Reports

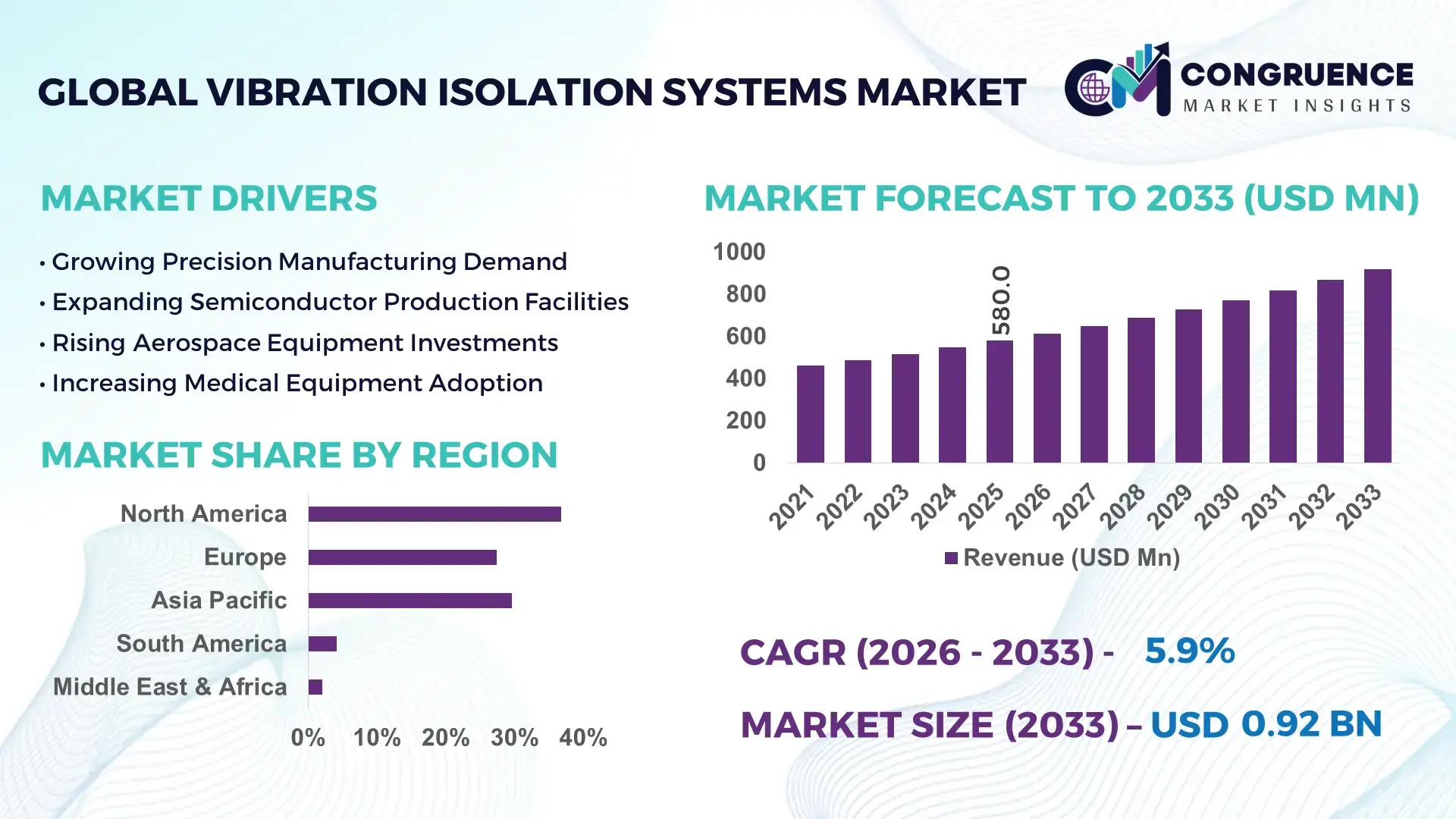

The Global Vibration Isolation Systems Market was valued at USD 580.0 Million in 2025 and is anticipated to reach a value of USD 917.5 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033. Growth is being propelled by rising deployment of precision vibration control solutions across semiconductor fabrication plants, advanced manufacturing facilities, rail infrastructure modernization programs, and high-performance industrial automation environments requiring micron-level stability.

The United States remains the dominant country, accounting for approximately 28% of global demand, supported by over USD 50 billion in semiconductor manufacturing commitments and extensive aerospace and defense production activity. Germany contributes nearly 8% of market consumption through advanced automotive and industrial engineering applications, while U.S. adoption of active vibration isolation platforms exceeds Germany by more than 15 percentage points in high-precision manufacturing environments. Ongoing supply-chain localization initiatives following semiconductor security measures continue accelerating installation rates across critical industrial assets.

Strategically, suppliers with strong exposure to semiconductor, aerospace, and automated manufacturing ecosystems are positioned to capture the highest-value deployment opportunities.

Market Size & Growth: USD 580.0 Million in 2025, reaching USD 917.5 Million by 2033, driven by semiconductor fab expansion, industrial automation upgrades, and precision manufacturing requirements.

Top Growth Drivers: Semiconductor equipment installations (+22%), industrial automation penetration (+18%), and rail infrastructure modernization programs (+14%) are accelerating adoption.

Short-Term Forecast: By 2028, advanced isolation platforms are expected to reduce equipment vibration-related downtime by nearly 25% across precision manufacturing facilities.

Emerging Technologies: AI-enabled monitoring, active vibration control systems, and advanced elastomeric composite materials are improving operational accuracy by over 20%.

Regional Leaders: North America (~USD 250 Million), Asia-Pacific (~USD 190 Million), and Europe (~USD 120 Million) lead through semiconductor, aerospace, and industrial modernization investments.

Consumer/End-User Trends: More than 45% of new semiconductor production lines incorporate advanced vibration isolation technologies during facility commissioning.

Pilot/Case Example: In 2024, multiple semiconductor facilities reported over 30% improvement in equipment stability after deploying active isolation platforms.

Competitive Landscape: Leading suppliers collectively control nearly 35% of the market, with key participants including TMC, Fabreeka, Hutchinson, Vibro/Dynamics, and ACE Controls.

Regulatory & ESG Impact: Energy-efficient isolation systems lower equipment energy losses by up to 12% while supporting stricter industrial performance standards.

Investment & Funding: More than USD 8 billion in semiconductor facility investments globally continue generating demand for high-performance vibration mitigation solutions.

Innovation & Future Outlook: Smart connected isolation platforms, predictive diagnostics, and digital twin integration are reshaping next-generation industrial asset management.

The Vibration Isolation Systems Market is increasingly shaped by demand from semiconductor manufacturing, aerospace assembly, medical imaging equipment, and automated production environments where operational precision directly influences productivity. Recent innovations include sensor-integrated active isolation platforms and adaptive control technologies capable of improving stability performance by more than 20%. Supply-chain diversification initiatives and critical manufacturing localization programs are accelerating installation activity, creating a favorable environment for advanced vibration management solutions and setting the stage for broader strategic industry adoption.

Vibration isolation systems are becoming strategically important because manufacturing competitiveness increasingly depends on precision, uptime, and equipment reliability. Semiconductor fabrication, aerospace component production, and high-speed automated manufacturing require tighter vibration tolerances than conventional industrial environments. Simultaneously, supply-chain restructuring and domestic manufacturing initiatives are encouraging investments in advanced production infrastructure where vibration control directly affects yield quality and operational efficiency.

Technology adoption is shifting from passive isolation products toward intelligent active control systems. Active solutions can deliver up to 30% higher vibration attenuation efficiency than traditional passive systems in precision manufacturing applications while reducing calibration interruptions. The United States and Japan lead deployment in semiconductor and aerospace environments, whereas Germany maintains strong adoption within automotive engineering and industrial machinery sectors. Over the next two to three years, implementation of smart monitoring capabilities is expected to expand significantly as facilities seek predictive maintenance and process optimization benefits.

A practical example is semiconductor fabrication facilities integrating active isolation platforms beneath lithography equipment to maintain sub-micron accuracy standards. Companies are expanding partnerships with automation providers, sensor manufacturers, and industrial software firms to deliver integrated solutions. Organizations that align vibration control investments with digital manufacturing strategies will strengthen operational resilience, improve production consistency, and secure a durable competitive advantage in increasingly precision-driven industrial markets.

The strongest growth catalyst is the rapid expansion of semiconductor manufacturing and advanced industrial automation. More than 45% of newly commissioned semiconductor production lines now incorporate specialized vibration control infrastructure, while automation intensity across precision manufacturing environments has increased by approximately 18% over recent years. Following strategic semiconductor localization initiatives in the United States and Asia, manufacturers are investing heavily in vibration-sensitive production assets. This shift directly improves process accuracy, reduces defect rates, and enhances equipment utilization. In response, suppliers are expanding production capacity, developing active isolation technologies, and forming partnerships with automation integrators. A notable strategic insight is that vibration performance is increasingly becoming a production-yield variable rather than merely an equipment protection requirement, elevating its importance in capital investment decisions.

Market expansion faces constraints from fluctuating raw material costs and the complexity of customized installation requirements. Elastomer materials, engineered composites, and specialized damping components have experienced cost fluctuations exceeding 15% in some procurement cycles. Additionally, installation and calibration expenses can represent 20–30% of total project costs in high-precision facilities. Supply concentration among specialized component manufacturers creates procurement challenges, particularly for projects requiring custom-engineered isolation solutions. These factors directly affect project economics, deployment timelines, and return-on-investment calculations. To mitigate risks, companies are diversifying supplier networks, localizing selected component production, and adopting long-term procurement agreements. A key operational insight is that lifecycle cost optimization is becoming as important as initial equipment performance during purchasing evaluations.

The emergence of intelligent vibration isolation systems creates substantial opportunities beyond traditional equipment protection applications. Integration of IoT sensors, predictive diagnostics, and AI-based control algorithms can improve vibration management efficiency by over 20% while reducing maintenance interventions by nearly 15%. Japan and South Korea are accelerating adoption of smart manufacturing technologies that increasingly require adaptive vibration mitigation capabilities. Digital twin integration and real-time monitoring platforms represent high-value opportunities for suppliers seeking differentiation. Companies are increasing R&D spending, establishing technology partnerships, and expanding software-enabled service portfolios. A particularly attractive opportunity lies in subscription-based monitoring and performance optimization services, transforming vibration isolation from a hardware-focused offering into a recurring-value industrial technology ecosystem.

The principal long-term challenge involves integrating vibration isolation technologies into increasingly complex industrial ecosystems. Modern production facilities often operate interconnected automation architectures where vibration management must interact with robotics, sensors, control software, and predictive maintenance platforms. Studies indicate that integration and commissioning activities can account for nearly 25% of total deployment timelines, while advanced facilities report technical workforce shortages exceeding 12% in specialized engineering roles. As manufacturing systems become more interconnected, maintaining consistent vibration performance across multiple assets becomes increasingly difficult. Companies must invest in workforce development, digital engineering capabilities, and collaborative technology partnerships. A critical strategic insight is that future market leadership will depend not only on isolation performance but also on seamless interoperability within smart manufacturing environments.

Smart Monitoring Integration Accelerates Industrial operators are embedding sensor-enabled vibration isolation platforms into production assets to improve real-time equipment visibility. Adoption of condition-monitoring-enabled systems increased by nearly 24% during the past two years, while unplanned maintenance events declined by approximately 18% in high-precision facilities. Semiconductor manufacturers in the United States are integrating vibration analytics into factory automation workflows, enabling faster fault detection and process stability. In response, suppliers are expanding software capabilities and forming partnerships with industrial automation providers to deliver integrated monitoring ecosystems rather than standalone hardware products.

Active Isolation Deployment Expands Active vibration isolation systems are gaining traction as manufacturers pursue tighter production tolerances. Deployment across semiconductor and advanced electronics facilities increased by roughly 21%, while precision equipment stability improved by more than 30% compared with conventional passive solutions. Technology transitions toward smaller semiconductor nodes and advanced optical inspection systems are accelerating adoption. Companies are scaling production of intelligent isolation platforms and investing in adaptive control technologies that automatically respond to changing operating conditions, improving throughput and reducing calibration downtime.

Localized Manufacturing Strategies Strengthen Supply-chain resilience has become a key operational priority following component shortages and geopolitical manufacturing realignments. More than 35% of industrial equipment suppliers have increased localized sourcing initiatives, while lead times for specialized isolation components have improved by nearly 15% in selected manufacturing hubs. Enterprises are restructuring procurement networks, expanding regional assembly capabilities, and securing long-term supplier agreements. A notable outcome is the growing preference for modular isolation systems that simplify deployment while reducing dependence on single-source component suppliers.

Precision Infrastructure Investments Rise Investments in data centers, semiconductor fabs, and advanced healthcare facilities are reshaping demand patterns for vibration control technologies. Installation activity within precision manufacturing environments increased by approximately 20%, while vibration-sensitive medical imaging deployments expanded by nearly 12%. Stricter performance requirements and workforce productivity objectives are pushing operators toward higher-specification solutions. Manufacturers are responding through product portfolio expansion, engineering collaborations, and customized deployment services designed to address increasingly complex facility requirements.

Passive vibration isolation systems represent the largest segment, accounting for approximately 62% of total market demand due to their cost-effectiveness, reliability, and ease of integration across industrial machinery, manufacturing equipment, HVAC installations, and transportation infrastructure. These systems remain the preferred choice for established industrial environments where vibration levels are predictable and lifecycle maintenance requirements are relatively low. Their scalability and lower installation complexity continue to support widespread deployment across automotive manufacturing plants and industrial processing facilities.Active vibration isolation systems are the fastest-growing segment, supported by rising demand from semiconductor fabrication, medical imaging, aerospace testing, and precision electronics manufacturing. Adoption of active solutions has increased by nearly 21% as operators seek vibration attenuation performance exceeding conventional systems by over 30%. Hybrid isolation platforms are also gaining traction by combining passive damping with active control capabilities, while pneumatic isolation systems maintain strategic relevance in laboratories and cleanroom environments. Suppliers are prioritizing advanced control algorithms, sensor integration, and modular architectures to capture higher-value applications where operational precision directly affects productivity and product quality.

Industrial equipment remains the leading application segment, contributing approximately 38% of market utilization due to extensive deployment across manufacturing plants, processing facilities, and automated production environments. Vibration isolation systems play a critical role in protecting machinery, reducing wear, and improving operational consistency. Manufacturers increasingly view vibration management as a productivity enhancement tool, with facilities reporting up to 20% reductions in vibration-related maintenance interventions following system upgrades. Semiconductor and electronics manufacturing represents the fastest-growing application segment as production tolerances become increasingly stringent. Adoption within precision manufacturing environments has risen by nearly 25%, driven by advanced lithography, inspection systems, and automated assembly processes. Medical equipment applications continue expanding as imaging accuracy requirements intensify, while aerospace and defense applications benefit from increasing investments in testing and calibration infrastructure. Companies are strengthening engineering capabilities, expanding application-specific product portfolios, and developing integrated monitoring solutions to address diverse operational requirements across end-use environments.

Manufacturing companies constitute the largest end-user group, representing approximately 48% of overall demand due to extensive requirements across automotive, electronics, industrial machinery, and precision engineering operations. High equipment utilization rates and growing automation intensity have elevated vibration control from a maintenance consideration to a production optimization priority. Facilities implementing advanced isolation systems have reported productivity improvements ranging between 12% and 18% through reduced equipment disturbances and improved process consistency. The semiconductor and electronics industry is the fastest-growing end-user category, driven by substantial investments in fabrication facilities, advanced packaging operations, and high-precision production environments. Demand from healthcare institutions is also increasing as hospitals and diagnostic centers expand deployment of vibration-sensitive imaging systems. Aerospace and defense organizations remain significant adopters due to stringent testing and performance validation requirements. Suppliers are tailoring solutions through industry-specific engineering, strategic partnerships, and customized service models to strengthen competitive positioning across diverse buyer groups.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America maintains a leading position in the vibration isolation systems market, supported by strong deployment across semiconductor fabrication, aerospace manufacturing, defense testing, and advanced automation facilities. The region contributes approximately 36.8% of global demand, with deployment concentrated in the United States and select Canadian industrial hubs. Increasing investments in semiconductor manufacturing facilities and high-precision production infrastructure are accelerating demand for active vibration isolation platforms. More than 45% of newly commissioned semiconductor production environments in the region incorporate advanced vibration control technologies to maintain process stability. Equipment suppliers are expanding engineering partnerships and localized service capabilities to support increasingly complex industrial installations and digital manufacturing ecosystems.

United States Market Outlook: The United States dominates regional demand due to its concentration of semiconductor fabrication plants, aerospace production facilities, and advanced industrial automation projects. Large-scale investments in domestic chip manufacturing and defense modernization continue strengthening deployment activity. Precision manufacturing facilities increasingly prioritize vibration attenuation as a production-yield variable, with active isolation adoption exceeding 50% in several high-value semiconductor applications. The country's strong engineering ecosystem and technology integration capabilities position it as the primary innovation center for next-generation vibration management solutions.

Europe represents a significant share of the global market, accounting for approximately 27.4% of overall demand. The region benefits from advanced automotive manufacturing, industrial machinery production, rail infrastructure modernization, and precision engineering applications. Germany, France, and the United Kingdom remain key deployment centers due to strong industrial automation intensity and equipment performance requirements. More than 30% of industrial modernization projects across major manufacturing facilities now include vibration mitigation upgrades as part of operational efficiency programs. Companies are integrating smart monitoring technologies and advanced damping systems to enhance equipment reliability, reduce maintenance requirements, and support increasingly automated production environments.

Germany Market Outlook: Germany serves as the region's most strategically important market due to its leadership in automotive engineering, industrial automation, and precision machinery manufacturing. The country hosts a dense concentration of vibration-sensitive production environments where operational accuracy directly impacts product quality. Nearly 40% of advanced manufacturing facilities are implementing predictive maintenance frameworks that incorporate vibration monitoring and control technologies. German manufacturers continue investing in intelligent production systems, creating sustained demand for high-performance isolation solutions integrated with Industry 4.0 infrastructure.

Asia-Pacific accounts for approximately 29.6% of global market activity and represents the fastest-expanding regional opportunity. The region benefits from large-scale electronics manufacturing, semiconductor fabrication expansion, industrial automation deployment, and infrastructure development programs. China, Japan, South Korea, and Taiwan collectively represent the highest concentration of vibration-sensitive manufacturing assets globally. Semiconductor production investments and advanced electronics assembly operations have increased deployment rates by more than 20% in several industrial clusters. Suppliers are expanding regional production capacity and strengthening partnerships with equipment manufacturers to address rising requirements for precision manufacturing and operational reliability.

China Market Outlook: China remains the most influential market within Asia-Pacific due to its extensive manufacturing ecosystem, industrial modernization initiatives, and growing semiconductor production capabilities. The country accounts for a substantial share of regional equipment installations and continues expanding investments in high-precision manufacturing infrastructure. More than 35% of newly upgraded advanced manufacturing facilities incorporate enhanced vibration control systems as part of productivity improvement programs. Strong domestic production capabilities and expanding automation adoption are reinforcing China's position as a major demand center for both passive and active vibration isolation technologies.

South America contributes approximately 4.1% of global market demand, with growth primarily supported by mining operations, industrial processing facilities, energy infrastructure, and manufacturing modernization initiatives. Brazil and Argentina account for the majority of regional deployment activity due to their established industrial bases and infrastructure development priorities. Operational efficiency programs across mining and heavy industrial sectors are increasing adoption of vibration mitigation technologies to reduce equipment wear and improve reliability. Although infrastructure constraints and investment variability continue influencing deployment pace, companies are pursuing targeted modernization projects that strengthen demand for cost-effective vibration control solutions.

Brazil Market Outlook: Brazil represents the largest market in South America owing to its extensive mining, manufacturing, and energy infrastructure sectors. Industrial operators increasingly deploy vibration isolation technologies to extend equipment lifespan and minimize maintenance disruptions in demanding operating environments. Equipment modernization initiatives across mining and processing facilities have contributed to double-digit growth in vibration management investments over recent years. Brazil's industrial diversification efforts and ongoing infrastructure upgrades continue creating opportunities for suppliers focused on durable and scalable vibration control systems.

The Middle East & Africa region accounts for approximately 2.1% of global demand but is becoming increasingly important through industrial diversification, infrastructure modernization, and strategic investment initiatives. Demand is concentrated within energy facilities, transportation infrastructure, healthcare projects, and emerging manufacturing hubs. Large-scale development programs across Gulf countries are accelerating deployment of vibration-sensitive equipment in critical infrastructure projects. Several industrial expansion initiatives have incorporated advanced equipment protection systems to improve operational performance and asset reliability. Suppliers are strengthening regional partnerships and technical support capabilities to capture opportunities associated with ongoing industrial transformation programs.

Saudi Arabia Market Outlook: Saudi Arabia stands as the most strategically significant market in the region due to extensive industrial diversification programs, infrastructure investments, and manufacturing expansion initiatives. The country is increasing deployment of advanced industrial equipment across energy, petrochemical, logistics, and production facilities, creating sustained demand for vibration isolation solutions. Industrial development projects continue integrating precision machinery and automated systems, while investments in smart manufacturing infrastructure support broader adoption of advanced vibration management technologies. Strong capital investment momentum and industrial modernization objectives position Saudi Arabia as a key regional growth center.

The market is characterized by competition between global technology leaders such as TMC, Hutchinson, Fabreeka, Kinetic Systems, Vibro/Dynamics, and ACE Controls, regional engineering specialists, and low-cost industrial vibration solution providers. The top five players collectively account for approximately 42–47% of global market activity, creating a moderately consolidated structure. Competition is centered on vibration attenuation performance, precision engineering, customization capability, and delivery responsiveness rather than price alone. Active vibration isolation platforms deliver up to 30% higher attenuation efficiency than conventional systems, while integrated monitoring solutions reduce maintenance interventions by nearly 15%, creating a clear technology-based differentiation strategy. Global leaders compete through product innovation, semiconductor-industry partnerships, localized manufacturing, and application-specific engineering support. Regional suppliers focus on shorter lead times and cost advantages.

The competitive shift is moving toward intelligent, sensor-enabled isolation systems and vertically integrated solution portfolios. High qualification requirements in semiconductor and aerospace applications create substantial entry barriers. Winning requires proven performance, precision engineering expertise, strong customer integration capabilities, and application-specific innovation.

Hutchinson SA

Fabreeka International, Inc.

Kinetic Systems, Inc.

Vibro/Dynamics Corporation

ACE Controls Inc.

GERB Schwingungsisolierungen GmbH & Co. KG

LORD Corporation

Farrat Ltd.

Isotech, Inc.

Bilz Vibration Technology AG

Trelleborg Industrial Solutions

Karman Rubber Company

Isolation Technology Inc.

The market is transitioning from conventional passive isolation products toward intelligent, adaptive vibration management platforms. Passive elastomer and pneumatic systems continue to dominate industrial applications due to reliability and lower lifecycle costs, but active vibration isolation technologies are gaining traction in semiconductor, aerospace, and medical imaging environments. Active systems provide up to 30% greater vibration attenuation performance compared with traditional passive solutions while improving process stability in vibration-sensitive operations. Adoption rates within advanced semiconductor facilities now exceed 45%, reflecting the growing need for precision manufacturing control.

Emerging technologies include AI-enabled vibration monitoring, MEMS-based sensing platforms, predictive diagnostics, and adaptive control algorithms. These technologies reduce unexpected maintenance events by approximately 15–20% while improving equipment utilization rates. Integration with industrial IoT infrastructure allows continuous monitoring of vibration signatures, enabling real-time operational optimization. Companies deploying smart vibration management platforms gain measurable advantages in equipment reliability, process consistency, and maintenance efficiency. Semiconductor manufacturers, precision engineering firms, and advanced healthcare facilities are leading adoption.

Between 2026 and 2028, competitive differentiation will increasingly depend on intelligent monitoring, digital twin integration, and autonomous vibration control capabilities. Suppliers investing in software-enabled platforms, sensor ecosystems, and predictive analytics will strengthen market positioning. The shift from standalone hardware to integrated performance-management solutions is expected to reshape procurement priorities and create new opportunities for technology-driven providers.

May 2025 – TMC partnered with NABEYA to expand distribution and customer support capabilities in Japan, strengthening access to semiconductor and precision manufacturing customers. The collaboration leverages NABEYA’s 40+ years of vibration-control expertise, accelerating regional market penetration and technical service capabilities. Source: www.techmfg.com

June 2025 – Hutchinson was selected by Deutsche Aircraft for insulation and advanced anti-vibration system development for the D328eco aircraft program. The lightweight system contributes to improved aircraft efficiency and operational performance, reinforcing Hutchinson’s aerospace technology position.

June 2025 – Hodek Vibration Technologies inaugurated its third manufacturing facility in Karnataka, India, adding Industry 4.0-ready production infrastructure. The expansion supports the company’s plan to scale business activity by more than 3x while diversifying vibration-control products for emerging mobility applications.

September 2025 – TDK subsidiary Tronics Microsystems entered the machine and asset health monitoring segment with new vibration sensor solutions. Leveraging over 20 years of MEMS expertise, the initiative strengthens predictive maintenance capabilities and expands digital monitoring opportunities across industrial sectors.

This report provides comprehensive analysis of vibration isolation technologies across passive systems, active systems, hybrid systems, and pneumatic isolation solutions. It evaluates demand patterns across industrial equipment, semiconductor manufacturing, aerospace and defense, healthcare equipment, and precision engineering applications. The study covers major end-user groups including manufacturing, semiconductor and electronics, healthcare, aerospace, and industrial infrastructure sectors. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, industrial activity, and technology adoption trends.

The report examines key technology developments including active vibration control, AI-enabled monitoring, predictive maintenance integration, MEMS-based sensing, and intelligent isolation platforms. More than 45% of advanced semiconductor installations now utilize enhanced vibration management technologies, while smart monitoring adoption continues expanding across industrial environments. Strategic insights include competitive positioning, technology benchmarking, investment priorities, partnership strategies, supply-chain developments, and operational performance trends shaping market direction between 2026 and 2033. The analysis supports expansion planning, product development, competitive intelligence, and long-term business decision-making.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 580.0 Million |

| Market Revenue (2033) | USD 917.5 Million |

| CAGR (2026–2033) | 5.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | TMC (Technical Manufacturing Corporation); Hutchinson SA; Fabreeka International, Inc.; Kinetic Systems, Inc.; Vibro/Dynamics Corporation; ACE Controls Inc.; GERB Schwingungsisolierungen GmbH & Co. KG; LORD Corporation; Farrat Ltd.; Isotech, Inc.; Bilz Vibration Technology AG; Trelleborg Industrial Solutions; Karman Rubber Company; Isolation Technology Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |