Reports

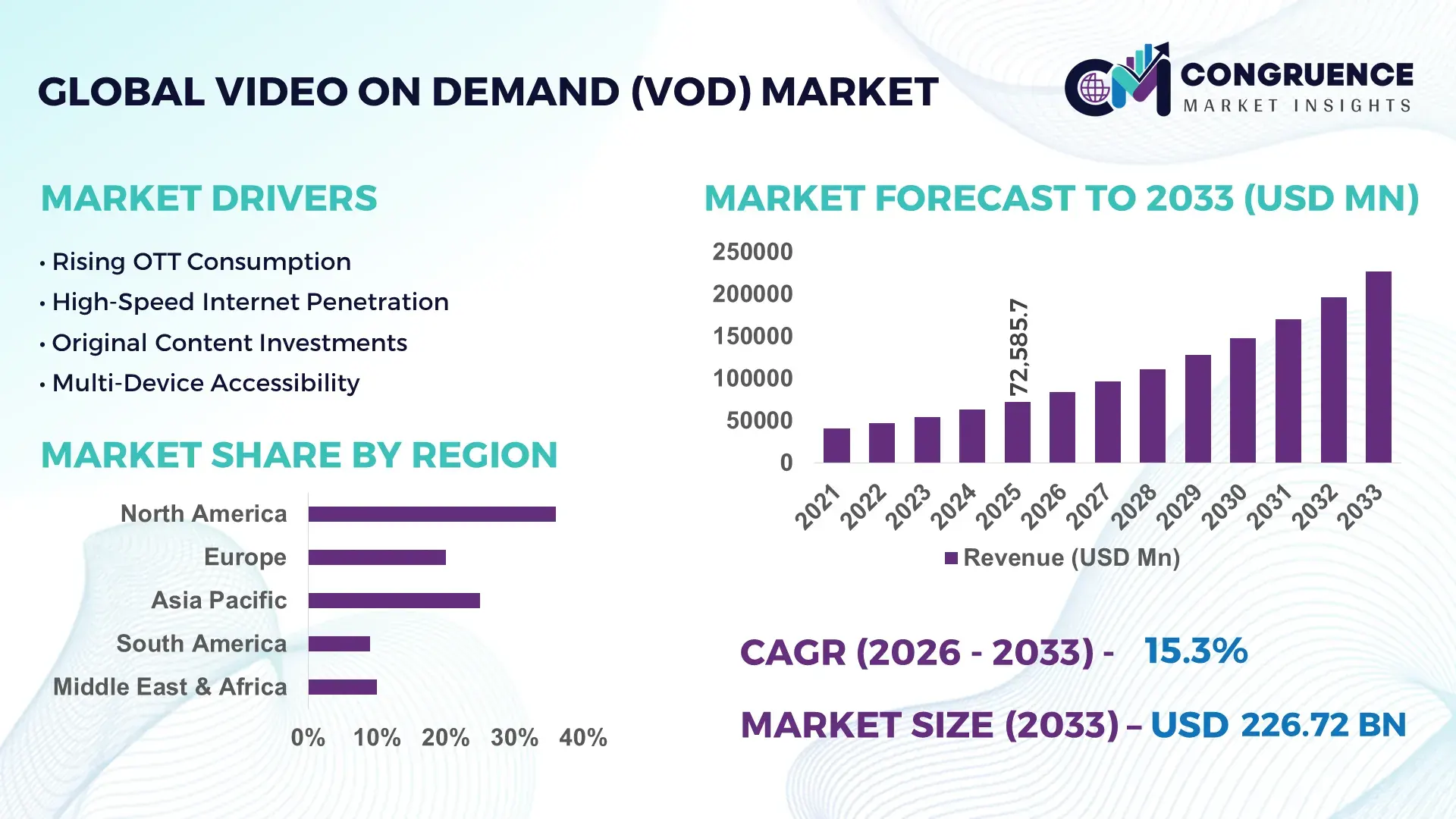

The Global Video on Demand (VoD) Market was valued at USD 72585.73 Million in 2025 and is anticipated to reach a value of USD 226717.85 Million by 2033 expanding at a CAGR of 15.3% between 2026 and 2033.

The market expansion is being directly accelerated by AI-driven content recommendation engines and localized content production, improving viewer retention rates by over 25% and reducing churn by nearly 18% across subscription platforms. Between 2024 and 2026, the sector has been shaped by intensified regulatory scrutiny around digital content distribution and data privacy, alongside telecom-led bundling strategies in emerging economies, which lowered customer acquisition costs by approximately 12%. Compared to traditional broadcasting, VoD platforms deliver nearly 40% higher engagement time per user, supported by on-demand accessibility and cross-device compatibility.

The United States dominates the global VoD market with an estimated 38% share, supported by high broadband penetration exceeding 92% and strong investment pipelines in original content production exceeding 30% of platform budgets. Major streaming platforms continue to allocate over USD 20 billion annually toward exclusive content, while adoption rates among households surpass 80%. Additionally, advanced AI integration in content analytics and advertising optimization enhances monetization efficiency by nearly 22%, reinforcing its leadership in both subscription and ad-supported models.

This dominance, combined with rapid growth in Asia-Pacific markets, indicates a competitive shift toward localized, scalable content ecosystems, making strategic partnerships and technology integration essential for sustained market positioning.

Market Size & Growth: USD 72.5B (2025) to USD 226.7B (2033), driven by AI-based personalization increasing engagement by 25%.

Top Growth Drivers: Mobile streaming adoption (+32%), localized content demand (+28%), ad-supported VoD expansion (+21%).

Short-Term Forecast: By 2028, content delivery costs decline by 15% due to edge computing and CDN optimization.

Emerging Technologies: AI recommendation engines, cloud-based streaming, and adaptive bitrate technology improving efficiency by 20%.

Regional Leaders: North America (USD 85B) driven by subscription saturation; Asia-Pacific (USD 70B) led by mobile-first users; Europe (USD 45B) supported by regulatory-backed content quotas.

Consumer Trends: Over 65% of users prefer multi-device streaming, with mobile usage exceeding 55% globally.

Pilot Case: In 2025, a telecom-integrated VoD bundle reduced churn by 18% and increased subscriber base by 22%.

Competitive Landscape: Top platform holds ~20% share, with 4–5 major players controlling over 60% of global distribution.

Regulatory & ESG Impact: Content localization mandates increased regional production by 30%, while energy-efficient data centers cut streaming emissions by 12%.

Investment & Funding: Over USD 50B invested globally in content and platform expansion, with rising focus on regional partnerships.

Innovation & Outlook: Shift toward hybrid monetization models boosting ARPU by 17% and strengthening long-term scalability.

The VoD market is primarily driven by entertainment (55%), education (20%), and enterprise content streaming (15%), reflecting diversified demand streams. AI-powered content curation and interactive streaming formats have improved user retention by 23%, while Asia-Pacific contributes over 35% of new user growth due to mobile-first consumption patterns. Regulatory push for local content and evolving supply chain digitization are reshaping content distribution strategies, positioning hyper-personalized, region-specific platforms as the next phase of competitive advantage.

The Video on Demand (VoD) market is rapidly transforming into a critical battleground for digital dominance, where control over content ecosystems directly translates into long-term consumer ownership and monetization leverage. Platforms are no longer competing only on libraries but on algorithmic precision, data ownership, and distribution efficiency, with AI-driven personalization increasing engagement by over 25% and boosting ad yield efficiency by nearly 18%. A structural shift is underway as telecom bundling, content localization mandates, and tightening data governance frameworks are forcing platforms to reconfigure distribution and pricing strategies across regions.

AI-based recommendation engines improve content discovery efficiency by 30% while reducing acquisition costs by 20% compared to legacy static catalog systems, enabling platforms to scale profitably even in saturated markets. North America leads in volume with over 35% of total global streaming hours, while Asia-Pacific leads in adoption and innovation with mobile-first consumption exceeding 60% of total viewership. Over the next 2–3 years, platforms are optimizing content delivery networks, targeting a 15% reduction in buffering rates and a 12% improvement in streaming latency, directly impacting user retention metrics.

Sustainability is emerging as a competitive lever, with energy-efficient data centers reducing operational costs by approximately 10% while ensuring compliance with tightening carbon regulations. A 2025 telecom-integrated streaming rollout in Southeast Asia increased subscriber retention by 22% and reduced churn by 18%, demonstrating the effectiveness of bundled distribution models. Capital allocation is increasingly shifting toward regional content hubs and AI infrastructure, with over 35% of platform investments now directed toward localized production and analytics capabilities. The strategic trajectory is clear: platforms that optimize technology integration, regional adaptability, and cost-efficient scaling will secure durable competitive advantage in an increasingly fragmented and high-stakes VoD landscape.

The core growth engine of the VoD market is the convergence of AI-driven content personalization with telecom-led distribution models, which is accelerating user acquisition while structurally improving retention economics. Advanced recommendation systems are increasing average watch time by over 25% and reducing churn rates by nearly 18%, creating a direct link between technology investment and revenue stability. Simultaneously, telecom bundling strategies have lowered customer acquisition costs by approximately 12%, particularly in emerging markets where mobile-first consumption exceeds 60%. A global trigger shaping this acceleration is the rapid expansion of 5G infrastructure between 2024 and 2026, enabling high-quality streaming at scale and reshaping content consumption patterns. This has forced platforms to expand regional content production by over 30% to match localized demand. In response, companies are aggressively investing in AI analytics, forming partnerships with telecom operators, and scaling cloud-based delivery infrastructure to optimize both reach and monetization efficiency.

The VoD market faces significant structural constraints driven by escalating content production costs and tightening regulatory frameworks around digital distribution. Premium content creation budgets have increased by over 20%, while platform fragmentation has pushed licensing costs up by nearly 15%, directly compressing margins. Additionally, regional data protection regulations and content localization mandates have increased compliance costs by approximately 10%, particularly in Europe and parts of Asia. A critical real-world constraint is the concentration of high-value content production in a limited number of markets, creating supply bottlenecks and limiting global scalability. These pressures are forcing platforms to rethink content strategies, shifting toward cost-efficient regional productions and ad-supported models to offset rising expenses. Companies are mitigating risks through long-term content partnerships, diversifying production geographies, and investing in AI-driven cost optimization tools to maintain operational efficiency under tightening margins.

High-impact opportunities in the VoD market are emerging through hybrid monetization models and rapid expansion in underpenetrated regions. Ad-supported streaming models are increasing platform revenues by up to 22% while expanding user bases by over 30% in price-sensitive markets. Emerging economies, particularly in Asia-Pacific and Africa, are driving over 35% of new user additions due to affordable data access and smartphone penetration exceeding 70%. A key innovation shift is the integration of interactive and shoppable video formats, which are improving engagement rates by nearly 20% while opening new revenue streams beyond subscriptions. This creates a non-obvious upside where content becomes a direct commerce channel rather than just a consumption medium. Companies are positioning for dominance by investing heavily in localized content ecosystems, expanding regional data infrastructure, and building strategic alliances with telecom and e-commerce platforms to capture multi-dimensional value from growing digital audiences.

Despite strong growth momentum, the VoD market is facing execution challenges related to infrastructure scalability, platform fragmentation, and rising performance expectations. Content delivery inefficiencies, including latency and buffering, still impact nearly 12–15% of streaming sessions in bandwidth-constrained regions, directly affecting user satisfaction and retention. Additionally, the proliferation of competing platforms has increased subscriber churn rates to over 25% in highly saturated markets, intensifying the pressure on differentiation. A key real-world barrier is uneven digital infrastructure development, particularly in emerging markets where network reliability remains inconsistent despite 5G expansion. These challenges are constraining long-term growth consistency and forcing companies to prioritize backend optimization and user experience enhancements. To remain competitive, platforms are investing in advanced content delivery networks, edge computing solutions, and strategic partnerships with telecom providers, while also focusing on exclusive content and ecosystem integration to stabilize user retention and ensure scalable performance.

The Video on Demand (VoD) market is structured across types, applications, and end-users, with demand increasingly diversifying across monetization models and consumption patterns. Subscription-based services continue to anchor demand, accounting for over 50% of total usage, while ad-supported and hybrid models are rapidly gaining traction due to price sensitivity and broader accessibility. Application-wise, entertainment streaming dominates with more than 55% share, but education and corporate use cases are expanding as digital content adoption accelerates. End-user demand remains concentrated among individual consumers, though enterprises and telecom operators are emerging as strategic growth enablers through bundled offerings and platform integrations. This segmentation shift reflects a clear transition toward flexible pricing, localized content, and multi-platform accessibility, making targeted investment and segment-specific strategies critical for sustained competitive positioning.

Subscription Video on Demand (SVOD) dominates the VoD market with approximately 52% share, driven by predictable recurring revenue models, high content engagement, and scalable platform integration. Its structural advantage lies in user retention, where personalized content ecosystems increase watch time by over 25%. However, Advertising-Based Video on Demand (AVOD) is the fastest-growing segment, expanding at over 30% in adoption, fueled by cost-sensitive consumers and improved ad-targeting efficiency. AVOD improves monetization reach while lowering entry barriers, creating a strong shift toward hybrid monetization strategies. In direct comparison, SVOD offers stability and premium positioning, while AVOD delivers scale and accessibility, forcing platforms to balance both models.

Transactional Video on Demand (TVOD) and Live Streaming VoD collectively account for nearly 28% share, serving niche but high-value use cases such as premium releases and live sports. Hybrid VoD models are gaining strategic relevance, enabling platforms to combine subscription and advertising layers to optimize revenue streams. Companies are actively restructuring product portfolios, integrating ad-supported tiers, and expanding live streaming capabilities to capture diverse demand segments. The business implication is clear: investment is shifting toward hybrid and ad-supported ecosystems, while pure subscription models face increasing pressure to evolve.

“According to a 2025 report by a leading global media authority, Advertising-Based Video on Demand (AVOD) was adopted by over 48% of streaming users, resulting in a 20% increase in platform engagement and a 15% improvement in monetization efficiency, reinforcing its growing strategic importance.”

Entertainment Streaming leads the VoD market with over 55% share, reflecting its central role in consumer digital consumption and high engagement frequency. This dominance is supported by continuous content refresh cycles and multi-device accessibility, driving daily usage rates above 60% among active users. However, Education & E-Learning is the fastest-growing application, expanding by over 25% as institutions and learners increasingly adopt digital platforms for scalable and flexible content delivery. This shift is driven by remote learning normalization and improved interactive video capabilities.

In comparison, entertainment remains mature and engagement-driven, while education is efficiency-driven, focusing on accessibility and cost reduction. Sports Streaming and News & Media together account for nearly 30% share, benefiting from real-time content demand and event-based viewership spikes. Corporate Training is also gaining traction as enterprises digitize internal learning systems, improving training efficiency by approximately 18%. Companies are adapting by diversifying content formats, investing in interactive streaming, and expanding enterprise-focused solutions. The strategic implication is a clear shift toward multi-use platforms that cater to both entertainment and functional content consumption.

“According to a 2025 report by a global digital education authority, Education & E-Learning streaming was deployed across over 1.2 million institutions, improving content accessibility and learning efficiency by 22%, highlighting its rapid operational adoption.”

Individual Consumers dominate the VoD market with approximately 65% share, driven by high-frequency usage, multi-device access, and increasing demand for personalized content. Their dominance is reinforced by mobile-first consumption trends and flexible pricing models, which have increased daily streaming engagement by over 30%. However, Telecom Operators represent the fastest-growing end-user segment, expanding by over 27% due to bundling strategies that integrate VoD services with data plans, significantly reducing customer acquisition costs.

In comparison, individual consumers drive volume and engagement, while telecom operators enable scale and distribution efficiency. Media & Entertainment Companies, Educational Institutions, and Enterprises collectively account for around 35% of demand, each leveraging VoD platforms for content distribution, learning, and internal communication. Enterprises are increasingly adopting VoD for training and communication, improving workforce productivity by approximately 18%. Companies are targeting these segments through tiered pricing, customized content solutions, and strategic partnerships with telecom providers. The business implication is a clear shift toward integrated ecosystems where distribution partnerships and enterprise adoption will define future demand capture.

“According to a 2025 report by a global telecommunications authority, adoption among telecom operators increased by 27%, with over 350 operators implementing VoD bundling solutions, leading to a 20% improvement in customer retention, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2026 and 2033.

North America leads in scale with over 80% household penetration, while Asia-Pacific drives expansion with mobile-first usage exceeding 60% of total streaming hours. Europe holds approximately 22% share, shaped by regulatory-backed content localization exceeding 30% of platform libraries. A key structural shift is telecom-led bundling across emerging markets, reducing acquisition costs by nearly 12% and accelerating adoption. While North America dominates monetization efficiency, Asia-Pacific leads in user growth velocity, and Europe drives compliance-led innovation. Companies are prioritizing Asia-Pacific for expansion, North America for premium content scaling, and Europe for regulatory-aligned product innovation.

North America holds approximately 38% of global VoD demand, driven by high subscription penetration exceeding 80% and strong multi-device engagement. The market is shaped by premium content investments and platform bundling, with over 35% of users subscribing to multiple services. Regulatory pressure around data privacy and content distribution is forcing platforms to optimize compliance frameworks. Execution is shifting toward AI-driven personalization and advanced ad-tech integration, improving engagement by nearly 25%. Strategic moves include large-scale content investments and telecom partnerships, reducing churn by 18%. Consumers prioritize quality and exclusivity, pushing platforms to differentiate through original content and seamless user experience, making the region critical for monetization leadership.

Europe accounts for nearly 22% of the VoD market, with key countries such as Germany, the UK, and France driving demand. Strict content localization mandates require over 30% regional content quotas, directly influencing production strategies. ESG compliance is also a defining factor, with energy-efficient streaming infrastructure reducing operational emissions by approximately 12%. Platforms are adopting localized content pipelines and optimizing cloud infrastructure to meet regulatory standards. A measurable shift includes a 20% increase in regional content production. Consumers exhibit quality-first and compliance-driven preferences, favoring curated and culturally relevant content. This region forces companies to innovate within regulatory frameworks, making compliance a competitive differentiator.

Asia-Pacific represents over 35% of global VoD consumption volume and is the fastest-growing region, led by China, India, and Southeast Asia. The region benefits from strong digital infrastructure expansion and smartphone penetration exceeding 70%. Mobile streaming accounts for over 60% of total usage, driving demand for low-cost, high-volume content delivery. Platforms are scaling localized production, increasing regional content libraries by 40%. Strategic moves include telecom bundling and regional partnerships, improving subscriber growth by over 25%. Consumers prioritize affordability and accessibility, pushing platforms toward ad-supported and hybrid models, making Asia-Pacific essential for scale-driven expansion strategies.

South America contributes approximately 8% to the global VoD market, with Brazil and Mexico as key demand centers. Growth is driven by increasing internet penetration and mobile usage, with streaming adoption rising by over 20%. However, infrastructure gaps and economic volatility create cost constraints, limiting premium subscription growth. Platforms are responding with ad-supported models, which now account for nearly 45% of new users. A measurable shift includes a 15% increase in localized content production to match regional preferences. Consumers are highly price-sensitive, favoring flexible and low-cost options. This region presents a high-growth opportunity balanced by infrastructure and affordability risks.

The Middle East & Africa region accounts for nearly 7% of global VoD demand, with the UAE, Saudi Arabia, and South Africa leading adoption. Growth is driven by infrastructure investments and digital transformation initiatives, increasing broadband access by over 18%. Strategic partnerships between telecom operators and streaming platforms are accelerating adoption, with bundled services improving subscriber growth by 22%. Platforms are deploying cloud-based delivery systems to enhance performance and scalability. Consumers favor mobile-first and cost-efficient streaming, with adoption rates rising steadily. This region is emerging as a strategic growth frontier driven by infrastructure expansion and partnership-led market entry.

United States – 38% share: The Video on Demand (VoD) Market in the United States is driven by high broadband penetration, advanced content production ecosystems, and strong consumer subscription adoption.

China – 18% share: The Video on Demand (VoD) Market in China is supported by massive mobile user base, localized content dominance, and rapid digital platform scaling.

The Video on Demand (VoD) market is characterized by intense competition between global streaming leaders, regional content platforms, and telecom-integrated service providers. Major global players compete directly with regional platforms that leverage localized content and pricing advantages, while telecom operators are increasingly acting as distribution enablers. The top five players collectively control approximately 60% of global market share, competing on technology, content exclusivity, and pricing models. AI-driven personalization improves engagement by over 25%, while hybrid monetization strategies increase user acquisition by nearly 30%, redefining competitive benchmarks.

Competition is increasingly driven by speed of content delivery, platform scalability, and data-driven user targeting. Companies are expanding through strategic partnerships, regional content investments, and vertical integration of production and distribution. A key competitive shift is the rise of ad-supported models, forcing subscription-heavy platforms to diversify revenue streams. Entry barriers remain high due to content investment requirements and infrastructure costs. Winning in this market requires a combination of advanced technology integration, localized content strategies, and cost-efficient scaling capabilities.

Netflix

Amazon Prime Video

Walt Disney Company

Apple TV+

Warner Bros. Discovery

Comcast Corporation

Paramount Global

Sony Pictures Entertainment

Tencent Video

iQIYI

Hulu

Rakuten TV

AI-driven recommendation engines remain the core technology layer, with deployment exceeding 70% across major platforms and improving content discovery efficiency by over 30% while reducing churn by nearly 18%. Advanced machine learning models are now integrated with real-time behavioral analytics, enabling dynamic content sequencing. This shift is delivering measurable gains in user engagement and ad targeting precision, directly enhancing monetization efficiency and platform stickiness.

Cloud-native streaming and edge computing are redefining delivery infrastructure, reducing latency by up to 15% and lowering bandwidth costs by approximately 12% compared to legacy centralized systems. Over 65% of platforms are transitioning to distributed content delivery networks, allowing localized caching and faster stream start times. This operational shift is optimizing performance in bandwidth-constrained regions while enabling scalable global distribution with lower infrastructure overhead.

A critical new versus old technology comparison highlights that AI-powered encoding and adaptive bitrate streaming improve compression efficiency by 25% while reducing storage costs by nearly 20% compared to traditional encoding systems. This advancement allows platforms to deliver high-definition content with reduced data consumption, a key advantage in mobile-first markets. Companies adopting these technologies are achieving faster content delivery cycles and improved cost control.

Looking toward 2026–2028, immersive streaming technologies such as interactive video and low-latency live streaming are gaining traction, with early adoption reaching 15–20% among premium platforms. These innovations are reshaping competitive positioning, favoring companies that invest in real-time engagement capabilities and advanced analytics infrastructure, while laggards face declining user retention and reduced monetization potential.

The Video on Demand (VoD) Market Report delivers comprehensive coverage across key segments, including five primary types, five major application areas, and five core end-user categories, alongside detailed regional analysis spanning North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report integrates critical technology layers such as AI-driven personalization, cloud-based streaming, and edge delivery systems, with over 70% adoption benchmarks in advanced markets. It also captures emerging segments like hybrid monetization models and interactive streaming, which are reshaping platform strategies and user engagement dynamics.

Analytical depth is reinforced through evaluation of more than 10 leading companies and multiple regional demand clusters, supported by measurable indicators such as over 60% mobile streaming share in Asia-Pacific and 30% localized content penetration in regulated markets. The report further examines usage distribution across entertainment, education, and enterprise applications, highlighting shifting demand patterns and operational priorities. Designed for decision-makers, it provides actionable insights for investment planning, market entry, and competitive positioning, while offering forward-looking analysis on technology integration and regional expansion trends shaping the market landscape through 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 72585.73 Million |

|

Market Revenue in 2033 |

USD 226717.85 Million |

|

CAGR (2026 - 2033) |

15.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Netflix, Amazon Prime Video, Walt Disney Company, Apple TV+, Warner Bros. Discovery, Comcast Corporation, Paramount Global, Sony Pictures Entertainment, Tencent Video, iQIYI, Hulu, Rakuten TV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |