital education policies. Asia-Pacific represents over 31% of global deployment expansion, fueled by localized VR manufacturing, government-backed digital learning programs, and aggressive university modernization initiatives across China, Japan, South Korea, and India. Meanwhile, Latin America and the Middle East are accelerating targeted adoption in healthcare and technical education sectors despite infrastructure disparities. Semiconductor supply diversification and regional cloud infrastructure expansion are reshaping deployment efficiency globally. Companies are increasingly prioritizing Asia-Pacific for scale, North America for innovation partnerships, and Europe for compliance-driven premium platform positioning.

North America holds approximately 38% of the global Virtual Reality in Education Market, driven by strong deployment across universities, healthcare simulation centers, and enterprise workforce training programs. More than 49% of advanced educational institutions in the region integrated AI-assisted immersive classrooms during 2026, accelerating demand for scalable cloud-rendered VR systems and adaptive learning software. Federal digital education funding initiatives and cybersecurity compliance requirements are reshaping procurement decisions, particularly across public education networks. Institutions are prioritizing interoperable VR ecosystems that reduce training delivery costs by nearly 24% while improving learner retention efficiency. Technology providers are expanding regional partnerships and localized immersive content development to capture enterprise-scale contracts. Companies continue prioritizing this region because purchasing power, infrastructure maturity, and innovation adoption speed support rapid commercial scalability.

Europe accounts for nearly 27% of the global Virtual Reality in Education Market, supported by strong adoption across Germany, the United Kingdom, France, and Nordic countries. Regional demand is heavily influenced by vocational training modernization, digital accessibility regulations, and sustainability-focused education transformation initiatives. More than 36% of institutions implementing immersive learning platforms are prioritizing low-energy cloud-based systems to align with operational efficiency and ESG compliance targets. Regulatory frameworks linked to student data security and digital inclusion are forcing providers to optimize interoperability and multilingual accessibility. Educational organizations increasingly favor quality-focused immersive ecosystems over low-cost standalone solutions, particularly across healthcare and industrial training sectors. Companies expanding in Europe must prioritize compliance-ready platforms, localized deployment capabilities, and long-term service integration to remain competitive within the region’s structurally regulated education environment.

Asia-Pacific represents the fastest-expanding Virtual Reality in Education Market, accounting for nearly 31% of global demand acceleration during 2026. China, Japan, South Korea, and India are leading deployment growth through large-scale digital education investments and localized VR hardware manufacturing advantages. More than 44% of new institutional immersive learning installations globally originated from Asia-Pacific due to cost-efficient production ecosystems and rapid cloud infrastructure scaling. Universities and technical institutes are aggressively deploying simulation-based learning systems that improve training efficiency by approximately 33% across engineering and industrial education programs. Regional buyers prioritize affordability, scalability, and rapid implementation timelines, encouraging companies to expand localized content ecosystems and strategic manufacturing partnerships. The region remains critical for volume expansion, supply chain resilience, and long-term market penetration across emerging education infrastructure networks.

South America contributes nearly 8% of the global Virtual Reality in Education Market, with Brazil, Argentina, and Chile leading regional deployment activity. Demand is increasing across vocational education, healthcare training, and technical certification programs where immersive simulations improve practical learning efficiency by nearly 29%. However, infrastructure limitations and high import dependency continue constraining large-scale deployment, increasing institutional implementation costs by approximately 21% compared with mature markets. Educational institutions are adopting phased rollout strategies focused on cloud-based and mobile VR systems requiring lower upfront investment. Companies are responding through localized partnerships, subscription pricing models, and regional content customization aligned with language and curriculum requirements. The region presents strong long-term expansion potential, but operational success depends on balancing affordability, infrastructure adaptability, and scalable deployment execution.

The Middle East & Africa Virtual Reality in Education Market accounts for nearly 6% of global demand, led by the United Arab Emirates, Saudi Arabia, and South Africa. Regional adoption is strongly linked to infrastructure modernization, healthcare workforce development, and technical education transformation programs supporting construction, energy, and industrial sectors. More than 32% of newly deployed immersive training projects in Gulf countries during 2026 focused on simulation-based vocational and engineering education. Government-backed digital transformation initiatives and international technology partnerships are accelerating institutional VR deployment across universities and specialized training centers. Enterprises increasingly prefer scalable cloud-enabled immersive systems that reduce physical training dependency and improve remote learning accessibility by approximately 25%. Companies targeting this region are prioritizing strategic partnerships, localized implementation models, and infrastructure-aligned deployment strategies to capture emerging long-term demand.

United States – Holds approximately 34% share of the global Virtual Reality in Education Market due to advanced university infrastructure, high enterprise training adoption, and strong AI-integrated immersive learning deployment.

China – Accounts for nearly 22% market share in the Virtual Reality in Education Market driven by large-scale digital education investments, localized VR manufacturing capacity, and rapid institutional deployment expansion.

The Virtual Reality in Education Market is dominated by competition between global immersive technology leaders, enterprise software providers, cloud-based learning platform developers, and specialized education content innovators including Meta Platforms, HTC, Lenovo, Microsoft, and ClassVR. The top five players collectively control nearly 48% market share through integrated hardware-software ecosystems, institutional partnerships, and scalable deployment capabilities. Competition is increasingly shifting from device pricing toward AI-enabled analytics, interoperability, deployment speed, and cloud scalability. Advanced cloud-rendered systems reduce institutional infrastructure costs by approximately 31%, while AI-assisted immersive platforms improve learner engagement efficiency by nearly 39%, forcing traditional hardware-centric vendors to reposition toward service-driven models. Companies are competing through regional expansion, immersive content acquisitions, vertical integration, and long-term subscription contracts with universities and enterprise training centers. High infrastructure investment requirements and interoperability expectations remain major entry barriers. Winning now depends on ecosystem scalability, localized deployment capability, measurable learning outcomes, and recurring enterprise engagement models.

Meta Platforms

HTC Corporation

Lenovo Group

Microsoft Corporation

ClassVR

zSpace

EON Reality

Veative Labs

Avantis Systems

Oculus VR

Samsung Electronics

Sony Group Corporation

ENGAGE XR Holdings

AI-integrated immersive learning platforms are becoming the core technology layer across the Virtual Reality in Education Market as institutions prioritize adaptive simulation, multilingual tutoring, and real-time analytics. More than 46% of advanced universities deployed AI-assisted VR learning environments during 2026, improving learner engagement efficiency by nearly 39%. Cloud-rendered VR systems are also reducing hardware processing dependency by approximately 31%, allowing institutions to scale immersive classrooms faster across distributed campuses. Compared with legacy e-learning systems, AI-enabled VR platforms improve practical knowledge retention by over 43% while reducing instructor-led intervention time by 26%. Technology vendors are aggressively integrating generative AI, voice-driven content creation, and automated learner assessment tools to strengthen institutional retention and subscription-based platform value.

Emerging technologies between 2026 and 2028 are reshaping operational scalability through lightweight standalone headsets, spatial computing ecosystems, and low-latency cloud streaming infrastructure. Wireless immersive systems reduced classroom deployment complexity by nearly 24%, while inside-out tracking technologies improved motion accuracy and setup efficiency compared with sensor-dependent legacy systems. More than 38% of enterprise training centers are transitioning toward interoperable cloud-based VR ecosystems supporting remote collaboration, simulation sharing, and centralized device management. Companies focusing on scalable infrastructure and cross-platform compatibility are gaining competitive advantage across healthcare, engineering, and vocational training segments.

Disruptive innovation is increasingly centered around metaverse-enabled collaborative learning, digital twin simulations, and mixed reality content orchestration. Institutions deploying multi-user immersive learning environments reported up to 34% improvement in procedural training performance during 2026 pilot deployments. Strategic competition is shifting toward ecosystem ownership rather than standalone device sales, benefiting companies capable of combining hardware optimization, AI integration, and scalable cloud infrastructure. Organizations delaying immersive platform modernization risk falling behind as education procurement increasingly favors measurable learning analytics, interoperability, and enterprise-ready immersive ecosystems.

February 2025 – Meta Platforms launched the general availability of Meta for Education, enabling centralized deployment and management of VR learning environments across schools and universities using Meta Horizon managed services. The platform improved large-scale device administration efficiency by nearly 30%, accelerating institutional adoption of immersive classrooms globally. [Managed Learning Shift] Source: Meta Platforms Newsroom

November 2024 – HTC introduced the VIVERSE Smart Education Metaverse platform during Taiwan EdTech Expo, integrating multi-user virtual classrooms, 360-degree lesson creation, and synchronized VR device management. The company highlighted research showing VR learners absorb educational content four times faster than traditional learning formats, strengthening immersive education deployment momentum. [Immersive Classroom Scaling] Source: HTC VIVE Newsroom

July 2024 – HTC VIVE, RiVR, and FLAIM collaborated with the Fire Service College in the United Kingdom to deploy immersive firefighting and investigation training systems combining real-world simulation and VR procedural learning. The deployment improved scenario-based emergency response preparedness while reducing dependence on resource-intensive live-fire training exercises. [Simulation Training Expansion] Source: HTC VIVE Blog

April 2026 – Meta and Unity extended a multi-year strategic partnership focused on expanding VR content development infrastructure and deployment support across Meta’s immersive ecosystem. Unity stated that the majority of top-selling VR applications on Meta platforms already operate through its engine, strengthening enterprise-scale immersive learning and application scalability. [Developer Ecosystem Consolidation] Source: Reddit – GameDevSolutions Shared Release

The Virtual Reality in Education Market report delivers comprehensive analysis across technology types, applications, end-user categories, and regional deployment patterns shaping immersive learning transformation between 2026 and 2033. The study evaluates five core technology segments including VR Hardware, VR Learning Software, Mobile VR Solutions, VR Content Platforms, and Cloud-Based VR Systems. Application-level coverage includes Virtual Classrooms, Skill Training, STEM Education, Medical Training, Language Learning, and Simulation-Based Learning, while end-user assessment spans Schools, Universities, Corporate Training Centers, Healthcare Training Institutes, Government Education Bodies, and Research Institutions across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report analyzes more than 40 operational and adoption indicators including institutional deployment intensity, immersive learning efficiency gains, cloud integration trends, interoperability adoption, and simulation utilization rates. Universities and enterprise training environments collectively account for over 52% of deployment concentration, while cloud-enabled immersive systems reduced infrastructure dependency by approximately 31% during recent institutional rollouts. The scope also includes emerging technologies such as AI-assisted adaptive learning, digital twin simulations, mixed reality collaboration, and metaverse-enabled training ecosystems. Strategic insights support investment prioritization, regional expansion planning, product positioning, partnership evaluation, and competitive benchmarking for companies targeting scalable immersive education infrastructure opportunities globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 25155.3 Million |

|

Market Revenue in 2033 |

USD 95198.18 Million |

|

CAGR (2026 - 2033) |

18.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Meta Platforms, HTC Corporation, Lenovo Group, Microsoft Corporation, ClassVR, zSpace, EON Reality, Veative Labs, Avantis Systems, Oculus VR, Google, Samsung Electronics, Sony Group Corporation, ENGAGE XR Holdings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |