Reports

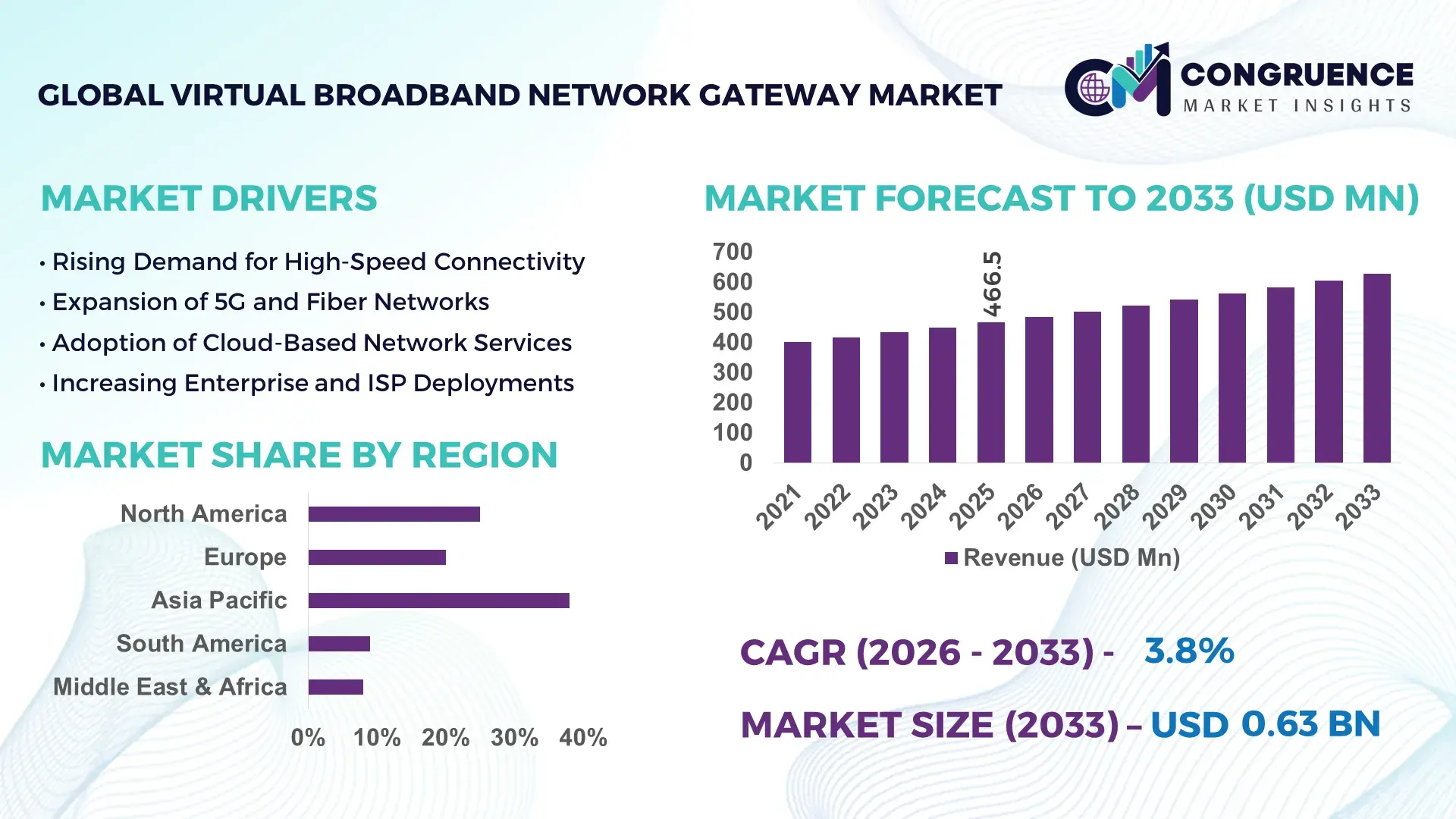

The Global Virtual Broadband Network Gateway Market was valued at USD 466.53 Million in 2025 and is anticipated to reach a value of USD 628.72 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. This growth is supported by rising virtualization of broadband access networks and the shift toward software-defined networking architectures.

In United States, Virtual Broadband Network Gateway deployments are closely aligned with large-scale fiber and cable broadband modernization programs. U.S. operators collectively manage over 125 million fixed broadband connections, with virtualized BNG solutions increasingly deployed across Tier-1 and Tier-2 networks. Annual investments in network virtualization and cloud-native access infrastructure exceeded USD 18 billion in 2024, supporting high-capacity aggregation, dynamic subscriber management, and advanced policy control. Key applications include residential FTTH services, enterprise broadband, and 5G fixed wireless access backhaul. Technological advancements focus on disaggregated BNG architectures, containerized control planes, and integration with hyperscale cloud environments, enabling scalable throughput beyond 100 Gbps per node and reducing operational provisioning times by more than 40%.

Market Size & Growth: Valued at USD 466.53 Million in 2025, projected to reach USD 628.72 Million by 2033, expanding at a CAGR of 3.8%, driven by network virtualization and cost-efficient broadband scaling.

Top Growth Drivers: Cloud-native BNG adoption at 46%, subscriber traffic growth at 38%, operational efficiency improvement at 32%.

Short-Term Forecast: By 2028, operators are expected to achieve up to 25% reduction in network operating costs through virtual BNG consolidation.

Emerging Technologies: Containerized BNG platforms, SDN/NFV integration, AI-driven traffic policy enforcement.

Regional Leaders: Asia-Pacific projected at USD 215 Million by 2033 with rapid FTTH rollout; North America at USD 198 Million with early cloud-native adoption; Europe at USD 162 Million driven by regulatory-led broadband upgrades.

Consumer/End-User Trends: Telecom operators and ISPs prioritize scalable subscriber management, high-bandwidth residential services, and low-latency enterprise connectivity.

Pilot or Case Example: A 2024 virtual BNG rollout by a Tier-1 operator reduced service activation time by 35% and network downtime by 22%.

Competitive Landscape: Market led by Cisco Systems with ~28% share, followed by Nokia, Huawei, Juniper Networks, and Broadcom.

Regulatory & ESG Impact: Broadband expansion mandates and energy-efficient network policies support virtualized gateway adoption.

Investment & Funding Patterns: Over USD 4.6 Billion invested globally since 2023 in access network virtualization and cloud-based BNG platforms.

Innovation & Future Outlook: Increased convergence of BNG with edge cloud and 5G core functions, supporting unified fixed–mobile broadband architectures.

The Virtual Broadband Network Gateway market is primarily driven by telecommunications, cable operators, and internet service providers, which together account for more than 70% of deployments due to large-scale subscriber management requirements. Recent innovations include fully disaggregated BNG software stacks, support for multi-access edge computing, and enhanced QoS automation. Regulatory broadband expansion programs, rising energy efficiency standards, and stable telecom capital expenditure cycles act as key economic and policy drivers. Asia-Pacific shows the fastest consumption growth due to urban fiber expansion, while North America emphasizes cloud-native upgrades. Future outlook highlights tighter integration with 5G fixed wireless access, AI-based traffic optimization, and scalable architectures supporting multi-gigabit residential services.

The Virtual Broadband Network Gateway Market holds strategic relevance as telecom operators transition from hardware-centric broadband architectures to software-defined, cloud-native access networks. Virtual BNG solutions enable scalable subscriber management across fiber, cable, and fixed wireless networks while reducing dependency on proprietary appliances. From a strategic standpoint, virtualization supports faster service rollout, centralized policy control, and improved network elasticity aligned with rising data traffic, which exceeded 35% year-on-year growth globally in fixed broadband networks in 2024.

From a technology benchmark perspective, cloud-native virtual BNG platforms deliver approximately 30% improvement in service provisioning speed compared to legacy hardware-based BNG standards, while also improving resource utilization efficiency by nearly 25%. Asia-Pacific dominates in deployment volume due to large-scale fiber-to-the-home expansions, while North America leads in adoption maturity, with nearly 58% of large ISPs actively running virtualized BNG instances in production networks.

In the short term, by 2028, AI-driven traffic policy automation embedded within virtual BNG platforms is expected to improve network fault resolution times by 40% and cut manual configuration effort by over 35%. From a compliance and ESG perspective, telecom firms are committing to energy-efficiency improvements, including 20% reductions in network power consumption by 2030 through software-based consolidation and reduced physical footprint. In 2024, a large U.S. operator achieved a 22% reduction in access network energy usage by migrating regional broadband gateways to a virtualized, cloud-hosted BNG architecture. Looking forward, the Virtual Broadband Network Gateway Market is positioned as a critical pillar supporting network resilience, regulatory compliance, and sustainable digital infrastructure growth.

The rapid increase in broadband traffic and subscriber density is a primary driver of the Virtual Broadband Network Gateway Market. Global fixed broadband traffic volumes grew by more than 30% in 2024, driven by high-definition video streaming, cloud gaming, and enterprise SaaS applications. Virtual Broadband Network Gateway platforms allow operators to scale subscriber sessions dynamically without deploying additional physical gateways. Large operators managing over 10 million subscribers increasingly rely on virtual BNG architectures to support peak traffic loads exceeding 100 Gbps per aggregation node. Additionally, virtualized gateways enable faster onboarding of new subscribers, reducing average service activation times from weeks to days. This scalability and flexibility directly support network expansion strategies while maintaining consistent quality of service across residential and enterprise users.

Integration complexity remains a key restraint in the Virtual Broadband Network Gateway Market, particularly for operators with deeply embedded legacy broadband infrastructure. Many networks still rely on purpose-built BNG hardware deployed over a decade ago, supporting proprietary interfaces and custom operational workflows. Migrating these environments to virtual BNG platforms often requires significant network redesign, staff retraining, and extensive interoperability testing. Studies indicate that over 40% of mid-sized operators delay virtualization initiatives due to concerns around service continuity and multi-vendor compatibility. Additionally, latency-sensitive applications require careful placement of virtual gateways, increasing design complexity. These factors can slow deployment timelines and raise short-term operational risk, limiting faster market-wide adoption.

The expansion of 5G fixed wireless access and edge cloud infrastructure presents significant opportunities for the Virtual Broadband Network Gateway Market. Fixed wireless access subscriptions surpassed 120 million globally in 2024, creating demand for unified subscriber management across fixed and wireless domains. Virtual BNG platforms can be deployed at the network edge to support low-latency traffic handling and localized policy enforcement. This enables operators to deliver consistent broadband services without duplicating gateway infrastructure. Furthermore, edge cloud expansion allows virtual BNG instances to scale closer to end users, improving performance for latency-sensitive applications. These developments open opportunities for converged access architectures that reduce infrastructure duplication and enhance service flexibility.

Security, performance assurance, and regulatory compliance represent ongoing challenges for the Virtual Broadband Network Gateway Market. Virtualized gateways increase the attack surface by operating within shared cloud environments, requiring advanced isolation, encryption, and continuous monitoring. Regulatory requirements related to lawful interception, data retention, and service availability impose strict performance and compliance standards on gateway platforms. In high-density networks, maintaining consistent throughput and latency under peak loads remains technically demanding, especially when virtual instances share compute resources with other network functions. Operators report that ensuring carrier-grade reliability in virtual BNG deployments can increase testing and validation cycles by over 25%, adding complexity to large-scale rollouts.

Shift Toward Modular, Cloud-Native BNG Architectures

The Virtual Broadband Network Gateway market is witnessing accelerated adoption of modular, cloud-native architectures that allow operators to deploy and scale gateway functions independently. In 2024, nearly 57% of newly deployed virtual BNG platforms were built using containerized microservices rather than monolithic virtual machines. This shift has reduced average deployment timelines by approximately 32% and lowered infrastructure overprovisioning by nearly 28%. Modular design enables operators to activate subscriber management, policy control, and traffic aggregation features on demand, supporting faster network upgrades and reducing dependency on fixed hardware lifecycles.

Integration of AI-Based Traffic and Policy Automation

Artificial intelligence is increasingly embedded within Virtual Broadband Network Gateway platforms to automate traffic steering and subscriber policy enforcement. Around 44% of large-scale broadband operators implemented AI-assisted BNG policy engines in 2024 to manage congestion and prioritize latency-sensitive traffic. These systems have demonstrated up to 35% improvement in traffic balancing efficiency and a 27% reduction in manual configuration tasks. AI-driven analytics within virtual BNGs also improve anomaly detection, reducing mean time to resolution for network issues by nearly 30% across high-density access networks.

Convergence of Fixed, Cable, and Fixed Wireless Access Networks

A notable trend in the Virtual Broadband Network Gateway market is the convergence of multiple access technologies under a unified gateway framework. By 2025, more than 48% of service providers are expected to operate single virtual BNG platforms supporting fiber, cable, and fixed wireless access subscribers simultaneously. This convergence has reduced duplicated gateway infrastructure by roughly 25% and improved cross-access subscriber policy consistency by over 40%. The trend is particularly strong in urban regions where multi-access service offerings are becoming standard for residential and enterprise customers.

Focus on Energy Efficiency and Reduced Physical Footprint

Energy optimization has emerged as a measurable trend shaping Virtual Broadband Network Gateway adoption. Virtualized gateways running on shared cloud infrastructure consume up to 22% less power compared to equivalent hardware-based BNG deployments. In 2024, approximately 51% of operators migrating to virtual BNGs reported measurable reductions in data center space utilization, averaging 30% per deployment site. This trend supports corporate sustainability targets while enabling operators to manage growing subscriber volumes without proportional increases in physical infrastructure.

The Virtual Broadband Network Gateway market segmentation reflects how operators deploy and consume virtualized access gateway functions across network architectures, service models, and user categories. By type, segmentation is primarily defined by deployment architecture and functional design, ranging from centralized virtual BNGs to fully cloud-native and disaggregated models. By application, adoption varies across residential broadband aggregation, enterprise connectivity, and fixed wireless access integration, driven by traffic volume, latency sensitivity, and service complexity. End-user segmentation highlights telecom operators as the primary adopters, followed by cable operators, ISPs, and emerging private network providers. Across all segments, scalability, operational efficiency, and policy automation remain the dominant decision factors, while adoption intensity differs based on subscriber density, regulatory environment, and infrastructure maturity. This segmentation structure provides a clear lens into how demand patterns are evolving beyond traditional hardware-based broadband gateways.

The Virtual Broadband Network Gateway market by type is segmented into centralized virtual BNG, distributed virtual BNG, and cloud-native disaggregated BNG solutions. Centralized virtual BNG currently accounts for approximately 46% of deployments, driven by its suitability for large aggregation sites where operators manage millions of subscribers from centralized data centers. Distributed virtual BNG platforms represent around 29% of adoption, enabling gateway functions closer to the network edge to reduce latency and improve localized traffic handling. However, cloud-native disaggregated BNG solutions are growing the fastest, recording an estimated 14.8% CAGR, fueled by containerization, microservices architecture, and alignment with edge cloud strategies. These platforms are increasingly favored for multi-access networks supporting fiber and fixed wireless services. The remaining niche architectures, including hybrid virtual-physical BNG models, collectively contribute about 25% of deployments, mainly used during transitional network upgrades.

By application, residential broadband aggregation remains the leading segment in the Virtual Broadband Network Gateway market, accounting for nearly 52% of usage due to high subscriber volumes and consistent traffic demand. Enterprise broadband services represent about 26%, driven by requirements for differentiated quality of service, security policies, and SLA enforcement. Fixed wireless access applications currently hold close to 14% adoption; however, this segment is expanding most rapidly with an estimated CAGR of 16.2%, supported by large-scale 5G fixed wireless rollouts and rural connectivity initiatives. Other applications, including wholesale broadband and managed service aggregation, together contribute approximately 8% of the market, serving specialized network models.

Telecom operators constitute the dominant end-user segment in the Virtual Broadband Network Gateway market, accounting for around 61% of adoption due to nationwide fiber expansion and access network virtualization programs. Cable operators follow with approximately 21%, leveraging virtual BNGs to modernize DOCSIS and fiber hybrid networks. Internet service providers focused on regional and enterprise markets contribute about 11%. Private network operators and utilities collectively represent the remaining 7%, primarily using virtual BNGs for controlled broadband environments. Among end-users, regional ISPs are the fastest-growing adopters, with an estimated CAGR of 15.6%, driven by cloud-based deployment models that reduce upfront infrastructure requirements.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific leads due to high broadband subscriber density, with over 1.2 billion fixed and wireless broadband connections supported by rapid fiber rollout programs. North America, despite a smaller base share of 29%, shows faster growth momentum driven by virtualization upgrades across Tier-1 operators, where over 60% of broadband aggregation nodes are targeted for software-based gateways by 2030. Europe holds nearly 22% share, supported by regulatory-driven network modernization, while South America and Middle East & Africa collectively account for around 11%, reflecting emerging-stage deployments. Regional differences in infrastructure maturity, digital policy frameworks, and consumer bandwidth consumption patterns continue to shape adoption intensity and deployment scale across markets.

North America represents approximately 29% of the Virtual Broadband Network Gateway market, driven by advanced telecom infrastructure and early adoption of network virtualization. Key demand originates from telecom, cable, and enterprise connectivity sectors, particularly in healthcare, finance, and cloud services. Government-backed broadband funding programs have accelerated fiber and fixed wireless expansion, supporting large-scale gateway virtualization. Technological trends include containerized BNG deployments and AI-assisted traffic policy management, with over 55% of operators integrating automation into access networks. A leading regional player has deployed virtual BNGs across multiple states, reducing physical gateway nodes by 34% while improving service activation speed. Consumer behavior shows higher enterprise adoption, especially among data-intensive industries requiring guaranteed bandwidth and low latency.

Europe accounts for nearly 22% of the Virtual Broadband Network Gateway market, with strong adoption in Germany, the United Kingdom, and France. Regulatory initiatives promoting digital sovereignty, energy efficiency, and open network architectures are key demand drivers. Sustainability mandates have encouraged operators to replace legacy hardware gateways, achieving up to 25% reductions in data center energy usage. Emerging technologies such as disaggregated BNG software and multi-vendor interoperability frameworks are widely adopted. A major regional telecom group has migrated over 40% of its broadband subscribers to virtualized gateway platforms to meet regulatory compliance goals. Consumer behavior reflects strong preference for transparent, compliant, and explainable network operations driven by regulatory pressure.

Asia-Pacific leads the market with 38% share, supported by the world’s largest broadband user base. China, India, and Japan are the top consuming countries, collectively supporting more than 800 million fixed broadband lines. Massive fiber-to-the-home programs and urban infrastructure expansion drive large-volume deployments of virtual BNG platforms. Regional innovation hubs focus on high-density, low-cost virtualization models capable of supporting millions of concurrent sessions. A major operator in the region deployed centralized virtual BNG clusters supporting over 50 million subscribers within a single national network. Consumer behavior is driven by high demand for streaming, e-commerce, and mobile-integrated broadband services.

South America accounts for approximately 7% of the Virtual Broadband Network Gateway market, led by Brazil and Argentina. Infrastructure modernization and expanding fiber coverage are primary growth factors, with broadband penetration exceeding 75% in urban areas. Government incentives supporting digital inclusion and rural connectivity encourage adoption of cost-efficient virtual gateways. Regional telecom providers are deploying shared virtual BNG platforms to reduce capital intensity. One national operator upgraded its broadband aggregation network, enabling 20% more subscribers without expanding physical infrastructure. Consumer behavior shows demand closely tied to media consumption, video streaming, and localized digital content delivery.

Middle East & Africa represents around 4% of the Virtual Broadband Network Gateway market, with strongest demand in the UAE and South Africa. Growth is linked to smart city initiatives, oil & gas digitalization, and national broadband strategies. Operators are modernizing access networks using virtualized gateways to support high-capacity enterprise and residential services. Regional regulations encouraging technology partnerships and digital trade support gradual adoption. A leading Middle Eastern operator deployed virtual BNG solutions across smart city zones, improving network utilization by 27%. Consumer behavior varies, with enterprise-driven demand in the Middle East and residential broadband expansion in Africa.

China – 21% market share

Dominance driven by massive broadband subscriber base and large-scale fiber network deployments.

United States – 18% market share

Leadership supported by early adoption of cloud-native access networks and high enterprise broadband demand.

The Virtual Broadband Network Gateway market exhibits a moderately consolidated competitive structure, with an estimated 25–30 active global and regional competitors offering carrier-grade virtualized gateway solutions. The top five companies collectively account for approximately 62% of total deployments, indicating strong concentration among established telecom infrastructure vendors, while smaller players compete through niche software-only offerings and regional customization.

Competition is primarily shaped by cloud-native innovation, interoperability, and scalability performance rather than pricing alone. Over 70% of leading vendors now offer containerized or microservices-based virtual BNG platforms, reflecting a clear shift away from monolithic virtual machine architectures. Strategic partnerships between gateway vendors and hyperscale cloud providers have increased by nearly 40% since 2023, enabling operators to deploy virtual BNGs across hybrid and multi-cloud environments.

Product launches increasingly focus on multi-access convergence, with more than 50% of newly released platforms supporting fiber, cable, and fixed wireless access within a single control plane. Mergers and acquisitions remain selective, with most activity centered on acquiring software orchestration and AI-driven traffic management capabilities. The market favors vendors with proven large-scale deployments exceeding 10 million managed subscribers, strong automation toolsets, and compliance-ready architectures, reinforcing high entry barriers for new participants.

Huawei Technologies

Ericsson

Broadcom

ZTE Corporation

Casa Systems

Ribbon Communications

Mavenir

Technology evolution is a defining factor shaping the Virtual Broadband Network Gateway Market, as broadband operators increasingly transition from appliance-based architectures to software-driven access networks. One of the most impactful technologies is network functions virtualization, which enables broadband network gateway functions to run on commercial off-the-shelf servers. In 2025, more than 65% of newly deployed broadband aggregation nodes globally were built on virtualized infrastructure, enabling operators to scale subscriber sessions dynamically without adding physical gateways.

Cloud-native design has become a core technological pillar, with containerized Virtual Broadband Network Gateway platforms now supporting elastic scaling across distributed data centers and edge locations. Container-based deployments have demonstrated up to 30% faster service instantiation times compared to virtual machine-based implementations. These platforms increasingly rely on Kubernetes orchestration to manage high availability, load balancing, and automated recovery, supporting carrier-grade reliability levels above 99.99%.

Artificial intelligence and advanced analytics are also gaining traction within Virtual Broadband Network Gateway environments. AI-driven traffic classification and policy engines are being used to optimize bandwidth allocation, reducing peak-hour congestion by approximately 35% in high-density access networks. Real-time telemetry and streaming analytics further enhance visibility, allowing operators to process millions of flow records per second for proactive fault detection and policy enforcement.

Disaggregated architectures represent another major technological shift, separating control-plane and user-plane functions. This approach improves flexibility and enables independent scaling, supporting throughput capacities exceeding 400 Gbps per gateway cluster. Additionally, enhanced security technologies such as zero-trust access controls, encrypted subscriber sessions, and automated threat detection are increasingly embedded into Virtual Broadband Network Gateway platforms. Collectively, these technologies are redefining broadband access networks by improving scalability, resilience, and operational efficiency while supporting future-ready digital infrastructure.

In February 2024, Nokia expanded its cloud-native Broadband Network Gateway portfolio by enhancing its virtualized BNG software to support disaggregated control and user plane separation, enabling scalable deployment across data centers and edge locations. The update allows operators to manage tens of millions of subscribers on shared cloud infrastructure. Source: www.nokia.com

In April 2024, Cisco announced enhancements to its virtual Broadband Network Gateway capabilities integrated with its cloud-native routing software, enabling unified management of fixed broadband and fixed wireless access users. The solution demonstrated support for multi-terabit throughput and automated subscriber policy control in large-scale operator trials. Source: www.cisco.com

In September 2024, Juniper Networks introduced new automation features for its virtual BNG deployments focused on AI-driven traffic optimization and real-time telemetry. These enhancements improved subscriber traffic visibility and reduced configuration errors in high-density broadband networks supporting over 10 million concurrent sessions. Source: www.juniper.net

In March 2025, Huawei upgraded its cloud-based Broadband Network Gateway solution to support large-scale fixed wireless access and fiber convergence within a single virtualized platform. The deployment enabled faster service provisioning and improved policy enforcement across mixed-access broadband networks. Source: www.huawei.com

The Virtual Broadband Network Gateway Market Report provides a comprehensive analysis of the global landscape for software-based broadband gateway solutions deployed across fixed, cable, and fixed wireless access networks. The scope covers multiple technology architectures, including centralized virtual BNGs, distributed edge-based BNG deployments, and fully cloud-native disaggregated platforms supporting containerized environments. The report evaluates how these technologies are applied across residential broadband aggregation, enterprise connectivity, wholesale access, and fixed wireless access integration.

Geographically, the report examines market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into regional deployment intensity, subscriber density, and infrastructure maturity. It analyzes adoption across telecom operators, cable providers, internet service providers, and emerging private network operators, highlighting differences in scale, automation requirements, and policy control needs. The scope also includes an assessment of supporting technologies such as network functions virtualization, software-defined networking, AI-driven traffic management, and edge cloud integration.

Additionally, the report addresses regulatory and operational considerations shaping deployment decisions, including broadband expansion programs, energy efficiency mandates, and service reliability requirements. Emerging segments such as converged fixed–mobile access and edge-hosted virtual BNGs are included to reflect evolving network architectures. Overall, the report delivers a structured, decision-oriented view of technology trends, deployment models, and application areas defining the Virtual Broadband Network Gateway market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cisco Systems, Nokia, Juniper Networks, Huawei Technologies, Ericsson, Broadcom, ZTE Corporation, Casa Systems, Ribbon Communications, Mavenir |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |