Reports

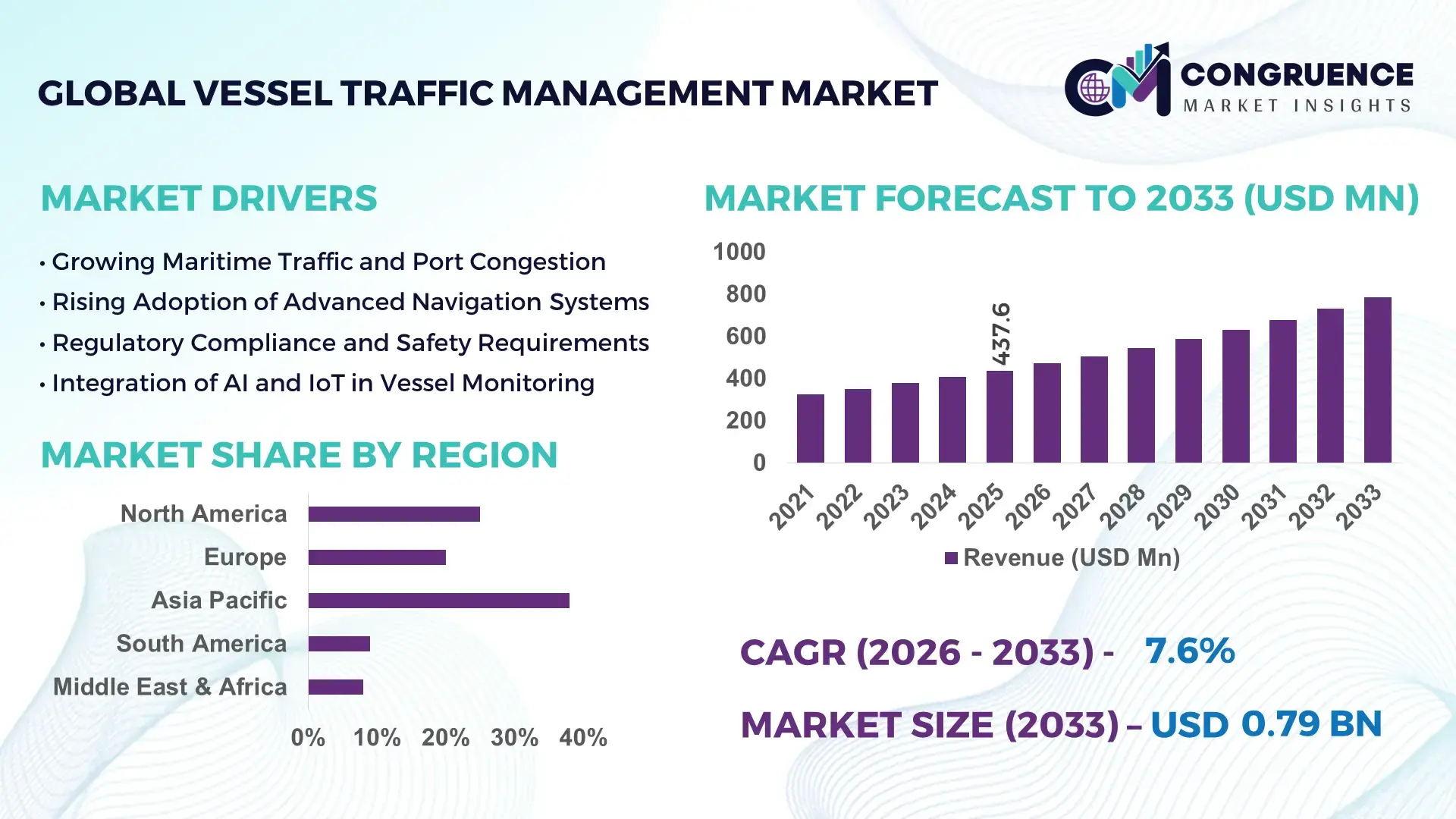

The Global Vessel Traffic Management Market was valued at USD 437.63 Million in 2025 and is anticipated to reach a value of USD 786.34 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033. Growth is supported by rising maritime trade volumes and accelerated digitalization of port operations.

China represents the most active national environment for vessel traffic management deployment. The country operates over 140 commercial ports and manages more than 36,000 km of navigable coastline supported by nationwide AIS coverage. Public and port authority investments in smart ports exceeded USD 9 billion between 2021 and 2024, enabling large-scale VTM integration with radar, satellite, and 5G systems. Applications span container ports, inland waterways, LNG terminals, and offshore energy corridors, with over 70% of tier-1 ports using integrated traffic control platforms. Adoption of AI-assisted collision avoidance and real-time data fusion has reduced average vessel waiting time by approximately 18% across major hubs.

Market Size & Growth: USD 437.63M (2025) to USD 786.34M (2033), CAGR 7.6%, driven by port automation and maritime safety mandates

Top Growth Drivers: Port digitization (+42%), AIS integration (+38%), maritime safety compliance (+31%)

Short-Term Forecast: By 2028, average vessel turnaround time reduced by ~15%

Emerging Technologies: AI-based traffic prediction, satellite-AIS fusion, cloud-native VTM platforms

Regional Leaders: Asia-Pacific USD 312M, Europe USD 214M, North America USD 176M by 2033; Asia-Pacific leads in smart port rollouts

Consumer/End-User Trends: Port authorities and coast guards increasing centralized, multi-port control adoption

Pilot or Case Example: 2024 smart harbor pilot achieved 22% reduction in near-miss incidents

Competitive Landscape: Market leader ~22% share; followed by four global marine electronics and defense technology providers

Regulatory & ESG Impact: Stricter navigation safety rules and emissions monitoring integration accelerating adoption

Investment & Funding Patterns: Over USD 1.4B invested since 2022 in port digitization and VTM upgrades

Innovation & Future Outlook: Integration with autonomous vessels and national maritime data platforms

The vessel traffic management market serves commercial ports, naval and coast guard operations, offshore energy zones, and inland waterways, with ports contributing roughly half of total system demand. Recent innovations include AI-driven anomaly detection, digital twins for traffic simulation, and integration with environmental monitoring systems. Regulatory pressure for navigational safety, decarbonization reporting, and coastal security continues to shape procurement priorities. Consumption growth is strongest in Asia-Pacific and Northern Europe due to dense port networks and modernization programs, while emerging economies are adopting modular VTM solutions. Future outlook centers on autonomous shipping readiness, cross-border traffic data sharing, and predictive traffic orchestration.

The Vessel Traffic Management Market holds growing strategic relevance as global maritime corridors experience sustained increases in vessel density, port congestion, and regulatory oversight. Modern vessel traffic management systems are now positioned as core infrastructure for national logistics resilience, coastal security, and port efficiency. AI-enabled traffic optimization delivers approximately 28% improvement in incident prediction accuracy compared to conventional radar-only traffic control standards. Asia-Pacific dominates in traffic volume due to high container throughput, while Europe leads in adoption, with nearly 62% of major ports operating fully integrated digital vessel traffic management platforms.

Strategically, port authorities and maritime agencies are prioritizing data-driven navigation control to reduce collision risk, improve berth utilization, and comply with international safety frameworks. By 2028, AI-based predictive traffic analytics are expected to improve average vessel scheduling efficiency by nearly 20%, directly lowering congestion-related delays. Environmental compliance is also shaping strategy, with firms committing to ESG performance improvements such as 30% reduction in navigational emissions exposure and digital reporting by 2030.

A measurable micro-scenario illustrates this shift: in 2024, a national port authority in Northern Europe achieved a 17% reduction in vessel waiting time through deployment of AI-assisted route optimization and centralized traffic coordination. Looking forward, the Vessel Traffic Management Market is evolving into a foundational pillar supporting resilient trade flows, regulatory compliance, and sustainable maritime growth through intelligent, interoperable, and environmentally aligned traffic control frameworks.

Rising global maritime traffic is a primary driver of the Vessel Traffic Management market, as commercial shipping lanes experience sustained increases in vessel movements. Major ports now handle over 20% more vessel calls compared to pre-2020 levels, increasing navigational complexity and collision risk. Vessel Traffic Management platforms enable centralized monitoring, traffic sequencing, and incident prevention across congested waterways. Deployment of integrated systems has demonstrated up to 25% improvement in traffic flow efficiency and measurable reductions in near-miss incidents. Inland waterways and offshore wind installation zones further expand demand, as coordinated vessel movements become essential for safety and operational continuity across mixed-use maritime environments.

High upfront costs associated with Vessel Traffic Management system deployment act as a restraint, particularly for small and mid-sized ports. Advanced installations require investment in radar networks, sensors, communication infrastructure, and software integration with existing port systems. In developing regions, modernization budgets are constrained, delaying adoption despite operational need. Integration challenges with legacy navigation tools can extend deployment timelines by 12–18 months, increasing total project costs. Additionally, ongoing expenses related to system maintenance, cybersecurity, and skilled operator training further limit adoption in cost-sensitive markets.

Smart port development presents significant opportunities for the Vessel Traffic Management market as ports transition toward fully digital, automated operations. Integration with berth management, cargo scheduling, and environmental monitoring systems allows Vessel Traffic Management platforms to expand beyond safety into operational optimization. AI-enabled traffic forecasting and digital twin simulations are being adopted to support port expansion planning and autonomous vessel readiness. Emerging economies investing in greenfield ports and inland waterway logistics represent untapped demand, where modular and cloud-based Vessel Traffic Management solutions can be deployed rapidly with lower infrastructure requirements.

Cybersecurity and data governance challenges increasingly affect the Vessel Traffic Management market as systems become more interconnected and cloud-enabled. Vessel Traffic Management platforms handle sensitive navigational, cargo, and security data, making them targets for cyber intrusion. Inconsistent data standards across regions complicate system interoperability and cross-border traffic coordination. Compliance with national data sovereignty laws can restrict centralized data processing, increasing system complexity. Addressing these challenges requires continuous investment in cybersecurity frameworks, encryption protocols, and skilled personnel, adding operational burden for system operators and vendors.

• Rapid Shift Toward Modular and Scalable Vessel Traffic Management Architectures: The Vessel Traffic Management market is increasingly adopting modular and scalable system architectures to reduce deployment time and capital intensity. Around 55% of newly commissioned VTM projects between 2023 and 2025 reported cost efficiency gains through modular system design, where radar, AIS, communication, and analytics modules are deployed independently. This approach has shortened installation timelines by nearly 30% and reduced on-site integration labor by approximately 25%, particularly in Europe and North America, where port modernization schedules are tightly constrained.

• Integration of Artificial Intelligence for Predictive Traffic Control and Risk Reduction: AI-driven analytics are becoming central to Vessel Traffic Management platforms, with over 48% of upgraded systems now incorporating machine-learning-based traffic prediction. These solutions deliver up to 35% improvement in early collision-risk detection compared to rule-based systems. Ports using AI-assisted traffic sequencing have reported berth utilization improvements of nearly 18% and reductions in congestion-related vessel idling by 20%, supporting both operational efficiency and environmental performance objectives.

• Expansion of Satellite-AIS and Long-Range Surveillance Coverage: Satellite-based AIS integration is transforming monitoring capabilities beyond coastal radar limits. More than 60% of national maritime authorities now combine terrestrial and satellite-AIS data, expanding surveillance coverage by over 90% compared to shore-based systems alone. This trend is particularly pronounced along high-traffic international shipping lanes, where long-range vessel tracking has reduced unidentified vessel incidents by approximately 22% and improved response coordination times by nearly 15%.

• Growing Alignment with Environmental Monitoring and Compliance Requirements: Environmental integration is a defining trend in the Vessel Traffic Management market, with nearly 45% of new systems incorporating emissions tracking and environmental risk alerts. Ports using integrated VTM-environment dashboards have achieved up to 28% improvement in incident response related to oil spills and hazardous cargo navigation. By embedding sustainability metrics into traffic control, operators are supporting compliance targets while improving transparency and operational accountability across regulated waterways.

The Vessel Traffic Management market segmentation reflects the industry’s transition toward digital, integrated, and safety-centric maritime operations. Segmentation by type highlights the shift from conventional hardware-centric systems to software-driven and intelligence-enabled platforms. Application-based segmentation shows strong concentration in commercial port operations, alongside growing usage in coastal surveillance and inland waterways. End-user segmentation is dominated by port authorities and maritime administrations, while private terminal operators and offshore infrastructure developers are increasing adoption. Across segments, demand is shaped by vessel density, regulatory enforcement, digital readiness, and the need for real-time situational awareness. Adoption patterns indicate that advanced economies favor fully integrated solutions, while emerging regions prioritize scalable and modular deployments aligned with phased infrastructure development.

The Vessel Traffic Management market by type includes Information Service (INS), Traffic Organization Service (TOS), Navigational Assistance Service (NAS), and Integrated Vessel Traffic Management Systems. Integrated systems represent the leading type, accounting for approximately 46% of total adoption, as they combine surveillance, decision support, and communication into unified platforms. Their dominance is supported by measurable outcomes such as 20–30% reductions in vessel queuing and improved incident response coordination. Traffic Organization Service systems currently account for around 28% of deployments, widely used in high-density ports to manage vessel sequencing and traffic separation. However, Navigational Assistance Service systems are the fastest-growing type, expanding at an estimated 9.4% CAGR, driven by demand for real-time guidance in narrow channels, offshore wind zones, and LNG terminals. Information Service platforms, including data dissemination and reporting tools, hold niche relevance for compliance and analytics, with the remaining segments collectively contributing about 26% of installations.

By application, port and harbor management is the leading segment in the Vessel Traffic Management market, accounting for nearly 49% of total system usage. This dominance reflects the need to manage dense vessel movements, berth allocation, and safety enforcement within confined port waters. Coastal surveillance follows with approximately 27% adoption, supporting national security, fisheries monitoring, and environmental protection initiatives. Inland waterway management is the fastest-growing application, expanding at an estimated 8.7% CAGR, supported by logistics diversification and inland port development programs. These systems improve traffic predictability and reduce collision risk across rivers and canals experiencing mixed commercial and passenger traffic. Offshore applications, including energy installations and offshore construction zones, contribute the remaining 24%, serving specialized operational safety needs.

Port authorities and harbor masters form the leading end-user segment in the Vessel Traffic Management market, accounting for approximately 52% of total deployments. Their adoption is driven by regulatory mandates, congestion management requirements, and public safety responsibilities. Coast guards and maritime safety agencies follow with around 23% share, using VTM platforms for surveillance, incident response, and compliance enforcement. Private terminal operators represent the fastest-growing end-user group, expanding at an estimated 9.1% CAGR, as operators seek to optimize berth productivity and reduce operational disruptions. Offshore energy operators and inland waterway authorities collectively contribute about 25% of adoption, reflecting expanding use cases beyond traditional port environments. Adoption rates among large commercial ports exceed 65%, while mid-sized ports report adoption near 40%, indicating continued expansion potential.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Asia-Pacific dominance is supported by high vessel traffic density, with more than 60,000 commercial vessel movements per month across major ports. Europe’s accelerated growth outlook reflects aggressive port digitalization mandates, where over 65% of tier-1 ports have committed to full Vessel Traffic Management upgrades by 2030. North America held approximately 24% market share in 2025, driven by modernization of coastal surveillance and inland waterway systems. The Middle East & Africa accounted for nearly 9%, supported by oil & gas maritime corridors, while South America contributed about 7%, reflecting selective investments in port safety and trade facilitation infrastructure. Regional differences in regulatory enforcement, port automation maturity, and maritime security priorities continue to shape demand patterns globally.

The North America Vessel Traffic Management Market accounted for approximately 24% of global adoption in 2025, supported by extensive commercial port networks and inland waterways. Demand is driven by container ports, energy terminals, and coast guard operations, with more than 70% of major ports operating centralized traffic control centers. Government-backed maritime safety programs and stricter navigation compliance requirements are accelerating upgrades of radar, AIS, and AI-enabled analytics platforms. Digital transformation trends include cloud-based control rooms and predictive traffic modeling, with nearly 45% of newly deployed systems integrating AI modules. A regional marine technology provider expanded its VTM platform in 2024 to support multi-port operations, delivering a 15% improvement in traffic coordination efficiency. Regional behavior shows higher enterprise adoption in logistics, energy, and defense-related maritime operations, prioritizing reliability and cybersecurity.

Europe represented close to 22% market share in 2025, with strong adoption across Germany, the UK, France, and the Nordic countries. Regulatory bodies emphasize navigational safety, emissions monitoring, and cross-border data interoperability, driving demand for advanced Vessel Traffic Management solutions. Over 60% of European ports have implemented or announced upgrades integrating AI-based decision support and environmental monitoring. Sustainability initiatives linked to maritime emissions reporting are influencing procurement, with integrated VTM-environment dashboards gaining traction. A European maritime systems supplier deployed traffic optimization solutions across multiple ports, achieving a 20% reduction in congestion-related delays. Consumer behavior in this region reflects regulatory pressure, with demand focused on explainable, auditable, and standards-compliant Vessel Traffic Management platforms.

Asia-Pacific is the largest regional market by volume, accounting for approximately 38% of global installations. China, India, and Japan are the top consuming countries, collectively handling over 50% of global container throughput. Infrastructure expansion, smart port initiatives, and coastal surveillance programs are key growth enablers. More than 75% of newly built large ports in the region include Vessel Traffic Management systems as standard infrastructure. Regional innovation hubs are advancing AI-assisted collision avoidance and 5G-enabled maritime communications. A major Asian port authority implemented an integrated VTM platform in 2024, reducing average vessel waiting time by 18%. Regional behavior shows adoption driven by high trade volumes, rapid infrastructure buildout, and increasing reliance on digital coordination tools.

South America accounted for roughly 7% of the global Vessel Traffic Management market in 2025, with Brazil and Argentina as key contributors. Demand is closely tied to port modernization, agricultural exports, and energy shipment corridors. Infrastructure upgrades focus on high-traffic ports, where Vessel Traffic Management systems have reduced navigational incidents by approximately 14%. Government trade facilitation policies and port concession models are supporting gradual system deployment. A regional port operator introduced centralized traffic monitoring in 2023, improving berth coordination efficiency by 12%. Consumer behavior reflects targeted adoption, with emphasis on safety and operational continuity rather than full-scale automation.

The Middle East & Africa held about 9% market share in 2025, supported by oil & gas shipping lanes, strategic canals, and port expansion projects. The UAE and South Africa are major growth countries, investing in smart port and coastal surveillance initiatives. Over 40% of new port projects in the Gulf region include advanced Vessel Traffic Management systems. Technological modernization includes long-range radar integration and satellite-AIS coverage. A regional port authority deployed a multi-sensor VTM platform in 2024, achieving a 16% improvement in incident response time. Regional consumer behavior emphasizes reliability, security, and integration with energy logistics.

China – 21% market share: High port density, extensive coastline coverage, and large-scale smart port investments driving Vessel Traffic Management adoption

United States – 17% market share: Strong regulatory enforcement, advanced coastal surveillance needs, and widespread modernization of port and inland waterway traffic control systems

The Vessel Traffic Management market exhibits a moderately consolidated structure, characterized by a mix of established marine technology providers and specialized navigation system developers. More than 30 active commercial competitors operate globally, addressing diverse port sizes, coastal surveillance needs, and inland waterway requirements. The top five companies collectively account for approximately 55–58% of total system deployments, reflecting strong positioning in large-scale port authority contracts and national maritime programs. Competitive differentiation is driven by system integration depth, AI-enabled analytics, cybersecurity readiness, and interoperability with port community systems.

Strategic initiatives are increasingly centered on long-term framework agreements, public–private partnerships, and multi-port rollouts rather than single-site deployments. Between 2023 and 2025, over 40% of competitive wins involved bundled solutions combining radar, AIS, AI analytics, and cloud-based control platforms. Product innovation remains intense, with nearly 60% of leading vendors introducing AI-assisted traffic prediction, satellite-AIS fusion, or digital twin simulation capabilities. Mergers and acquisitions remain selective, accounting for less than 10% of competitive expansion, while partnerships with telecom and satellite operators have increased by 25% to enhance coverage and data reliability. Overall, competition is shifting toward lifecycle service value, scalability, and compliance-driven differentiation.

Kongsberg Gruppen

Saab AB

Thales Group

Leonardo S.p.A.

Indra Sistemas

Wärtsilä

Japan Radio Co., Ltd.

Lockheed Martin

Frequentis

The Vessel Traffic Management market is undergoing a substantial technological transformation driven by integration, intelligence, and interoperability. Traditional radar and AIS (Automatic Identification System) infrastructures remain foundational, but their capabilities are being rapidly extended through data fusion architectures. Today, more than 65% of deployed systems feature combined radar, AIS, and long-range satellite tracking, expanding situational awareness coverage by up to 90% compared to radar-only systems. This trend enables maritime authorities to monitor vessel movements far beyond coastal limits and supports critical response coordination across extensive sea lanes. A defining technology trend in this market is the adoption of artificial intelligence and machine learning for predictive traffic analytics and risk assessment. AI modules embedded within Vessel Traffic Management platforms can process historical and real-time datasets, delivering up to 35% improvement in early collision risk identification relative to rule-based methods. These systems also support automated anomaly detection, reducing false alerts and enabling operators to prioritize critical events with precision.

Cloud-native deployment models and edge computing are reshaping platform architectures. North American and European ports report that over 40% of new installations leverage hybrid cloud infrastructure to facilitate remote operations, data redundancy, and multi-agency collaboration. Edge computing at key sensor nodes drives lower latency for critical decision support, particularly in high-density harbors where milliseconds matter. Another key innovation is the integration of digital twin technologies, allowing simulation of traffic flows and scenario testing. Digital twin environments can model complex scenarios involving mixed conventional and autonomous vessels, with measurable benefits such as traffic delay reduction of near-term schedule disruptions by over 20% in trial environments. Enhanced cybersecurity frameworks are also central; more than 50% of advanced Vessel Traffic Management systems incorporate encrypted communications, multi-factor authentication, and continuous threat monitoring to counter rising maritime cyber risks.

Finally, interoperability standards and open APIs are gaining prominence, enabling Vessel Traffic Management systems to connect seamlessly with port community systems, environmental monitoring networks, and national secure communication infrastructures. This interoperability not only supports regulatory compliance but fosters ecosystem expansion, unlocking new operational efficiencies and strategic value for adopters.

• In April 2024, Kongsberg Norcontrol was selected by the Maritime and Port Authority of Singapore (MPA) to develop an AI-enabled Next Generation Vessel Traffic Management System prototype that integrates advanced analytics and hotspot identification tools to manage growing maritime traffic complexity efficiently in one of the world’s busiest routes. (Kongsberg)

• In September 2024, Wärtsilä Corporation secured the prototyping tender for Singapore’s Next-Generation Vessel Traffic Management System (NGVTMS) project, initiating collaboration at a maritime innovation lab to build open-architecture traffic solutions with machine learning for collision prediction. (Wärtsilä)

• In March 2025, Thales Group installed its AI-enhanced Vessel Traffic Management System across 14 major European ports, significantly improving operational coordination efficiency and data processing capacity for integrated port operations.

• In 2025, a major Asia-Pacific port operator received an advanced dual-AIS and radar-integrated Vessel Traffic Management solution from a leading global technology provider, aligning with the region’s dominant deployment volume and enhancing long-range monitoring accuracy.

The Vessel Traffic Management Market Report provides a comprehensive framework for understanding deployment, segmentation, regional dynamics, applications, and technology innovations shaping global maritime traffic oversight. It covers detailed system classifications, including Vessel Traffic Services (VTS), Port Management Information Systems (PMIS), Aids to Navigation (AtoN) Management Systems, and River Information Systems (RIS), with insights into how each segment contributes to operational safety and coordination across commercial and defense environments. The report also examines key components such as surveillance hardware, integrated software platforms, and advanced analytical services, demonstrating the role of digital integration in enhancing situational awareness and decision support.

Geographic regions analyzed include North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with market-level breakdowns illustrating installation density, regulatory drivers, and infrastructure readiness. Applications span port and harbor operations, coastal monitoring, inland waterways, and offshore energy zones, reflecting diversified use cases for Vessel Traffic Management platforms. Technology focus areas include AI-enabled predictive traffic analytics, long-range satellite-AIS integration, cloud-native control architectures, digital twin simulations, and cybersecurity enhancements tailored to maritime traffic systems. Emerging subsegments such as autonomous vessel traffic integration and environmental monitoring align with smart maritime initiatives.

The report also explores strategic industry focus areas—such as interoperability standards, data-sharing protocols, and public–private modernization partnerships—to illuminate future pathways for investment and innovation. Detailed vendor profiling, competitive benchmarking, and real-world deployment case studies offer decision-makers clarity on adoption trends, performance outcomes, and long-term transformation priorities within the global Vessel Traffic Management ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kongsberg Gruppen, Saab AB, Thales Group, Leonardo S.p.A., Indra Sistemas, Wärtsilä, Japan Radio Co., Ltd., Lockheed Martin, Frequentis |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |