Reports

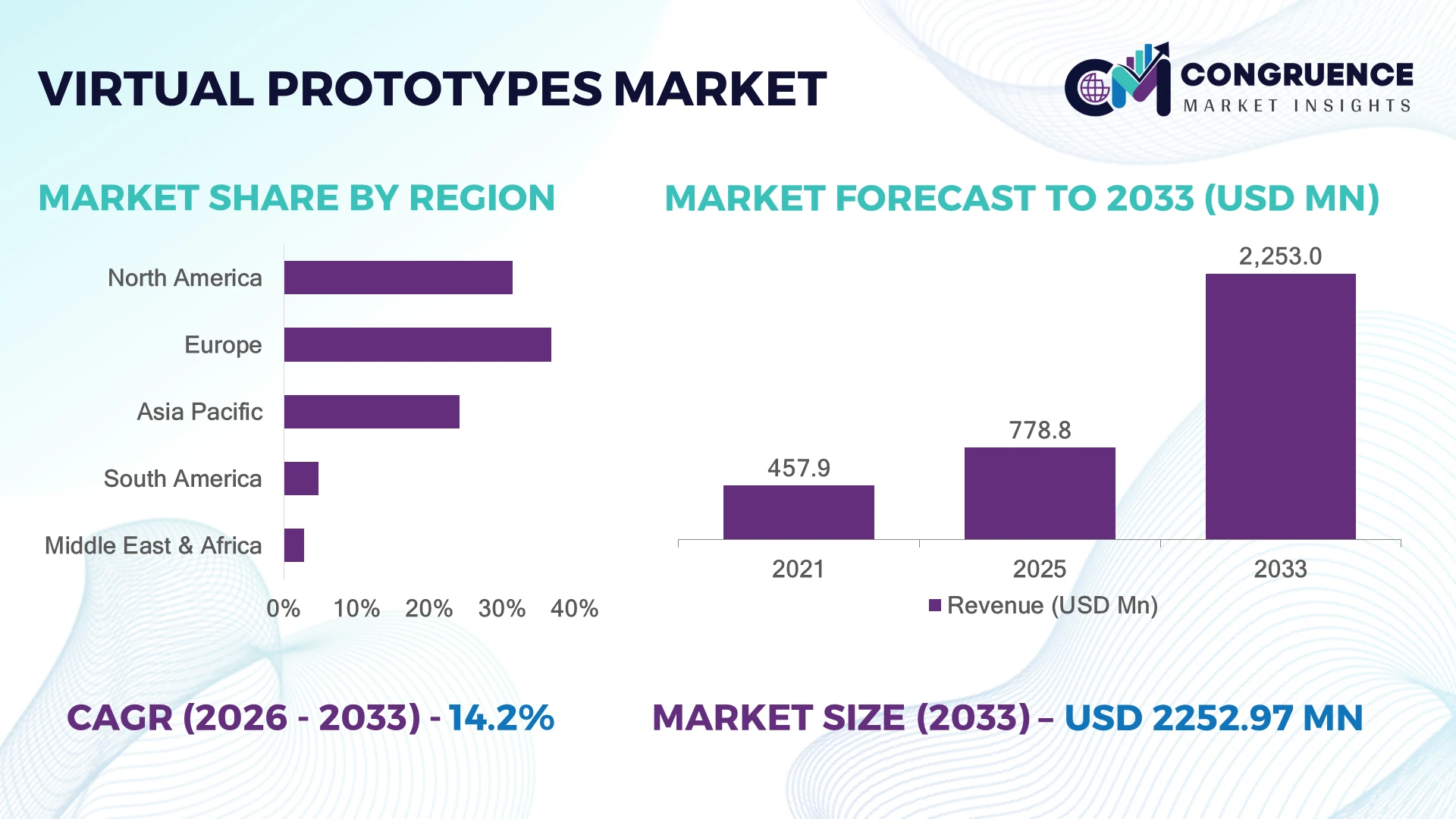

The Global Virtual Prototypes Market was valued at USD 778.8 Million in 2025 and is anticipated to reach a value of USD 2,253.0 Million by 2033 expanding at a CAGR of 14.2% between 2026 and 2033. Rapid digital engineering adoption across automotive, aerospace, industrial manufacturing, and electronics is accelerating virtual validation, reducing physical prototype iterations, and shortening product development cycles.

Germany leads the global landscape with nearly 23% of advanced industrial virtual prototype deployments, supported by strong automotive and precision engineering investments exceeding 35 major digital manufacturing initiatives. Compared with Japan, German manufacturers integrate simulation-led design across a broader share of production programs, while over 68% of large industrial enterprises utilize advanced digital engineering platforms to optimize product performance and manufacturing efficiency.

Organizations prioritizing integrated simulation ecosystems and collaborative digital engineering capabilities will secure faster innovation cycles, stronger product quality, and sustainable competitive differentiation.

Market Size & Growth: USD 778.8 Million in 2025, projected to reach USD 2,253.0 Million by 2033 at 14.2% CAGR, driven by expanding digital engineering and simulation-first product development.

Top Growth Drivers: Automotive digital engineering adoption exceeds 72%, industrial simulation usage surpasses 64%, and cloud-based collaboration improves engineering productivity by over 38%.

Short-Term Forecast: By 2028, prototype validation time declines by nearly 35% while engineering workflow efficiency improves by approximately 30%.

Emerging Technologies: AI-assisted simulation, cloud-native digital twins, and GPU-accelerated multiphysics modeling accelerate advanced product validation across global industries.

Regional Leaders: North America approaches USD 810 Million, Europe exceeds USD 690 Million, and Asia-Pacific nears USD 540 Million, supported by regional manufacturing digitalization and supply-chain modernization.

Consumer/End-User Trends: More than 67% of large manufacturers prioritize virtual testing before physical production, reducing design revisions and accelerating commercialization.

Pilot/Case Example: In 2024, an automotive digital engineering initiative reduced physical prototype requirements by 45% while shortening vehicle validation timelines by 28%.

Competitive Landscape: Siemens holds approximately 18% market presence alongside Dassault Systèmes, PTC, Ansys, and Autodesk through continuous platform innovation.

Regulatory & ESG Impact: Digital validation lowers engineering material waste by nearly 32% while supporting stricter product compliance and sustainability objectives.

Investment & Funding: More than USD 2.4 Billion has been directed toward industrial simulation, AI engineering software, and strategic technology partnerships worldwide.

Innovation & Future Outlook: Next-generation AI-driven digital twins, immersive collaborative engineering, and real-time simulation platforms are strengthening global product innovation strategies.

Virtual Prototypes Market demand continues expanding across electric vehicles, aerospace systems, industrial equipment, and semiconductor product design, where rapid design validation and predictive simulation improve engineering accuracy. AI-enabled physics simulation and cloud collaboration platforms now support over 60% faster design iterations in leading engineering environments. Ongoing supply-chain localization is further encouraging manufacturers to adopt virtual development workflows before large-scale production, strengthening strategic planning across high-value industries.

Virtual prototypes have become a strategic capability for manufacturers seeking faster innovation, improved engineering precision, and lower product development risk. Growing digital transformation across automotive, aerospace, electronics, healthcare, and industrial equipment is reshaping competitive strategies, while supply-chain restructuring encourages companies to validate products digitally before committing to production capacity. Organizations increasingly integrate simulation into enterprise engineering platforms to improve design collaboration and operational resilience.

Compared with traditional physical prototype development, virtual prototype platforms reduce validation cycles by approximately 40% while lowering engineering modification costs by nearly 30% through real-time simulation and digital testing. North America maintains leadership in enterprise software deployment and advanced R&D integration, whereas Asia-Pacific records faster manufacturing implementation driven by expanding electronics production, industrial automation, and smart factory investments. Over the next two to three years, enterprise-wide simulation integration is expected to become standard across large manufacturing organizations.

Automotive manufacturers increasingly deploy digital twin-enabled prototype environments to evaluate vehicle performance before physical assembly, reducing testing complexity and accelerating design approvals. Technology providers are expanding cloud engineering partnerships, strengthening AI capabilities, and enhancing collaborative simulation platforms to improve deployment flexibility. Companies that establish scalable virtual engineering ecosystems today will secure stronger competitive positioning, greater operational efficiency, and faster commercialization of next-generation products.

The transition toward simulation-first engineering is reshaping product development across automotive, aerospace, electronics, and medical device manufacturing. More than 70% of global automotive OEMs now integrate virtual validation into early-stage design, while digital engineering workflows reduce physical prototype iterations by nearly 45% and shorten product verification cycles by approximately 35%. Germany's Industry 4.0 initiatives continue to encourage wider deployment of advanced simulation environments across precision manufacturing facilities. This structural shift enables manufacturers to identify design flaws before tooling investments, reducing engineering risk and improving production readiness. In response, leading software providers are expanding AI-enabled simulation capabilities, strengthening cloud collaboration platforms, and forming strategic partnerships with industrial manufacturers to deliver integrated digital engineering ecosystems with greater scalability and operational efficiency.

Complex integration across heterogeneous engineering environments remains a significant limitation for enterprise-scale deployment. Around 52% of manufacturers continue operating mixed legacy CAD and PLM infrastructures, while nearly 40% report interoperability challenges between simulation, lifecycle management, and manufacturing execution platforms. Japan's precision manufacturing sector faces prolonged software migration timelines because highly customized engineering workflows require extensive validation before implementation. These structural constraints increase deployment costs, delay engineering collaboration, and reduce operational flexibility across distributed design teams. Companies are responding through standardized data architectures, localized implementation services, multi-year software agreements, and open-platform integration strategies that reduce dependency on proprietary environments while improving long-term system compatibility and implementation efficiency.

Artificial intelligence combined with digital twin technology is creating high-value opportunities beyond conventional virtual design. AI-assisted engineering can improve simulation accuracy by nearly 30%, while automated design optimization reduces development effort by approximately 25% across complex industrial programs. South Korea's semiconductor and electronics manufacturers are expanding intelligent simulation platforms to accelerate advanced product development and improve manufacturing precision. Increasing government support for industrial digitalization further strengthens enterprise investment in connected engineering ecosystems. Software vendors are expanding R&D, acquiring specialized simulation companies, and developing cloud-native engineering platforms that combine predictive analytics, real-time collaboration, and lifecycle intelligence, enabling customers to unlock measurable productivity improvements and create recurring digital engineering service models.

Maintaining secure, enterprise-wide virtual engineering environments presents a growing execution challenge as organizations expand global design collaboration. More than 48% of manufacturers identify cybersecurity as a primary concern for cloud-based engineering platforms, while approximately 37% experience shortages of advanced simulation specialists capable of managing multidisciplinary digital workflows. The United States continues strengthening industrial cybersecurity requirements for critical manufacturing sectors, increasing compliance expectations for engineering software deployments. These pressures complicate large-scale implementation, intellectual property protection, and long-term operational consistency across international engineering teams. Technology providers must strengthen zero-trust security frameworks, expand workforce training, invest in secure cloud infrastructure, and deepen ecosystem partnerships to ensure scalable, resilient, and globally synchronized virtual prototype deployment.

AI-Enabled Simulation Acceleration: Engineering teams are embedding generative AI into simulation workflows, with more than 58% of large manufacturers using AI-assisted design optimization and nearly 42% reducing validation iterations through automated model refinement. Digital engineering teams now complete complex design evaluations up to 30% faster, improving launch schedules. Software vendors are expanding AI partnerships and integrating intelligent simulation assistants to strengthen enterprise productivity amid growing engineering talent shortages.

Cloud-Native Engineering Collaboration: Cloud deployment has become standard for globally distributed product development, with approximately 65% of multinational manufacturers operating collaborative simulation environments and over 48% shifting engineering workloads from on-premise infrastructure. Supply-chain localization is encouraging synchronized product development across multiple facilities. Platform providers are strengthening secure cloud architectures, expanding regional data centers, and enhancing collaborative lifecycle management to reduce engineering bottlenecks and improve design consistency.

Digital Twin Integration Expansion: Virtual prototypes are increasingly connected with operational digital twins, allowing nearly 55% of industrial enterprises to validate product performance before production while reducing manufacturing change orders by approximately 28%. Germany's smart manufacturing initiatives continue supporting integrated engineering environments that connect design, production, and quality management. Technology companies are expanding unified engineering platforms through acquisitions and ecosystem partnerships to improve lifecycle visibility and operational decision-making.

Industry-Specific Simulation Platforms: Engineering software is shifting from generic modeling toward sector-optimized simulation environments. More than 47% of automotive manufacturers and around 39% of aerospace companies now deploy specialized virtual prototype workflows tailored to regulatory and performance requirements. This transition improves compliance readiness, shortens certification activities, and enhances product reliability. Vendors are scaling vertical-specific solutions, expanding industry consulting capabilities, and incorporating advanced materials modeling to address increasingly complex product architectures.

The market is segmented into Software, Services, and Integrated Solutions. Software remains the dominant segment, accounting for approximately 61% of enterprise deployments because organizations prioritize scalable simulation, digital validation, and collaborative engineering capabilities within unified product development environments. Mature software platforms integrate CAD, CAE, PLM, and digital twin technologies, enabling engineering teams to reduce design revisions by nearly 35% while improving development productivity by approximately 30%. Leading vendors continue strengthening AI-assisted simulation, cloud deployment, and interoperability features to support increasingly complex industrial applications. Integrated Solutions represent the fastest-growing segment as manufacturers seek end-to-end engineering ecosystems rather than standalone simulation tools. Services maintain strategic importance by supporting implementation, customization, workforce training, and lifecycle optimization, particularly among large industrial enterprises modernizing legacy engineering infrastructure. Companies are increasing investments in integrated product portfolios, strategic acquisitions, and technology partnerships to strengthen long-term customer retention while expanding recurring engineering software ecosystems.

The market is segmented into Automotive, Aerospace & Defense, Industrial Manufacturing, Healthcare & Medical Devices, Electronics & Semiconductor, Construction, and Others. Automotive remains the leading application, representing nearly 34% of deployments due to continuous product innovation, electrification programs, and increasing reliance on virtual validation before physical production. Manufacturers report reductions of nearly 40% in prototype iterations while shortening vehicle development timelines by approximately 30%. Software developers continue expanding simulation capabilities supporting battery systems, lightweight materials, and autonomous vehicle engineering. Healthcare & Medical Devices is emerging as the fastest-growing application as digital engineering accelerates regulatory validation and customized product development. Aerospace & Defense continues emphasizing high-fidelity simulation for certification efficiency, while Electronics & Semiconductor manufacturers increasingly rely on virtual prototypes to manage miniaturized and highly integrated product architectures. Industrial Manufacturing and Construction further strengthen adoption through smart factory modernization and digital infrastructure initiatives. Companies are expanding industry-focused engineering platforms, automation capabilities, and collaborative development environments to address specialized operational requirements.

The market is segmented into Automotive Manufacturers, Aerospace & Defense Companies, Industrial Manufacturers, Electronics & Semiconductor Companies, Healthcare & Medical Device Companies, Engineering Service Providers, and Research & Academic Institutions. Automotive Manufacturers remain the dominant end-user group with approximately 32% of overall deployment activity, supported by extensive product portfolios, global engineering operations, and continuous vehicle innovation programs. Large manufacturers improve engineering productivity by nearly 33% while reducing physical testing requirements through integrated simulation workflows. Technology providers continue delivering customized enterprise platforms, long-term licensing models, and strategic implementation partnerships. Healthcare & Medical Device Companies represent the fastest-growing end-user segment as digital validation supports complex device design, regulatory documentation, and precision engineering. Aerospace & Defense organizations continue expanding advanced simulation capabilities for mission-critical systems, while Electronics & Semiconductor Companies increasingly adopt virtual engineering to accelerate high-performance product development. Engineering Service Providers strengthen market expansion by delivering outsourced simulation expertise, and Research & Academic Institutions support future workforce development and engineering innovation. Vendors are broadening ecosystem partnerships, industry-specific solutions, and cloud deployment models to address increasingly specialized enterprise requirements.

Europe accounted for the largest market share at 36.8%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.6% between 2026 and 2033.

North America represents approximately 31.4% of the global Virtual Prototypes Market, supported by extensive deployment across aerospace, automotive, medical devices, industrial automation, and semiconductor manufacturing. Large enterprises continue integrating AI-driven simulation, cloud engineering, and digital twin technologies to shorten product development cycles and improve engineering collaboration. More than 69% of major manufacturers in the region utilize simulation-based validation before physical testing, strengthening operational efficiency and reducing redesign costs. Strategic investment in cloud-native engineering platforms and high-performance computing infrastructure continues to accelerate enterprise-scale deployment. Technology vendors are expanding ecosystem partnerships, enhancing interoperability between CAD, CAE, and PLM platforms, and strengthening collaborative engineering capabilities to support increasingly complex product development programs.

United States Market Outlook: The United States remains the largest contributor within North America due to its leadership in engineering software, aerospace innovation, automotive R&D, and semiconductor design. More than 72% of Fortune 500 industrial manufacturers have adopted enterprise digital engineering platforms across multiple business units. Continuous investment in AI-enabled engineering software, advanced computing infrastructure, and collaborative product lifecycle management strengthens the country's competitive position while accelerating deployment across defense, healthcare, and industrial manufacturing.

Europe leads the global Virtual Prototypes Market with a 36.8% market share, supported by advanced automotive manufacturing, aerospace engineering, industrial machinery production, and widespread Industry 4.0 implementation. Manufacturers increasingly integrate virtual validation into product lifecycle management to improve production efficiency, engineering precision, and sustainability objectives. More than 74% of large industrial manufacturers across key European economies utilize simulation technologies during early product development stages. Cross-industry digital manufacturing initiatives and continued modernization of engineering infrastructure are strengthening enterprise adoption while encouraging broader deployment of integrated simulation ecosystems across complex manufacturing environments.

Germany Market Outlook: Germany is the region's largest market, driven by its globally competitive automotive, industrial equipment, and precision engineering sectors. Approximately 23% of global advanced industrial virtual prototype deployments are concentrated in Germany, supported by strong investment in digital manufacturing and engineering automation. Enterprise collaboration between software developers, manufacturing companies, and research institutions continues accelerating AI-assisted simulation, digital twins, and integrated engineering platforms, reinforcing Germany's position as the technological leader within the global virtual prototype ecosystem.

Asia-Pacific accounts for approximately 24.2% of the global market and represents the fastest-expanding regional landscape as manufacturers accelerate digital transformation across automotive, electronics, semiconductor, and industrial equipment production. Rapid factory modernization, expanding smart manufacturing initiatives, and increasing engineering software adoption continue strengthening deployment across high-volume production environments. Nearly 61% of new engineering software implementations within large manufacturing enterprises now include integrated simulation capabilities. Companies are expanding cloud engineering infrastructure, AI-enabled product development, and collaborative digital platforms to improve production flexibility and reduce engineering complexity.

China Market Outlook: China remains the largest market across Asia-Pacific due to its extensive manufacturing ecosystem and expanding investment in industrial digitalization. More than 65% of large electronics and automotive manufacturers have adopted advanced simulation technologies within product development operations. Continued expansion of smart factories, high-performance computing infrastructure, and domestic engineering software capabilities enables enterprises to accelerate innovation while strengthening supply-chain resilience and advanced manufacturing competitiveness.

South America represents approximately 4.8% of the global market as manufacturers increasingly digitalize engineering processes across automotive production, mining equipment, energy infrastructure, and industrial machinery. Growing investment in digital manufacturing platforms supports gradual adoption of virtual validation despite infrastructure disparities across several industries. Nearly 36% of large industrial enterprises have expanded engineering software deployment during modernization initiatives. Companies continue investing in workforce development, localized implementation services, and cloud engineering environments to improve operational efficiency while reducing development risks associated with complex industrial equipment.

Brazil Market Outlook: Brazil dominates the regional market through its diversified manufacturing base and expanding automotive and aerospace industries. Approximately 58% of enterprise virtual engineering deployments within South America are concentrated in Brazil. Manufacturers increasingly integrate simulation-based validation into industrial production programs while strengthening partnerships with global engineering software providers to improve product quality, operational productivity, and manufacturing competitiveness.

Middle East & Africa accounts for approximately 2.8% of the global market, supported by increasing industrial diversification, infrastructure modernization, and investment in advanced engineering capabilities. Energy, construction, aerospace, and industrial development projects are encouraging broader adoption of digital engineering solutions that improve design accuracy and operational planning. Around 33% of large engineering organizations are expanding cloud-based simulation capabilities to support complex infrastructure programs. Technology providers continue strengthening regional partnerships, implementation services, and engineering training programs to accelerate enterprise adoption across strategically important industries.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale industrial diversification initiatives, smart manufacturing investments, and infrastructure modernization programs. More than 40% of newly established advanced industrial facilities incorporate digital engineering technologies during project planning and design phases. Continued investment in industrial cities, aerospace capabilities, and advanced manufacturing ecosystems is strengthening demand for integrated virtual prototype platforms while supporting long-term engineering innovation and operational excellence.

The Virtual Prototypes Market is led by Siemens Digital Industries Software, Dassault Systèmes, PTC, Ansys, and Autodesk, while Altair and specialized simulation providers compete through industry-focused innovation. Global platform vendors primarily compete against regional engineering software specialists on technology depth rather than price alone. The top five players collectively control approximately 64% of the market. Competition centers on AI-enabled simulation, cloud-native collaboration, interoperability, and digital twin integration, with nearly 68% of enterprise customers prioritizing platform compatibility and over 57% demanding end-to-end engineering workflows. Around 46% of new enterprise contracts include long-term cloud deployment and lifecycle management capabilities. Companies are expanding through strategic partnerships, industrial AI integration, vertical platform development, and acquisition of niche engineering software providers. The competitive landscape is shifting toward unified digital engineering ecosystems, making fragmented standalone solutions less attractive. High switching costs, complex enterprise integration, and engineering data migration remain significant entry barriers. Success depends on delivering scalable, intelligent, interoperable platforms with measurable engineering productivity advantages.

Dassault Systèmes

PTC Inc.

Ansys, Inc.

Autodesk, Inc.

Altair Engineering Inc.

Cadence Design Systems, Inc.

Hexagon AB

ESI Group

COMSOL AB

Siemens EDA

Bentley Systems, Incorporated

Artificial intelligence, cloud-native simulation, and digital twin technologies are redefining virtual prototype development across advanced manufacturing. More than 61% of large engineering organizations now integrate AI-assisted design optimization into simulation workflows, while automated model generation reduces engineering effort by approximately 28%. Cloud-based engineering environments support globally distributed design teams, enabling faster collaboration and standardized product validation across multiple facilities. These technologies improve engineering consistency while reducing physical testing requirements and accelerating product commercialization.

Modern AI-driven virtual prototype platforms outperform conventional standalone simulation tools by reducing validation cycles by nearly 35% and improving multidisciplinary engineering productivity by approximately 30%. Around 58% of enterprise manufacturers now deploy integrated CAD, CAE, and PLM environments instead of disconnected engineering applications. Global software leaders and industrial manufacturers benefit most from unified engineering ecosystems because integrated workflows improve decision-making, strengthen digital continuity, and reduce operational complexity across product development programs.

Between 2026 and 2028, industrial AI, physics-informed simulation, and real-time digital twins will become standard capabilities within enterprise engineering platforms. Adoption of intelligent engineering assistants is expected to exceed 70% among large manufacturers, enabling predictive design optimization, automated compliance validation, and continuous lifecycle simulation. Organizations investing early in interoperable digital engineering ecosystems will secure stronger operational resilience, faster innovation cycles, and greater competitive differentiation.

February 2025 Dassault Systèmes partnered with Volkswagen Group to deploy the cloud-based 3DEXPERIENCE platform across Volkswagen, Audi, and Porsche engineering operations, enabling virtual twin-driven vehicle development for multiple brands. Source: www.3ds.com

February 2025 Dassault Systèmes introduced 3D UNIV+RSES with generative AI services, integrating virtual twins and AI-driven engineering workflows for industrial customers. Source: www.3ds.com

April 2025 Dassault Systèmes and Airbus expanded their strategic partnership, extending the 3DEXPERIENCE platform to more than 20,000 users supporting future civil, military aircraft, and helicopter programs. Source: www.3ds.com

February 2026 Dassault Systèmes announced a strategic partnership with NVIDIA to integrate industrial AI with virtual twin technology, enabling science-based AI models for engineering and manufacturing.

This report delivers comprehensive analysis of the Virtual Prototypes Market across Software, Services, and Integrated Solutions, covering major applications including automotive, aerospace and defense, industrial manufacturing, healthcare, electronics, construction, and other engineering sectors. The assessment evaluates demand across automotive manufacturers, aerospace companies, industrial enterprises, electronics producers, engineering service providers, and research institutions. Regional coverage spans Europe, North America, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global industrial deployment activity.

The report examines AI-enabled simulation, digital twins, cloud engineering, product lifecycle management, collaborative design platforms, and high-performance computing trends shaping enterprise adoption. It provides strategic benchmarking across leading companies, evaluates deployment patterns, technology integration, competitive positioning, innovation priorities, and evolving enterprise purchasing strategies. The analysis supports investment planning, product expansion, partnership evaluation, market entry decisions, and long-term competitive positioning between 2026 and 2033 while identifying emerging industrial opportunities and evolving customer requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 778.8 Million |

| Market Revenue (2033) | USD 2,253.0 Million |

| CAGR (2026–2033) | 14.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Siemens Digital Industries Software; Dassault Systèmes; PTC Inc.; Ansys, Inc.; Autodesk, Inc.; Altair Engineering Inc.; Cadence Design Systems, Inc.; Hexagon AB; ESI Group; COMSOL AB; Bentley Systems, Incorporated |

| Customization & Pricing | Available on Request (10% Customization Free) |