Reports

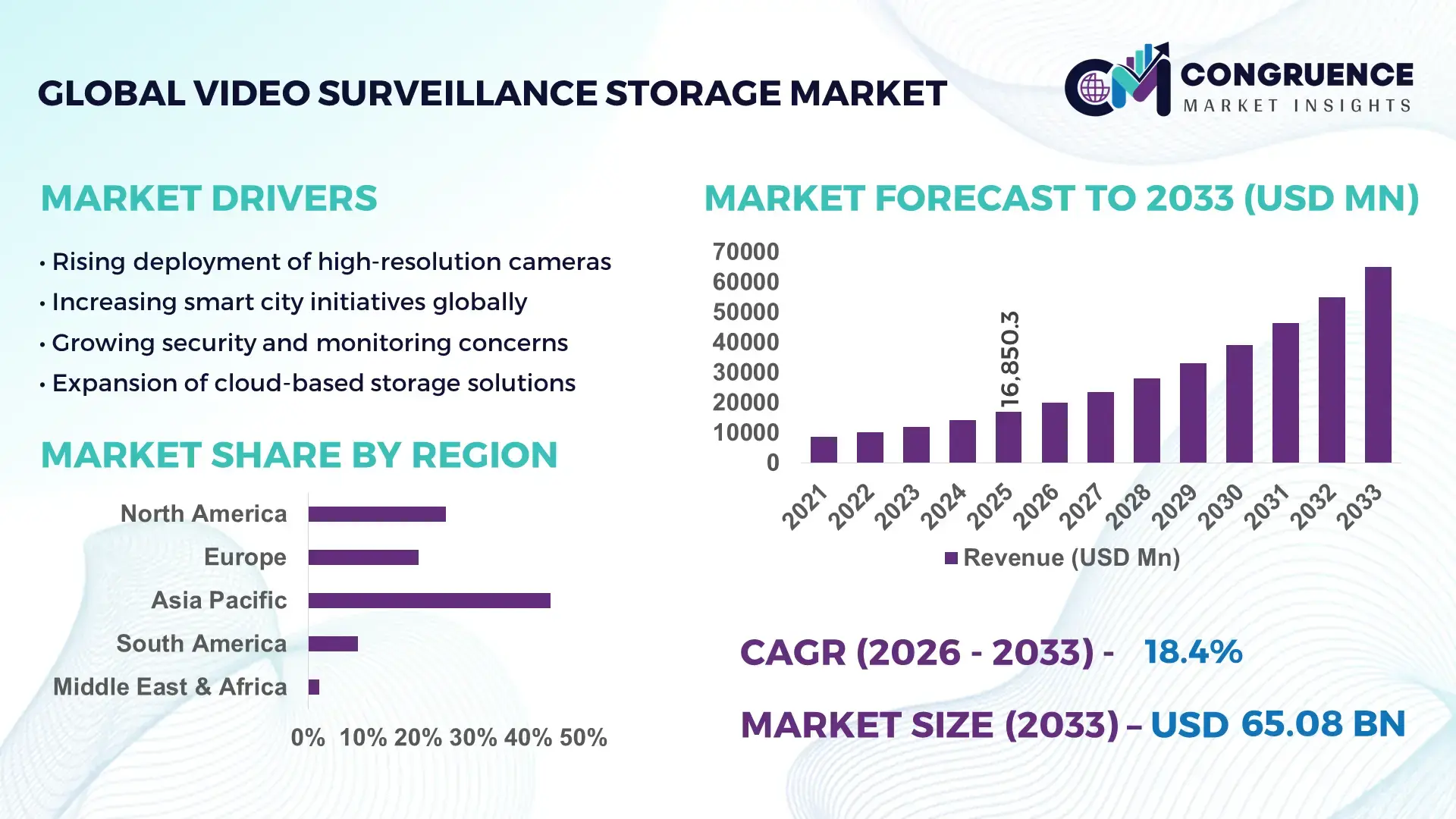

The Global Video Surveillance Storage Market was valued at USD 16850.3 Million in 2025 and is anticipated to reach a value of USD 65076.09 Million by 2033 expanding at a CAGR of 18.4% between 2026 and 2033.

Rapid migration from legacy DVR-based systems to scalable cloud and hybrid storage architectures is accelerating capacity demand, with AI-enabled video analytics increasing storage loads by over 35% per deployment. Between 2024 and 2026, heightened urban security mandates and data localization laws across Asia and Europe have driven on-premise and edge storage investments, particularly in regulated sectors such as transportation and public safety.

China dominates the global landscape with approximately 38% market share, supported by large-scale smart city programs across more than 500 urban centers and annual infrastructure investments exceeding USD 20 billion. The country processes over 60% of global surveillance video data, driven by dense camera networks exceeding 200 million active units. Compared to North America’s higher cloud adoption (over 55% deployments), China maintains a stronger edge-storage model due to regulatory constraints, delivering 25% faster real-time processing efficiency. India and Southeast Asia are emerging as high-growth regions, with deployments expanding at over 30% annually due to urbanization and infrastructure digitization. This geographic imbalance highlights a critical strategic shift toward localized storage solutions and hybrid deployment models to balance compliance, latency, and cost efficiency.

Market Size & Growth: USD 16.8B (2025) to USD 65.0B (2033), CAGR 18.4%, driven by AI-based video analytics increasing storage demand by 35% per system.

Top Growth Drivers: AI analytics (+35%), smart city expansion (+28%), data localization mandates (+22%).

Short-Term Forecast: By 2027, storage cost per TB expected to decline by 18% while processing efficiency improves by 27% with hybrid architectures.

Emerging Technologies: AI-driven compression reduces storage needs by 30%; edge computing adoption exceeds 45%; object-based storage growing at 25% annually.

Regional Leaders: Asia-Pacific USD 28B (smart cities expansion), North America USD 18B (cloud adoption >55%), Europe USD 12B (compliance-driven storage).

Consumer/End-User Trends: Over 62% of enterprises shifting to hybrid storage; public safety accounts for 40% of deployments.

Pilot/Case Example: 2025 metro surveillance upgrade reduced retrieval time by 42% and storage costs by 20% using AI indexing.

Competitive Landscape: Top player holds ~14% share; key players include 4–5 major global storage and surveillance providers dominating enterprise contracts.

Regulatory & ESG Impact: Data sovereignty laws increased local storage demand by 33%; energy-efficient storage systems cut power usage by 18%.

Investment & Funding: Over USD 9B invested (2024–2026) in cloud and edge storage expansion amid supply chain localization trends.

Innovation & Future Outlook: Transition to AI-optimized, autonomous storage systems improving data retrieval speed by 40% and enabling predictive surveillance capabilities.

Banking, transportation, and government sectors collectively contribute over 65% of total demand, with retail adding another 18% through loss prevention systems. AI-based video compression and intelligent indexing have reduced storage footprint by 25%, while edge-based storage deployments now account for 45% of new installations. Asia-Pacific leads demand growth at over 30%, supported by infrastructure expansion and regulatory enforcement. Increasing integration of predictive analytics into storage systems signals a shift toward proactive security frameworks, setting the stage for more autonomous and scalable surveillance ecosystems.

Video surveillance storage is rapidly transforming into a core digital infrastructure layer, directly influencing security intelligence, operational efficiency, and data-driven decision-making across industries. The accelerating shift toward AI-powered video analytics is pushing storage systems beyond passive archiving into active, real-time processing ecosystems, making storage a competitive differentiator rather than a backend utility. At the same time, tightening data sovereignty regulations and supply chain localization pressures are forcing enterprises to redesign storage architectures for compliance and resilience.

AI-enabled compression and intelligent storage management improve efficiency by 30% while reducing cost by 22% compared to legacy DVR-based systems, fundamentally optimizing storage economics. Asia-Pacific leads in volume with over 48% deployment share, while North America leads in adoption and innovation with more than 55% cloud-integrated storage penetration. Over the next 2–3 years, hybrid storage adoption will exceed 65%, reducing data retrieval latency by 35% and improving system uptime by 20%. Energy-efficient storage solutions are also emerging as an ESG advantage, lowering power consumption by 18% and enabling compliance-driven market access.

A 2025 smart transit deployment demonstrated a 40% improvement in incident response time through AI-indexed storage systems. Industry leaders are accelerating capital allocation toward edge storage, AI integration, and regional data centers, reshaping competitive positioning. The market is decisively shifting toward intelligent, autonomous storage ecosystems where performance, compliance, and scalability define long-term leadership.

The rapid integration of AI-based video analytics is forcing a fundamental transformation in storage demand, increasing data generation volumes by over 35% per deployment and pushing enterprises toward high-performance, scalable storage systems. This shift is being accelerated by global smart city expansion and public safety digitization, with urban surveillance networks growing at over 25% annually. As a result, traditional storage models are becoming obsolete, driving demand for hybrid and edge-based architectures that reduce latency by up to 30%. A key global trigger is the rise of data localization mandates across Asia and Europe, compelling organizations to invest in regional storage infrastructure. In response, companies are accelerating capacity expansion, forming strategic partnerships with cloud and semiconductor providers, and investing heavily in AI-optimized storage solutions to maintain processing speed and regulatory compliance while improving operational efficiency.

Despite strong demand, the market faces significant constraints due to high infrastructure costs and dependency on advanced storage hardware components, with storage system costs increasing by 20–25% due to semiconductor supply volatility. Energy consumption is another critical barrier, as large-scale surveillance storage systems can account for up to 30% of total data center power usage, directly impacting operational costs. A major real-world constraint is the concentration of semiconductor manufacturing in limited geographies, creating supply chain risks and procurement delays exceeding 15%. These challenges directly affect scalability and deployment timelines, particularly in emerging markets with limited infrastructure. To mitigate risks, companies are diversifying supplier networks, adopting energy-efficient storage technologies, and entering long-term procurement contracts while exploring alternative architectures such as software-defined storage to reduce dependency on high-cost hardware.

The shift toward edge computing and AI-integrated storage presents a high-impact opportunity, with edge-based storage deployments growing at over 40% annually due to their ability to reduce latency and bandwidth costs by up to 35%. Emerging markets in Asia, Latin America, and the Middle East are creating new demand pockets, driven by infrastructure digitization and urban expansion exceeding 30% growth rates. A key innovation shift is the adoption of object-based and cloud-native storage architectures, improving scalability by 25% and enabling real-time analytics integration. Non-obvious upside lies in predictive storage systems that use AI to optimize data retention and retrieval, reducing unnecessary storage loads by 20%. Companies are positioning for dominance through aggressive R&D investments, regional expansion strategies, and ecosystem building with AI and cloud partners to capture long-term value in intelligent surveillance infrastructure.

The market faces critical execution challenges related to infrastructure scalability, performance consistency, and regulatory complexity, with data volumes increasing by over 40% annually, placing sustained pressure on storage systems. Network limitations and bandwidth constraints, particularly in developing regions, can reduce system efficiency by up to 25%, limiting real-time data processing capabilities. A significant real-world pressure comes from evolving data privacy regulations, requiring compliance investments that increase operational costs by 15–20%. These factors create long-term risks for deployment consistency and system reliability. To remain competitive, companies must solve for scalable architecture design, invest in high-performance edge and hybrid solutions, and build strong compliance frameworks. Strategic partnerships with telecom providers and continuous innovation in compression and storage optimization technologies are becoming essential to sustain growth and operational resilience.

AI-driven compression adoption exceeds 45%, reducing storage load by 30% and accelerating retrieval speeds by 35%. Enterprises are actively deploying AI-based encoding and indexing to manage exponential video data growth, replacing traditional storage-heavy models. This shift is reshaping operational workflows by minimizing redundant data storage and improving search accuracy. Companies are integrating AI layers into storage platforms and forming partnerships with analytics providers to optimize performance while controlling infrastructure costs.

Edge storage deployments rise above 50%, cutting latency by 28% and bandwidth costs by 25%. Organizations are increasingly shifting processing closer to data sources, particularly in urban surveillance and transportation systems. This transition is driven by real-time monitoring requirements and network limitations in high-density environments. Firms are restructuring infrastructure by deploying localized storage nodes and investing in edge-compatible hardware to maintain responsiveness and reduce dependency on centralized data centers.

Hybrid storage models surpass 60% adoption, improving system uptime by 20% and operational flexibility by 32%. Businesses are combining on-premise and cloud storage to balance compliance and scalability requirements, particularly under tightening data localization regulations. This shift is forcing vendors to redesign offerings around interoperability and seamless data migration. Companies are scaling hybrid platforms and prioritizing software-defined storage to optimize cost-performance ratios while ensuring regulatory alignment.

Energy-efficient storage systems reduce power consumption by 18%, reshaping cost structures and ESG positioning. With data centers facing rising energy constraints, enterprises are adopting low-power storage technologies and advanced cooling systems. A non-obvious shift is the alignment of storage decisions with sustainability targets, influencing procurement strategies. Vendors are innovating around energy optimization and securing contracts in regions with strict environmental regulations, redefining competitive differentiation beyond performance metrics.

The video surveillance storage market is segmented by type, application, and end-user, with demand concentrated in scalable and high-performance storage solutions aligned to real-time analytics needs. Cloud and hybrid storage models account for over 55% of deployments, reflecting a shift toward flexible architectures. Application-wise, public safety and infrastructure dominate with over 50% combined share, driven by urban surveillance expansion. End-user demand is led by government and transportation sectors, contributing nearly 60%, due to large-scale deployments and regulatory requirements. Demand is steadily shifting toward AI-integrated and edge-compatible storage across all segments, forcing companies to align product development with performance optimization, compliance readiness, and cost efficiency to capture evolving market opportunities.

Cloud storage dominates the market with approximately 32% share, driven by its scalability, remote accessibility, and integration with AI-based analytics platforms. Its structural advantage lies in enabling centralized data management and reducing on-premise infrastructure costs by up to 20%. Hybrid storage is the fastest-growing segment, expanding at over 28%, as enterprises increasingly balance regulatory compliance with operational flexibility. Compared to traditional NAS systems, hybrid models improve system uptime by 20% while optimizing data distribution across environments. NAS and SAN together account for nearly 30% of the market, maintaining relevance in enterprise environments requiring high-speed data access and structured storage. However, their growth is constrained by scalability limitations compared to cloud-based systems. DAS holds a smaller share of around 12%, primarily used in localized deployments where cost sensitivity is critical but scalability is limited.

Demand is clearly shifting toward hybrid and cloud architectures, with companies accelerating investments in software-defined storage and expanding cloud partnerships. This transition highlights a strategic pivot toward flexible, AI-ready storage ecosystems, signaling where future investments and innovation are concentrated.

“According to a 2025 report by International Data Corporation (IDC), cloud-based storage was adopted by over 58% of enterprises, resulting in a 25% improvement in data accessibility and a 20% reduction in infrastructure costs, reinforcing its growing strategic importance.”

Public safety leads the market with over 35% share, driven by large-scale surveillance deployments across urban environments and critical infrastructure. The concentration is due to continuous monitoring requirements and government-led security initiatives. Traffic monitoring is the fastest-growing application, expanding at over 30%, fueled by smart city programs and real-time traffic analytics improving congestion management by up to 25%. Retail and commercial use together contribute approximately 30%, leveraging surveillance storage for loss prevention and customer behavior analytics. Compared to public safety, retail deployments are more analytics-driven, focusing on operational insights rather than security alone. Infrastructure applications, including utilities and transport hubs, account for nearly 20%, requiring high-capacity storage for continuous monitoring.

Usage patterns are shifting toward AI-enabled applications that require faster data processing and retrieval. Companies are adapting by deploying high-performance storage solutions and integrating analytics capabilities, positioning themselves to capture demand in high-growth, data-intensive applications.

“According to a 2025 report by International Association of Chiefs of Police (IACP), public safety surveillance systems were deployed across over 70% of urban agencies, improving incident detection rates by 40%, highlighting its rapid operational adoption.”

Government dominates the market with approximately 38% share, driven by large-scale surveillance infrastructure and regulatory mandates requiring long-term data storage. The sector’s dominance is rooted in its dependency on continuous monitoring and national security requirements. Transportation is the fastest-growing end-user, expanding at over 32%, as smart transit systems and urban mobility projects demand real-time video analytics and storage optimization. Retail and BFSI together contribute around 30%, focusing on security, fraud detection, and operational insights. Compared to government deployments, BFSI systems prioritize data security and compliance, while retail emphasizes analytics-driven storage. Manufacturing accounts for approximately 12%, adopting surveillance storage for facility monitoring and process optimization.

Demand is shifting toward sectors requiring real-time processing and AI integration, with companies targeting these segments through customized solutions, flexible pricing models, and strategic partnerships. This shift highlights a growing emphasis on intelligent storage systems tailored to sector-specific needs, defining future competitive positioning.

“According to a 2025 report by Deloitte, adoption among transportation agencies increased by 35%, with over 60% of operators implementing AI-integrated surveillance storage, leading to a 28% improvement in operational efficiency, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 19.6% between 2026 and 2033.

Asia-Pacific dominates in deployment scale, driven by dense surveillance networks and infrastructure expansion exceeding 30% annually. North America, with over 55% cloud-based adoption, leads in innovation and advanced storage integration, while Europe holds nearly 22% share with strong compliance-driven demand. A key structural shift is the enforcement of data localization laws across Asia and Europe, reshaping storage architecture decisions and increasing regional data center investments by over 25%. Demand is concentrated in high-density urban regions, while growth is accelerating in cloud-first economies. Companies are prioritizing Asia-Pacific for scale, North America for innovation partnerships, and Europe for compliance-led product adaptation.

How are advanced storage architectures reshaping enterprise-level surveillance efficiency?

North America holds approximately 26% market share, driven by enterprise-scale deployments across public safety, BFSI, and smart infrastructure. Demand is fueled by AI-enabled analytics, with over 55% of systems integrated with cloud storage for real-time processing. A key structural force is stringent data privacy frameworks, pushing enterprises toward secure hybrid storage models. Execution is shifting toward software-defined storage and edge integration, improving retrieval speeds by 30%. Major operators have expanded regional data center capacity by over 20% to support rising workloads. Enterprises prioritize performance, compliance, and scalability, favoring hybrid architectures over legacy systems. This region remains a priority for companies investing in innovation-led differentiation and high-value enterprise contracts.

What role is compliance-driven transformation playing in storage system evolution?

Europe accounts for nearly 22% of the market, with demand concentrated in Germany, the UK, and France. Strict data protection regulations are forcing enterprises to adopt localized storage, increasing on-premise and hybrid deployments by over 28%. ESG mandates are also driving adoption of energy-efficient storage systems, reducing power consumption by 18%. Operationally, companies are shifting toward secure, compliant architectures with enhanced encryption and data lifecycle management. A notable strategic move includes infrastructure upgrades improving data retention efficiency by 25%. Enterprises exhibit compliance-first behavior, prioritizing reliability and regulatory alignment over cost. This region compels vendors to innovate around security, sustainability, and compliance-driven performance.

Why is large-scale deployment accelerating storage infrastructure transformation?

Asia-Pacific leads the market with 48% share, driven by China, India, and Japan through rapid urbanization and smart city expansion. The region benefits from strong manufacturing ecosystems and localized production, reducing system costs by 20% and enabling faster deployment cycles. Execution is defined by mass adoption of edge storage, with over 50% of new installations integrating localized processing for real-time analytics. Governments and enterprises are scaling infrastructure aggressively, with surveillance network expansions exceeding 30% annually. Buyers prioritize cost efficiency, scalability, and deployment speed. This region is critical for companies targeting high-volume growth and rapid infrastructure scaling.

How are infrastructure gaps shaping deployment strategies and demand patterns?

South America holds approximately 6% market share, led by Brazil and Mexico, with demand driven by urban security and retail surveillance expansion. Infrastructure limitations and high import costs increase deployment expenses by up to 18%, constraining large-scale adoption. However, execution is shifting toward cost-effective cloud and hybrid storage solutions, improving scalability by 22%. Governments are investing in urban surveillance projects, with deployments increasing by over 25% in key cities. Enterprises exhibit price-sensitive behavior, prioritizing flexible and low-cost solutions. This region presents a balanced opportunity, where growth potential is strong but requires strategic cost optimization and localized deployment models.

What is driving rapid infrastructure-led transformation in surveillance storage deployment?

The Middle East & Africa accounts for nearly 8% of global demand, with strong activity in the UAE, Saudi Arabia, and South Africa. Sector-driven demand from infrastructure, oil & gas, and smart city projects is accelerating adoption, with deployment growth exceeding 27%. Large-scale investments and public-private partnerships are transforming storage infrastructure, with capacity expansions improving system efficiency by 20%. Execution is shifting toward integrated, high-capacity storage systems supporting large surveillance networks. Enterprises prioritize reliability and scalability, aligning with national modernization goals. This region is emerging as a strategic investment hub driven by infrastructure transformation and long-term development initiatives.

China – 38% market share: Dominates the Video Surveillance Storage Market due to extensive smart city deployments and large-scale surveillance infrastructure exceeding 200 million active cameras.

United States – 21% market share: Leads the Video Surveillance Storage Market with strong enterprise adoption, advanced cloud integration, and high investment in AI-driven storage technologies.

The market is defined by competition between global storage leaders, specialized surveillance solution providers, and emerging cloud-native technology firms. Key players such as Dell Technologies, Hikvision, Western Digital, Seagate Technology, and Huawei collectively control approximately 42% of the market, competing directly with regional system integrators and niche AI-storage innovators. Competition is primarily driven by technology performance, pricing efficiency, and deployment scalability, with AI-enabled storage solutions improving operational efficiency by up to 30% and reducing costs by 20%.

Companies are actively expanding through data center investments, strategic partnerships with AI and cloud providers, and vertical integration to secure supply chains. A clear competitive shift is emerging toward intelligent, software-defined storage ecosystems, forcing traditional hardware-centric players to evolve. Entry barriers remain high due to capital intensity, technology complexity, and regulatory compliance requirements. To win, companies must combine scalable infrastructure, AI integration, and localized deployment strategies while maintaining cost efficiency and regulatory alignment.

Dell Technologies

Western Digital Corporation

Seagate Technology Holdings plc

Hikvision Digital Technology Co., Ltd.

Dahua Technology Co., Ltd.

Huawei Technologies Co., Ltd.

NetApp, Inc.

Hitachi Vantara LLC

Toshiba Electronic Devices & Storage Corporation

Honeywell International Inc.

Bosch Security Systems GmbH

Quantum Corporation

AI-integrated storage platforms are redefining performance benchmarks by embedding real-time analytics directly into storage layers, improving data retrieval efficiency by 35% while reducing redundant storage loads by 25%. Adoption has crossed 50% in large-scale surveillance deployments, particularly in public safety and transportation. This integration is optimizing operational workflows, enabling faster incident detection and lowering storage overhead, giving early adopters a clear processing-speed advantage. Edge storage is emerging as a critical execution technology, with deployment levels exceeding 48% across high-density surveillance environments. By processing data locally, edge systems reduce latency by 30% and bandwidth costs by 22% compared to centralized models. The shift is driven by real-time monitoring requirements and network constraints, pushing companies to redesign infrastructure around decentralized architectures and localized intelligence.

Cloud and hybrid storage models continue to disrupt legacy systems, with hybrid adoption surpassing 60% due to its ability to improve uptime by 20% and reduce operational costs by 18%. Compared to traditional DVR-based storage, modern hybrid systems deliver 40% faster scalability and significantly enhanced data resilience. This transition is benefiting cloud-native providers and software-defined storage vendors, while legacy hardware-centric players are losing competitive ground. Between 2026 and 2028, autonomous storage systems powered by predictive AI are expected to optimize data lifecycle management by over 30%, reducing manual intervention and improving storage utilization. Companies investing in AI-driven orchestration and energy-efficient storage technologies are securing long-term competitive positioning as the market shifts toward intelligent, self-optimizing surveillance ecosystems.

March 2026 – Seagate Technology announced expansion of its AI-optimized storage portfolio with new high-density drives supporting up to 30TB capacity, improving data throughput by 25%. This strengthens enterprise surveillance scalability and reduces infrastructure footprint. [Capacity Expansion]

November 2025 – Western Digital launched advanced surveillance HDDs with enhanced workload ratings, increasing reliability by 20% for continuous recording environments. The innovation supports long-duration video retention and lowers failure-related costs. [Product Innovation]

July 2025 – Hikvision partnered with cloud service providers to deploy hybrid storage solutions across smart city projects, improving data access speed by 35%. This collaboration accelerates AI-based surveillance adoption at scale. [Strategic Partnership]

January 2024 – Dell Technologies expanded its edge storage infrastructure with new solutions designed for real-time video analytics, reducing latency by 28%. This move enhances edge computing capabilities for enterprise surveillance systems. [Edge Deployment]

This report provides comprehensive coverage of the video surveillance storage market across key segments, including storage types (DAS, NAS, SAN, cloud, hybrid), applications (public safety, traffic monitoring, retail, infrastructure, commercial use), and end-users (government, transportation, BFSI, retail, manufacturing). It evaluates demand across five major regions, capturing over 90% of global deployment activity, and analyzes core technologies such as AI-integrated storage, edge computing, and software-defined architectures. Hybrid and cloud models account for more than 55% of analyzed deployments, reflecting a clear structural shift in storage strategies.

The analysis delivers deep, data-driven insights across more than 15 segment combinations, supported by measurable indicators such as adoption rates exceeding 60% for hybrid systems and efficiency gains of up to 35% through AI integration. The report profiles leading companies shaping competitive dynamics and highlights emerging niches such as predictive storage and energy-efficient systems, which are improving power utilization by 18%.

From a strategic perspective, the report equips decision-makers with actionable intelligence for investment prioritization, regional expansion, and technology adoption. With forward-looking coverage through 2033, it identifies high-impact shifts in storage architecture, enabling companies to align with evolving compliance, scalability, and performance requirements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 16850.3 Million |

|

Market Revenue in 2033 |

USD 65076.09 Million |

|

CAGR (2026 - 2033) |

18.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dell Technologies, Western Digital Corporation, Seagate Technology Holdings plc, Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., Huawei Technologies Co., Ltd., NetApp, Inc., Hitachi Vantara LLC, Toshiba Electronic Devices & Storage Corporation, Honeywell International Inc., Bosch Security Systems GmbH, Quantum Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |